US Market Open: Stocks lower and DXY flat in quiet trade into a number of earnings

22 Jul 2025, 11:00 by Newsquawk Desk

- White House Press Secretary Leavitt said they could see more tariff letters for August 1st.

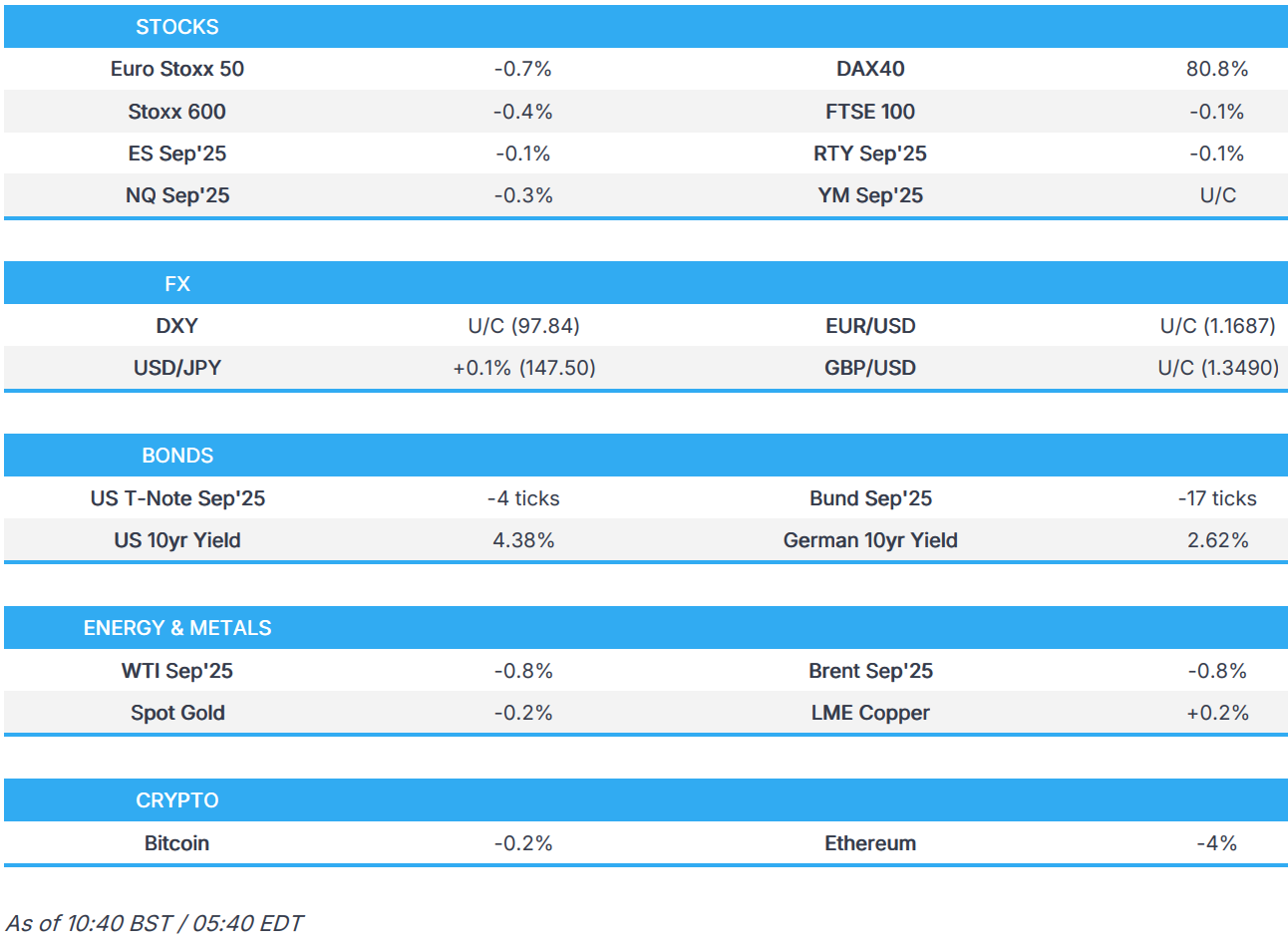

- European bourses are in the red and currently trade at session troughs, US equity futures also incrementally lower.

- DXY is flat awaiting fresh catalysts, whilst Antipodeans lag given the risk-tone.

- JGBs react to the election, bonds elsewhere have a bearish bias, Gilts lag.

