US Market Open: European stocks bid on EU trade reports, GOOGL +3%, TSLA -6% post-earnings; ECB due

24 Jul 2025, 11:10 by Newsquawk Desk

- US President Trump said they will have straight, simple tariffs of between 15% and 50% on countries, while he added the US is in serious talks with the EU and if they agree to open up to US businesses, US will let them pay lower tariffs.

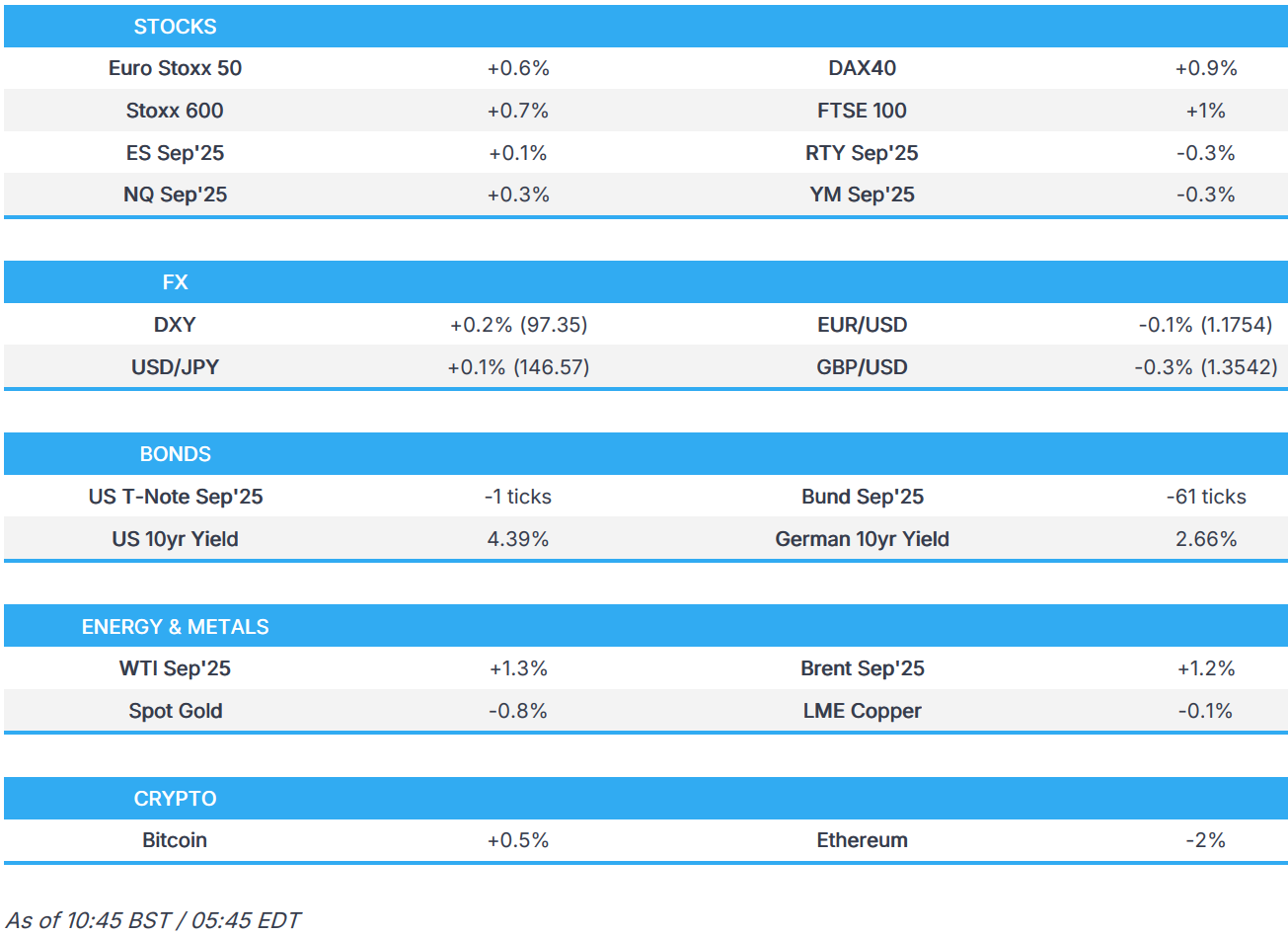

- European bourses continue to gain, albeit are off best levels; US futures mixed, GOOGL +3%, TSLA -6% in pre-market trade.

