Europe Market Open: Europe primed for a firmer open ahead of data, earnings & Fed

30 Jul 2025, 06:55 by Newsquawk Desk

- US Treasury Secretary Bessent said he will see US President Trump regarding the China tariff pause on Wednesday and some technical details remain on the China tariff pause, while the China tariff extension decision will be up to Trump and if he does not approve tariff pause extension, tariffs on Chinese goods would 'boomerang' back to April 2nd levels, or another level that he chooses.

- US President Trump said Chinese President Xi wants to meet and he thinks it will happen before the end of the year, while he stated that they will either approve the trade extension or not. Chinese Vice Commerce Minister Li said the US and China have agreed to extend the trade truce; Bessent said China jumped the gun a little on the 90-day pause.

- Crude futures surged yesterday amid comments from US President Trump who confirmed changing the deadline for Russia to reach a Ukraine ceasefire agreement to 10 days, while there were simultaneous comments from Treasury Secretary Bessent who told Chinese officials that China could face high tariffs if it continues to purchase sanctioned Russian oil due to US secondary tariff legislation.

- APAC stocks traded mixed following the subdued handover from Wall St; European equity futures indicate a mildly positive cash market open with Euro Stoxx 50 futures up 0.3% after the cash market closed with gains of 0.8% on Tuesday.

- Looking ahead, highlights include French GDP, Spanish CPI, German GDP & Retail Sales, Italian GDP, ECB Wage Tracker, EZ GDP & Sentiment, US ADP National Employment, GDP Advance (Q2), PCE (Q2), Fed, BoC, BCB Policy Announcements Speakers including Fed Chair Powell, BoC's Macklem & Rogers, Supply from Italy, US Quarterly Treasury Refunding Announcement.

- Earnings from Hermes, Airbus, Vinci, Danone, Capgemini, HSBC, GSK, Aston Martin, Santander, Caixabank, Telefonica, Intesa Sanpaolo, Leonardo, Mercedes Benz, Siemens Healthineers, BASF, Adidas, Porsche AG, Meta, Microsoft, RobinHood, Carvana, Lam Research, Qualcomm, Ford, Arm, eBay, FMC, Vertiv, Altria, Kraft Heinz, GE Healthcare & VF Corp.

