US Market Open: Stocks firmer & USD continues to gain ahead of JOLTS, consumer confidence and earnings

29 Jul 2025, 11:20 by Newsquawk Desk

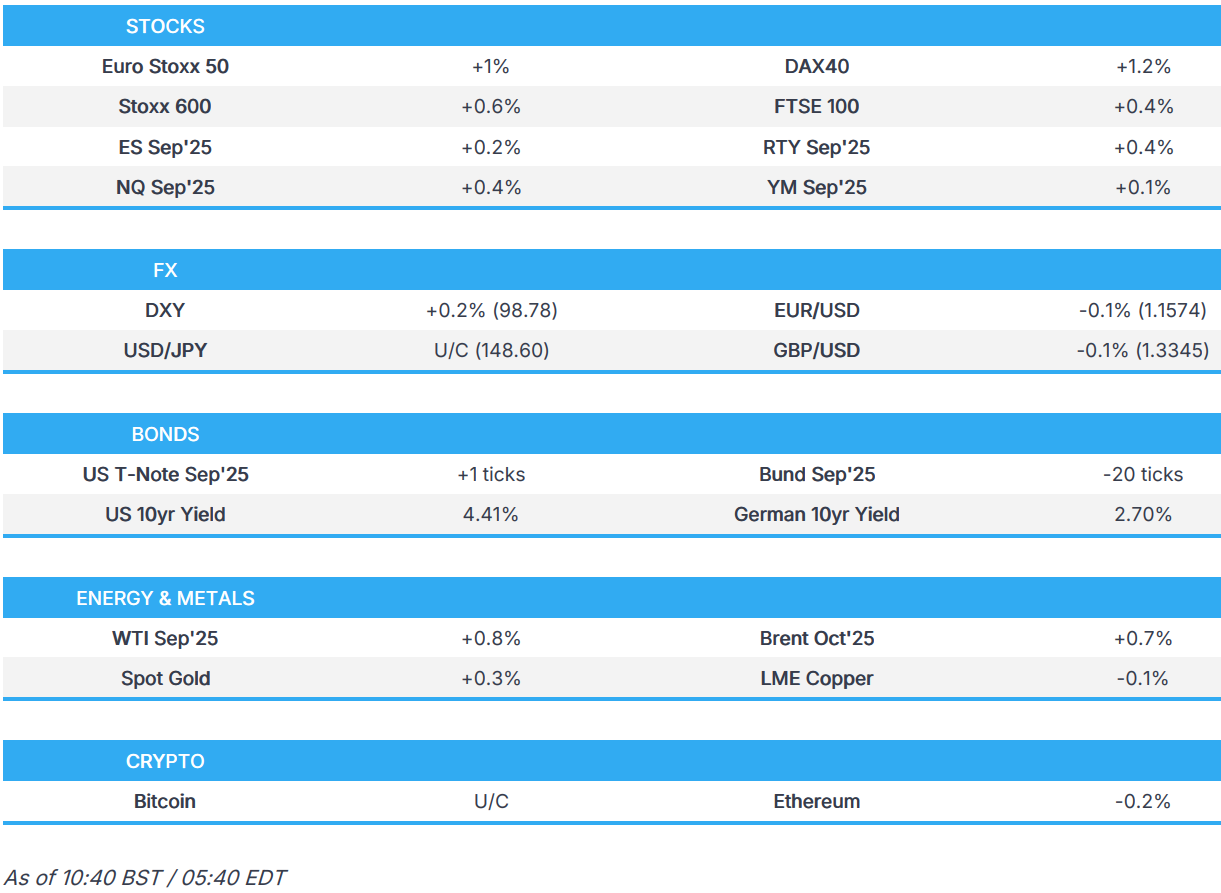

- European bourses are broadly in the green, alongside strength in US futures ahead of a busy earnings slate.

- USD is firmer, EUR/USD's descent continues as markets digest the EU-US trade agreement.

- USTs await data and a 7yr auction, Bunds are on the backfoot giving back some of the prior day’s upside.

- Crude resumes upside while metals are hampered by the Dollar.

