US Market Open: Tech outperforms after META and MSFT surge after earnings; PCE and earnings ahead

31 Jul 2025, 11:05 by Newsquawk Desk

- BoJ maintained rates as expected, raised growth and inflation outlook. Continued to note uncertainty over trade; Ueda said, no large change to central outlook that growth pace will slow down and underlying inflation stalls.

- US President Trump announced that South Korea will be subject to a 15% tariff and make USD 350bln in investments in the US.

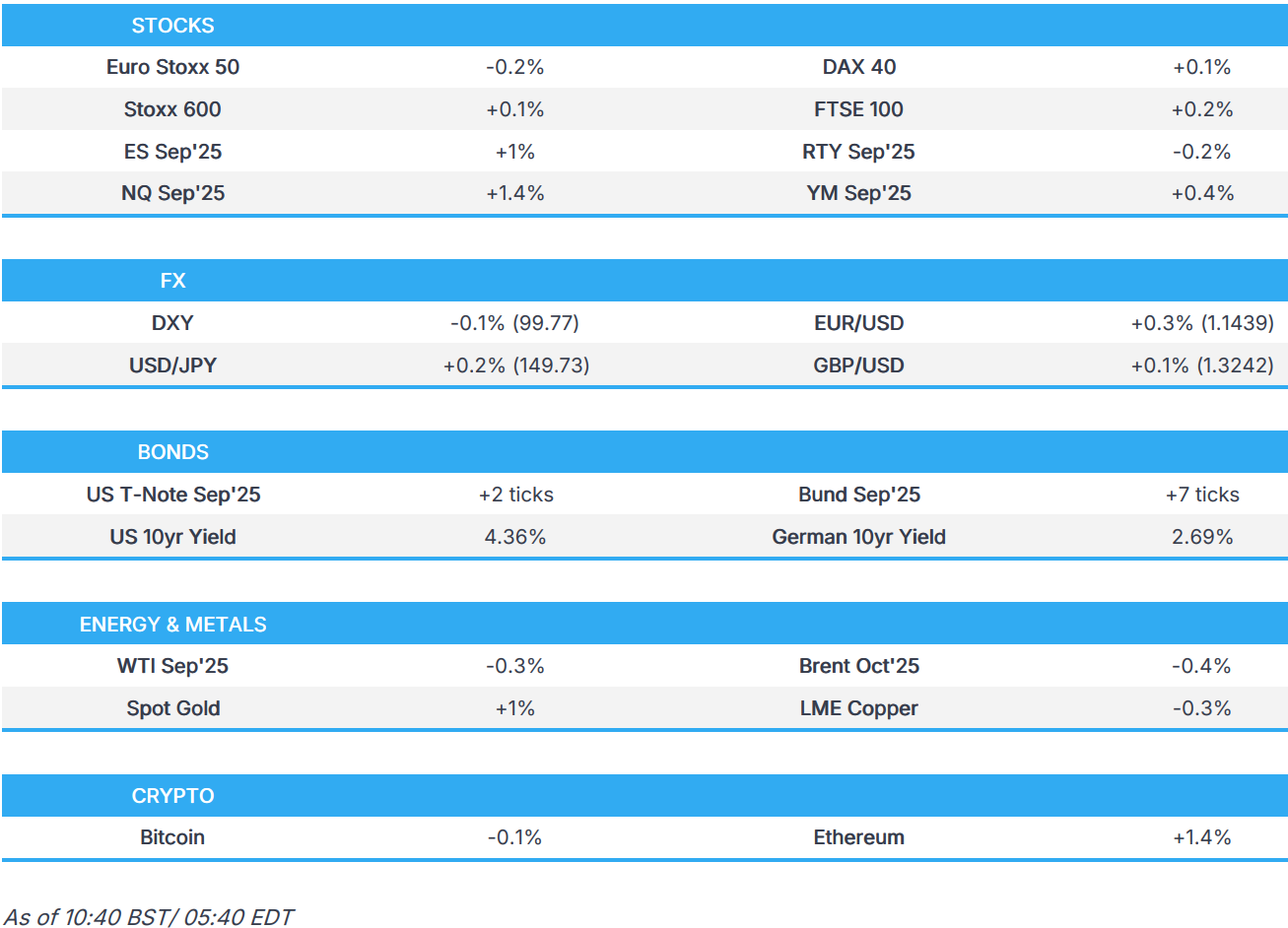

- European bourses opened higher but have waned off best levels, NQ outperforms after stunning earnings from META +12% & MSFT +8%.

