US Market Open: Stocks firmer, Trump to announce Fed Kugler's replacement this week; quiet calendar ahead

04 Aug 2025, 10:50 by Newsquawk Desk

- US President Trump said on Sunday that he will announce a new head of the BLS in the next three or four days.

- US President Trump said he is to announce a replacement for Fed's Kugler in the next couple of days after Kugler resigned on Friday.

- OPEC+ said in a statement that eight members are to raise oil output by 547k bpd in September, citing steady global economic and current healthy market fundamentals; crude slips.

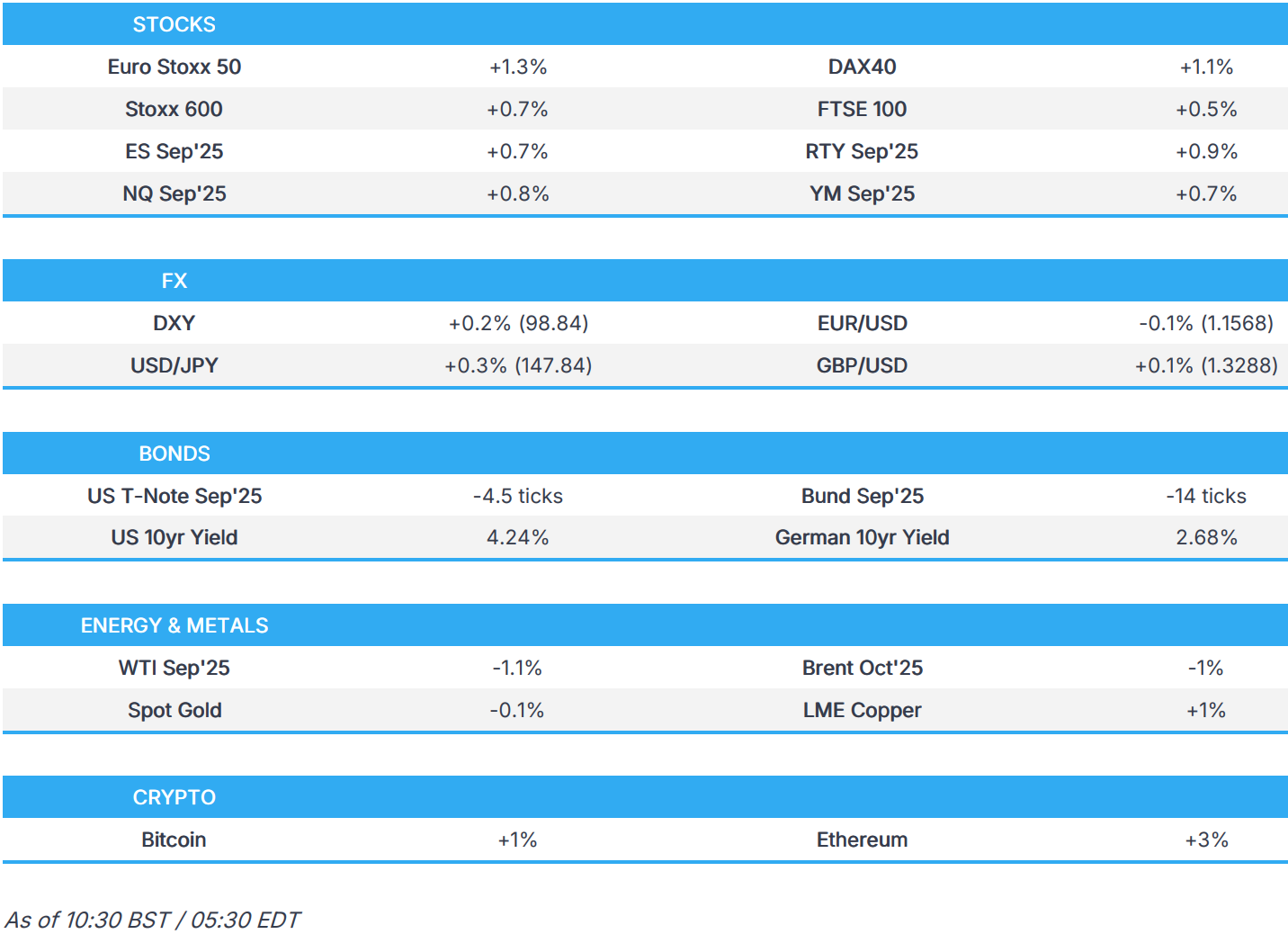

- European bourses are mostly higher, but with clear underperformance in the SMI as the region returns from holiday; US futures are broadly higher.

- USD is attempting to claw back some of Friday's lost ground; havens lag with clear underperformance in the CHF.

