US Market Open: European bourses pressured, USD bid & US equity futures mixed into Durable Goods

25 Jul 2025, 10:55 by Newsquawk Desk

- US President Trump said he spoke with Fed Chair Powell on rates and the meeting was productive, while he noted that there was no tension and he repeated several times that he believes Powell will do the right thing.

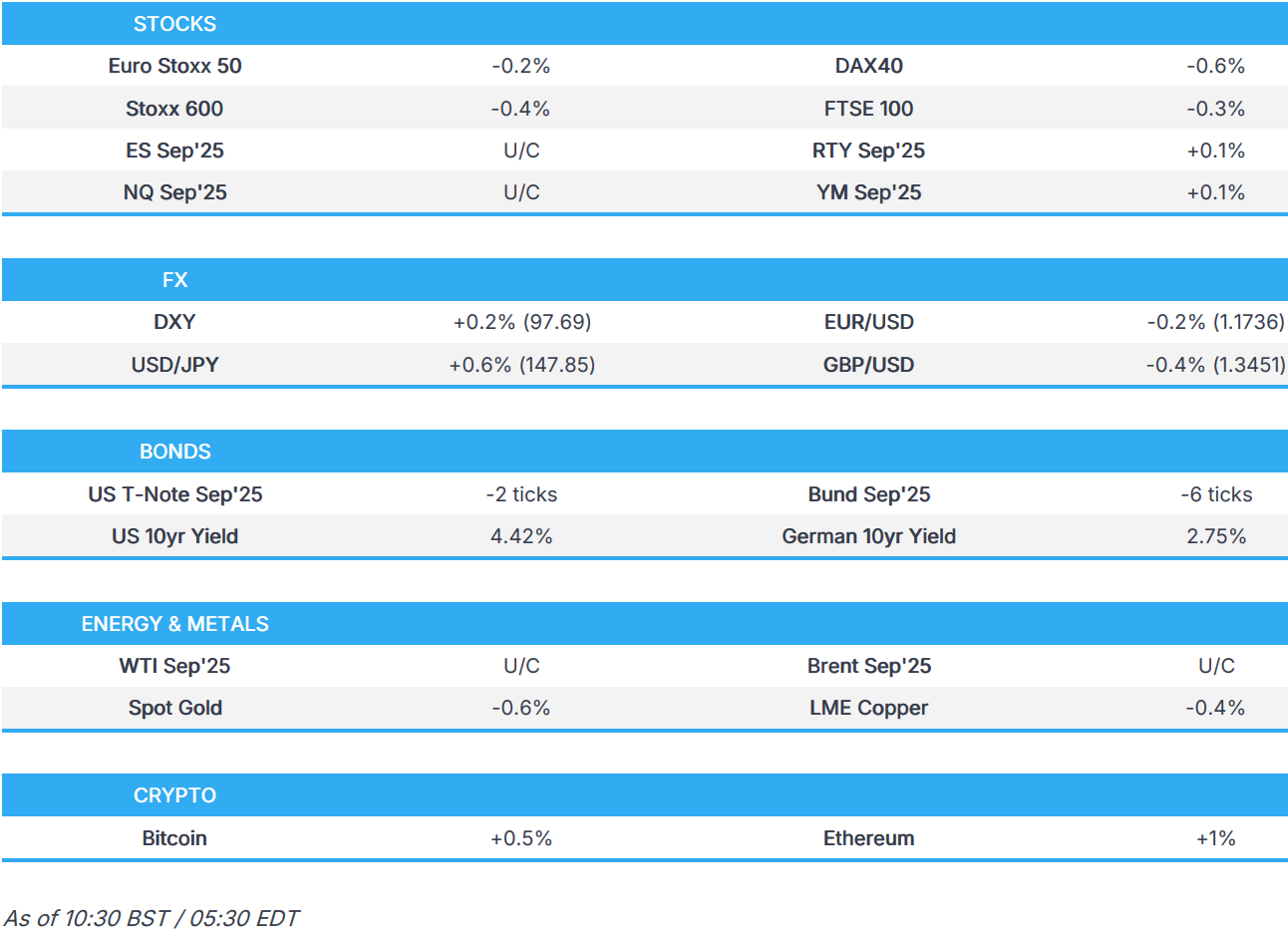

- European bourses are under pressure but off worst levels, LVMH +4% post-earnings; US futures trade mixed around the unchanged mark.

