US Market Open: Major indices entirely in the red after Trump tariff announcement; Fed speak & NFP ahead

01 Aug 2025, 11:20 by Newsquawk Desk

- US President Trump announced tariffs on countries ranging from 10%-41% including a tariff rate of 10% for Brazil, 30% for South Africa, 20% for Taiwan and 25% for India. Canada’s tariff increased from 25% to 35%, while Mexico received a 90-day extension of the current tariff rates.

- Japan eyes a 15% rate for the US chip tariff, on par with EU, with Japan’s trade negotiator stating Japan should be able to secure a 15% rate for the new sectoral tariff the US is planning to impose on chips, according to Nikkei.

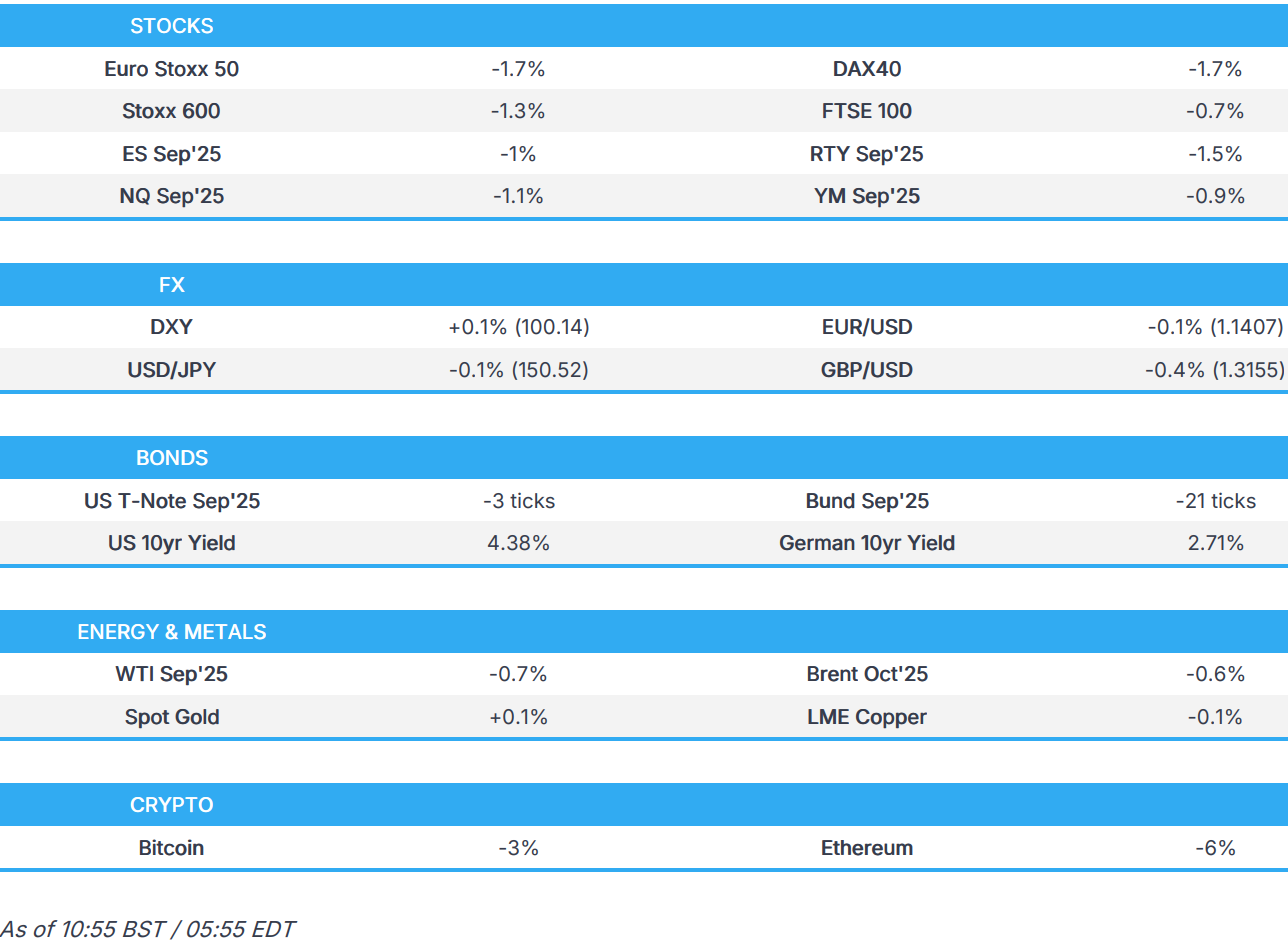

- European and US indices are entirely in the red in reaction to the Trump’s latest tariff levy; AMZN -8% & AAPL +2% post-earnings.

- USD is broadly firmer vs. peers as NFP looms large; CHF/NZD pressured after the respective countries received tariff hikes.

- USTs are near enough flat, Bunds are softer but unreactive to HICP, Gilts heavy.

- Crude is on the backfoot, gold awaits NFP, copper stable.

- Looking ahead, Global Manufacturing PMI (Finals), US NFP, ISM Manufacturing, UoM Sentiment Final, Atlanta Fed GDPNow, Speakers including Fed's Bowman, Waller (Unconfirmed), Hammack.

- Earnings from, Earnings from Exxon, Chevron, Regeneron & Colgate.

TARIFFS/TRADE

- US President Trump announced tariffs on countries ranging from 10%-41% including a tariff rate of 10% for Brazil, 30% for South Africa, 20% for Taiwan and 25% for India, while the order stated "These modifications shall be effective with respect to goods entered for consumption, or withdrawn from warehouse for consumption, on or after 12:01 a.m. eastern daylight time 7 days after the date of this order".

- White House said President Trump signed an executive order modifying reciprocal tariff rates for certain countries, with the tariff on Canada increased from 25% to 35% effective August 1st, while it added that Trump determined it is necessary and appropriate to modify the reciprocal tariff rates for certain countries. Furthermore, it stated that countries listed in Annex I of the executive order will be subject to the tariff specified therein and countries not listed in Annex I will be subject to a 10% tariff, while goods transhipped to evade the 35% tariff on Canada will be subject instead to a transshipment tariff of 40%.