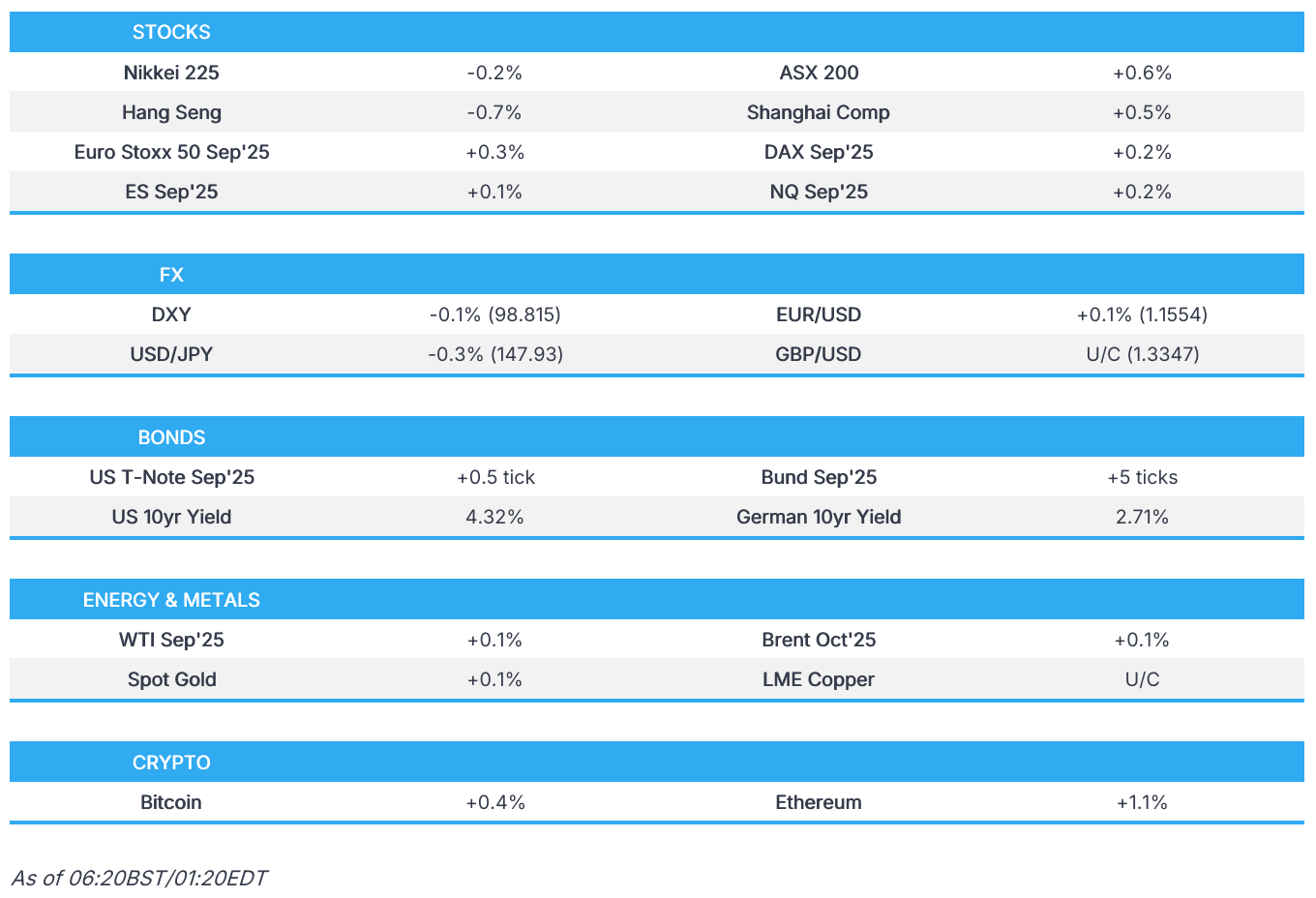

SNAPSHOT

US TRADE

EQUITIES

- US stocks were lower on Tuesday amid a deluge of earnings, which saw Industrials reside as the sectoral laggard and hit by Boeing (BA) (-4%) and UPS (UPS) (-10.5%) post-results, with the latter weighed on as it didn't provide revenue or operating profit guidance amid the current macro uncertainty.

- In terms of the sectors, Real Estate, Utilities, and Energy were at the top of the pile with the latter buoyed by gains of more than 3.5% in oil prices amid comments from US President Trump and Treasury Secretary Bessent on the timeframe for Russia to agree to a ceasefire and warning of Russian oil sanctions.

- Attention was also on US-China trade talks, with the overwhelming readout being positive, although Bessent said he will be meeting with Trump in the Oval Office on Wednesday and that the final decision on the trade truce will be up to the President.

- SPX -0.30% at 6,371, NDX -0.21% at 23,308, DJI -0.46% at 44,633, RUT -0.61% at 2,243.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said Chinese President Xi wants to meet, and he thinks it will happen before the end of the year. Trump also said he spoke with Treasury Secretary Bessent and that it was a very good meeting with the China trade team, while he stated regarding China, that they will either approve the trade extension or not. Furthermore, Trump said the India trade deal is not finalised and that India may pay tariffs of 20%-25%.

- US Treasury Secretary Bessent said he will see US President Trump regarding the China tariff pause on Wednesday and some technical details remain on the China tariff pause, while the China tariff extension decision will be up to Trump and if he does not approve tariff pause extension, tariffs on Chinese goods would 'boomerang' back to April 2nd levels, or another level that he chooses. Bessent also stated he hopes China's 5yr plan would include rebalancing and 90 days is one option for a trade truce extension, as well as suggested they could have another meeting in 90 days and noted there was no discussion in Stockholm regarding a possible Trump-Xi meeting.

- US Treasury Secretary Bessent told Chinese officials that, given US secondary tariff legislation on sanctioned Russian oil, China could face high tariffs if it continues to purchase it. It was separately reported that Bessent said they are discussing big economic frameworks regarding China trade and that China jumped the gun a little on the 90-day pause, while he added that China trade and the August 12th deadline are pending Trump's approval and he doesn’t know where they will be in 90 days but noted good news is they're talking.

- USTR Greer confirmed verification of the London framework and is to make sure magnets are flowing. Greer said they are discussing details on the tariff pause with China, and a 90-day extension is one option for Trump to approve, while he added the US did not agree to any changes on export controls.