- DXY is a touch higher, JPY lags, GBP digests retail sales miss.

- USTs essentially flat, Bunds weighed on by continued ECB repricing.

- Gold loses its shine while Crude remains rangebound awaiting the next catalyst.

- Looking ahead, US Durable Goods, Atlanta Fed GDPNow. Earnings from AutoNation & AON.

TARIFFS/TRADE

- US Treasury Secretary Bessent said the US is in a pretty good place with China on trade and he will talk to China about them buying sanctioned oil from Russia and Iran, while Bessent separately commented that he met with Singapore's Trade Minister.

- UK PM Starmer is to press US President Trump over a deal to cut tariffs on UK steel imports, according to FT.

- India’s Commerce Minister said he was optimistic that India could reach an agreement with the US ahead of the August 1st deadline and he had some wonderful engagement with his “friend and colleague from the US”. Furthermore, he said they are making fantastic progress with the US on a trade deal and hopes they'll be able to conclude a "very consequential partnership".

- Chinese Foreign Ministry says China is willing to import more marketable high-quality European products; says EU should relax restrictions on exports of high-tech products to China.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.4%) opened lower across the board, continuing the downbeat mood seen in the APAC session. Downside which extended in the morning, but more recently a slight bounce has been seen across a few major indices such as the Euro Stoxx 50 and STOXX 600.

- European sectors hold a strong negative bias, with only a couple of industries holding afloat. Autos were initially the underperformer, but then flicked into the green as Volkswagen (+4%) pared initial losses, as traders fully digested the results and CEO commentary. Though its not all good for the sector, with Traton firmly in the red after it slashed its 2025 outlook amid US tariff uncertainty. LVMH (+4.5%) also bounced off lows seen at the open, to currently trade higher - the Co. reported a deeper than expected sales decline but its commentary on China was a little more upbeat.

- US equity futures (ES U/C NQ U/C RTY +0.1%) are mixed but ultimately trading on either side of the unchanged mark; the RTY is back on a firmer footing today, and incrementally outperforms after a session of losses in the prior session.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

EARNINGS

- Volkswagen (VOW3 GY) - Headline metrics missed and cut guidance. Q2 (EUR): Revenue 80.8bln (exp. 82.19bln), -3% Y/Y. Op. Margin 4-5% (prev. guided 5.5-6.5%)

- Puma (PUM GY) - Co. cut its FY outlook, and now expects a loss in adj. EBIT terms, citing weak demand and tariff concerns.

- NatWest (NWG LN) - Strong NII and NII. Raises FY Income guidance and starts a GBP 750mln share buyback programme.

FX

- DXY is a touch higher, in an extension of yesterday's upside, which was brought about by upside in US yields in the wake of weekly claims and PMI metrics. That being said, DXY is still down by the best part of 1% on the week alongside the flattening of the US yield curve and a pick-up in the JPY earlier in the week. Focus today will be on US Durable Goods and Atlanta Fed GDPNow. DXY briefly eclipsed yesterday's best at 97.55 before topping out at 97.63.

- EUR remains more resilient than peers vs. the USD in the wake of Thursday's "hawkish" ECB policy announcement. To recap, the GC stood pat on policy as expected given the current uncertainties surrounding the trade outlook. The greatest source of traction came after Lagarde reiterated that policy remains in a good place, suggesting that policymakers are not in a rush to adjust policy. Elsewhere, German IFO metrics came in a touch below expected but failed to engineer any traction in EUR. EUR/USD remains within Thursday's 1.1731-88 range.

