Europe Market Open: Weekend newsflow quiet & light calendar ahead; OPEC+ agree to increase output by 548k BPD as expected

04 Aug 2025, 07:00 by Newsquawk Desk

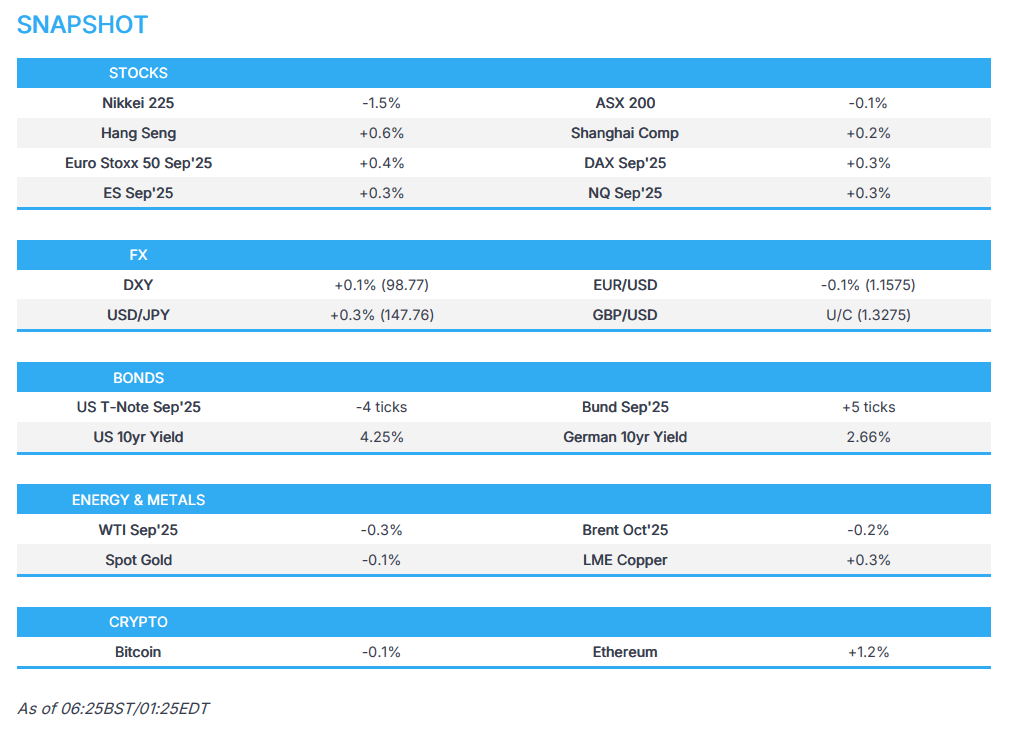

- APAC stocks traded mixed following a quiet weekend of newsflow and last Friday's disappointing Non-Farm Payrolls data.

- US President Trump said on Sunday that he will announce a new head of BLS in the next three or four days.

- US President Trump said he is to announce a replacement for Fed's Kugler in the next couple of days after Kugler resigned on Friday.

- European equity futures indicate a positive cash market open with the Euro Stoxx 50 future up 0.4% after the cash market suffered losses of 2.9% on Friday.

- DXY is a touch firmer after Friday's selling pressure, EUR/USD ran out of steam ahead of 1.16, USD/JPY trades on a 147 handle.

- Crude slightly lower after OPEC+ agreed to increase oil output by 548k BPD in September.

- Looking ahead, highlights include Swiss CPI (Jul), EZ Sentix Index Aug), US Employment Trends (Jun), Durable Goods R (Jun) & Factory Orders.

SNAPSHOT

US TRADE

EQUITIES

- US stocks declined amid a risk-off session on Friday in response to the woeful US jobs report but also as Trump implemented sweeping tariffs, whereby the overall tariffs raised the average US tariff rate to 15.2% from 13.3%, and up from 2.3% before Trump took office. The NFP report came in beneath expectations but the highlight was the two month net revisions of -258k, bringing the 3 month average to just 35k from the prior 150k, seeing traders boost Fed rate cut bets with September now priced at around 90% vs sub-50% pre-data, while equities had also faced pressure from the downside in Amazon (AMZN) after earnings too.