- GBP lags on soft PMIs, EUR eyes ECB and potential EU-US breakthrough.

- EGBs hit by trade updates, Gilts off lows post-PMIs, USTs await data.

- Crude rises on trade optimism and geopolitics, gold unwinds risk premium.

- Looking ahead, Global PMIs, US Jobless Claims, Canadian Retail Sales, ECB & CBRT Policy Announcements, Speakers including RBNZ’s Conway & ECB President Lagarde, Supply from the US.

- Earnings from LVMH, Carrefour, Michelin, Intel, American Airlines, Blackstone, Dow Chemical, Nasdaq, Union Pacific, Honeywell & Keurig Dr Pepper.

TARIFFS/TRADE

- EU diplomats say that members have supported potential tariffs on EUR 93bln of US goods

- US President Trump said they will have straight, simple tariffs of between 15% and 50% on countries, while he added the US is in serious talks with the EU and if they agree to open up to US businesses, US will let them pay lower tariffs. Trump said they will be charging straight tariffs to most of the rest of the world and are in the process of completing a deal with China, while they are making deals with various Asian countries on energy and made a deal with the EU but it was related to military equipment.

- White House said on reports of an EU trade deal, that discussions about a possible deal should be considered speculation.

- South Korea's Finance Ministry said the 2 + 2 trade talks with the US were cancelled due to the US Treasury Secretary's schedule, while the US proposed talks in the immediate future and the sides will set the time for another round of talks ASAP. Furthermore, it stated that South Korea's trade envoy is to still meet with his US counterpart during his trip, while there were separate reports that the US and South Korea have discussed creating a fund to invest in American projects as part of a trade deal and South Korea is to invest more than USD 100bln as part of a US trade deal, according to Yonhap.

- Japan's Tariff negotiator Akazawa says there is no difference in understanding between Japan and the US on the trade deal; had no discussion with US President or US officials on how to implement the deal.

- Indonesia Chief Economy Minister says its possible that Indonesia's key commodities could get a lower tariff than 19% or even close to 0%.

- Indonesian Economy Minister says Indonesia has asked the US for lower tariffs on goods produced in the free trade zone.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) opened stronger across the board, with positive trade developments continuing to boost sentiment. However, as the morning progressed, indices have dipped off earlier highs but still reside firmer across the board. Sentiment boosted today thanks to an FT report which suggested that the US and the EU were closing in on a trade deal with a 15% tariff rate, albeit this is yet to be officially confirmed.

- European sectors hold a strong positive bias, with the industry compilation today largely dictated by post-earning movers. Optimised Personal Care tops the pile, largely driven by Reckitt which soars after the Co. reported a Q2 sales beat, lifted its annual guidance and plans a GBP 1bln share buyback. Banks take second spot, lifted by post-earning strength in Deutsche Bank and BNP Paribas. Food Beverage and Tobacco underperforms alongside Real Estate today; the former has been pressured by heavyweight Nestle, after its results. (details all below).

- US equity futures (ES +0.1%, NQ +0.3%, RTY -0.3%) are mixed. Tech heavy NQ outperforms with the likes of Google (+3%) and ServiceNow (+7%) boosting the index after earnings, whilst Tesla (-6%) slips after its results.