- JPY is continuing to give back some of its gains vs. the USD seen earlier in the week on account of the US-Japan trade deal. Today's price action has been aided by softer-than-expected Tokyo CPI data, which showed the headline and core readings retreated beneath the 3% level for the first time since March. Attention is now pivoting to next week's BoJ policy announcement, which is widely-expected to see policymakers stand pat on rates. Source reporting today via Bloomberg noted that the BoJ sees a potential rate hike environment this year and expects to have enough data by end-2025 to consider a move.

- GBP is pressured vs. the USD in the wake of softer-than-expected June retail sales metrics. M/M retail sales printed at 0.9% vs. Exp. 1.2% (prev. -2.8%), Y/Y came in at 1.7% vs. Exp. 1.8% (prev. -1.1%). Nonetheless, GBP was sent lower vs. both the USD and EUR with markets despondent regarding the current UK macro environment, which is one characterised by slowing growth, a loosening labour market and stubborn inflation. Cable has delved as low as 1.3460 but still holding comfortably above the weekly trough from Monday at 1.3402.

- Antipodeans are both softer vs. the USD alongside this morning's soft risk tone and a lack of pertinent antipode-specific drivers.

- Barclays month-end rebalancing: weak USD selling against all majors.

- PBoC set USD/CNY mid-point at 7.1419 vs exp. 7.1609 (Prev. 7.1385).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A softer start to the session for USTs. However, once again, the magnitude of price action is relatively modest for USTs at this point in time. Some focus on Trump's meeting with Fed Chair Powell, where the President called for cuts but said it is not necessary to fire him and doing so would be a big move. Attention now turns to US Durable goods & Atlanta Fed’s GDPNow tracker. Thus far, USTs are at the low-end of a 110-24+ to 110-31 band, entirely within Thursday’s 110-19+ to 111-02 parameter.

- Bunds are also in the red but under much more pressure than USTs. At most, lower by over 70 ticks to a 128.84 trough and a fresh low for the week. Overnight action was contained, in-fitting with peers, with selling emerging in the early-European morning, gradually at first but then intensifying into the cash equity open despite the weaker start there - no real driver for the move. As such, it appears the move is a continued repricing of the ECB after the meeting yesterday where Lagarde said they are in a good policy place. Since, source reports via Bloomberg and Reuters outline that the baseline for September is for rates to be maintained. No move to Ifo this morning, the series printed softer than forecast across the board.

- Gilts are softer, between USTs and Bunds in terms of magnitude. Lower by 20 ticks at most in a 91.32-55 band and entirely within Thursday’s 91.18-69 parameters. The only update of note so far has been Retail Sales, which saw a bounce in-line with the direction of analyst expectations, though disappointing the strong consensus view. Nonetheless, Pantheon Macro maintains their Q2 GDP growth view of 0.2% Q/Q.

- Click for a detailed summary

COMMODITIES

- WTI and Brent held an upward bias following Thursday's gains on the back of trade optimism, with desks pointing out that Chevron's resumption of operations in Venezuela overlooked against the backdrop of trade developments. More recently some pressure has been seen across the crude complex, to take WTI and Brent towards the unchanged mark. Today's session has been lacking on pertinent updates, still awaiting the readout of the Iran/E3 meeting. WTI resides in a USD 66.05-66.74/bbl range with its Brent counterpart in a USD 69.21-69.86/bbl range at the time of writing.

- Precious metals are lower despite the cautious risk tone but amid a firmer Dollar as assets are seemingly sold in favour of cash heading into the weekend. Spot gold dipped under yesterday's low (USD 3,351.46/oz) as it eyes the 50 DMA to the downside (USD 3,341.27/oz) as it trades in a USD 3,344.64-3,373.50/oz parameter.

