Europe Market Open: USD & Stocks firm; Trump to speak on CNBC at 13:00 BST

05 Aug 2025, 06:50 by Newsquawk Desk

- APAC stocks were mostly higher following the rally on Wall St where the major indices clawed back post-NFP losses.

- European equity futures indicate a marginally higher cash market open with Euro Stoxx 50 future up 0.3% after the cash market finished with gains of 1.5% on Monday.

- DXY trades higher, but remains below the 99.0 mark, EUR/USD retains its position on a 1.15 handle.

- Fed's Daly (2027 voter) said two rate cuts this year still seems to be the appropriate amount of recalibration.

- Looking ahead, highlights include Global Composite and Services Final PMIs, EZ Producer Prices, Canadian Trade, US ISM Services, International Trade Balance, RCM/TIPP Economic Optimism, Atlanta Fed GDPNow, New Zealand Jobs, Supply from UK, Germany & US.

- Earnings from AMD, Arista Networks, Snap, Pfizer, Caterpillar, BP, Diageo, Fresnillo, Infineon, Deutsche Post, Fresenius Medical Care, Continental, Hugo Boss, Bper Banca & Telecom Italia.

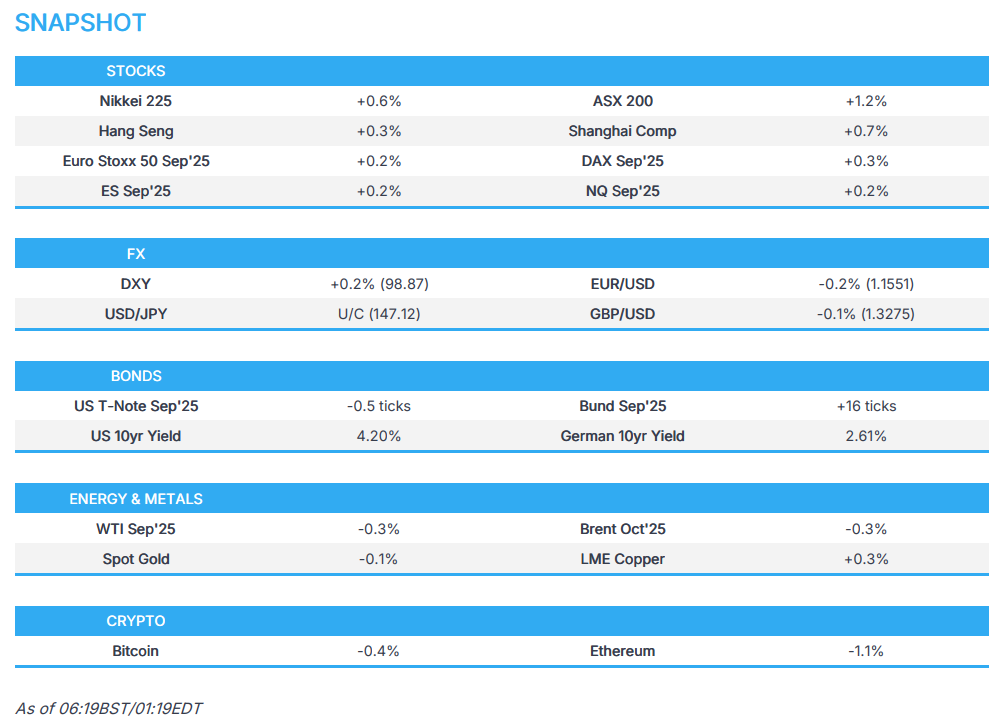

SNAPSHOT

US TRADE

EQUITIES

- US stocks were bid on Monday and pared some of the weakness seen last week with outperformance in the small-cap Russell 2000 index, while gains were led by Communication, Utilities and Technology sectors. Conversely Energy, Consumer Staples and Consumer Discretionary lagged with energy the only sector in the red amid lower crude and natgas prices after crude prices sold off throughout the morning before bouncing off lows in response to a post from US President Trump who announced he will be substantially raising the tariff paid by India to the US due to buying massive amounts of Russian oil and then selling it on the open market for big profits.

- SPX +1.47% at 6,330, NDX +1.87% at 23,189, DJI +1.34% at 44,174, RUT +2.10% at 2,212.

- Click here for a detailed summary.

TARIFFS/TRADE

- US is exploring better location trackers for AI chips to curtail flows to China, according to Bloomberg.

- Canada said Canadian ministers Anand and Champagne are to travel to Mexico this week.

- Brazil Finance Minister Haddad believes he will speak to US Treasury Secretary Bessent this week and said they have never left the negotiating table with the US, and will not do so until there is an agreement on the horizon. Haddad said they don't want only China or the EU to invest in Brazil, but want the US to invest too, while he added the US needs to understand that Brazil wants partnerships, but not as a satellite or a colony. In relevant news, Brazil's Supreme Court Justice ordered a house arrest of former Brazilian President Bolsonaro, while the US State Department later condemned the order imposing house arrest on Bolsonaro and said it will hold accountable all those aiding and abetting sanctioned conduct.

NOTABLE HEADLINES

- Fed's Daly (2027 voter) said she is comfortable with the Fed's July decision, but is less comfortable in making that same decision again and again, while she added that they can't wait to be certain there is no inflation persistence and need to make a call based on what's most likely. Daly said there is still a lot of uncertainty over whether a September rate cut would be appropriate and she was willing to wait another cycle regarding the July Fed decision, but cannot wait forever. Furthermore, she said every meeting going forward is 'live' for thinking about policy adjustments and they may do fewer than two rate cuts, but the more likely thing is that they need to do more, and two rate cuts this year still seems to be the appropriate amount of recalibration.

