US Market Open: Sentiment boosted on US/Japan deal; autos outperform awaiting EU deal

23 Jul 2025, 11:20 by Newsquawk Desk

- US President Trump announced trade deals with the Philippines, Indonesia and Japan, with the latter involving a USD 550bln investment in the US and 15% tariffs for Japanese goods.

- Japanese PM Ishiba is likely to announce resignation as early as this month, according to Yomiuri – reports which he later pushed back on.

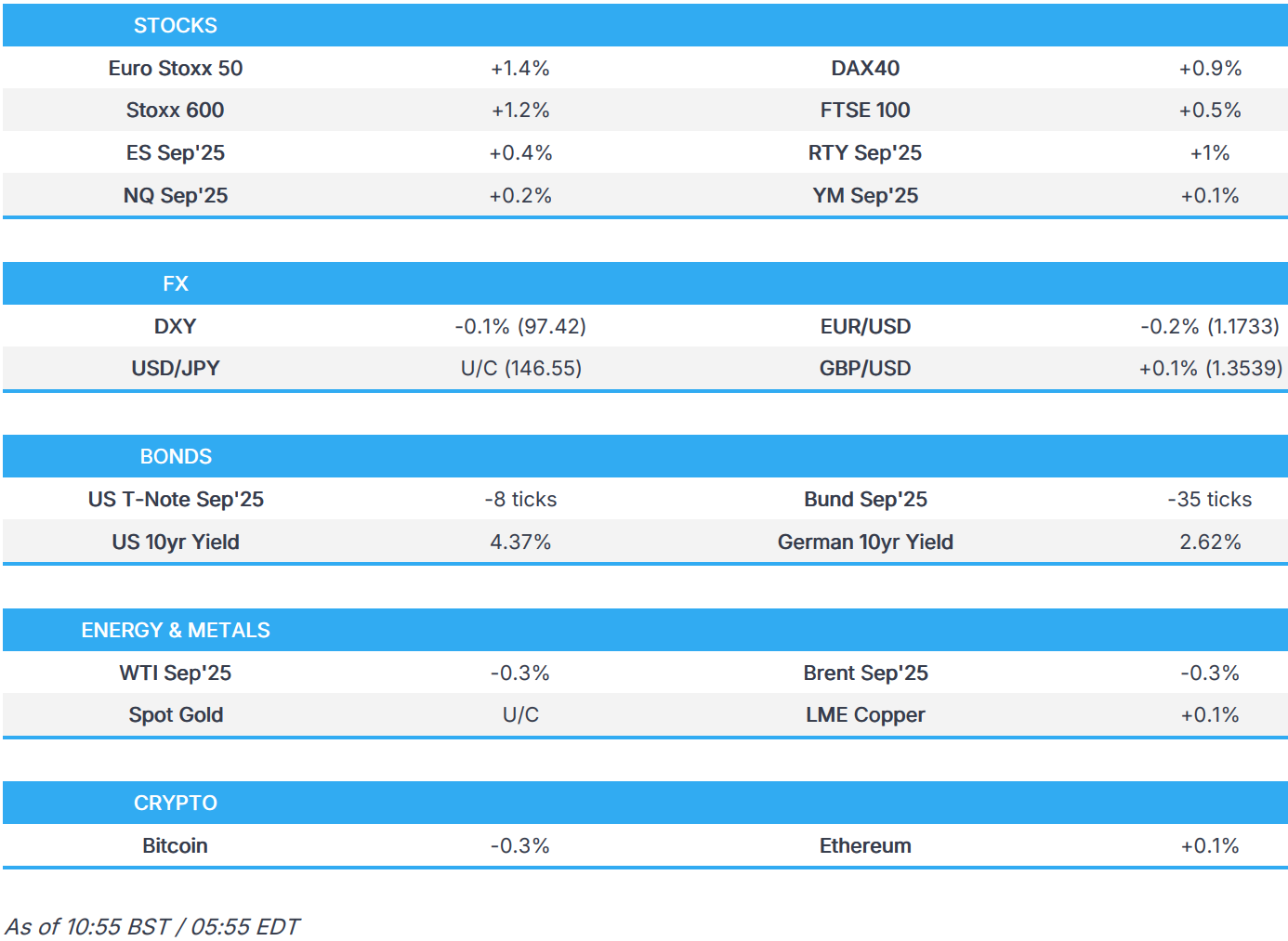

- European bourses benefit from the US-Japan trade deal; RTY continues to outperform.

- USD is flat, Antipodeans are the G10 outperformers whilst the EUR lags a touch; JPY choppy on US-Japan trade deal and reports surrounding PM Ishiba.