- Looking ahead, highlights include US JOLTS Job Openings, Advance Goods Trade Balance, Wholesale Inventories Advance, Consumer Confidence, Dallas Fed Services Revenues, Atlanta Fed GDPNow, ECB SCE, Supply from the US, Earnings from Kering, Banca Generali, Terna, Grifols, Visa, Marathon Digital, Starbucks, Booking, UnitedHealth, Sofi, Paypal, UPS, Spotify, Merck, Nucor, JetBlue, Procter & Gamble.

TARIFFS/TRADE

- Japan's Economy Minister Akazawa, says his understanding is that if a third country reaches an agreement with the US on lower sectoral tariffs, such as chips and pharma, the same rate would apply to Japan.

- US President Trump posted "I’m in Scotland now after having just completed the EU Deal, and numerous others. The United States is doing GREAT, to put it mildly!!!"

- US Commerce Secretary Lutnick said President Trump will mull a few deals this week and set tariff rates on other nations by the end of the week, while he added the table is set with nations that have offered access and "Next week, we're off".

- US President Trump's administration reportedly hears competing proposals on Myanmar policy shift with the Trump team reviewing policy ideas on Myanmar, focused on trade, critical minerals, and China competition, according to Reuters sources.

- South Korea's Finance Minister said they will do their best to derive the best trade agreement and will discuss shipbuilding, as well as other areas for longer-term cooperation with the US.

- Chinese trade negotiations team arrives at the venue for a second day of talks with the US. 29th July 2025

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) opened mostly higher and continued to trade with an upward bias throughout the morning. Upside which follows a mostly higher session on Wall Street, but in contrast to mixed price action across the APAC region.

- European sectors hold a positive bias, with only a handful of industries residing in the red. Industrials take the top spot, lifted by significant post-earning strength in Philips (+13%). Basic Resources is found at the foot of the pile, with downside today driven by broadly lower metals prices.

- US equity futures (ES +0.2% NQ +0.4% RTY +0.3%) are modestly firmer across the board, with some modest outperformance in the NQ after again closing at record highs in the prior session.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

EARNINGS

AstraZeneca (AZN LN) +2.5%: Beats on rev. & adj. EPS, affirms FY guidance.

- Stellantis (STLAM IM/STLAP FP) -2.0%: Expects EUR 1.2bln tariff hit in H2.

- Philips (PHIA NA) +13.0%: Strong EBITDA beat & raises margin, guides adj. EBITA lower citing tariffs; optimistic on China and US.

FX

- After a steady start to the session, DXY is once again on the front foot with the index mechanically boosted by the weakening EUR. That being said, there are some reasons to be positive surrounding the US, mainly on the trade front with the US continuing to grind out deals with trading partners and facing no retaliation in doing so. Furthermore, markets are also anticipating a 90-day extension of the current 90-day US-China truce. Today, attention will turn towards the data slate with JOLTS and Consumer Confidence due on deck. DXY briefly made its way onto a 99 handle with a session peak at 99.05.

- EUR/USD has very much picked up where it left off as the selling pressure in the pair continues following the EU-US trade agreement. Initially many desks were of the view that the removal of uncertainty would be deemed as a market positive. However, this narrative has since given way to negativity around the actual terms of the deal. This has been voiced by various national leaders such as German Chancellor Merz, who warned of the significant impact it will have on the German economy. Elsewhere, the June ECB Consumer Expectations Survey for June saw the 1-year inflation expectation decline to 2.6% from 2.8%. EUR/USD has taken out its 50DMA at 1.1570 with a current session low at 1.1527.

- GBP is softer vs. the USD but to a lesser extent than most peers following the recent cross-related selling in EUR/GBP. ING writes that the recent moves appear to be driven more by positioning, "where opposing fiscal and monetary prospects between the eurozone and the UK had made long EUR/GBP one of the conviction trades this summer". Cable has hit a multi-month low at 1.3315 with not much in the way of support seen until the 1.33 mark.