- Ongoing USD rally pauses for breath ahead of PCE, JPY pressured after BoJ Governor Ueda.

- JGBs boosted by Ueda, USTs towards the post-Powell lows into PCE.

- Crude lacklustre, Gold benefits from haven flows & copper dented by Trump tariff details.

- Looking ahead, US Challenger Layoffs, PCE (Jun), Jobless Claims, Employment Wages, Chicago PMI, Atlanta Fed GDPNow, Canadian GDP, SARB Policy Announcement.

- Earnings from Apple, Amazon, Strategy, Coinbase, Reddit, Riot, Cloudflare, Roku, CVS, Roblox, AbbVie, Norwegian Cruise Line, Cigna, Howmet Aerospace, Mastercard & PG&E.

TARIFFS/TRADE

- US President Trump announced that the US has agreed to a "Full and Complete Trade Deal" with South Korea in which South Korea will give the United States USD 350bln for investments owned and controlled by the US, and selected by Trump, while South Korea will also purchase USD 100bln of LNG, or other energy products and South Korea has also agreed to invest a large sum of money for their Investment purposes with this sum to be announced within the next two weeks when the President Lee comes to the White House for a bilateral meeting. Trump added "It is also agreed that South Korea will be completely OPEN TO TRADE with the United States, and that they will accept American product including Cars and Trucks, Agriculture, etc. We have agreed to a Tariff for South Korea of 15%. America will not be charged a Tariff."

- South Korean Presidential Office confirmed US lowered tariffs on South Korean autos to 15% from 25%, while it added that chips and drug tariffs will not be worse than those applied to other countries and stated that USD 200bln of funds are allocated for chips, nuclear power, batteries, and bio sectors. Furthermore, it stated that the rice and beef market will not be opened and that South Korea demanded 12.5% auto tariffs but President Trump insisted on 15%.

- US President Trump posted "I don’t care what India does with Russia. They can take their dead economies down together, for all I care. We have done very little business with India, their Tariffs are too high, among the highest in the World. Likewise, Russia and the USA do almost no business together. Let’s keep it that way, and tell Medvedev, the failed former President of Russia, who thinks he’s still President, to watch his words. He’s entering very dangerous territory!"

- US President Trump will discuss Mexico's plan to cut trade deficit with Mexican President Sheinbaum on Thursday ahead of the August 1st deadline.

- US President Trump plans to sign new executive orders on Thursday, imposing higher tariff rates on several countries that have been unable to reach negotiated trade agreements by Friday deadline, while this could include a number of America's biggest trading partners, including Canada, Mexico and Taiwan, according to POLITICO.

- Pakistan's government said the trade agreement with the US will result in a reduction in reciprocal tariffs, especially on Pakistani exports to the US, and is expected to spur increased US investment in Pakistan’s infrastructure and development projects. Furthermore, it stated that the US–Pakistan deal marks the beginning of economic collaboration in energy, mines and minerals, IT, cryptocurrency, and other sectors.

- US Commerce Secretary Lutnick announced trade deals were made with Cambodia and Thailand. However, the Thai Finance Minister later said they are still working a bit more on the trade proposal to the US and he expects to receive info on US tariffs within 24 hours.

- EU is to give 0% tariff for export quota of 1mln metrics tons of Indonesian crude palm oil a year under free trade agreement, according to an Indonesia official.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.1%) opened higher across the board with a slew of mostly positive earnings from within Europe, and with significant post-earning strength in Meta and Microsoft also boosting sentiment. Though in recent trade, the complex has waned off best levels, with a few indices now slipping into the red; no fresh driver behind this pullback.