- Walmart (WMT) is to overhaul its AI agent strategy, via WSJ; to consolidate its agents into four 'super agents' to simplify the user experience. Co. intends to announce this on Thursday.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

EARNINGS

-

Alphabet Inc (GOOGL) Q2 2025 (USD): EPS 2.31 (exp. 2.16), Revenue 96.43bln (exp. 93.85bln), Cloud Revenue 13.624bln (exp. 13.14bln), Ad revenue 71.34bln (exp. 69.64bln), Search revenue 54.19bln, FY Capex view about USD 85bln (prev. 75bln, exp. 73.31bln);Shares +3% in pre-market traade

- IBM (IBM) Q2 2025 (USD): EPS 2.80 (exp. 2.65), Revenue 16.98bln (exp. 16.58bln);Shares -5% in pre-market traade

- Tesla (TSLA) Q2 2025 (USD): Adj. EPS 0.40 (exp. 0.41), Revenue 22.5bln (exp. 22.09bln); CEO Musk warned of "rough times".Shares -6% in pre-market traade

- Roche (ROG SW) H1 2025 (CHF): Beat, Q2 beat, Confirms guide. Shares +1%

- Nestle (NESN SW) H1 2025 (CHF): Revenue miss, guidance confirmed despite factoring in increased headwinds. Shares -3%

- TotalEnergies (TTE FP) Q2 2025 (USD): Miss, lower adj. net income from business segments in Q2, primarily due to lower oil and gas prices. Shares -1.6%

- Reckitt (RKT LN) H1 2025 (GBP): Revenue 6.981bln (exp. 7.026bln); raised guidance and announced buyback. Shares +10%

FX

- DXY is a touch higher after a run of four consecutive daily losses. Yesterday's downside was largely due to the appreciation of the JPY in the wake of the US-Japan trade deal. ING has made the observation that "The dollar didn’t suffer in the first half of July from trade tensions re-escalating. And it is equally finding no benefit from positive trade deal news". Noise around the Trump administration's disdain for the current direction of FOMC policy will likely pick up today with the President set to visit the Fed at 21:00BST. DXY has delved as low as 97.10 with focus on a test of 97.00; not breached since 7th July (96.89 was the low that day).

- EUR is a touch softer vs. the USD with the recent rally pausing for breath. This week has seen optimism increase on the trade front with reporting via Reuters and the FT suggesting that the US and EU are closing in on a 15% tariff deal, which would waive tariffs on some products. Elsewhere, flash EZ PMI metrics for July showed minor improvements and beats on expectations for the manufacturing, services and composite metrics. The accompanying report said the data was indicative of "robust" economic growth for Q3 and a continuation of the disinflation trend. That being said, the release is unlikely to have any sway on the upcoming ECB rate decision with markets fully priced for an unchanged rate as the GC views current policy as well-positioned.

- JPY is mildly extending on its recent run of gains vs. the USD with the Yen buoyed after securing a trade deal with the US, which will see Japanese goods subject to a 15% tariff (including autos). Additionally, Japan will invest USD 550bln into the US and is expected to sign an LNG deal with the US. Accordingly, markets have continued to bolster bets on BoJ tightening this year with 22bps of hikes seen by year-end vs. circa 14bps at the start of the week. USD/JPY has briefly made its way onto a 145 handle with a session low at 145.86; lowest since July 10th.

- GBP is struggling and sits at the bottom of the G10 leaderboard in the wake of disappointing flash PMI metrics for July. The services metric unexpectedly declined to 51.2 from 52.8, manufacturing nudged higher to 48.2 from 47.7 with the composite coming in at 51.0 vs. previous 52.0. The accompanying release was a gloomy one with S&P Global noting the data showed "output growth weakened to a pace indicative of the economy growing at a mere 0.1% quarterly rate, with risks tilted to the downside in the coming months". Cable has slipped to a low of 1.3547 but is holding above its 50DMA at 1.3529 and yesterday's low at 1.3515.

- Antipodeans both remain buoyed by the encouraging risk tone in the absence of any antipodean-specific drivers. As such, both will likely take direction from the trade environment in the short-term.

- PBoC set USD/CNY mid-point at 7.1385 vs exp. 7.1503 (Prev. 7.1414).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Bunds are under pressure into the ECB. Weighed on by the constructive updates on the EU-US trade front. As reports noted that the US and the EU were closing in on a trade deal with a 15% tariff rate, albeit this is yet to be officially confirmed, and White House Trade Adviser Navarro said to take it with a pinch of salt. Bunds find themselves lower by 87 ticks at most to a 129.71 base, notching a marginal new WTD trough. As for PMIs, the French and German figures were mixed vs consensus while the EZ figure beat and came in above the prior for all metrics. Attention now turns to the ECB, where rates are expected to be kept steady.