- US NEC Director Hassett said Treasury Secretary Bessent and USTR Greer are to give President Trump a briefing on talks on Wednesday regarding China tariff negotiations, and he is hearing it was a very, very positive meeting, while he added that Trump will be pleased with things. Hassett also commented that a number of deals are very close and just awaiting tariff rates, as well as noted that Trump and his team decided to let the NVIDIA (NVDA) chips go, in apparent reference to H20 AI chip shipments to China.

- Chinese Vice Commerce Minister Li said the US and China have agreed to extend the trade truce and both sides will continue to push forward the extension of the pause of reciprocal tariffs as well as Chinese countermeasures, while they will continue to maintain communication and will have timely communication on trade and economic issues.

- China's top trade Negotiator Li said China and US teams continued to make use of the trade consultation mechanism and the two sides had candid, in-depth and constructive discussions, as well as reviewed the implementation of the Geneva consensus. Furthermore, it was reported that China's top trade negotiator said at the close of talks that the two sides "will continue to push for the continued extension of the pause" in tariffs.

- China and the US are to continue pushing for a continued extension of the pause on 24% reciprocal tariffs of the US side and countermeasures of the Chinese side, according to CNBC's Yoon, citing a Chinese international trade representative.

- US Commerce Secretary Lutnick urged South Korea to bring its best trade offer to talks, according to WSJ.

- Taiwan trade delegation will continue talks with the US on tariffs in Washington, according to three people familiar with the matter cited by Reuters.

- The US ambassador to Canada said, "Hopefully very soon," a trade deal between Canada and the US will be reached.

- Brazil's Vice President Alckmin said they are working towards a tariff reduction in all sectors and should not rush into discussions on big tech regulation.

APAC TRADE

EQUITIES

- APAC stocks traded mixed following the subdued handover from Wall St, where the S&P 500 snapped a six-day win streak and as participants braced for approaching key events, including the FOMC and several megacap earnings releases.

- ASX 200 advanced with gains led by strength in Real Estate and Consumer Staples, while stocks also benefited from the softer yield environment after CPI data either matched or printed below forecasts.

- Nikkei 225 lacked conviction amid little pertinent catalysts, and as the BoJ kicked off its two-day policy meeting.

- Hang Seng and Shanghai Comp were mixed with the mainland underpinned following the conclusion of the two-day talks between the US and China, where negotiators were pushing for a 90-day truce extension and await a sign-off from US President Trump.

- US equity futures traded rangebound after the prior day's declines and as participants await data, earnings and the Fed.

- European equity futures indicate a mildly positive cash market open with Euro Stoxx 50 futures up 0.3% after the cash market closed with gains of 0.8% on Tuesday.

FX

- DXY pared some of its gains after advancing yesterday alongside the continued post-EU/US trade deal pressure in EUR, while the US Commerce Secretary expects talks to continue but noted there was "Plenty of horse trading left to do in EU talks". Elsewhere, focus yesterday was also on the second day of US-China trade talks in Stockholm, where officials were pushing for a 90-day extension on the tariff truce but with the final decision up to President Trump who will meet with Treasury Secretary Bessent today, while participants also await data releases including the latest GDP and ADP figures stateside, as well as the FOMC policy announcement.

- EUR/USD attempted to nurse some of this week's losses, although the recovery lost steam with the single currency languishing firmly beneath the 1.1600 level.

- GBP/USD traded uneventfully as price action was confined within tight parameters at the 1.3300 handle.

- USD/JPY retreated to below the 148.00 level with gradual headwinds seen after Japan's government issued an emergency warning and ordered an evacuation following a powerful 8.7 magnitude earthquake in Russia's far east region, although Japan's Chief Cabinet Secretary later stated that there had been no casualties or damage reported so far.

- Antipodeans were rangebound with AUD/USD shrugging off the bout of selling pressure seen following the quarterly and monthly CPI data, which mostly printed softer than expected.

- PBoC set USD/CNY mid-point at 7.1441 vs exp. 7.1742 (Prev. 7.1511).

FIXED INCOME

- 10yr UST futures plateaued after rallying throughout the prior day amid cooling house price data, soft JOLTS data and a stellar 7yr auction ahead of the Fed.

- Bund futures struggled for direction following the recent indecision, and as German GDP and Retail Sales data loom.

- 10yr JGB futures mildly gained but with upside capped amid a lack of data from Japan and with the BoJ kick-starting its 2-day policy meeting.