- US official said that if the US has a surplus with a country, the tariff rate is 10% and small deficit nations have a 15% tariff, while they are still working out technicalities of rules of origin terms for transshipment and will implement rules of origin details in the coming weeks. The official said the US has more trade deals to come and the challenge with India includes geopolitical differences over BRICS and Russia, as well as noted that differences with India cannot be resolved overnight and there is no final decision on China.

- US President Trump said on Thursday that they just made a couple of other trade deals a little while ago and later commented that Canada's stance on a Palestinian state is not a deal-breaker. Trump also commented he may speak with Canadian PM Carney on Thursday night and he is open to further talks with Canada and open to more deals.

- US Commerce Secretary Lutnick said the China trade extension is up to US President Trump, while he stated if Canadian PM Carney complies, "maybe" Trump will reduce tariffs on Canada, but added that the 35% Trump sent in the letter is surely on the cards.

- White House Trade Adviser Navarro said the US is moving forward on progress with India, Canada and China, according to Fox News.

- Mexico’s Economy Minister Ebrard said the 90-day deal with the US was achieved without a concession from Mexico and they are moving closer to the renewal of their trade deal with the US. Ebrard separately commented that the tariff debate with the US includes concerns about intellectual property and the rules of origin panel, while he added that they have to address those issues from the perspective of revising the USMCA.

- Malaysian Trade Minister says "Pharma and Semiconductors are exempted from US tariffs".

- Swiss Economy Ministry understands that the 39% tariff rate does not apply to pharmaceuticals.

