US Market Open: Quiet trade approaching data, earnings and Fed announcement

30 Jul 2025, 11:20 by Newsquawk Desk

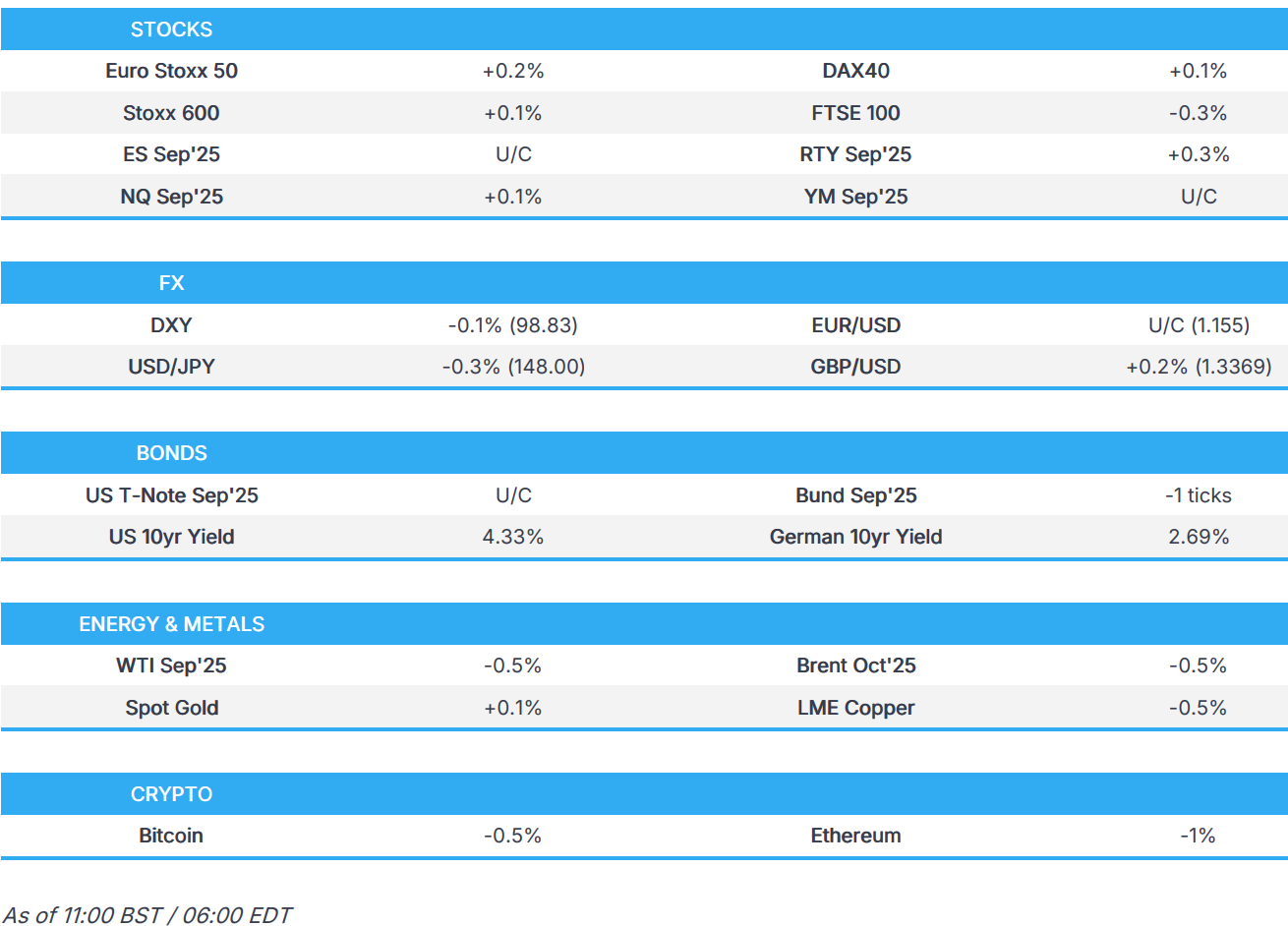

- European bourses are mixed amidst a slew of earnings, US futures flat/firmer ahead of a busy data docket and earnings from Meta and Microsoft.