- SPX -1.65% at 6,235, NDX -1.96% at 22,763, DJI -1.24% at 43,586, RUT -2.08% at 2,166.

- Click here for a detailed summary.

TARIFFS/TRADE

- USTR Greer said the trade truce deadline for China is still under discussion.

- Canada’s trade envoy LeBlanc said PM Mark Carney and US President Donald Trump are expected to talk “over the next number of days” after a failure by their countries to reach a deal before the Aug. 1st tariff deadline, while LeBlanc plans to speak with US Commerce Secretary Lutnick and still sees a chance to ease Trump tariffs, according to Bloomberg.

- Canadian ministers are to discuss trade in meetings with Mexico's President Sheinbaum and government officials, according to The Globe and Mail.

- Brazil’s Finance Minister Haddad said they will have a meeting with US Treasury Secretary Bessent in the week ahead and will clarify in the meeting how the Brazilian justice system works.

- China is reportedly choking the supply of critical minerals to Western defence companies, according to WSJ.

- Japanese Economy Minister Akazawa said the US is attempting to alter the rules and norms of global trade, while he stated that waiting for a deal in writing might have delayed a levy cut.

NOTABLE HEADLINES

- US President Trump said he would remove Fed Chair Powell in a heartbeat but added that removing Powell would disturb the market, while he stated Powell will most likely stay on as Chair and he will appoint a new Fed Chair once Powell’s term ends.

- US President Trump said he is to announce a replacement for Fed's Kugler in the next couple of days after the Fed announced on Friday that Governor Kugler is resigning from the Fed board effective August 8th.

- US President Trump said on Friday that he was informed the US jobs numbers are being produced by a Biden appointee who faked job numbers before the election to try to boost Kamala Harris’s chances of victory, and he directed his team to fire her immediately. Furthermore, Trump said on Sunday that he will announce a new head of BLS in the next three or four days, while he also commented that there could be a dividend or distribution of money to Americans from tariff revenues.

- Fed’s Williams said he is going into the September meeting with an open mind and that modestly restrictive policy is still needed, while he added the unusually large downward revisions in May and June payrolls were really the news in the report.

- Apple (AAPL) CEO Cook said he intends to win the AI race and will make the appropriate investments to do so.

- Boeing (BA) defence workers are set to strike on Monday after the Co.’s St. Louis employees rejected the latest offer, while Boeing stated that it is prepared for a strike and has fully implemented its contingency plan.

APAC TRADE

EQUITIES

- APAC stocks traded mixed following a quiet weekend of newsflow and last Friday's disappointing Non-Farm Payrolls data.

- ASX 200 was subdued amid underperformance in the top-weighted financials sector and with weakness also seen in energy, Industrials and tech, although losses were stemmed by resilience in defensives and miners.

- Nikkei 225 underperformed after recent currency strength and briefly dipped back beneath the 40k level.

- Hang Seng and Shanghai Comp were kept afloat amid earnings and corporate updates, while the PBoC announced last week that it is to expand the issuance scale of sci-tech bonds and promote cross-border financing facilitation, as well as strengthen the implementation and supervision of interest rate policies.

- US equity futures (ES 0.3%, NQ +0.3%) got some slight reprieve following last Friday's data, tariff and earnings-facilitated sell-off.

- European equity futures indicate a positive cash market open with the Euro Stoxx 50 future up 0.4% after the cash market suffered losses of 2.9% on Friday.

FX

- DXY regained some composure after retreating on Friday owing to the weak Non Farm Payrolls report which printed below estimates and was accompanied by hefty downward two-month net revision. The disappointing data led to a boost in Fed rate cut bets with money markets currently pricing in around a 90% probability of a cut at next month's FOMC meeting vs below 50% prior to the data, while President Trump also fired the head of the BLS who he claimed had "RIGGED" jobs figures to make him and Republicans look bad.

- EUR/USD took a breather after Friday's spike higher and after hitting some resistance just shy of the 1.1600 handle.

- GBP/USD traded little changed in the absence of pertinent catalysts for the UK over the weekend and languished in relatively close proximity for a retest of the 1.3300 level to the upside.

- USD/JPY attempted to nurse losses after collapsing on Friday from above 150.00 to sub-148.00 territory in the aftermath of the US jobs data but with the rebound limited amid the downbeat mood in Tokyo and with a lack of tier-1 releases from Japan at the start of the week.