- JGBs slump on trade updates, peers elsewhere lower given the risk tone and into supply.

- Crude complex choppy awaiting fresh catalysts, XAU takes a breather following recent upside.

- Looking ahead, US Existing Home Sales, Supply from the US. Earnings from Tesla, Alphabet, ServiceNow, IBM, Chipotle, GE Vernova, Freeport, AT&T, Thermo Fisher Scientific, Lamb Weston, Infosys, Moody's, CME & Hilton.

TARIFFS/TRADE

JAPAN

- US President Trump announced that they completed a massive deal with Japan, which he said is perhaps the largest deal ever made with Japan to invest USD 550bln into the US and will open their country to trade including cars and trucks, rice and certain other agricultural products, and other things. Trump added that Japan will pay reciprocal tariffs to the US of 15% and is forming a JV with the US in Alaska and they are going to make a deal on LNG.

- Japan's top trade negotiator Akazawa said they were able to reach an agreement that is beneficial to both countries and struck a deal with the US after a 70-minute meeting with President Trump, while he added that steel and aluminium are not included in the tariff deal.

- Japanese PM Ishiba confirmed they agreed with the US to lower tariffs with auto tariffs lowered to 15% and will continue working closely with the US. Ishiba said the deal does not include lowering tariffs on Japan's agricultural products, while Japan will raise the portion of rice imports from the US within the minimum access framework.

- BoJ Deputy Governor Uchida says US-Japan trade agreement is a big progress and will reduce uncertainty over Japan's economic outlook; will reflect trade agreement in economic outlook report; uncertainty remains on tariff impact. There is always upside and downside risks to the outlook. Japan trade deal roughly falls in line with assumptions BoJ made in projections at prior quarterly report on May 1st; at present, must support the economy through accommodative monetary policy.

OTHER

- US President Trump said Europe is coming to Washington for trade talks on Wednesday.

- US President Trump said we are going to get drug prices down and drug companies will have a lot of problems if they don't agree, while he added that they will use import restrictions to force foreign suppliers to cut drug prices.

- China's Commerce Minister held a video call with the EU's trade chief and had candid and in-depth discussions, while they discussed China and EU trade cooperation and issues, as well as EU sanctions on Chinese firms and China lodged solemn representations over sanctions.

- US President Trump will meet UK PM Starmer during his weekend trip and they will seek to formalise a trade deal.

- Brazilian Finance Ministry official Durigan said they have been working on a plan to protect themselves from potential 50% taxation by the US, and the work has not been completed, while they have tried to do everything possible to reverse the 50% tariff by the US and have been looking at the possible need to help Brazilian companies due to US tariffs which will be done with the least possible fiscal impact.

- Chinese Commerce Ministry confirms Chinese Vice Premier He Lifeng is to hold talks with the US; VP is to visit Sweden between July 27-30th.

- Germany and France are to push the EU prepare trade retaliation against the US, unless it makes compromises. (FT)

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +1.2%) opened firmer across the board, and continued to trade higher throughout the morning - currently at session highs.

- European sectors hold a very strong positive bias, with only a couple of sectors residing in negative territory. Autos tops the pile and is currently the clear outperformer, largely benefiting from trade optimism after Japan finally struck a deal with US - optimism which stems from traders factoring in the potential benefits European automakers now have on pricing over Japanese autos. Consumer Products also benefit from the broader risk tone.

- US equity futures (ES +0.4% NQ +0.2% RTY +1%) are modestly firmer across the board with some outperformance in the RTY, which builds on the strength seen in the prior session. The price action on Tuesday was characterised by outflows from favoured sectors (such as Tech), into recent underperformers (such as Value stocks).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is flat with the USD showing a mixed performance vs. peers (softer vs. antipodes, firmer vs. havens). Incremental macro drivers for the US remain on the light side with price action for the USD in recent sessions led by the retreat in US yields. Over the past 24 hours, the US has struck trade deals with Japan (see JPY section for details), Indonesia and the Philippines. These agreements have reduced fears surrounding the August 1st deadline. Albeit, deals with its two largest trading partners, the EU and China, are yet to be reached. DXY sits towards the bottom end of yesterday's 97.30-99 range.

- EUR is a touch weaker vs. the USD with macro drivers lacking. Trade headlines regarding the EU and US remain on the light side following weekend reports that the EU is looking at a wider set of potential countermeasures against the US if a deal is not reached by August 1st. EUR/USD trades towards the top end of yesterday's 1.1679-1.1760 range.