- USD rally pauses for breath as markets await Q2 flash GDP and FOMC.

- USTs contained into numerous US events, Bunds were little moved by national and EZ-wide GDP metrics.

- Crude takes a breather after Tuesday’s rally while gold holds around the unchanged mark.

- Looking ahead, US ADP National Employment, GDP Advance (Q2), PCE (Q2), Fed, BoC, BCB Policy Announcements Speakers including Fed Chair Powell, BoC's Macklem & Rogers. US Quarterly Treasury Refunding Announcement.

- Earnings from Airbus, Vinci, Microsoft, RobinHood, Carvana, Lam Research, Qualcomm, Ford, Arm, eBay, FMC, Vertiv, Altria, Kraft Heinz, GE Healthcare.

TARIFFS/TRADE

- Taiwan trade delegation will continue talks with the US on tariffs in Washington, according to three people familiar with the matter cited by Reuters.

- Brazil's Vice President Alckmin said they are working towards a tariff reduction in all sectors and should not rush into discussions on big tech regulation.

- India is said to be eying a deadline in the autumn for a US deal, according to Bloomberg sources

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.1%) opened mixed and have continued to trade sideways throughout the morning; though more recently, some upside has been seen. European traders have had French GDP (marginally beat expectations), German Retail Sales (beat), Spanish CPI (mixed), German GDP (Q/Q in-line; Y/Y firmer), EZ Sentiment (stronger-than-expected), EZ GDP (above expectations) - little move seen across the equities complex.

- European sectors are mixed and with the breadth of the market fairly narrow, aside from the day’s underperformer. Chemicals is weighed on by post-earning losses in Symrise (-6%), where the co. reported a rev. slowdown. Consumer Products is found around the middle of the pile, given the mixed earnings from within the sector; in Luxury, Kering (+4%) and Hermes (-4%) are playing tug-of-war, whilst Adidas (-7%) adds to the downside after its H1’25 update. The German sportswear giant reported strong profits, attributed to resilience in the retro shoe market – though it was still shy of expectations; further adding to the pressure is the co. flagging a USD 231mln tariff-related hit.

- US equity futures are modestly firmer across the board, ahead of a tinderbox of key events, including FOMC/BoC policy decisions, Mag 7 earnings and important US data. Key pre-market movers; Starbucks (+5%, revenue beat due to China strength, and as it progresses with its turnaround strategy), Visa (-2%, Q3 results beat estimates but the company kept its FY earnings outlook unchanged).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is a touch softer as the recent recovery in the USD pauses for breath. The USD has been bolstered in recent sessions by developments on the trade front following the recent EU-US agreement and expectations of an extension to the 90-day truce between the US and China; subject to Trump's approval. Market pricing places the odds of a September reduction at 68% with a total of 46bps of loosening priced by year-end. DXY is currently tucked within Tuesday's 98.58-99.14 range. Ahead, a slew of US data points and the FOMC announcement.

- EUR is attempting to atone for recent losses following the downside seen in the wake of the recent EU-US trade deal, which has been framed by many as a "win" for the US and subsequently drawn objections from various European leaders. Note, the agreement still requires ratification from the EU and national parliaments. Focus today turned back to the data slate following national and EZ-wide GDP metrics; the latter saw growth slow to 0.1% from 0.6% following an unwind of the front-loading seen in Q1 ahead of expected tariffs. Elsewhere, the ECB's wage tracker passed with little in the way of fanfare; 2025 metric was revised a touch higher to 3.152% from 3.144%. EUR/USD remains within Tuesday's 1.1519-99 range and below its 50DMA at 1.1574.