- Antipodeans held on their post-NFP spoils with slight tailwinds in AUD/USD following a rise in the latest MI Inflation Gauge.

FIXED INCOME

- 10yr UST futures slightly pulled back after rallying on the dismal US jobs report on Friday which resulted in money markets pricing around a 90% likelihood of a Fed rate cut at the next meeting in September.

- Bund futures held on to the post-NFP spoils but with upside capped after failing to sustain the 130.00 status.

- 10yr JGB futures followed suit to last Friday's gains in global peers amid the negative mood in Tokyo, although JGBs are off today's peak after hitting some resistance during a brief test of the 139.00 level.

COMMODITIES

- Crude futures were mildly lower with pressure seen at the open following the OPEC+ decision on Sunday to raise output by 547k bpd for September and with OPEC+ 8 to meet next on September 7th, where they could discuss returning another layer of output cuts of 1.65mln bbls. Nonetheless, prices are off their lows as the latest output increase was relatively in line with expectations, while Goldman Sachs maintained its 2026 Brent crude forecast and sees OPEC+ pausing future hikes amid rising OECD stockpiles.

- OPEC+ said in a statement that eight members are to raise oil output by 547k bpd in September, citing steady global economic and current healthy market fundamentals, while it stated that eight OPEC+ countries are to meet next on September 7th and sources noted the group may discuss returning another layer of cuts of 1.65mln bbls which are in place until end-2026, according to Reuters.

- Kuwait’s Oil Minister praised the OPEC+ decision to raise output and said the meeting reflects continued coordination among participating countries to ensure the stability of the oil market, while he added that the decision was based on thorough analysis of market data regarding production inventories and future expectations.

- Libya’s Sharara oilfield reached its highest production since 2018 at nearly 311k bpd.

- Azerbaijan is to export 1.2bcm of gas to Syria each year from BP-led Shah Deniz gas field.

- Spot gold marginally eased back after Friday's data-triggered surge and as the dollar regained poise.

- Copper futures were lacklustre with demand contained alongside the mixed risk appetite in Asia-Pac.

CRYPTO

- Bitcoin gained overnight and briefly tested the 115k level to the upside.

NOTABLE ASIA-PAC HEADLINES

- India's capital markets regulator called for structural reforms to the country's vast derivatives market, according to FT.

DATA RECAP

- Australian Melbourne Institute Inflation Gauge MM (Jul) 0.9% (Prev. 0.1%)

- Australian Melbourne Institute Inflation Gauge YY (Jul) 2.9% (Prev. 2.4%)

GEOPOLITICS

MIDDLE EAST

- Hamas said it won’t disarm unless an independent Palestinian state is established. It was separately reported that Hamas’s armed wing said it is ready to respond positively and cooperate with any request from the Red Cross to deliver food to hostages in Gaza, while it added that Israel must stop aerial operations during the delivery of aid to hostages.

- Jordan’s armed forces said two armed people were killed after a foiled infiltration attempt through its border with Syria.

- Syrian Defence Ministry said an attack by Syrian Defence Forces in the northern city of Mamjib injured four army personnel and three civilians.

RUSSIA-UKRAINE

- Russian Defence Ministry said Russian forces captured the village of Oleksandro Kalynove in Eastern Ukraine.

- IAEA team at Ukraine’s Zaporizhzhia Nuclear Power Plant heard explosions and saw smoke coming from a nearby location where the plant said one of its auxiliary facilities was attacked.

- Ukraine’s military said it struck Russia’s Ryazan oil refinery again.

- US President Trump said there will be sanctions if Russia does not stop the war, but added that Russia seems to be good at avoiding sanctions, while he stated that special envoy Witkoff will be going to Russia on Wednesday or Thursday.

- US President Trump ordered two nuclear submarines to be positioned in the appropriate regions on Friday, "just in case these foolish and inflammatory statements” from Russia's Medvedev are more than just that.

- Indian officials said they will continue to buy Russian oil despite threats of additional tariffs from US President Trump’s administration.

OTHER

- Russia-China navy exercises began in the Sea of Japan, according to TASS.

EU/UK

NOTABLE HEADLINES

- UK's FCA proposed a redress scheme for motor finance claims which could cost banks up to GBP 18bln, according to FT.