- PBoC Deputy Governor met with US business delegation on July 29th, according to a statement, two sides had in-depth talks on US-Sino relations; China's macroeconomic policies and the opening up of financial industry.

- India is engaged with US for further trade talks; US delegation to visit Delhi on August 24th, according to Reuters sources; India expects USD 40bln exports to impacted by the high US tariffs

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.3%) opened entirely in the red, and has continued to trundle lower as the August 1st tariff deadline passed. US President Trump announced new rates on 92 countries, which brought the average US tariff rate to 15.2% (prev. 13.3%, prev. 2.3% pre-Trump).

- European sectors are entirely in the red, in-fitting with the risk tone. Media is found right at the bottom of the sectoral list, pressured by post-earning losses in UMG (-6.3%); the Co. lowered its earnings forecast and highlighted rising content costs. Tech is also on the backfoot, as the sector cools from recent upside and as the risk-tone weighs.

- Healthcare completes the bottom three, with US President Trump to blame; he sent letters to 17 pharma companies (in both US and Europe), asking them to lower drug prices before the end of September. The likes of Novo Nordisk (-4%) and GSK (-1.7%) both move lower, but are off worst levels.

- US equity futures (ES -1% NQ -1.2% RTY -1.5%) are entirely in the red, as the August 1st deadline crosses, and as the US announced the latest modifications to world tariffs.

- There has also been two more earnings releases from the Magnificent 7; Apple (+1.8%) reported Q3 revenues above expectations, driven by strong iPhone 16 demand and a rebound in China. It guided Q4 revenue rising mid- to high-single digits, topping expectations (exp. 3%). Amazon (-8%) shares fall in the pre-market after guiding Q3 operating income below expectations; slower AWS growth and lack of visible returns from AI investment weighed on sentiment.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

AFTER-MARKET EARNINGS

- Amazon.com Inc (AMZN) Q2 2025 (USD) EPS 1.68 (exp. 1.33), Rev. 167.7bln (exp. 161.91bln), AWS net sales 30.9bln (exp. 30.77bln): Co. shares -8% pre-market

- Apple Inc (AAPL) Q3 2025 (USD): EPS 1.57 (exp. 1.43), Rev. 94.04bln (exp. 89.29bln), iPhone rev. 44.58bln (exp. 44.52bln), Services rev. 27.42bln (exp. 26.80bln), Mac rev. 8.05bln (exp. 7.26bln), iPad rev. 6.58bln (exp. 7.24bln), Wearables, Home & Accessories net sales 7.40bln (exp. 7.82bln), Americas rev. 41.20bln (vs. 37.68bln y/y), Greater China rev. 15.37bln (exp. 15.12bln): Co. shares +2% pre-market

FX

- DXY began steady with the USD showing a mixed performance vs. peers. Markets are currently digesting the fallout from the latest executive orders from US President Trump, which has seen the imposition of tariffs on countries ranging from 10%-41%. This includes a tariff rate of 10% for Brazil, 30% for South Africa, 20% for Taiwan and 25% for India. Canada’s tariff increased from 25% to 35%, while Mexico received a 90-day extension of the current tariff rates. Accordingly, the average US tariff rate has risen to 15.2% (prev. 13.3%; 2.3% pre-Trump). It's also worth noting that the July payrolls release looms large with consensus looking for the rate of job growth to slow to 110k from 147k and the unemployment rate to rise to 4.2% from 4.1%. A soft outturn could reignite expectations of a September cut. Elsewhere, ISM manufacturing data is also due on deck and we expect to hear statements from Waller and Bowman on the justification of their dissent. As the morning progressed, the DXY gained a firm footing on a 100 handle with a current session high at 100.25.

