Europe Market Open: Fed & BoJ hold rates, hawkish Powell supports dollar; META, MSFT surge after hours

31 Jul 2025, 06:50 by Newsquawk Desk

- Fed kept rates on hold with dissent from Waller and Bowman. Powell said will not let tariffs become inflationary.

- BoJ maintained rates as expected, raised growth and inflation outlook. Continued to note uncertainty over trade.

- US equity futures rebounded after-hours with strength in tech/AI-related names after Microsoft (+8.3%) and Meta (+11.5%) smashed Q2 earnings.

- US President Trump announced that South Korea will be subject to a 15% and make USD 350bln in investments in the US.

- European equity futures suggest a mildly positive open. Hang Seng lags post-disappointing Chinese PMIs.

- DXY rally pauses for breath, EUR/USD remains on a 1.14 handle. USTs rebounded off the lows after post-Powell pressure.

- Looking ahead, highlights include French CPI, PPI, German Unemployment Rate, CPI, EZ Unemployment Rate, Italian CPI, US Challenger Layoffs, PCE (Jun), Jobless Claims, Employment Wages, Chicago PMI, Atlanta Fed GDPNow, Canadian GDP, SARB Policy Announcement.

- Earnings from Shell, Unilever, LSE, Haleon, Standard Chartered, Anglo American, Sanofi, Schneider Electric, Safran, Credit Agricole, Saint Gobain, SocGen, Accor, Teleperformance, Air France, AB InBev, BBVA, Holcim Puma, Lufthansa, BMW, Apple, Amazon, Strategy, Coinbase, Reddit, Roku, CVS, Roblox, AbbVie, Norwegian Cruise Line, Cigna, Mastercard & PG&E.

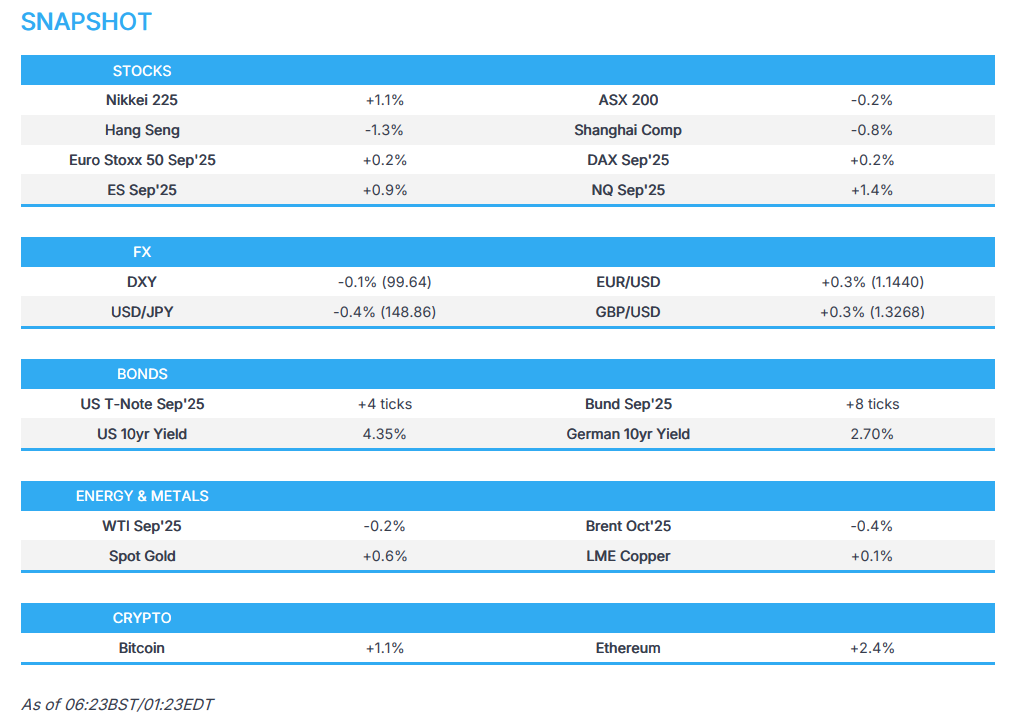

SNAPSHOT

US TRADE

EQUITIES

- US stocks and Treasuries were sold, while the dollar saw a notable bid in the wake of a hawkish Fed Chair Powell. In the FOMC rate decision, the central bank held rates at 4.25-4.50%, as expected, with Governors Waller and Bowman dissenting in favour of a 25bps cut, although little move was seen. In Powell's presser, he said no decision has been made about the September meeting, and they will not let tariffs become inflationary, because they will make sure it does not become serious by deploying their tools. In the wake of these comments, particularly the latter, US indices and T-Notes sold off to session lows, while the Dollar rose to peaks, and Fed money market pricing became more hawkish, with only 38bps of cuts seen by year-end now vs 46bps post Fed statement. However, equity futures rebounded after-hours with strength in tech/AI-related names after Microsoft (MSFT) and Meta (META) smashed Q2 earnings expectations.