- Bonds are paring the NFP upside, but with focus on dovish implication of Fed's Kugler resignation & the BLS firing.

- Looking ahead, US Employment Trends (Jun), Durable Goods R (Jun) & Factory Orders, Earnings from Palantir, Hims & Hers, Wayfair, BioNTech & Tyson Foods. Holiday: Canadian Civic Holiday.

TARIFFS/TRADE

- USTR Greer said the trade truce deadline for China is still under discussion.

- Canada’s trade envoy LeBlanc said PM Mark Carney and US President Donald Trump are expected to talk “over the next number of days” after a failure by their countries to reach a deal before the Aug. 1st tariff deadline, while LeBlanc plans to speak with US Commerce Secretary Lutnick and still sees a chance to ease Trump tariffs, according to Bloomberg.

- Canadian ministers are to discuss trade in meetings with Mexico's President Sheinbaum and government officials, according to The Globe and Mail.

- Brazil’s Finance Minister Haddad said they will have a meeting with US Treasury Secretary Bessent in the week ahead and will clarify in the meeting how the Brazilian justice system works.

- China is reportedly choking the supply of critical minerals to Western defence companies, according to WSJ.

- Japanese Economy Minister Akazawa said the US is attempting to alter the rules and norms of global trade, while he stated that waiting for a deal in writing might have delayed a levy cut.

- EU said to be awaiting US President Trump's actions on its car tariffs and exemptions this week, according to Bloomberg.

EUROPEAN TRADE

EQUITIES

- European equities (STOXX 600 +0.6%) began the week in the green (ex. SMI), and have continued to climb higher as the session progressed. The SMI (-0.6%) underperforms as it reacts to the US unexpectedly raising tariffs on Swiss goods to 39% (from 31%); as a reminder, Switzerland was on holiday last Friday.

- European sectors began mixed, though as the session has progressed, the picture looks more positive. Banks reside at the top and Healthcare at the bottom; the latter is hampered by heavyweight Novartis (-0.5%), given the broader pressure across Swiss stocks.

- Stateside, equity futures (ES +0.7%, NQ +0.8%, RTY +0.9%) have been firming throughout the morning with some modest outperformance in the RTY after closing with significant losses on Friday.

- Tesla (TSLA) sold 67,886 China-made vehicles in July (vs. 71,599 in June), according to China's CPCA.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has started the week off on the front foot but gains are very modest in comparison to the post-payrolls downside on Friday, which saw the index close lower by 1.4%. The knock-on impact to Fed pricing means that markets price an 89% chance of a 25bps cut next month and a total of 59bps of loosening by year-end. This also comes in the context of a potentially more dovish composition of the FOMC with US President Trump set to name Kugler's replacement in the coming days. Elsewhere on the personnel front, Trump is also set to announce the replacement for the head of the BLS, whom he fired on Friday, claiming that they "faked job numbers" before the election in an attempt to help his political rivals. DXY has been unable to make its way back onto a 99 handle with a current session peak at 98.97.

- EUR/USD is on the backfoot after a choppy week last week, which saw EUR slide against the USD in the wake of the EU-US trade deal before mounting a partial recovery on Friday post-payrolls. The macro narrative surrounding the EU remains as it was, and that could remain the case with little in the way of market-moving scheduled releases for the Eurozone this week. EUR/USD failed to crack 1.16 to the upside, topping out at 1.1597 and has since slipped back below its 200DMA at 1.1581 with a session low at 1.1551.

- After a wild week last week, which saw an initial rally in USD/JPY (on account of broad USD strength and a dovish reaction to the BoJ policy announcement) swiftly reversed in the wake of the US NFP report, USD/JPY is attempting to clamber off the lows. USD/JPY delved as low as 147.07 overnight (vs. Friday's 147.28 trough) but has since recovered to levels closer to 148 as the USD attempts to atone for recent losses. Overnight, comments from Japanese Trade Negotiator Akazawa stated that the recently announced trade agreement between the US and Japan is not a legally binding commitment. This has raised some doubts over how rigidly Japan will stick to its existing pledges with the US.

- GBP is fractionally lower vs. the USD with incremental macro drivers from the UK on the light side. That will change on Thursday with the latest BoE policy announcement and MPR, which is 82% priced for a 25bps reduction. Within the vote split, Morgan Stanley expects a 1:7:1 outcome with Mann voting for a hold and Dhingra voting for a 50bp cut. Additionally, the desk expects unchanged messaging and an uplift to near-term inflation forecasts. Cable has returned to a 1.32 handle but is still enjoying the bulk of Friday's gains, trading in a 1.3254-93 range.