- JPY is attempting to claw back some lost ground vs. the USD with some tailwinds seen overnight after Japan's government issued an emergency warning and ordered an evacuation following a powerful 8.7 magnitude earthquake in Russia's far east region. Attention now turns towards the upcoming BoJ policy announcement, which is set to see policymakers stand pat on current policy settings. USD/JPY has slipped below the 148 mark with a session low at 147.81.

- GBP is marginally firmer vs. the USD after a run of four consecutive losses. UK-specific newsflow light, more focus on US developments today. Cable remains on a 1.33 handle and trades in close proximity to Tuesday's 1.3364 peak.

- AUD sits at the foot of the G10 leaderboard following a soft outturn for Australian CPI overnight, which saw headline Y/Y CPI slow to 2.1% from 2.4%. Oxford Economics writes that the data clears the way for another rate cut in August (currently priced at 92%). AUD/USD has slipped back below its 50DMA at 0.6513.

- CAD is flat ahead of the BoC rate announcement, which is expected to see the policy rate left unchanged at 2.75%. Additionally, the BoC is likely to leave out forward guidance again, given uncertainties in the economy. USD/CAD remains on a 1.37 handle and within Tuesday's 1.3731-88 range.

- PBoC set USD/CNY mid-point at 7.1441 vs exp. 7.1742 (Prev. 7.1511).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are contained ahead of a packed day. In a 111-10 to 111-13 band, matching the WTD peak from Tuesday. A number of key events today, including US ADP National Employment, GDP/PCE (Q2), BoC/Fed Policy Announcements. Also in focus is US President Trump who may provide some US-China trade updates, following the meeting between the two countries in Sweden. Into the packed docket, given the contained benchmark action, yields are also near-enough unchanged but with a very marginal steepening bias. An upward move for USTs brings last week’s 111-14+ high into view. On the flip side, 111-00 is the first support point before 110-24+ and 110-24 from earlier in the week.

- Bunds spent much of the European morning a touch firmer having picked up gradually throughout the European morning but action is still relatively muted into the above US risk events. As high as 129.84 with gains of c. 20 ticks at best. The morning has been dominated by earnings (see Equities) with the European risk tone largely contained but with some earnings-driven regional variation. Equities aside, the first readings of Q2 GDP saw stronger-than-forecast quarterly French release, in-line German and weaker Italian (Y/Y outside forecast range) & Dutch readings. No move to these. Thereafter the EZ wide figures (beat both Q/Q and Y/Y) - again no reaction.

- Gilts are managing to eek some marginal outperformance vs peers, with gains of 21 ticks at best vs 19 at most in Bunds. If the current 91.96 high is breached then we look to last week’s 92.15 peak and then 92.24 from the week before.

- UK DMO sells GBP 300mln 3.75% 2052 Gilt via tender; b/c 4.62x, average yield 5.383%

- Italy sells EUR 7.0bln vs exp. EUR 5.5-7.0bln 2.70% 2030, 3.60% 2035, 1.35% 2030 BTP & EUR 2.0bln vs exp. EUR 1.5-2.0bln 2034 CCTeu

- Click for a detailed summary

COMMODITIES

- Flat/subdued trade across the crude complex as prices take a breather following Tuesday's hefty gains. This morning, some downticks in the complex coincided with comments from Polish PM Tusk, who sees a chance that the Russia-Ukraine conflict could be paused in the near future, via Bloomberg. That being said, Tusk is not involved in any Russia-Ukraine talks. WTI resides in a USD 69.01-69.79/bbl range with its Brent counterpart in a USD 72.52-72.24/bbl range.

- Precious metals are mixed today with spot palladium/silver marginally lower whilst gold is flat. Spot gold resides in a USD 3,321.79-3,333.77/oz range, and within Monday's USD 3,308.16-3,334.27/oz parameter.

- Mixed trade across base metals with newsflow on the lighter side ahead of the aforementioned risk events. This morning, China's Politburo held a meeting on the economy, and said the economy still faces challenges, adding that China should accelerate the issuance of government bonds, and called to implement more proactive fiscal policy, via Xinhua. 3M LME copper resides in a USD 9,726.35-9,826.65/t range at the time of writing.