- SPX -0.12% at 6,363, NDX +0.16% at 23,345, DJI -0.38% at 44,461, RUT -0.47% at 2,232.

- Click here for a detailed summary.

FOMC

- Fed left rates on hold at 4.25-4.50%, as expected, in which Kugler did not vote and both Waller and Bowman dissented, preferring to lower the FFR rate by 25bps. Fed said recent indicators suggest that the growth of economic activity moderated in the first half of 2025 (prev. Recent indicators suggest economic activity has continued to expand at a solid pace) and stated that Inflation remains somewhat elevated, while the unemployment rate remains low, and labour market conditions remain solid. Fed also stated that uncertainty about the economic outlook remains elevated (prev. Uncertainty about the economic outlook has diminished but remains elevated) and it maintained language that "In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks."

- Fed Chair Powell said the economy is in a solid position and inflation is somewhat above target, while the labour market is at or near maximum level and he believes the current stance of policy leaves them well positioned to respond in a timely way. Fed Chair Powell said most measures of longer-run inflation expectations are consistent with the Fed's goal and sees the current stance as appropriate to guard against inflation risks, as well as noted that they are on track to wrap up the policy review by late summer and will receive a good amount of data in the coming months.

- Fed Chair Powell said during the Q&A that the economy is not behaving although modestly restrictive policy is holding it back inappropriately, when asked about a September rate cut, while they have made no decisions about September and expect to have more information coming up. Powell said the statement about uncertainty reflects changes since the last meeting and it had not diminished further since the June meeting, as well as noted they are still a ways away from seeing where things settle with many uncertainties left to resolve and it feels like there is much more to come. Fed Chair Powell said regarding the dissents that what you want is a clear explanation and had that today; people thought carefully about this and put their positions out there, while majority was of the view that inflation is above target and maximum employment is at target, which calls for a modestly restrictive stance of policy for now. Furthermore, he said a reasonable base case is that tariffs are one-time price impacts, but in the end, this will not turn out to be inflation, because they will make sure it is not by deploying their tools and are trying to accomplish the goal in an efficient manner.

TARIFFS/TRADE

- US President Trump announced that the US has agreed to a "Full and Complete Trade Deal" with South Korea in which South Korea will give the United States USD 350bln for investments owned and controlled by the US, and selected by Trump, while South Korea will also purchase USD 100bln of LNG, or other energy products and South Korea has also agreed to invest a large sum of money for their Investment purposes with this sum to be announced within the next two weeks when the President Lee comes to the White House for a bilateral meeting. Trump added "It is also agreed that South Korea will be completely OPEN TO TRADE with the United States, and that they will accept American product including Cars and Trucks, Agriculture, etc. We have agreed to a Tariff for South Korea of 15%. America will not be charged a Tariff."

- South Korean Presidential Office confirmed US lowered tariffs on South Korean autos to 15% from 25%, while it added that chips and drug tariffs will not be worse than those applied to other countries and stated that USD 200bln of funds are allocated for chips, nuclear power, batteries, and bio sectors. Furthermore, it stated that the rice and beef market will not be opened and that South Korea demanded 12.5% auto tariffs but President Trump insisted on 15%.

- US President Trump said they are busy working on trade deals and stated they have just concluded a deal with Pakistan, whereby Pakistan and the US will work together on developing massive oil reserves, while they are in the process of choosing the oil company that will lead this partnership. Furthermore, he stated that other countries are making offers for a tariff reduction.

- US President Trump said they are negotiating with other countries and the rest will receive a "bill", while he said they are negotiating with India now, and we will see what happens with India which will be known at the end of the week. Trump also stated that they are moving along well with China, as well as noted it is going to work out well and they are going to have a very fair deal with China.

- US President Trump posted "I don’t care what India does with Russia. They can take their dead economies down together, for all I care. We have done very little business with India, their Tariffs are too high, among the highest in the World. Likewise, Russia and the USA do almost no business together. Let’s keep it that way, and tell Medvedev, the failed former President of Russia, who thinks he’s still President, to watch his words. He’s entering very dangerous territory!"

- US President Trump will discuss Mexico's plan to cut trade deficit with Mexican President Sheinbaum on Thursday ahead of the August 1st deadline.

- US President Trump plans to sign new executive orders on Thursday, imposing higher tariff rates on several countries that have been unable to reach negotiated trade agreements by Friday deadline, while this could include a number of America's biggest trading partners, including Canada, Mexico and Taiwan, according to POLITICO.