- EUR steady vs. the USD with a firmer-than-expected outturn for Eurozone inflation unable to provide much traction for the shared currency. HICP Y/Y for July remained at the 2% target (Exp. 1.9%), whilst both core metrics came in 10bps over consensus, and services declined to 3.1% from 3.3%. For now, today's NFP print is likely to provide the greatest source of traction for EUR/USD. Again, as the morning has progressed, the mentioned USD pickup has weighed with EUR/USD now just sub-1.14.

- JPY is marginally firmer vs. the USD in what has been a bruising week for the Yen vs. the dollar. Part of this has been a USD story and part has been stemming from the fallout from the latest Japan deal, political uncertainty and a reticence yesterday for the BoJ to attempt to bolster rate hike bets. The Yen depreciation has not gone unnoticed in Tokyo with the Japanese Finance Minister Kato stating that he is "alarmed over FX moves". On the trade front, the Nikkei reports that Japan is eyeing a 15% rate for the US chip tariff, which would be on par with the EU. After hitting a multi-month high at 150.91 overnight, USD/JPY has pulled back but remains above the 150 mark and its 200DMA at 149.56.

- GBP remains on the backfoot vs. the USD with Cable extending its losing streak to a 7th session in a row. It remains the case that macro drivers for the UK remain on the light side, however, next week will see the latest BoE policy announcement and MPR, which is 82% priced for a 25bps reduction. Cable has slipped onto 1.31 handle for the first time since 13th May with a session low at 1.3142.

- NZD is underperforming its antipodean peer in the wake of the latest Trump tariff announcements, which has seen the rate for New Zealand increase to 15% from 10% and Australia hold steady at 10%.

- PBoC set USD/CNY mid-point at 7.1496 vs exp. 7.2033 (Prev. 7.1494).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are slightly softer on the final day of a very busy week. For today, the highlights are July’s NFP report, ISM Manufacturing and expected explanations of dissent from Fed’s Bowman and Waller. Thus far, USTs have been holding around the low end of a 110-28+ to 111-00+ band. The bearish bias this morning appears to be tariff-induced (i.e. higher inflation, firmer yields). For NFP, the headline is seen at 110k (prev. 147k), Unemployment Rate at 4.2% (prev. 4.1%); post-Fed, Chair Powell said the unemployment rate is the figure to watch.

- Bunds are in the red, to a slightly larger degree than USTs but faring better than Gilts (see below). Pressure this morning is likely a function of the latest tariff measures from Trump, measures which have seen tariff increases for several key economies and as such biased yields across the curve with a clear steepening bias in the early morning; though, this does come after a period of flattening for the curve. No significant reaction to any of the morning’s PMI data (the EZ-wide figure was unrevised). The day’s main EZ event was July’s Flash HICP, printed hotter than expected for the three main Y/Y metrics with all measures remaining at the prior rate - again no real move.

- Gilts are on the back foot. No fixed income pertinent newsflow specifically for the UK. Pressure is likely a function of the global inflation implications of the latest tariff measures, as discussed. Currently, Gilts are lagging peers. However, this seems to be more a function of the bouts of relative outperformance seen over the last few days rather than a UK specific. Currently, at a 91.49 low and, despite the extensive 91.16-92.28 WTD range, set to end the week with near enough unchanged.

- Click for a detailed summary

COMMODITIES

- Crude is on the backfoot following Thursday's macro-induced losses as markets awaited Trump's revised tariffs. In terms of the highlights from the announcement, the average US tariff rate has now risen to 15.2% (prev. 13.3%; 2.3% pre-Trump). China was not mentioned; EU/UK/Japan had their rates as agreed; Switzerland, New Zealand, and Canada's tariffs were increased, while Mexico pays a lower tariff for 90 days. WTI resides in a 68.70-69.55/bbl range while Brent sits in a USD 71.18-72.00/bbl range.

- Precious metals are mostly softer despite a relatively stable dollar (DXY oscillates around 100) and despite of the broad downbeat risk tone. Focus today on NFP, ISM Manufacturing and Fed speak. Spot gold resides in a USD 3,281.74-3,300.54/oz range at the time of writing, within Thursday's USD 3,276.28-3,314.98/oz parameter.