- Crude moves in lockstep with risk while base metals remain cushioned.

- Looking ahead, US Richmond Fed Index, NBH Policy Announcement, Speakers including Fed Chair Powell & Bowman, ECB’s Lagarde. Earnings from SAP, Intuitive, Capital One, Baker Hughes, Coca Cola, Lockheed Martin, Philip Morris, RTX, DR Horton, Northrop Gruman, Danaher, MSCI & Pulte.

TARIFFS/TRADE

- Canadian PM Carney issued a statement following a meeting with US Senators and stated they discussed work to strengthen continental defence and security, as well as Canada’s successes in dismantling illegal drug smuggling and securing the border.

- Canada's Minister of Intergovernmental Affairs Leblanc will be in Washington this week for trade discussions.

- Japan's tariff negotiator Akazawa and US Commerce Secretary Lutnick met for over two hours in Washington on Monday and held frank talks to seek agreement benefiting both Japan and the US, while Japan will continue to seek common ground on tariff issues with the US, according to the Japanese government.

- South Korean Finance Minister Koo said he will hold trade talks with his US counterpart on July 25th, while Koo added that the Foreign Minister and Industry Minister will conduct meetings with US counterparts as soon as possible.

- India and US mini trade deal is ruled out before August 1st, according to CNBC TV18, citing sources.

- India-US trade deal prospects are dim ahead of the August 1st deadline, sides remain deadlocked over ags and dairy products, according to Reuters sources.

- Malaysia has been asked by the US to extend tax exemptions for US EVs, while Malaysia is seeking a 20% US levy, but is said to be resisting EV and ownership demands, according to Bloomberg.

- "Chinese experts warned that if the US attempts to weaponize trade talks and tariffs...Beijing will not yield to the pressure. Such moves would also risk undermining the trade negotiation mechanism between the two countries", via Global Times.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.4%) opened mostly lower and sentiment continued to deteriorate as the session progressed. Downside, which followed a mixed APAC session, where indices failed to sustain early upward momentum.

- European sectors hold a slight negative bias, with only a handful of industries managing to stay afloat. Utilities takes the top spot, joined closely by Basic Resources and then Travel & Leisure to complete the top three. Chemicals sits at the foot of the pile, with two of the top 10 industry constituents reporting today; Givaudan reported weak sales and Akzo Nobel missed across its headline figures, alongside a cut to its FY Adj. EBITDA view.

- US equity futures are modestly lower in quiet trade; the NQ marginally underperforms following poor earnings from NXP Semiconductor. The docket is void of any pertinent Tier 1 data releases (Richmond Fed Index is due), but earnings will pick up to keep markets busy.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is flat after declining around 0.6% on Monday. There was no obvious fundamental catalyst for the pullback in the USD on Monday with some pinning the move on the flattening of the US curve and price action being exaggerated by summer trading conditions. The macro narrative since the start of the week is relatively unchanged, with trade deals between the US and global trading partners remaining elusive and the Fed in its blackout period. On the latter, both Powell and Bowman are due on the speaker slate today but are not expected to comment on monetary policy. DXY has failed to make its way back onto a 98 handle with a current session peak at 97.99.

- EUR is flat. Focus at the start of the week has been on the trade agenda with the EU reportedly looking at a wider set of potential countermeasures against the US in the event that a deal is not reached by August 1st. Note, if a deal is not reached by the deadline, the EU will be subject to a 30% tariff rate by the US. As August 1st draws closer and a deal is lacking, the EUR will likely embed a greater risk premium. EUR/USD currently trading around the 1.17 mark, session high at 1.1703.

- JPY is softer vs. the USD as Japanese participants return to market and digest the upper house election results, which saw the ruling majority lose its coalition. Today's losses appear to be more of a scaling back of Monday's upside vs. the USD rather than a reassessment of the outcome of the election.

- GBP is flat vs the Dollar. Today's main macro highlight from the UK has come via a worse-than-expected outturn for UK borrowing figures with Borrowing in June coming in at GBP 20.7bln vs. Exp. GBP 16.75bln; the second-highest June borrowing since monthly records began in 1993, after that of June 2020. BoE Governor Bailey is currently speaking with the Treasury Select Committee; nothing too pertinent thus far. Cable is back on a 1.34 handle and trades in a 1.3462-91 range.