- White House is preparing an executive order that would fine banks for dropping customers for political reasons, according to the WSJ.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher following the rally on Wall St where the major indices clawed back post-NFP losses amid rate cut hopes.

- ASX 200 ascended with every sector in the green and outperformance in real estate, tech, and consumer discretionary.

- Nikkei 225 took impetus from global peers and shrugged off a firmer currency with earnings releases remaining a driver for individual stocks.

- Hang Seng and Shanghai Comp were ultimately kept afloat after the latest S&P Global PMI figures which showed a strong acceleration in Services PMI, while Composite PMI cooled but remained in expansionary territory.

- US equity futures (ES +0.2%, NQ +0.3%) held on to the prior day's spoils after fully recovering last Friday's data-induced losses.

- European equity futures indicate a marginally higher cash market open with Euro Stoxx 50 future up 0.3% after the cash market finished with gains of 1.5% on Monday.

FX

- DXY eked mild gains but remained beneath the 99.00 level following the recent mixed performance against G10 peers and as markets awaited US President Trump's announcement regarding the replacements for the BLS head and Fed Governor Kugler, while recent comments from Fed's Daly had little impact in which she noted that she is comfortable with the Fed's July decision, but is less comfortable in making that same decision again and again, as well as stated that they can't wait to be certain there is no inflation persistence and need to make a call based on what's most likely.

- EUR/USD lacked direction after yesterday's choppy performance and with resistance seen near the 1.1600 level, while the EU is said to suspend trade countermeasures on the US by six months and is awaiting Trump's actions on car tariffs and exemptions this week.

- GBP/USD traded flat after briefly retesting the 1.3300 level to the upside with price action contained amid a lack of pertinent catalysts and with the BoE expected to cut rates later in the week.

- USD/JPY attempted to nurse some losses after briefly dipping beneath the 147.00 level with recent price action a function of yield differentials.

- Antipodeans lacked demand in the absence of tier-1 data from Australia and New Zealand, while the latest Chinese PMI data was somewhat mixed.

- PBoC set USD/CNY mid-point at 7.1366 vs exp. 7.1667 (Prev. 7.1395)

FIXED INCOME

- 10yr UST futures took a breather after yesterday's two-way price action and eventual extension of post-NFP gains amid a boost in Fed rate cut bets, while participants now await 1yr and 3yr supply from the US.

- Bund futures lingered around the prior day's highs after scaling above the 130.00 level but with further upside capped as supply also looms with a EUR 5bln Schatz auction due later followed by EUR 2.5bln of Bund issuances on Wednesday.

- 10yr JGB futures tracked the recent gains in global peers amid softer yields and with prices unfazed by the latest 10yr JGB auction results which were mostly weaker than previous.

COMMODITIES

- Crude futures were lacklustre following the prior day's declines and the recent OPEC+ output hike decision, but were off the prior day's lows with President Trump threatening to substantially raise tariffs on India for its massive purchases of Russian oil and reselling in the open market.

- Libya's National Oil Corporation signed an MoU with Exxon (XOM) following a decade-long halt in activity.

- Spot gold traded rangebound overnight after recent advances and with gains capped by a firmer dollar.

- Copper futures kept afloat alongside the mostly positive risk environment and after the latest PMI data from China which was somewhat mixed but showed an acceleration in China's services industry.

- Chile's Codelco said it will have to submit four reports so the mining regulator can lift the suspension of its underground operation after an accident at the El Teniente mine.

CRYPTO

- Bitcoin trickled lower overnight after retreating beneath the USD 115k level.

- US CFTC acting chairman announced CFTC will launch an initiative for trading spot crypto asset contracts listed on CFTC-registered futures exchanges.

NOTABLE ASIA-PAC HEADLINES

- BoJ Minutes from the June Meeting stated many members said inflation is somewhat overshooting forecasts, but must scrutinise economic developments due to downside risk to growth from US tariff policy and members shared the view that the BoJi expected to continue raising the policy rate if the economy and prices move in line with its forecast. Furthermore, one member said must support economy with current rate level as underlying inflation likely to stagnate temporarily and a member said the rate hike phase may be on pause for time being, but the BoJ must respond nimbly and resume hiking rates depending on US policy development.

DATA RECAP

- Chinese S&P Global Services PMI (Jul) 52.6 vs. Exp. 50.4 (Prev. 50.6)

- Chinese S&P Global Composite PMI (Jul) 50.8 (Prev. 51.3)

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu is leaning towards expanding the Gaza offensive and seizing the enclave, according to Israel's N12.

- IDF Chief of Staff Zamir cancelled a trip to Washington to meet with Pentagon officials after learning that PM Netanyahu gave the green light to occupy the Gaza Strip, according to Israeli Media cited by Sky News Arabia.

RUSSIA-UKRAINE

- Russia's Foreign Ministry said Russia no longer considers itself bound by the moratorium on the deployment of short and medium-range missiles. It was later reported that Russia's Medvedev blamed NATO countries for the end of the moratorium on short and medium-range missiles, while he stated that Moscow will take further steps.

- Dutch Defence Ministry said the Netherlands will be the first to contribute to NATO's new "Priority Ukraine Requirements List (PURL)" financing mechanism for Ukraine with the Netherlands to pay EUR 500mln under the new mechanism.

EU/UK

NOTABLE HEADLINES

- UK FCA head warned UK lenders must stop “haggling” over a planned multibillion-pound redress scheme for consumers mis-sold car finance, according to FT.