- 3M LME Copper is relatively stable following Thursday's slide, which saw the CME-LME arb collapse as the US copper tariff was not as bad as feared, as the 50% tariff applied to copper pipes and wiring, whilst omitting copper input materials such as ores, concentrates and cathodes. 3M LME copper prices reside in a USD 9,597.85-9,696.30/t range.

- Codelco said a worker died and nine were injured with five missing at the Andesita mine at El Teniente in Chile after a seismic event.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HICP Flash YY (Jul) 2.0% vs. Exp. 1.9% (Prev. 2.0%); Services 3.1% (prev. 3.3%); YY (Jul) 2.4% vs. Exp. 2.3% (Prev. 2.4%); HICP-X F, E, A & T Flash YY (Jul) 2.3% vs. Exp. 2.2% (Prev. 2.3%).

- EU HCOB Manufacturing Final PMI (Jul) 49.8 vs. Exp. 49.8 (Prev. 49.8)

- Spanish HCOB Manufacturing PMI (Jul) 51.9 vs. Exp. 51.5 (Prev. 51.4)

- Italian HCOB Manufacturing PMI (Jul) 49.8 vs. Exp. 49.0 (Prev. 48.4)

- French HCOB Manufacturing PMI (Jul) 48.2 vs. Exp. 48.4 (Prev. 48.4)

- German HCOB Manufacturing PMI (Jul) 49.1 vs. Exp. 49.2 (Prev. 49.2)

- UK S&P Global Manufacturing PMI (Jul) 48.0 vs. Exp. 48.2 (Prev. 48.2)

- UK Nationwide House Price MM (Jul) 0.6% vs. Exp. 0.3% (Prev. -0.8%, Rev. -0.9%); YY 2.4% vs. Exp. 2.1% (Prev. 2.1%)

- Italian Retail Sales NSA YY (Jun) 1.0% (Prev. 1.3%); Retail Sales SA MM (Jun) 0.6% (Prev. -0.4%)

NOTABLE US HEADLINES

- US President Trump criticised Fed Chair Powell in which he called him 'Too late' and said he is a terrible Fed Chair.

GEOPOLITICS

- US President Trump said Iran has been acting very badly and their nuclear capability was decimated but added that Iran can start again.

- US President Trump said it is disgusting what Russia is doing and they are going to put sanctions on Russia.

- China cyber association accused the US of a cyberattack on the defence sector to steal secrets, according to Bloomberg.

- Ukrainian Presidential Office head says Ukrainian partners confirm "positive signals" from the White House on Russia sanctions.

CRYPTO

- Bitcoin is on the backfoot, and trades back below the USD 115k mark - downside which is in-fitting with the broader risk tone.

APAC TRADE

- APAC stocks traded mostly subdued following the weak handover from US peers and as participants digested the latest Trump tariff adjustments ahead of the deadline and with the key US Non-Farm Payrolls report on the horizon.

- ASX 200 was pressured with underperformance in tech, healthcare and financials leading the declines in most sectors as sentiment is dampened amid trade uncertainty.

- Nikkei 225 slumped at the open but was well off today's worst levels with a rebound facilitated by recent currency weakness.

- Hang Seng and Shanghai Comp were lacklustre mood following the latest S&P Global China General Manufacturing PMI (formerly sponsored by Caixin) which missed forecasts and surprisingly returned to contractionary territory.

- US equity futures lacked demand after declining on Thursday and with little impact seen following the mixed fortunes in the likes of Apple and Amazon post-earnings.

NOTABLE ASIA-PAC HEADLINES

- China's MOFCOM announced tax credit policies related to direct investment by foreigners.

DATA RECAP

- Chinese S&P Global China General Manufacturing PMI (formerly sponsored by Caixin) (Jul) 49.5 vs. Exp. 50.4 (Prev. 50.4)