- US Private inventory data (bbls): Crude +1.5mln (exp. -1.3mln), Distillate +4.2mln (exp. +0.3mln), Gasoline -1.7mln (exp. -0.6mln), Cushing +0.5mln.

- Click for a detailed summary

NOTABLE DATA RECAP

- Spanish CPI YY Flash NSA (Jul) 2.7% vs. Exp. 2.6% (Prev. 2.3%); Core 2.3% (Prev. 2.2%); MM Flash NSA (Jul) -0.10% vs. Exp. -0.40% (Prev. 0.70%)

- Spanish HICP Flash YY (Jul) 2.7% vs. Exp. 2.7% (prev. 2.3%); MM (Jul) -0.4% vs. Exp. -0.3% (Prev. 0.7%)

- German Retail Sales MM Real (Jun) 1.0% vs. Exp. 0.5% (Prev. -1.6%, Rev. -0.6%); YY Real (Jun) 4.9% vs. Exp. 2.3% (Prev. 1.6%, Rev. 4.6%)

- French GDP Preliminary QQ (Q2) 0.3% vs. Exp. 0.1% (Prev. 0.1%)

- ECB Wage Tracker: 2025 Annual 3.152% (prev. 3.144%)

- German GDP Flash YY NSA (Q2) 0.0% vs. Exp. 0.1% (Prev. -0.2%); GDP Flash QQ SA (Q2) -0.1% vs. Exp. -0.1% (Prev. 0.4%); GDP Flash YY SA (Q2) 0.4% vs. Exp. 0.2% (Prev. 0.0%)

- Italian GDP Prelim YY (Q2) 0.4% vs. Exp. 0.6% (Prev. 0.7%); Prelim QQ (Q2) -0.1% vs. Exp. 0.1% (Prev. 0.3%)

- EU GDP Flash Prelim YY (Q2) 1.4% vs. Exp. 1.2% (Prev. 1.5%); GDP Flash Prelim QQ (Q2) 0.1% (Prev. 0.6%); EU GDP Flash Prelim QQ (Q2) 0.1% vs. Exp. 0.0% (Prev. 0.6%)

- EU Services Sentiment (Jul) 4.1 vs. Exp. 3.3 (Prev. 2.9, Rev. 3.1); Consumer Confid. Final (Jul) -14.7 vs. Exp. -14.7 (Prev. -14.7); EU Selling Price Expec (Jul) 9.2 (Prev. 5.6, Rev. 6.2); Cons Infl Expec (Jul) 25.1 (Prev. 21.2, Rev. 21.3); Economic Sentiment (Jul) 95.8 vs. Exp. 94.5 (Prev. 94.0, Rev. 94.2); Industrial Sentiment (Jul) -10.4 vs. Exp. -11.0 (Prev. -12.0, Rev. -11.8)

NOTABLE EUROPEAN HEADLINES

- ECB Blog: "China-US trade tensions could bring more Chinese exports and lower prices to Europe"

NOTABLE US HEADLINES

- Tsunami waves of 3.6ft seen at Crescent City in California, according to NTWC.

GEOPOLITICS

- Polish PM Tusk sees a chance that the Russia-Ukraine conflict could be paused in the near-future, via Bloomberg; “There are many signs pointing to the fact that the Russia-Ukraine war may be at least suspended in the nearest time” Tusk said.

- "A senior Israeli official briefed the Saudi Al-Arabiya channel that there are warnings that elements backed by Iran are planning to attack Israel from southern Syria.", according to journalist Elster.

- Kremlin spokesman says a meeting between the Presidents of Russia and the US is not on the agenda, according to Russian representative Ulyanov on X

- China Defence Ministry says Chinese and Russian navies will hold joint military exercise in waters and airspace near Vladivostok in August.

CRYPTO

- Bitcoin is a little lower and trades just above the USD 118k mark; Ethereum posts deeper losses and holds just above USD 3.8k.