- European sectors are mixed, and with a fairly wide breadth of the market. Banks take the top spot, with several European banking reporting today; including from the likes of BBVA (+8%, Bottom line beat), SocGen (+7%, lifts annual targets), Credit Ag (U/C, broadly in-line), Mediobanca (-0.2%, in-line), ING (-0.3%, missed on NII, expects impact following sale of Russian business). Industrials have also been buoyed following key results from within the sector; Airbus (-0.6%, Q2 metrics beat but provided cautious commentary on meeting 2025 delivery target), Safran (+4.6%, Revenue beat and upped its rev. growth outlook for FY), Rolls Royce (+9%, soars after raising profit guidance). Basic Resources is found right at the foot of the pile, pressured by the significant losses seen in copper prices seen in the prior session.

- US equity futures are mixed, with clear outperformance in the NQ (+1.3%) following stunning earnings from Meta and Microsoft which are both higher by 11% and 9% respectively, in pre-market trade.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

AFTER-MARKET EARNINGS

- Meta Platforms Inc (META) Q2 2025 (USD): EPS 7.14 (exp. 5.85), Revenue 47.52bln (exp. 44.87bln); +12% shares pre-market.

- Microsoft Corp (MSFT) Q2 2025 (USD): EPS 3.65 (exp. 3.35), Revenue 76.44bln (exp. 73.76bln); +8% shares pre-market.

- Arm Holdings (ARM) Q1 2026 (USD): Adj. EPS 0.35 (exp. 0.35), Revenue 1.05bln (exp. 1.05bln); -7% shares pre-market.

- Qualcomm Inc (QCOM) Q3 2025 (USD): Adj. EPS 2.77 (exp. 2.70), Revenue 10.37bln (exp. 10.30bln); -6% shares pre-market.

- eBay Inc (EBAY) Q2 2025 (USD): Adj. EPS 1.37 (exp. 1.30), Revenue 2.7bln (exp. 2.64bln); +13% shares pre-market.

- Western Digital Corp (WDC) Q4 2025 (USD): Adj. EPS 1.66 (exp. 1.46), Revenue 2.605bln (exp. 2.46bln); +9% shares pre-market.

FX

- The recent rally in USD has paused for breath after DXY stalled ahead of the 100 mark post-FOMC. To recap, the Fed held rates at 4.25-4.50%, as expected, with Governors Waller and Bowman dissenting in favour of a 25bps cut. In Powell's presser, he said no decision has been made about the September meeting, and they will not let tariffs become inflationary, because they will make sure it does not become serious by deploying their tools. For today's agenda, monthly PCE metrics for June will take centre stage with core M/M PCE expected to pick up to 0.3% from 0.2%. Note, desks expect that inflation is poised for further firming in the coming months. Elsewhere, labour market data in the form of weekly claims and Challenger layoffs are due ahead of tomorrow's crucial NFP print. If the upside in DXY resumes and takes out the 100 mark, the next target will come via the 29th May peak at 100.54.

- EUR/USD is attempting to atone for recent losses, which have been driven by a combination of the fallout from the EU-US trade deal and yesterday's FOMC policy announcement. For the Eurozone, regional CPI metrics have continued to drip feed into the market ahead of the bloc-wide release tomorrow. Metrics from France printed 10bps firmer-than-expected Y/Y on a headline basis but 10bps weaker for the normalised print. Regional CPIs from Germany have seen an uptick on a M/M basis from the prior and mixed Y/Y ahead of the mainland metrics at 13:00BST. EUR/USD has found support just above the 1.14 mark. If the level gives way, the June 10th low sits at 1.1373.