- USTs are also in the red, but to a much lesser extent. Directionally in-fitting with EGBs but holding around the 111-00 mark after a brief blip to a 110-28+ low in the European morning. In contrast to Bunds, the current low is clear of Monday’s 110-24 WTD base. Trade aside, the Fed remains in focus as Trump himself will be visiting the Fed this evening. Currently, it is unclear if he will be meeting with Chair Powell or not during this visit. Docket ahead will include US Jobless Claims, PMIs and the US 2, 5, 7, 2yr FRN Refunding Announcement.

- Gilts opened lower by 26 ticks given the risk tone and pressure in Bunds at the time. Thereafter, it extended to a 92.29 trough ahead of its own PMI data. Metrics which were mixed vs expectations but featured a sizeable miss in Services at 51.2 (exp. 53, prev. 52.8) coming in outside of the forecast range. Internal commentary was also downbeat, S&P calculating output growth is indicative of just 0.1% quarterly growth and risks are tilted to the downside in the coming months. In reaction to the series, a move higher from 91.43 to a 91.57 peak occurred just after the series, given the mixed/weak headlines.

- Italy sells EUR 2.75bln vs exp. EUR 2.25-2.75bln 2.10% 2027 BTP & EUR 1.5bln vs exp. EUR 1.25-1.5bln 1.10% 2031 I/L.

- Click for a detailed summary

COMMODITIES

- Firmer trade across the crude complex with a bulk of this morning's price action commencing just before 07:00 BST as European traders entered the fray, to the trade optimism felt across markets following the US-Japan deals alongside unofficial reports of an EU-US deal, although US officials suggested taking these reports with a pinch of salt. The price action also coincided with commentary from US envoy Barrack, who said Lebanon's failure to disarm Hezbollah means that the Israeli raids will continue. WTI resides closer to the upper end of a USD 65.37-66.24/bbl range, while Brent sits in a USD 68.61-69.45/bbl range.

- Precious metals are lower across the board amid the outflow of havens on trade optimism, with a similar performance seen across the bond market. Spot gold resides in a USD 3,366-3,393.48/oz range at the time of writing.

- Base metals are flat/mixed despite the broader risk appetite as traders gear up for trade deals ahead of next Friday's deadline, with the EU and US on watch, whilst officials from Washington and Beijing also gear up for a meeting next week, in Sweden. Furthermore, markets are also on the lookout for details regarding the US copper tariff. 3M LME copper resides in a USD 9,923.05-9,969.00/t range.

- China June YTD gold output fell 0.3% Y/Y to 179.083 metric tons and China June YTD gold consumption fell 3.54% Y/Y to 505 metric tons. according to the China Gold Association.

- Click for a detailed summary

NOTABLE DATA RECAP

PMIs

- EU HCOB Composite Flash PMI (Jul) 51.0 vs. Exp. 50.8 (Prev. 50.6); Manufacturing Flash PMI (Jul) 49.8 vs. Exp. 49.7 (Prev. 49.5); Services Flash PMI (Jul) 51.2 vs. Exp. 50.7 (Prev. 50.5)

- French HCOB Composite Flash PMI (Jul) 49.6 vs. Exp. 49.3 (Prev. 49.2); French HCOB Services Flash PMI (Jul) 49.7 vs. Exp. 49.6 (Prev. 49.6); HCOB Manufacturing Flash PMI (Jul) 48.4 vs. Exp. 48.5 (Prev. 48.1)

- German HCOB Services Flash PMI (Jul) 50.1 vs. Exp. 50.0 (Prev. 49.7); HCOB Manufacturing Flash PMI (Jul) 49.2 vs. Exp. 49.5 (Prev. 49.0); Composite Flash PMI (Jul) 50.3 vs. Exp. 50.7 (Prev. 50.4)

- UK Flash Services PMI (Jul) 51.2 vs. Exp. 53.0 (Prev. 52.8); Flash Composite PMI (Jul) 51.0 vs. Exp. 51.8 (Prev. 52.0); Manufacturing PMI (Jul) 48.2 vs. Exp. 48.0 (Prev. 47.7)

Other

- German GfK Consumer Sentiment (Aug) -21.5 vs. Exp. -19.2 (Prev. -20.3)

- French Business Climate Mfg (Jul) 96.0 vs. Exp. 96.0 (Prev. 96.0, Rev. 97)

NOTABLE US HEADLINES

- US President Trump signed AI executive orders to fast-track big projects and to turn America into an AI export powerhouse.