- Pakistan's government said the trade agreement with the US will result in a reduction in reciprocal tariffs, especially on Pakistani exports to the US, and is expected to spur increased US investment in Pakistan’s infrastructure and development projects. Furthermore, it stated that the US–Pakistan deal marks the beginning of economic collaboration in energy, mines and minerals, IT, cryptocurrency, and other sectors.

- US Commerce Secretary Lutnick announced trade deals were made with Cambodia and Thailand. However, the Thai Finance Minister later said they are still working a bit more on the trade proposal to the US and he expects to receive info on US tariffs within 24 hours.

NOTABLE HEADLINES

- US President Trump said he hears they're going to do it in September, when speaking on the Fed cutting interest rates.

- US NEC Director Hassett said the data is consistent with the Fed cutting rates and that many economists think the Fed has been too slow.

AFTER-MARKET EARNINGS

- Meta Platforms Inc (META) Q2 2025 (USD): EPS 7.14 (exp. 5.85), Revenue 47.52bln (exp. 44.87bln); shares rose 11.5% after-market.

- Microsoft Corp (MSFT) Q2 2025 (USD): EPS 3.65 (exp. 3.35), Revenue 76.44bln (exp. 73.76bln); shares rose 8.3% after-market.

- Arm Holdings (ARM) Q1 2026 (USD): Adj. EPS 0.35 (exp. 0.35), Revenue 1.05bln (exp. 1.05bln); shares fell 8.1% after-market

- Qualcomm Inc (QCOM) Q3 2025 (USD): Adj. EPS 2.77 (exp. 2.70), Revenue 10.37bln (exp. 10.30bln); shares fell 4.8% after-market.

- eBay Inc (EBAY) Q2 2025 (USD): Adj. EPS 1.37 (exp. 1.30), Revenue 2.7bln (exp. 2.64bln); shares rose 12.1% after-market.

- Western Digital Corp (WDC) Q4 2025 (USD): Adj. EPS 1.66 (exp. 1.46), Revenue 2.605bln (exp. 2.46bln); shares rose 10.2% after-market.

APAC TRADE

BOJ

- BoJ maintained its short-term interest rate target at 0.5%, as expected with the decision made by unanimous vote, while it noted that underlying inflation is likely to stall due to slowing growth but will gradually accelerate thereafter and underlying consumer inflation likely to be at a level generally consistent with the 2% target in the second half of the projection period from fiscal 2025 through 2027. BoJ stated that uncertainty over trade policy and its developments, and their impact on the economic and price outlook, remains high and noted that real interest rates are at extremely low levels, while it must have no preconception in judging whether the economy and prices are moving in line with the forecast. BoJ reiterated that it will conduct monetary policy as appropriate from the perspective of sustainably and stably achieving the 2% inflation target and will continue to raise the policy rate if the economy and prices move in line with the forecast, in accordance with improvements in the economy and prices. Furthermore, it noted there is high uncertainty surrounding trade policy developments and their impact on the economy and stated that a prolonged period of high uncertainties regarding trade policies could lead firms to focus more on cost-cutting and as a result, moves to reflect price rises in wages could also weaken. In terms of the latest Outlook Report, board members' median forecasts for Core CPI were raised through to 2027, while the median forecast for Real GDP was upgraded for FY25 but maintained for the following two years after.

EQUITIES

- APAC stocks traded mixed in the aftermath of a hawkish Powell and strong mega-cap earnings stateside, while participants also digested the US-South Korea trade deal, disappointing Chinese PMIs and the BoJ policy announcement at month-end.

- ASX 200 was lacklustre amid losses in miners following weaker H1 earnings from Rio Tinto and with a record drop seen in copper prices after the Trump administration excluded refined copper from planned 50% tariffs.

- Nikkei 225 outperformed and reclaimed the 41,000 level after recent currency weakness and better-than-expected Industrial Production & Retail Sales from Japan, while the BoJ policy provided no major fireworks as the central bank kept its short-term rates unchanged but highlighted trade-related uncertainty and raised its Core CPI projections.

- Hang Seng and Shanghai Comp were pressured following disappointing official PMI data in which the headline Manufacturing and Non-Manufacturing PMI figures missed expectations with the former remaining in contraction territory.

- US equity futures (ES +0.9%, NQ +1.4%) advanced on the back of strong earnings from the likes of Microsoft and Meta, while there is some trade optimism following the US-South Korea trade deal.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market finished with gains of 0.3% on Wednesday.

FX

- DXY took a breather after surging to just shy of the 100.00 level yesterday with an uplift seen owing to the stronger-than-expected GDP data and in the aftermath of the FOMC where the Fed kept the Fed Funds Rate unchanged at 4.25%-4.50%, as expected, while Powell provided some hawkish-leaning comments at the press conference as he stated they have made no decisions about a rate cut in September and the reasonable base case is that tariffs are one-time price impacts, but in the end, this will not turn out to be inflation, because they will make sure it is not by deploying their tools. Furthermore, attention was also on trade developments after a few deals were reached including between the US and South Korea, involving a 15% tariff rate for South Korea.