- JPY is softer vs. the USD in the wake of the latest BoJ policy announcement. The BoJ maintained its short-term interest rate target at 0.5%, as expected with the decision made by unanimous vote. The policy statement was one of caution given the uncertainties provided by the trade war and as such, there was little reaction to the release. During the follow-up press conference, JPY upside vs. the USD was pared and USD/JPY made its way back onto a 149 handle after Ueda refrained from any hawkish overtures, whilst emphasising that in the near-term, growth is expected to slow and inflation is set to stall. He also noted that the current FX rate is not diverging far from BoJ assumptions. USD/JPY ventured as high as 149.72. If 150 gives way, that will open up a potential move towards the pre-Liberation Day high at 150.54.

- GBP is slightly firmer vs. the USD with Cable almost entirely at the whim of the USD given how barren the UK docket has been this week. That is set to remain the case until next week's BoE policy announcement, which is 82% priced for a 25bps reduction. Cable remains stuck on a 1.32 handle after delving as low as 1.3228 yesterday.

- Antipodeans both sit towards the top end of the G10 leaderboard following the current upbeat risk sentiment. For AUD, upside has been restricted as better-than-expected Building Approvals and Retail Sales data for Australia were offset by disappointing official Chinese PMI data.

- Brazil Central Bank maintained the Selic rate at 15.00%, as expected, with the decision unanimous and it expects an interruption of the tightening cycle, while it stated it is assessing the accumulated effects of the already implemented adjustment and will evaluate whether the current interest rate level, assuming it remains stable for a very prolonged period, will be enough to ensure inflation convergence to target. BCB said the Committee will remain vigilant and future monetary policy steps can be adjusted, as well as noted it will not hesitate to resume the rate hiking cycle if appropriate.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs entered the Tokyo lunch break at 137.87, within proximity of opening levels. Thereafter, in reaction to the BoJ, JGBs resumed trade a few ticks lower before slipping to a 137.75 session low - it maintained rates. Thereafter, JGBs picked up off that low and made their way to highs around 138.00 into the presser with Governor Ueda. Within this, he struck a dovish tone saying “No large change to central outlook that growth pace will slow down and underlying inflation stalls”, a remark that has seemingly been interpreted as pointing to less of a need to tighten. Following this, JGBs lifted from just above the 138.00 mark to a 138.18 high with upside in excess of 30 ticks.

- USTs currently holds a very modest bullish bias but is essentially contained around the 111-00 mark in a 110-31 to 111-03+ band. Today, the docket is once again packed with earnings while the data docket features PCE before Friday’s jobs; note, there will be another set of employment and inflation data after this week’s before the September Fed. Back to today, PCE is expected 0.3% (prev. 0.1%) M/M and 2.5% (prev. 2.3%) Y/Y). Pantheon, on the data ahead, expects cost-push pressures from tariffs to intensify in the coming months, which should push core goods PCE higher.

- Bunds are also contained, but in a slightly wider 129.46-83 band. This morning, Europe has primarily been digesting the busiest day of earnings thus far (see Equities). No significant move to any of the morning’s data points. Began with hotter-than-expected import prices from Germany (downside of a handful of ticks), French prelim. Inflation came in hotter-than-expected on a harmonised level while the headline figures were somewhat mixed but both dipped from the prior, lifting the benchmark but around 10 ticks. Thereafter, German unemployment was mixed with a lower rate but a smaller than expected change and an increase to the total. Finally, the state CPI’s from Germany saw the M/M conform to the mainland skew (uptick from the prior) while the Y/Y figures were more mixed; fleeting downside to the release. Bunds are modestly firmer into a busy US afternoon that also features the mainland German inflation figures.

- Gilts once again the slight outperformer. But, newsflow for the UK has been essentially non-existent. At the upper-end of a 92.09-27 band, notching a fresh WTD peak. If the move continues, then we look to 92.63 from mid-July.

- Click for a detailed summary

COMMODITIES

- Flat to modestly lower, following a session of gains on Wednesday, continuing to be propped up by the shortened US deadline for Russia to reach a peace deal with Ukraine. WTI Sep resides in a USD 69.72-70.41/bbl while Brent Oct trades in a USD 72.10-72.82/bbl range.