- JPY is the only of the majors firmer/flat vs. the USD as a run of three consecutive losses vs. the USD pauses for breath. The extent of the rebound is relatively limited at this stage and as such, it is probably not worth reading too much into the price action. Political uncertainty in Japan remains rife with ongoing speculation over whether PM Ishiba will be forced to step down from his position following the recent upper house elections. USD/JPY ventured as high as 148.74 before pulling back below Monday's 148.57 peak.

- Antipodeans are on the backfoot today, swept away alongside the broadly firmer Dollar. Overnight, the Aussie and Kiwi were little changed and price action was fairly muted given the mixed risk appetite in the region.

- PBoC set USD/CNY mid-point at 7.1511 vs exp. 7.1891 (Prev. 7.1467).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are contained amid quiet newsflow. Had a slight upward bias in the early European morning but only a handful of ticks in magnitude at most. Marginal strength that faded as the morning progressed with the risk tone strong. For the US, the day’s main events include a number of data points such as JOLTS, Consumer Confidence, then Atlanta Fed’s GDPNow tracker before US 7yr supply. Today, direction will be drawn from the mentioned data points though it remains to be seen just how much the market will move into a packed second half of the week with the FOMC on Wednesday, PCE on Thursday and then NFP on Friday.

- Bunds are directionally in-fitting with USTs, though trading heavier than their US counterpart so far. Pressure that is seemingly a function of the outperformance seen in Bunds yesterday with the benchmark ending the day near its 129.79 peak. Spent the early European morning contained near that peak and Monday’s 129.73 close. Thereafter, as outlined in USTs above, Bunds came under pressure to a 129.43 low with downside of 30 ticks at most as the risk tone picked up. No real move to the German Bobl auction which was in-line with its introduction.

- Gilts have been in the red and while they have, like Bunds, been lower by 30 ticks at most, for the most part, they have been trading marginally better than their German peer. However, ahead of the morning’s DMO auction this flipped slightly as Bunds came marginally off lows, following a slight pullback in the equity risk tone and potentially as yields reacted to session highs in crude, while Gilts proved relatively unreactive and remained just off lows. Supply was strong, with Gilts lifting by a handful of ticks post-auction and now trade roughly in-line with Bunds. Leaving Gilts 10 ticks off the 91.16 low but some 20 from the initial 91.46 high.

- Most recently, the complex has bounced a touch following the UK/German supply, albeit still within ranges and with the directional bias still at play.

- UK sells GBP 5bln 4.375% 2028 Gilt: b/c 3.71x (prev. 3.46x), average yield 3.941% (prev. 3.847%) & tail 0.2bps (prev. 0.1bps).

- Germany sells EUR 3.409bln vs exp. EUR 4.5bln 2.20% 2030 Bobl: b/c 1.50x (prev. 1.50x), average yield 2.28% (prev. 2.26%) & retention 24.24% (prev. 24.92%).

- Click for a detailed summary

COMMODITIES

- WTI and Brent began the European session around the unchanged mark, taking a breather following the upside seen in the prior session - as a reminder, the complex was boosted after US President Trump cut his deadline for Russian President Putin to reach a peace deal with Ukraine. More recently, the complex has seen some upside, currently trading at session highs; nothing behind the strength, but potentially as traders position themselves ahead of another appearance from US President Trump later today and in-fitting with the positive risk tone seen in the equities complex. Brent Oct'25 currently trades towards the upper end of a USD 69.18-69.83/bbl range.

- Mixed/flat trade across precious metals, taking a breather from Monday's price action in the absence of macro updates and in the run up to tomorrow's FOMC. Spot gold resides in a USD 3,308.16-3,330.10/oz range, and within Monday's USD 3,301.76-3,345.52/oz parameter.

- Mostly lower trade across precious metals as upside is seemingly hampered by the stronger dollar. 3M LME copper resides in a USD 9,759.90-9,796.85/t range at the time of writing.

- Kuwait Oil Minister says OPEC+ decisions are made based on market developments. Optimistic about oil market fundamentals, OPEC+ efforts target energy security and market balance.

- US President Trump calls on the UK to incentivise drillers in the North Sea.