- JPY is a touch softer vs. the USD alongside an encouraging risk tone, which has been buoyed by news of the US-Japan trade agreement. The deal will see Japanese goods subject to a 15% tariff (including autos, which had been threatened by a 25% rate). Additionally, Japan will invest USD 550bln into the US and is expected to sign an LNG deal with the US. The deal has notably bolstered Japanese equities with Auto names leading the charge. However, the FX reaction is more muted. One driver behind this is the ongoing fallout from Sunday's Upper House election. Reports in Japanese press suggest that PM Ishiba is set to announce his resignation - something, which he has since refuted. USD/JPY sits towards the middle of its current 146.21-147.21 range.

- GBP is marginally firmer vs. the USD with UK-specific newsflow on the light side. Cable is trading higher for its third session in a row, however, this appears to be more of a USD story, than a GBP one. That could change tomorrow with flash PMI metrics for July due on deck. Expectations for marginal upticks in the services and manufacturing components. Elsewhere, retail sales data is due on Friday. Cable has extended its run on a 1.35 handle and breached its 50DMA at 1.3523. Next upside target comes via the 11th July high at 1.3585.

- Antipodeans are both sit at the top of the G10 leaderboard following the upbeat risk sentiment seen in the wake of the US-Japan trade deal. Newsflow out of Australia and New Zealand remains light. AUD/USD has gained a firmer footing on a 0.65 handle with a current session high at 0.6581.

- PBoC set USD/CNY mid-point at 7.1414 vs exp. 7.1596 (Prev. 7.1460)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- An eventful session for Japan. Firstly, US President Trump announced that a trade deal has been agreed and will result in a 15% tariff level (full details on the feed). An update that supported the JPY and weighed on JGBs with yields picking up across the Japanese curve with the short-end leading and the 10yr making a marginal new post-2008 peak at 1.601%; surpassing 1.60% from the week before the Upper House election. Amidst this, reports emerged from various outlets that PM Ishiba was, despite his initial post-election commitment, planning to announce his resignation in either July or August and take personal responsibility for the Upper House result. The trade update weighed on JGBs from 138.50 to 138.00 at the resumption of trade before slipping further to a 137.56 low in the hours after as the reports around Ishiba circulated. Thereafter, a slight pickup from lows occurred - but this proved short-lived with session lows hitting after a weak 40yr auction.

- USTs are in the red, holding at a 111-04 low with downside just shy of 10 ticks at most. Newsflow has been focussed almost entirely on trade as Trump announced deals with Japan, Indonesia and the Philippines. Furthermore, China’s Commerce Ministry has confirmed talks with the US next week in Sweden. Pressure seen across the fixed income benchmarks, with JGBs leading as above, amid the positive risk tone and prospect for more trade updates today (see Bunds). The mentioned trough holds just before the 111-00 mark, if breached the 21st July base is next at 110-24 before 110-19 from July 18th and then a double-bottom at 110-08+.

- Bunds are under pressure, to a slightly larger extent than USTs. Downside that is perhaps ahead of EUR 5bln 2035 Bund tap into Thursday’s ECB (no move expected, focus on commentary/guidance) and the language from Trump overnight. China's Commerce Minister held a video call with the EU's trade chief and had candid and in-depth discussions, while they discussed China and EU trade cooperation and issues, as well as EU sanctions on Chinese firms and China lodged solemn representations over sanctions. Altogether, Bunds down to a 130.33 low with downside of c. 50 ticks at most but yet to test Tuesday’s 130.24 base or by extension the WTD low at 129.73 from Monday.

- Gilts echo the above with downside of around 50 ticks at most. Specifics for the UK have been light with the benchmark largely just following the risk tone. While in the red, Gilts remains above Tuesday’s 91.46 base and by extension the 91.29 WTD trough from Monday. Bearish action ahead of a GBP 3bln 2040 Gilt auction due. Results of this were strong, with a b/c of 3.69x and a more typical tail, sparking upside in Gilts of around 10 ticks from the 91.58 low.

- UK sells GBP 3bln 4.375% 2040 Gilt: b/c 3.69x (prev. 2.88x), tail 0.1bps (prev. 1.0bps), average yield 5.066% (prev. 4.850%).

- Germany sells EUR 3.832bln vs exp. EUR 5bln 2.60% 2035 Bund: b/c 1.5x (prev. 1.6x), average yield 2.62% (prev. 2.63%), retention 23.36% (prev. 24.05%)

- Click for a detailed summary

COMMODITIES

- Choppy price action in contained ranges for the crude complex, ultimately holding a mild negative bias whilst newsflow remains rather light. This follows the Tuesday weakness seen in prices as tariff woes linger ahead of the August 1st deadline. Sticking with trade, the EU and US are yet to move forward on a deal, whilst the Chinese Commerce Ministry confirmed that Chinese Vice Premier is to hold talks with the US next week.