- EUR/USD moved off the prior day's lows after support held at the 1.1400 level but with the rebound limited after recent underperformance owing to US data and Powell comments.

- GBP/USD got some slight reprieve after slipping beneath the 1.3300 handle yesterday with very few pertinent drivers for the UK to support GBP.

- USD/JPY pulled back from its recent surge above the 149.00 level, while there was a choppy reaction to the BoJ policy meeting where it unsurprisingly kept the rate unchanged.

- Antipodeans attempted to claw back some of this week's losses but with the recovery contained amid the mixed risk appetite and as better-than-expected Building Approvals and Retail Sales data for Australia were offset by disappointing official Chinese PMI data.

- Brazil Central Bank maintained the Selic rate at 15.00%, as expected, with the decision unanimous and it expects an interruption of the tightening cycle, while it stated it is assessing the accumulated effects of the already implemented adjustment and will evaluate whether the current interest rate level, assuming it remains stable for a very prolonged period, will be enough to ensure inflation convergence to target. BCB said the Committee will remain vigilant and future monetary policy steps can be adjusted, as well as noted it will not hesitate to resume the rate hiking cycle if appropriate.

FIXED INCOME

- 10yr UST futures rebounded off support at the 111.00 level after having been pressured by a hot GDP report and hawkish comments from Fed Chair Powell's press conference.

- Bund futures traded rangebound after recent indecision and as German Unemployment and CPI data loom.

- 10yr JGB futures were subdued following the uninspiring performance in global peers and after the BoJ rate decision in which the central bank kept rates unchanged, noted high uncertainty surrounding trade policy and raised its Core CPI forecasts across the projection horizon.

COMMODITIES

- Crude futures were rangebound after extending on gains yesterday in the aftermath of the better-than-expected US GDP data and Trump trade headlines.

- Spot gold nursed some of the prior day's losses but remained just beneath the USD 3,300/oz level after slumping alongside a firmer dollar and a collapse in copper prices.

- Copper futures suffered a record intraday drop following the announcement of US President Trump's proclamation on copper which excluded refined copper from planned 50% tariffs.

- White House announced that President Trump issued a proclamation imposing universal 50% tariffs on imports of semi-finished copper products and copper-intensive derivative products effective August 1st, while the White House said copper input materials and copper scrap are not subject to 232 or reciprocal tariffs.

CRYPTO

- Bitcoin mildly gained overnight after climbing back above the USD 118k level.

APAC DATA RECAP

- Chinese NBS Manufacturing PMI (Jul) 49.3 vs. Exp. 49.7 (Prev. 49.7)

- Chinese NBS Non-Mfg PMI (Jul) 50.1 vs. Exp. 50.3 (Prev. 50.5)

- Chinese Composite PMI (Jul) 50.2 (Prev. 50.7)

- Japanese Industrial O/P Prelim MM SA (Jun) 1.7% vs. Exp. -0.6% (Prev. -0.1%)

- Japanese Retail Sales YY (Jun) 2.0% vs. Exp. 1.8% (Prev. 2.2%, Rev. 1.9%)

- Australian Building Approvals (Jun) 11.9% vs. Exp. 2.0% (Prev. 3.2%)

- Australian Retail Sales MM Final (Jun) 1.2% vs. Exp. 0.4% (Prev. 0.2%)

- Australian Retail Trade (Q2) 0.3% (Rev. 0.1%)

GEOPOLITICS

MIDDLE EAST

- Israel PM Netanyahu has not ruled out a plan to destroy the rest of northern Gaza and occupy it, despite the army's warnings about the danger to the hostages, according to Guy Elster citing Haaretz.

- Canadian PM Carney said Canada intends to recognise the state of Palestine at the 80th session of the UN General Assembly in September. Israel's Foreign Ministry commented shortly after that Israel rejects the statement by Canada’s PM over planned recognition of Palestinian state, and the change in the position of the Canadian government at this time is a reward for Hamas and harms efforts to achieve a ceasefire in Gaza and a framework for the release of the hostages.

- US imposed sweeping new sanctions on a vast international oil trading network which it claimed has funnelled tens of billions of dollars in oil revenue to Iran, according to FT.

RUSSIA-UKRAINE

- Two top Senate Republicans laid out a plan to allow allies to finance donations of US weapons and military equipment to Ukraine, according to WSJ.

EU/UK

NOTABLE HEADLINES

- German Finance Minister urged cabinet ministers to cut spending to close the budget gap of over EUR 30bln in 2027, via an interview with Ard-Tagesthemen.