- Mixed trade across base metals in line with the broader tentativeness across the markets amid a lack of fresh catalysts. 3M LME copper resides in a narrow USD 9,821.45-9,887.75/t range at the time of writing.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GfK Consumer Confidence (Jul) -19.0 vs. Exp. -20.0 (Prev. -18.0)

- UK Retail Sales MM (Jun) 0.9% vs. Exp. 1.2% (Prev. -2.7%, Rev. -2.8%); Ex-Fuel MM (Jun) 0.6% vs. Exp. 1.2% (Prev. -2.8%, Rev. -2.9%)

- UK Retail Sales YY (Jun) 1.7% vs. Exp. 1.8% (Prev. -1.3%, Rev. -1.1%); Ex-Fuel YY (Jun) 1.8% vs. Exp. 2.0% (Prev. -1.3%, Rev. -1.2%)

- EU Money-M3 Annual Growth (Jun) 3.3% vs. Exp. 3.7% (Prev. 3.9%); Loans to Non-Fin (Jun) 2.7% (Prev. 2.5%); Loans to Households (Jun) 2.2% (Prev. 2.0%)

- German Ifo Business Climate New (Jul) 88.6 vs. Exp. 89.0 (Prev. 88.4); Current Conditions New (Jul) 86.5 vs. Exp. 86.7 (Prev. 86.2); Expectations New (Jul) 90.7 vs. Exp. 91.1 (Prev. 90.7)

NOTABLE EUROPEAN HEADLINES

- UK and Australia are to sign a GBP 20bln nuclear-powered submarine deal, according to The Times.

- ECB's Villeroy says the increases in US tariffs and the extent of which is still uncertain, are not expected to cause inflation to rise, it is important to remain completely open about future monetary policy decisions.

- ECB's Rehn says ECB will base policy decisions on a meeting-specific assessment of the inflation outlook and the risks surrounding it.

- ECB's Kazaks says no urgent need to move rates and noted value holding rates at the current level.

- ECB's Rehn says ECB will base policy decisions on a meeting-specific assessment of the inflation outlook and the risks surrounding it.

- ECB Survey of Professional Forecasters (Q3): Headline inflation expectations revised down for 2025-26 but unchanged for 2027 and the longer term

- UK Chancellor Reeves is reportedly considering overruling the Supreme Court in the scenario that they uphold all of the appeal court ruling that customers could be entitled to billions in compensation, via Guardian citing sources.

NOTABLE US HEADLINES

- US President Trump said during his visit to the Federal Reserve in Washington that it is a tough construction job, while Trump and Powell briefly voiced disagreement over renovation figures and he reiterated that he wants Powell to lower interest rates. Trump later commented that he talked with Fed Chair Powell on rates and the meeting was productive, and noted that there was no tension, while he repeated several times that he believes Powell will do the right thing. Trump also said he has maybe three names in mind for Powell's replacement but stated it is not necessary to fire Powell which would be a big move.

- US President Trump posted "It was a Great Honor to tour the Renovation (and some new Construction!) of the Federal Reserve Building with Chairman Jerome Powell, Senator Tim Scott, and others. It’s got a long way to go, would have been much better if it were never started, but it is what it is and, hopefully, it will be finished ASAP. The cost overruns are substantial but, on the positive side, our Country is doing very well and can afford just about anything — Even the cost of this building! I’ll be watching and, hopefully, adding some expertise. As everyone knows, I renovated the Old Post Office on Pennsylvania Avenue, and it was a roaring SUCCESS. The total Construction cost was a small fraction of the Fed Building’s cost, and it is many times the size. With all of that being said, let’s just get it finished and, even more importantly, LOWER INTEREST RATES!"

- BofA weekly flow report notes USD 25.9bln into bonds, USD 13.7bln into cash, USD 5.8bln into stocks, USD 3.6bln into crypto, USD 1.6bln into gold.

GEOPOLITICS

MIDDLE EAST

- French President Macron announced that France will recognise a Palestinian state in September at the UN General Assembly.

- Israeli PM Netanyahu condemned French President Macron's decision to recognise a Palestinian state and stated that such a move rewards terror and risks creating another Iranian proxy. Furthermore, Israel's Defence Minister said Macron's announcement of his intention to recognise the Palestinian state is a disgrace and a surrender to terrorism, while they will not allow the establishment of a Palestinian entity that would harm their security and endanger their existence.

- US Secretary of State Rubio posted the US strongly rejects French President Macron's plan to recognise a Palestinian state.