- Click for a detailed summary

NOTABLE DATA RECAP

- Spanish Retail Sales YY (Jun) 6.2% (Prev. 4.8%)

- Spanish Estimated GDP QQ (Q2) 0.7% vs. Exp. 0.6% (Prev. 0.6%); GDP YY (Q2) 2.8% vs. Exp. 2.5% (Prev. 2.8%)

- UK BOE Consumer Credit (Jun) 1.417B GB vs. Exp. 1.2B GB (Prev. 0.859B GB, Rev. 0.92B GB; Mortgage Lending (Jun) 5.34B GB vs. Exp. 2.35B GB (Prev. 2.054B GB, Rev. 2.213B GB); M4 Money Supply (Jun) 0.3% (Prev. 0.2%); Mortgage Approvals (Jun) 64.167k vs. Exp. 63.0k (Prev. 63.032k, Rev. 63.288k)

- UK BRC Shop Price Index YY (Jul) 0.7% (Prev. 0.4%)

NOTABLE EUROPEAN HEADLINES

- ECB staff accused ECB President Lagarde of running an 'unaccountable legal fortress' with members of its own staff accusing the central bank of behaving in an "anti-democratic" way in the latest escalation of tensions between the ECB and its employees, according to FT.

- ECB Consumer Expectations Survey (Jun) - 1-year CPI 2.6% (prev. 2.8%), 3-year 2.8% (prev. 2.8%), 5-year 2.1% (prev. 2.1%).

- Deutsche Bank no longer expects the ECB to deliver rate cuts; now sees next policy move to be a rate hike at the end of 2026.

GEOPOLITICS

- Iranian Foreign Ministry spokesman dismissed US President Trump's accusation of Tehran's interference in Gaza ceasefire talks, according to Iran International.

- US President Trump remains open to dialogue with North Korea leader Kim to achieve a fully denuclearised North Korea, according to the White House.

- North Korea said it rejects any attempt to deny its status as a nuclear state and stated it is not beneficial for North Korea and the US as nuclear states to move in a confrontational direction, while it does not deny that North Korean leader Kim and US President Trump's personal relationship is not bad.

- US President Trump's administration blocked Taiwan's President Lai from a New York stopover en route to Central America in August after China raised objections with Washington about the visit, according to FT.

- Thai army spokesman said Cambodia conducted attacks in several places after the ceasefire deadline although the acting PM later stated that the Thailand-Cambodia border is calm following small clashes. Thai Army spokesman says the commander of key Thai military force along the disputed border has met with the Cambodian counterpart.

- EU has decided to temporarily stop financial assistance to Ukraine due to corruption concerns, according to Ekonomichina Pravda.

CRYPTO

- Bitcoin is essentially flat and trades around the USD 119k mark.

APAC TRADE

- APAC stocks traded mixed with a mostly negative bias after a similar performance among global peers as participants digested trade developments and as risk events loom.

- ASX 200 marginally declined with weakness in telecoms and the top-weighted financial sector leading the descent, while there were few catalysts to provide an uplift.

- Nikkei 225 continued to give back previous trade-related spoils despite recent currency weakness. Japanese PM Ishiba remained defiant and noted there is no change in his intention to stay in office despite many reportedly calling for PM Ishiba's resignation at Monday's LDP meeting.

- Hang Seng and Shanghai Comp were pressured albeit to varying degrees with little information so far from the US-China talks in Sweden which are set to enter a second day

NOTABLE ASIA-PAC HEADLINES

- US President Trump posted "The Fake News is reporting that I am SEEKING a “Summit” with President Xi of China. This is not correct, I am not SEEKING anything! I may go to China, but it would only be at the invitation of President Xi, which has been extended. Otherwise, no interest!"

- Japan's ruling LDP is said to hold a decision-making plenary meeting, according to FNN. It was separately reported that Japanese Finance Minister Kato said sales tax is vital for the social security system in Japan and it is inappropriate to lower the consumption tax rate.

- China is to ‘tighten oversight’ in crowded manufacturing sectors such as EVs and solar power, according to SCMP citing a Ministry of Industry and Information Technology (MIIT) meeting on Monday.

- Toyota (7203 JT) is to reportedly start EV production in Europe as early as 2028, according to Nikkei.