- Antipodeans are both at the bottom of the G10 leaderboard alongside the current flimsy risk tone. Little follow-through was seen into AUD following the RBA minutes, which provided very little incrementally. The account noted that the majority agreed it was prudent to await confirmation on inflation slowdown before easing, although the Board agreed further rate cuts are warranted over time with focus on the timing and extent of easing.

- PBoC set USD/CNY mid-point at 7.1460 vs exp. 7.1635 (Prev. 7.1522).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs climbed higher overnight in reaction to Sunday’s Japanese Upper House election. At best, posted gains of 40 ticks to a 138.71 peak but ended the Japanese day off highs, though still markedly clear of the 138.31 open.

- USTs are in the red, but only marginally. In a thin 111-01+ to 111-06+ band as fresh catalysts are light and the US docket, ex-earnings, is limited on account of the Fed blackout. Note, a handful of Fed speakers due today incl. Chair Powell; however, remarks are not expected to be pertinent to monetary policy. Elsewhere, Richmond Fed Index is also due. If the current marginal pressure extends, Friday’s low resides at 110-21+, that week’s low at 110-10+, and the current WTD base at 110-08.

- Bunds are in-fitting with USTs. Softer in a 130.24 to 130.49 band. Specifics this morning have been light with no pertinent EU trade updates, data or speakers thus far; as is the case for the Fed, the ECB is currently in its quiet period, so while President Lagarde is scheduled today, she is not expected to provide any pertinent commentary. No reaction to this morning’s ECB Bank Lending Survey, where credit standards were broadly unchanged for firm loans in Q2, tightened slightly for households but more markedly for consumer credit. If the morning’s bearish bias extends, then the July 7th low stands at 130.02 before the figure and then numerous levels from the last two weeks between 129.73 and 129.02.

- Gilts are underperforming a touch, began the morning lower by 12 ticks in-fitting with the above modest bearish bias before slipping another 20 to a 91.46 base. While in the red by just over 30 ticks at worst, the benchmark remains clear of Monday’s 91.29 low and last week’s 91.08 trough. This morning’s underperformance is seemingly a function of the latest PSNB data. A series that showed borrowing in June was above market consensus and the second-highest June figure since records began; highest was in 2020, during COVID. A series that provides no relief for the Chancellor’s fiscal position and keeps the narrative for the Autumn Budget firmly towards tax increases. Elsewhere, BoE Governor Bailey is currently speaking with the Treasury Select Committee; nothing too pertinent thus far.

- UK sells GBP 1.7bln 1.125% 2035 I/L: b/c 3.35x (prev. 3.02x) & real yield 1.588% (prev. 1.386%).

- Germany sells EUR 0.422bln vs exp. EUR 0.5bln 2.30% 2033 Green and EUR 0.931bln vs exp EUR 1bln 2.50% 2035 Green Bund.

- Click for a detailed summary

COMMODITIES

- Subdued trade across the crude complex as prices move in tandem with broader sentiment, with just over a week left until US President Trump's August 1st tariff deadline, with little in the way of deals announced in recent days. WTI trades towards the bottom of a USD 65.07-65.86/bbl range while Brent resides in a USD 68.36-69.12/bbl parameter.

- Precious metals are taking a breather following Monday's rise and with macro newsflow rather light ahead of the August 1st tariff deadline, which also coincides with the US jobs report and the ISM Manufacturing PMI. Spot gold trades in a USD 3,344.90-3401.65/oz range after failing to sustain above USD 3,400/oz in APAC hours.

- Mostly but modestly subdued trade across base metals, although losses seem somewhat cushioned by the recent Chinese dam project, with iron ore prices overnight closing higher for a fifth consecutive session. 3M LME copper meanwhile trades flat in a notably narrow USD 9,827.70-9,883.00/t range at the time of writing.

- Coking coal prices overnight surged by 8%, hitting the daily limit. Some cited unverified market chatter that the Chinese National Energy Administration has reportedly issued a verification notice requiring all mines that have exceeded production capacity to suspend operations for rectification.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK PSNB, GBP (Jun) 20.684B GB vs. Exp. 16.75B GB (Prev. 17.686B GB, Rev. 17.440B GB)

- UK grocery inflation stood at 5.2% in the four weeks to July 13th, via Kantar.

NOTABLE EUROPEAN HEADLINES

- BoE Governor Bailey says they have seen steeper yield curves and it's a global phenomenon; UK experience is not out of line with other markets. The cause of the steeper yield curve reflects greater uncertainty on trade policy. The steeper yield curve also reflects global uncertainty on fiscal policy.