COMMODITIES

- Crude futures were little changed overnight after surging yesterday amid comments from US President Trump who confirmed changing the deadline for Russia to reach a Ukraine ceasefire agreement to 10 days, while there were simultaneous comments from Treasury Secretary Bessent who told Chinese officials that China could face high tariffs if it continues to purchase sanctioned Russian oil due to US secondary tariff legislation.

- US Private inventory data (bbls): Crude +1.5mln (exp. -1.3mln), Distillate +4.2mln (exp. +0.3mln), Gasoline -1.7mln (exp. -0.6mln), Cushing +0.5mln.

- Spot gold lacked direction with participants awaiting upcoming key events, including the FOMC announcement.

- Copper futures gradually edged higher amid the slight improvement in risk appetite overnight and mild optimism in its largest buyer following trade talks with the US.

CRYPTO

- Bitcoin saw two-way trade and rebounded from an early dip to reclaim the USD 118k status.

NOTABLE ASIA-PAC HEADLINES

- Chinese Finance Minister Lan said China will continue to enhance consumption and will make good use of more proactive fiscal policies, while he added that the uncertainty of China's development environment is rising. Lan stated China will promote healthy development of the property market and actively address local government debt risks.

- Monetary Authority of Singapore maintained its FX-based policy as it kept the prevailing rate of appreciation of the SGD NEER policy band, while it made no change to the width and level at which the band is centred. MAS said prospects for the Singapore economy remain subject to significant uncertainty, especially in 2026, and Singapore’s GDP growth is projected to moderate in the second half of 2025 from its strong pace in H1. Furthermore, it stated that inflationary pressures should remain contained in the near term and the MAS is in an appropriate position to respond to risks to medium-term price stability.

DATA RECAP

- Australian CPI QQ (Q2) 0.7% vs. Exp. 0.8% (Prev. 0.9%)

- Australian CPI YY (Q2) 2.1% vs. Exp. 2.2% (Prev. 2.4%)

- Australian RBA Trimmed Mean CPI QQ (Q2) 0.6% vs. Exp. 0.7% (Prev. 0.7%)

- Australian RBA Trimmed Mean CPI YY (Q2) 2.7% vs. Exp. 2.7% (Prev. 2.9%)

- Australian RBA Weighted Median CPI QQ (Q2) 0.6% vs. Exp. 0.6% (Prev. 0.7%)

- Australian RBA Weighted Median CPI YY (Q2) 2.7% vs. Exp. 2.7% (Prev. 3.0%)

- Australian Weighted CPI YY (Jun) 1.9% vs. Exp. 2.1% (Prev. 2.1%)

GLOBAL NEWS

GLOBAL NEWS

- A magnitude 8.7 earthquake struck Petropavlovsk-Kamchatsky, Russia region, while the Russian regional governor said the earthquake off Kamchatka was the strongest in decades, with a tsunami threat declared, and people were urged to move away from the coastline. Japan's government also issued an emergency warning and ordered an evacuation, while it expected a tsunami as high as 3 metres to arrive along large coastal areas along Pacific Ocean, although Japan's Chief Cabinet Secretary Hayashi later stated there were no casualties or damage reported so far after the quake of Kamchatka triggered a tsunami and NHK reported a tsunami of 30 centimetre reaching Japan's northern Hokkaido. Furthermore, the Honolulu Department of Emergency Management called for evacuation of some coastal areas after the earthquake in Russia and warned destructive tsunami waves were expected, while USCG Oceania issued an order for all commercial vessels to evacuate all commercial harbours in Hawaii with all harbours closed to incoming vessel traffic and California Governor Newsom confirmed that a tsunami warning is in effect for California, particularly the north coast.

GEOPOLITICS

MIDDLE EAST

- UK PM Starmer's office told the cabinet that the UK will recognise the state of Palestine in September before the UNGA, unless the Israeli government takes substantive steps to end the situation in Gaza.

- US President Trump said he never discussed the UK decision to recognise the Palestinian state unless Israel acts on Gaza, and the US is not in that camp.

RUSSIA-UKRAINE

- US President Trump said on Tuesday that it's 10 days away regarding changing the Russia deadline and the threat of secondary sanctions on Russian oil, while he added that tariffs may or may not impact Russia and that there was no response from Russia on tariffs. Trump commented on Russian oil that he doesn’t worry about it as they have so much oil in the US and will just step it up further, as well as noted that oil prices are currently pretty low.