- Mixed trade across precious metals with spot gold the marked outperformer despite a softer Dollar, but with haven flows emanating from tariff woes as the August 1st US tariff negotiation deadline looms. Spot gold resides in a USD 3,276.28-3,314.98/oz range at the time of writing, within yesterday's USD 3,268.12-3,334.09/oz parameter.

- On Wednesday, Comex copper prices slumped over 20% after the White House provided details on the copper tariff, with a universal 50% tariff on imports of semi-finished copper products and copper-intensive derivative products effective August 1st, while refined and concentrate imports will be excluded. 3M LME copper prices reside in a USD 9,575.15-9,820.78/t range while CME prices trade in a USD 4.3332-4.652/lb parameter.

- Kazakhstan Energy Minister says it plans to supply 1.7mln T oil via BTC pipeline in 2025; Russia wants to increase oil transit to China via Kazakhstan by 2.5mln T.

- Russian Deputy PM Novak says discussed situation on the oil market and prospects for cooperating between the two countries within the OPEC+ framework with Saudi Energy Minister.

- India is reportedly mulling options to appease US President Trump following a "shock" 25% tariff level, according to Bloomberg sources; India reportedly mulling upping its natgas purchases from the US, and imports of communication equipment and gold.

- Click for a detailed summary

NOTABLE DATA RECAP

- The state CPI’s from Germany saw the M/M conform to the mainland skew (uptick from the prior) while the Y/Y figures were more mixed.

- German Import Prices YY (Jun) -1.4% vs. Exp. -1.6% (Prev. -1.1%); MM 0.0% vs. Exp. -0.2% (Prev. -0.7%)

- French CPI (EU Norm) Prelim YY (Jul) 0.9% vs. Exp. 0.8% (Prev. 0.9%); MM NSA (Jul) 0.20% vs. Exp. 0.10% (Prev. 0.40%)

- German Unemployment Change SA (Jul) 2.0k vs. Exp. 15.0k (Prev. 11.0k); Unemployment Rate SA (Jul) 6.3% vs. Exp. 6.4% (Prev. 6.3%); Unemployment Total SA (Jul) 2.97M (Prev. 2.972M); Unemployment Total NSA (Jul) 2.979M (Prev. 2.914M)

- Italian CPI (EU Norm) Prelim YY (Jul) 1.7% vs. Exp. 1.6% (Prev. 1.8%); Consumer Price Prelim MM (Jul) 0.4% vs. Exp. 0.1% (Prev. 0.2% CPI (EU Norm); Prelim MM (Jul) -1.0% vs. Exp. -1.0% (Prev. 0.2%); Consumer Price Prelim YY (Jul) 1.7% vs. Exp. 1.5% (Prev. 1.7%)

- EU Unemployment Rate (Jun) 6.2% vs. Exp. 6.3% (Prev. 6.3%, Rev. 6.2%)

NOTABLE EUROPEAN HEADLINES

- German Finance Minister urged cabinet ministers to cut spending to close the budget gap of over EUR 30bln in 2027, via an interview with Ard-Tagesthemen.

NOTABLE US HEADLINES

- China reportedly summons NVIDIA (NVDA) on H20 chip backdoor security risk, according to Bloomberg.

- BofA institute Total Card Spending (w/e July 26th) +0.9% Y/Y (prev. +1.8%) (June avg. +0.2%).

- US Senator Warren (D) sent a letter to Commerce Secretary Lutnick asking that new rules developed by the Ministry maintain incentives for companies to keep computing infrastructure in the US, according to Punchbowl

GEOPOLITICS

- Canadian PM Carney said Canada intends to recognise the state of Palestine at the 80th session of the UN General Assembly in September. Israel's Foreign Ministry commented shortly after that Israel rejects the statement by Canada’s PM over planned recognition of Palestinian state, and the change in the position of the Canadian government at this time is a reward for Hamas and harms efforts to achieve a ceasefire in Gaza and a framework for the release of the hostages.

- US imposed sweeping new sanctions on a vast international oil trading network which it claimed has funnelled tens of billions of dollars in oil revenue to Iran, according to FT.