- US President Trump was told by the DoJ in May that his name is among many in the Epstein files, according to WSJ.

- White House official told Reuters on Wednesday that the administration was not denying that President Trump's name appears in the files.

- US Treasury Secretary Bessent a new Fed Chairman nominee is likely to be announced in December or January.

- White House said US President Trump will visit the Federal Reserve on Thursday at 16:00EDT/21:00BST.

- BofA Institute Total Card Spending (w/e July 19th): +1.8% Y/Y (vs. +0.2% June avg.); despite base effect from Prime Day (AMZN) timing change, spending growth was solid.

GEOPOLITICS

- North Korea leader Kim supervises artillery firing, according to KCNA

- US Envoy Barrack says Lebanon's failure to disarm Hezbollah means that the Israeli raids will continue; " There is no open deadline for disarming Hezbollah and the one who decides the duration of this period is Israel, not the United States". Elsewhere, "The likelihood that Iran will not conclude a deal with the United States is "very small", according to Sky News Arabia.

- Israeli officials say "At present, it is not possible to determine whether Hamas new response is indeed improved or allows for progress. Consultations will be held in the coming hours.", via Jerusalem Post's Stein; follows, PM Netanyahu says they are examining the Hamas response to the Gaza ceasefire proposal.

- Russia's Kremlin says did not expect a breakthrough from talks with Ukraine, according to Tass.

- Russia's Kremlin says it is hard to see how President Putin and Ukrainian President Zelensky could meet before the end of August.

- Thailand acting PM says Cambodia has fired heavy weapons into Thailand without specific targets, civilians have been killed; there has been no declaration of war; conflict has not spread to more provinces.

CRYPTO

- Bitcoin is on a slightly firmer footing today, trading just above USD 118k; Ethereum a little lower and trades above USD 3.6k.

APAC TRADE

- APAC stocks mostly extended on gains following the positive handover from Wall St and as recent trade developments continued to underpin risk sentiment.

- ASX 200 lacked conviction and lagged behind regional peers with heavy losses seen in gold miners after a drop in the precious metal, while participants also digested several quarterly production updates.

- Nikkei 225 continued its rally and briefly breached the 42,000 level to the upside as the euphoria from the US-Japan trade agreement lingered and with the electrical equipment manufacturers leading the advances, although the index has since pulled back from today's best levels.

- Hang Seng and Shanghai Comp were higher with little fresh catalysts to derail the recent positive momentum and following some optimistic comments from US Treasury Secretary Bessent ahead of next week's US-China talks in Sweden in which he stated that they are in a very good place with China right now and are back on track with China negotiations, while he also seemingly suggested they could do a rolling 90-day deadline when asked about the tariff deadline with China.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi said China and the EU are at another critical historic juncture and should enhance communication, increase mutual trust and deepen cooperation, while China and EU leaders should demonstrate vision and responsibility, as well as make correct strategic choices that meet the expectations of the people.

- EU's von der Leyen said rebalancing bilateral relations is essential and they have reached an inflection point, while she added it is vital for China and Europe to acknowledge respective concerns and come forward with real solutions. President von der Leyen said as cooperation has deepened, so have imbalances and noted that the China–EU relationship is one of the most important and consequential in the world.

- European Council President Costa said to Chinese President Xi that they need concrete progress on issues related to trade and the economy.

- US Commerce Secretary Lutnick said regarding the TikTok sale that he thinks a deal will happen and America will buy it.

- US lawmakers subpoenaed JPMorgan (JPM) and Bank of America (BAC) over the IPO of a Chinese battery startup, while the House committee had previously urged banks to stop work on CATL’s initial public offering, according to WSJ.

- PBoC Statement: China to support stable development of industries such as hogs, beef cattle, dairy cattle, sheep, and aquatic products.