- Israeli official told Reuters that Hamas’s response to ceasefire talks does not allow for progress without a concession by Hamas and Israel intends to continue talks.

- Israeli official said the Israeli delegation will return to Qatar only when there is a feasible prospect of finalising an agreement and Hamas's response does not allow for progress unless they show flexibility, while mediators were surprised by Israel's decision and stated that "It would have been better if they had stayed and closed a deal", according to Journalist Stein.

- Hamas said it is surprised by the remarks from US Envoy Witkoff over the group's position in ceasefire negotiations, while it added that mediators welcomed the group's constructive and positive stance in negotiations, and it is keen to continue Gaza ceasefire negotiations.

- Gaza ceasefire talks expected to continue next week following Israeli review of Hamas response, according to Al Qahera citing a source.

- European states are prepared to offer Iran an extension on a looming deadline to reimpose international sanctions, if it agrees to conditions, according to FT.

- Explosions were heard at a weapons depot in Yemen's Al-Anad military base.

- "[Iran Supreme Leader] Khamenei adviser: No country can stop the progress of Iran's nuclear program", via Sky News Arabia.

OTHER NEWS

- Thailand's acting PM said escalation and progression of military exchanges with Cambodia is moving towards war.

- Thailand's military said border clashes took place with Cambodia early on Friday in two Thai provinces and that Cambodian forces have conducted sustained bombardment with heavy weapons, field artillery and rocket systems, while Thai forces have responded with appropriate supportive fire and advised civilians to leave the conflict areas. Furthermore, Thailand's military condemned Cambodia's use of long-range weapons to target civilian areas and said Cambodia's barbaric acts have senselessly claimed lives and injured numerous innocent civilians.

- UK Foreign Ministry said it advises against all but essential travel to parts of Thailand.

- Ukraine President Zelensky says negotiating teams have discussed a leaders summit, movement towards a meeting in some form. Ukraine needs an additional USD 25bln/yr for drone production.

CRYPTO

- Bitcoin is on the backfoot and trades just above the USD 115k, cooling from recent highs above USD 120k.

APAC TRADE

- APAC stocks were lower after the mixed performance in the US and with light catalysts for markets outside of earnings.

- ASX 200 mildly retreated with the downside led by underperformance in key industries including mining, materials, resources and financials, while Whitehaven Coal failed to benefit despite posting higher quarterly output and sales.

- Nikkei 225 gave back some of this week's gains amid profit taking despite a weaker currency and mostly softer Tokyo CPI.

- Hang Seng and Shanghai Comp conformed to the downbeat mood but with the downside in the mainland cushioned after a firm PBoC liquidity effort which resulted in a net daily injection of around CNY 602bln via 7-day reverse repos, while participants await next week's US-China trade discussions in Sweden.

NOTABLE ASIA-PAC HEADLINES

- PBoC Deputy Governor Zou Lan wrote that the PBoC will promote the Treasury's role in cash and liquidity management, according to PBoC-backed Financial News.

- Japanese PM Ishiba held meetings with party leaders, although Japan's CDP leader Noda said PM Ishiba did not mention his future in talks with party leaders, while Japan Innovation Party co-Leader Maehara said he is not considering joining PM Ishiba's coalition.

- BoJ reportedly sees a potential rate hike environment this year, via Bloomberg citing sources; expects to have enough data by end-2025 to consider a move. No requirement to make a significant change to the outlook. US deal reduces uncertainty.

- China will implement proactive fiscal policy to promote economic recovery.

DATA RECAP

- Tokyo CPY YY (Jul) 2.9% vs Exp. 3.0% (Prev. 3.1%); Ex. Fresh Food YY (Jul) 2.9% vs Exp. 3.0% (Prev. 3.1%)

- Tokyo CPY Ex. Fresh Food & Energy YY (Jul) 3.1% vs Exp. 3.1% (Prev. 3.1%)

- Japanese Services PPI (Jun) 3.20% vs Exp. 3.20% (Prev. 3.30%)