- Antipodeans are both slightly softer vs. the USD but holding onto a bulk of their post-NFP gains. AUD is slightly more resilient than NZD following a rise in the latest Melbourne Institute Inflation Gauge.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are lower, attempting to pare back some of the post-NFP upside seen on Friday, but with focus also on the dovish implications of Fed’s Kugler resignation and Trump’s firing of the BLS Chief. On the former, it was announced that Fed’s Kugler is to resign from her role at the Fed (sparking a slight dovish reaction on Friday); thereafter, US President Trump said he will announce a replacement in the coming days. Traders will keep an eye out for the appointment, as it provides Trump the opportunity to shove in his favoured candidate to replace Powell, once his term ends. On the Trump-BLS saga; after blaming (and then firing) the BLS Chief for a poor NFP report, Trump confirmed he will be announcing a new appointee in the coming days. Price action today has been relatively contained and trades at the mid-point of a 111-31+ to 112-12 range; the peak for the day surpassed Friday’s high at 112-11, and further upside will bring into play the high from 1 July at 112-12+.

- Bunds are downbeat, in-fitting with global peers. Currently trading in a 129.50 to 130.06 range, which is well within Friday’s confines of 129.12 to 130.21. Newsflow has been very light today, aside from EZ Sentix Index, which printed at -3.7, far below the expected 8.0; the Sentix director manager described the recent EU-US trade deal as a “mood killer”. Commentary over the weekend came via ECB’s Patsalides, who said that the EZ continues to remain resilient despite trade woes, though he added that “the environment remains uncertain”. On the latest ECB policy decision (where the Bank opted to keep rates steady), Patsalides said it would be “premature to interpret this decision as a pause”.

- Gilts are also trading in tandem with peers, holding a bearish bias but with price action fairly muted. UK paper is currently lower by around 12 ticks in a 92.24 to 92.49 range. Newsflow has been exceptionally quiet so far, but all attention will be on Thursday’s BoE policy announcement.

- Click for a detailed summary

COMMODITIES

- Choppy trade in the crude complex and now ultimately softer following the initial modest gap lower at the reopen in the aftermath of the OPEC+ decision on Sunday and after the NFP and ISM-induced slide on Friday. To recap, OPEC+ said in a statement that eight members will raise oil output by 547,000 bpd in September (some sources last week suggested it could be lower). The eight countries are scheduled to meet again on September 7th, where they may consider reinstating another 1.65mln bpd of cuts that are currently in place until the end of 2026, according to Reuters sources. WTI resides in a 66.56-67.62/bbl range while Brent sits in a USD 68.90-69.88/bbl range.

- Mostly softer trade across precious metals as the Dollar claws back some ground after Friday's data-induced losses. Price action this morning has been fairly contained as the yellow metal takes a breather, with support found near its 50 DMA this morning, as spot gold resides in a USD 3,345.00-3,364.81/oz range at the time of writing.

- Mixed trade across base metals amid quieter weekend newsflow and a relatively uneventful European session thus far in terms of macro impulses. Little move was seen on reports that China could step up monetary easing efforts in H2 2025 by cutting benchmark interest rates and banks’ RRR in order to guide overall financing costs lower and support the economy, according to Shanghai Securities News. 3M LME copper prices reside in a USD 9,635.10-9,696.80/t range.

- OPEC+ said in a statement that eight members are to raise oil output by 548k bpd in September, citing steady global economic and current healthy market fundamentals, while it stated that eight OPEC+ countries are to meet next on September 7th and sources noted the group may discuss returning another layer of cuts of 1.65mln bbls which are in place until end-2026, according to Reuters.

- Kuwait’s Oil Minister praised the OPEC+ decision to raise output and said the meeting reflects continued coordination among participating countries to ensure the stability of the oil market, while he added that the decision was based on a thorough analysis of market data regarding production inventories and future expectations.

- Libya’s Sharara oilfield reached its highest production since 2018 at nearly 311k bpd.

- Azerbaijan is to export 1.2bcm of gas to Syria each year from the BP-led Shah Deniz gas field.

- China rejects US request to stop importing oil from Iran and Russia, according to Al Hadath.

- Click for a detailed summary

NOTABLE EUROPEAN HEADLINES

- UK's FCA proposed a redress scheme for motor finance claims which could cost banks up to GBP 18bln, according to FT.

- Germany's engineering association VDMA said engineering orders -5% Y/Y in June (domestic -5%, foreign -5%); engineering orders -2% Y/Y in April-June (domestic -2%, foreign -1%).