- Mixed/flat trade across precious metals amid a lack of fresh catalysts during the European session as traders await potential further trade updates in the run-up to next Friday's US-set deadline.

- Mixed trade across base metals with the risk tone also somewhat tentative, awaiting the next catalysts. 3M LME copper trades in a narrow USD 9,870.05-9,932.80/t range at the time of writing.

- US Private Inventory Data (bbls): Crude -0.6mln (exp. -1.6mln), Distillates +3.5mln (exp. -1.1mln), Gasoline -1.2mln (exp. -0.9mln), Cushing +0.3mln.

- Brazilian miner Vale reported Q2 iron ore output at 83.6mln tons (prev. 67.7mln tons Q/Q), iron sales 77.3mln tons (prev. 66.1mln tons Q/Q).

- Contamination issue with Azeri BTC oil has reportedly been resolved; Loadings continue from the Turkish port of Ceyhan, according to Reuters sources.

- Azeri central bank sees 2025 average oil price as USD 68.60/bbl and USD 299/100 cubic metres.

- Click for a detailed summary

NOTABLE EUROPEAN HEADLINES

- European Commission President von der Leyen says EU/Japan "Competitiveness Alliance" will: Increase trade, strengthen economic security with robust rare earth supply chains and accelerate innovation.

GEOPOLITICS

MIDDLE EAST

- Israel's Defence Minister said there is a possibility of a renewed campaign against Iran.

- US Special Envoy Witkoff will travel to Europe this week for meetings on issues including Gaza and will continue pushing for a Gaza ceasefire.

- US is to mediate the Israel-Syria meeting on Thursday to avoid new crises, according to Axios.

- US President Trump's administration has informed Hamas and Israel that it would like to see an end to the conflict, via Al Arabiya.

- On Israel-Lebanon, US envoy Barrack says "There are problems preventing the full implementation of the ceasefire agreement", according to Sky News Arabia.

- "Al-Arabiya sources: Hezbollah's military wing informs [Lebanon's Speaker of the Parliament] Berri that it will not surrender weapons", via Al Arabiya.

RUSSIA-UKRAINE

- US Energy Secretary Wright told Fox News that sanctioning Russian oil is a very real possibility.

CRYPTO

- Bitcoin is a little lower and trades just around USD 118k whilst Ethereum holds around flat at USD 3.6k.

APAC TRADE

- APAC stocks were mostly higher as focus centred on the latest trade developments after US President Trump announced three trade deals in one day with the Philippines, Indonesia and Japan, with the latter involving a USD 550bln investment in the US and 15% tariffs for Japanese goods.

- ASX 200 gained with the advances led by strength in materials, miners, energy and resources, while defensives are at the other end of the spectrum.

- Nikkei 225 surged above 41,000 following the announcement of a US-Japan trade deal involving a 15% tariff on Japanese goods including autos and auto parts which is less than the previous threat of 25% tariffs and in turn, boosted automakers which dominated the list of biggest gainers with several up by double-digit percentages, while there were also tailwinds as the JPY slightly softened in the aftermath of a report that PM Ishiba is to announce his resignation by the end of August.

- Hang Seng and Shanghai Comp conformed to the mostly positive risk tone with US President Trump noting that there will probably be a meeting with Chinese President Xi in the not-too-distant future, while US Treasury Secretary Bessent said they will likely work out an extension regarding the August 12th deadline with China and he will attend talks next Monday and Tuesday with China in Stockholm.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Ishiba is to resign with the PM to announce his resignation by the end of August, according to Mainichi newspaper. It was separately reported that Japanese PM Ishiba is likely to announce resignation as early as this month, according to Yomiuri.

- Japanese PM Ishiba says he met with former PM Kishida overnight, shared a strong sense of crisis, resignation was not discussed with them.

- Japanese PM Ishiba says absolutely no truth to reports about his resignation.

- BoJ Deputy Governor Uchida said Japan's economy has recovered moderately although some weakness has been seen in part and noted that Japan's economic growth is likely to moderate due to the effects of trade and other policies. Uchida said uncertainty surrounding trade policies remains extremely high and it is important to maintain loose monetary policy to support the economy. Furthermore, he said interest rates are expected to be raised in accordance with economic and price improvements if the scenario is realised and he will judge whether the economy and prices move in line with the forecast without any pre-set idea.

- Thereafter, BoJ Deputy Governor Uchida says at present, BoJ must support the economy through accommodative monetary policy. US-Japan trade deal roughly falls in line with assumptions BoJ made in projections at prior quarterly report on May 1.