APAC TRADE

- APAC stocks traded mixed following the subdued handover from Wall St, where the S&P 500 snapped a six-day win streak and as participants braced for approaching key events, including the FOMC and several megacap earnings releases.

- ASX 200 advanced with gains led by strength in Real Estate and Consumer Staples, while stocks also benefited from the softer yield environment after CPI data either matched or printed below forecasts.

- Nikkei 225 lacked conviction amid little pertinent catalysts, and as the BoJ kicked off its two-day policy meeting.

- Hang Seng and Shanghai Comp were mixed with the mainland underpinned following the conclusion of the two-day talks between the US and China, where negotiators were pushing for a 90-day truce extension and await a sign-off from US President Trump.

NOTABLE ASIA-PAC HEADLINES

- Chinese Finance Minister Lan said China will continue to enhance consumption and will make good use of more proactive fiscal policies, while he added that the uncertainty of China's development environment is rising. Lan stated China will promote healthy development of the property market and actively address local government debt risks.

- Monetary Authority of Singapore maintained its FX-based policy as it kept the prevailing rate of appreciation of the SGD NEER policy band, while it made no change to the width and level at which the band is centred. MAS said prospects for the Singapore economy remain subject to significant uncertainty, especially in 2026, and Singapore’s GDP growth is projected to moderate in the second half of 2025 from its strong pace in H1. Furthermore, it stated that inflationary pressures should remain contained in the near term and the MAS is in an appropriate position to respond to risks to medium-term price stability.

- A magnitude 8.7 earthquake struck Petropavlovsk-Kamchatsky, Russia region, while the Russian regional governor said the earthquake off Kamchatka was the strongest in decades, with a tsunami threat declared, and people were urged to move away from the coastline. Japan's government also issued an emergency warning and ordered an evacuation, while it expected a tsunami as high as 3 metres to arrive along large coastal areas along Pacific Ocean, although Japan's Chief Cabinet Secretary Hayashi later stated there were no casualties or damage reported so far after the quake of Kamchatka triggered a tsunami and NHK reported a tsunami of 30 centimetre reaching Japan's northern Hokkaido. Furthermore, the Honolulu Department of Emergency Management called for evacuation of some coastal areas after the earthquake in Russia and warned destructive tsunami waves were expected, while USCG Oceania issued an order for all commercial vessels to evacuate all commercial harbours in Hawaii with all harbours closed to incoming vessel traffic and California Governor Newsom confirmed that a tsunami warning is in effect for California, particularly the north coast.

- China's Politburo held a meeting on the economy; says economy still faces challenges, says China should accelerate the issuance of government bonds; calls to implement more proactive fiscal policy, via Xinhua. President Xi says China "must break down over-competition", urges measures to boost consumption and the expansion of domestic demand in all directions.

- Nissan (7201 JT) Q1 (JPY): Net loss 115.8 (prev. profit 28.56bln Y/Y). Operating loss 79.12bln (prev. profit 995mln). Notes of impairment loss of JPY 40.6bln, recorded as an extraordinary loss in statement; forecasts JPY 180bln operating loss for Apr-Sep.

- United Microelectronics (UMC) Q2 (TWD): net 8.9bln (prev. 13.79bln Y/Y), revenue 58.76bln (prev. 56.80bln Y/Y).

DATA RECAP

- Australian CPI QQ (Q2) 0.7% vs. Exp. 0.8% (Prev. 0.9%); YY 2.1% vs. Exp. 2.2% (Prev. 2.4%)

- Australian RBA Trimmed Mean CPI QQ (Q2) 0.6% vs. Exp. 0.7% (Prev. 0.7%); YY (Q2) 2.7% vs. Exp. 2.7% (Prev. 2.9%)

- Australian RBA Weighted Median CPI QQ (Q2) 0.6% vs. Exp. 0.6% (Prev. 0.7%); YY (Q2) 2.7% vs. Exp. 2.7% (Prev. 3.0%)

- Australian Weighted CPI YY (Jun) 1.9% vs. Exp. 2.1% (Prev. 2.1%)