NOTABLE DATA RECAP

- EZ Sentix Index (Aug) -3.7 vs. Exp. 8.0 (Prev. 4.5)

- Swiss Manufacturing PMI (Jul) 48.8 vs. Exp. 49.7 (Prev. 49.6)

- Turkish CPI MM (Jul) 2.06% vs. Exp. 2.4% (Prev. 1.37%)

NOTABLE US HEADLINES

- US President Trump said he would remove Fed Chair Powell in a heartbeat but added that removing Powell would disturb the market, while he stated Powell will most likely stay on as Chair, and he will appoint a new Fed Chair once Powell’s term ends.

- US President Trump said he is to announce a replacement for Fed's Kugler in the next couple of days after the Fed announced on Friday that Governor Kugler is resigning from the Fed board effective August 8th.

- Fed’s Williams said he is going into the September meeting with an open mind and that modestly restrictive policy is still needed, while he added the unusually large downward revisions in May and June payrolls were really the news in the report.

- Apple (AAPL) CEO Cook said he intends to win the AI race and will make the appropriate investments to do so.

- Boeing (BA) defence workers are set to strike on Monday after the company’s St. Louis employees rejected the latest offer, while Boeing stated that it is prepared for a strike and has fully implemented its contingency plan.

- A conservative think tank run by former US VP Pence is reportedly lobbying Hill offices against a push to make gambling losses 100% tax-deductible, according to Punchbowl.

GEOPOLITICS

MIDDLE EAST

- Hamas said it won’t disarm unless an independent Palestinian state is established. It was separately reported that Hamas’s armed wing said it is ready to respond positively and cooperate with any request from the Red Cross to deliver food to hostages in Gaza, while it added that Israel must stop aerial operations during the delivery of aid to hostages.

- Jordan’s armed forces said two armed people were killed after a foiled infiltration attempt through its border with Syria.

- Syrian Defence Ministry said an attack by Syrian Defence Forces in the northern city of Mamjib injured four army personnel and three civilians.

- A senior official from the International Atomic Energy Agency (IAEA) will visit Iran within the next 10 days, according to Iran International, cited by the Iranian Foreign Ministry.

RUSSIA-UKRAINE

- Russia's Kremlin said, "We're not talking about any kind of nuclear escalation"; "it's obvious that US submarines are already on combat duty anyway". Contacts with Witkoff are always useful and important. US mediation efforts in the Ukraine conflict are very important. Putin may meet Trump’s envoy Witkoff this week. Everyone should be very, very careful with nuclear rhetoric. No desire to get into a polemic with Trump over nuclear submarines.

- The Russian Defence Ministry said Russian forces captured the village of Oleksandro Kalynove in Eastern Ukraine.

- IAEA team at Ukraine’s Zaporizhzhia Nuclear Power Plant heard explosions and saw smoke coming from a nearby location where the plant said one of its auxiliary facilities was attacked.

- Ukraine’s military said it struck Russia’s Ryazan oil refinery again.

- US President Trump said there will be sanctions if Russia does not stop the war, but added that Russia seems to be good at avoiding sanctions, while he stated that special envoy Witkoff will be going to Russia on Wednesday or Thursday.

- US President Trump ordered two nuclear submarines to be positioned in the appropriate regions on Friday, "just in case these foolish and inflammatory statements” from Russia's Medvedev are more than just that.

- Indian officials said they will continue to buy Russian oil despite threats of additional tariffs from US President Trump’s administration.

OTHER

- Russia-China navy exercises began in the Sea of Japan, according to TASS.

CRYPTO

- Bitcoin is a little firmer and trades just shy of USD 115k, whilst Ethereum posts slightly larger intraday gains around USD 3.6k.

APAC TRADE

- APAC stocks traded mixed following a quiet weekend of newsflow and last Friday's disappointing Non-Farm Payrolls data.

- ASX 200 was subdued amid underperformance in the top-weighted financials sector and with weakness also seen in energy, Industrials and tech, although losses were stemmed by resilience in defensives and miners.

- Nikkei 225 underperformed after recent currency strength and briefly dipped back beneath the 40k level.

- Hang Seng and Shanghai Comp were kept afloat amid earnings and corporate updates, while the PBoC announced last week that it is to expand the issuance scale of sci-tech bonds and promote cross-border financing facilitation, as well as strengthen the implementation and supervision of interest rate policies.

NOTABLE ASIA-PAC HEADLINES

- China could step up monetary easing efforts in H2 2025 by cutting benchmark interest rates and banks’ RRR in order to guide overall financing costs lower and support the economy, according to Shanghai Securities News.

- India's capital markets regulator called for structural reforms to the country's vast derivatives market, according to FT.

- PBoC did not purchase or sell Chinese sovereign bonds on the open market in July; PBoC conducted CNY 1.4tln of outright reverse repos in July on the open market.