CRYPTO

- Bitcoin is a little firmer and trades around USD 118.5k whilst Ethereum is just shy of USD 3.9k.

APAC TRADE

- APAC stocks traded mixed in the aftermath of a hawkish Powell and strong mega-cap earnings stateside, while participants also digested the US-South Korea trade deal, disappointing Chinese PMIs and the BoJ policy announcement at month-end.

- ASX 200 was lacklustre amid losses in miners following weaker H1 earnings from Rio Tinto and with a record drop seen in copper prices after the Trump administration excluded refined copper from planned 50% tariffs.

- Nikkei 225 outperformed and reclaimed the 41,000 level after recent currency weakness and better-than-expected Industrial Production & Retail Sales from Japan, while the BoJ policy provided no major fireworks as the central bank kept its short-term rates unchanged but highlighted trade-related uncertainty and raised its Core CPI projections.

- Hang Seng and Shanghai Comp were pressured following disappointing official PMI data in which the headline Manufacturing and Non-Manufacturing PMI figures missed expectations with the former remaining in contraction territory.

BOJ

ANNOUNCEMENT:

- BoJ maintained its short-term interest rate target at 0.5%, as expected with the decision made by unanimous vote, while it noted that underlying inflation is likely to stall due to slowing growth but will gradually accelerate thereafter and underlying consumer inflation likely to be at a level generally consistent with the 2% target in the second half of the projection period from fiscal 2025 through 2027. BoJ stated that uncertainty over trade policy and its developments, and their impact on the economic and price outlook, remains high and noted that real interest rates are at extremely low levels, while it must have no preconception in judging whether the economy and prices are moving in line with the forecast. BoJ reiterated that it will conduct monetary policy as appropriate from the perspective of sustainably and stably achieving the 2% inflation target and will continue to raise the policy rate if the economy and prices move in line with the forecast, in accordance with improvements in the economy and prices. Furthermore, it noted there is high uncertainty surrounding trade policy developments and their impact on the economy and stated that a prolonged period of high uncertainties regarding trade policies could lead firms to focus more on cost-cutting and as a result, moves to reflect price rises in wages could also weaken. In terms of the latest Outlook Report, board members' median forecasts for Core CPI were raised through to 2027, while the median forecast for Real GDP was upgraded for FY25 but maintained for the following two years after.

UEDA

- Rising wages at Japanese firms are becoming the norm in recent years.

- No large change to central outlook that growth pace will slow down and underlying inflation stalls. Moves to pass on rising costs to prices continue. Underlying inflation could slow down in line with slowdown in economic growth. Underlying inflation is gradually rising; not in phase of stalling due to tariffs. Wage impact on prices not picking up too fast. Even if economy and prices undershoot BoJ projections, need to keep in mind that policy rates are low at 0.5%.

- Current FX rate not diverging far from BoJ assumptions.

- Will continue to raise policy rate if economy and prices move in line with forecasts, in accordance with improvement in economy and prices. Policy decision would not depend solely on new CPI forecasts.

DATA RECAP

- Chinese NBS Manufacturing PMI (Jul) 49.3 vs. Exp. 49.7 (Prev. 49.7); Non-Manufacturing PMI (Jul) 50.1 vs. Exp. 50.3 (Prev. 50.5)

- Chinese Composite PMI (Jul) 50.2 (Prev. 50.7)

- Japanese Industrial O/P Prelim MM SA (Jun) 1.7% vs. Exp. -0.6% (Prev. -0.1%)

- Japanese Retail Sales YY (Jun) 2.0% vs. Exp. 1.8% (Prev. 2.2%, Rev. 1.9%)

- Australian Building Approvals (Jun) 11.9% vs. Exp. 2.0% (Prev. 3.2%)

- Australian Retail Sales MM Final (Jun) 1.2% vs. Exp. 0.4% (Prev. 0.2%)

- Australian Retail Trade (Q2) 0.3% (Rev. 0.1%)