- UK Deputy PM Rayner is pushing for councils to be given new powers to tax tourists, despite opposition from Chancellor Reeves, according to The Telegraph.

- ECB July Bank Lending Survey: Corporate credit demand is weak but rose in Q2 and expected to rise further in Q3 Credit standards for firm loans remained broadly unchanged. Credit standards tightened slightly for housing loans and more markedly for consumer credit. Housing loan demand continued to increase strongly, while demand for firm loans remained weak. Trade war was a drag on demand but did not lead to a tightening in credit standards.

- UK FCA says "borrowers will find it easier to remortgage, saving time and money, under changes confirmed by the FCA". Under these changes, buyers will: Find it easier to reduce their mortgage term, helping to lower the total cost of borrowing and reduce the risk of repayment extending into retirement. More easily remortgage with a new lender, helping them access cheaper products. Be able to discuss options with their mortgage provider and get advice when they need it.

NOTABLE US HEADLINES

- US Treasury Secretary Bessent said the Fed should conduct an exhaustive internal review of non-monetary policy operations and its decision to undertake massive building renovation at a time of operating losses should be reviewed.

- SoftBank (9984 JT) and OpenAI's USD 500bln AI project struggles to get off the ground with the Stargate venture, introduced at a White House event earlier this year, now setting a more modest goal of building a small data centre by year-end, according to WSJ.

GEOPOLITICS

MIDDLE EAST

- Iran's Foreign Minister said Iran is open to talks with the US but not directly for now, while it was separately reported that Iran's Foreign Minister told Fox News they cannot give up Iranian enrichment.

- Iranian Foreign Minister reiterates that Iran will not give up uranium enrichment program, via IRNA.

- World Health Organisation's Tedros said WHO staff residence in Deir al Balah, Gaza, was attacked three times on Monday as well as its main warehouse, while he demanded the immediate release of the detained staff and protection of all its staff. Tedros said two WHO staff and two family members were detained although three were later released and one staff member remained in detention.

CRYPTO

- Bitcoin is a little lower and trades just above the USD 118k whilst Ethereum posts deeper losses to USD 3.6k.

APAC TRADE

- APAC stocks traded mixed after failing to sustain the early upward momentum seen at the open following the fresh record intraday highs on Wall St and with two-way price action seen in Japan following the ruling coalition's upper house election loss.

- ASX 200 was rangebound as strength in the mining, materials, resources and healthcare sectors offset the losses in financials, energy and industrials, while the RBA Minutes from the July meeting provided very little to shift the dial but continued to signal future cuts ahead.

- Nikkei 225 initially surged to above the 40,000 level as participants returned from the long weekend, but then wiped out its gains and then some, as participants second-guessed the ramifications of the ruling coalition's upper house election setback.

- Hang Seng and Shanghai Comp kept afloat in rangebound trade amid a lack of major fresh catalysts and after the Hong Kong benchmark breached the 25,000 level.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Kato said it was a tough upper house election result for the LDP and the government will take the outcome of the upper house elections seriously, while he added that the government has repeated that sales tax cuts are not appropriate.

- RBA Minutes from the July meeting stated the Board agreed further rate cuts are warranted over time, while the focus was on the timing and extent of easing. The Minutes stated that the Board considered whether to leave rates at 3.85% or to cut by 25bps and a majority agreed it was prudent to await confirmation on inflation slowdown before easing, while the majority felt cutting rates three times in four meetings would not be cautious and gradual. The case for no change cited some data as inflation had been slightly firmer than expected, the job market had also not loosened as expected and there was less risk of a severe global downturn. Furthermore, members agreed monetary policy was modestly restrictive, though financial conditions had eased and it was difficult to know how far rates can fall before policy is no longer restrictive, so prudence is needed.

- BoJ is likely to leave its benchmark rate unchanged next week, according to Bloomberg sources; sees little impact from election on rate stance; watching for trade talk impact before any hikes; sees upward price risks if there is large fiscal loosening.

- China's Forex Regulator says overseas investors in general net increased their onshore equity and bond holdings in Q2; supply and demand in the FX market is "basically stable"; Yuan has been basically stable at reasonable and balanced levels this year.

- PBoC Shanghai Head Office says foreign holdings of yuan-denominated bonds traded on China's interbank market totalled CNY 4.23tln at the end of June.