US Market Open: USD firm & stocks eek gains ahead of Trump’s appearance on CNBC

05 Aug 2025, 11:00 by Newsquawk Desk

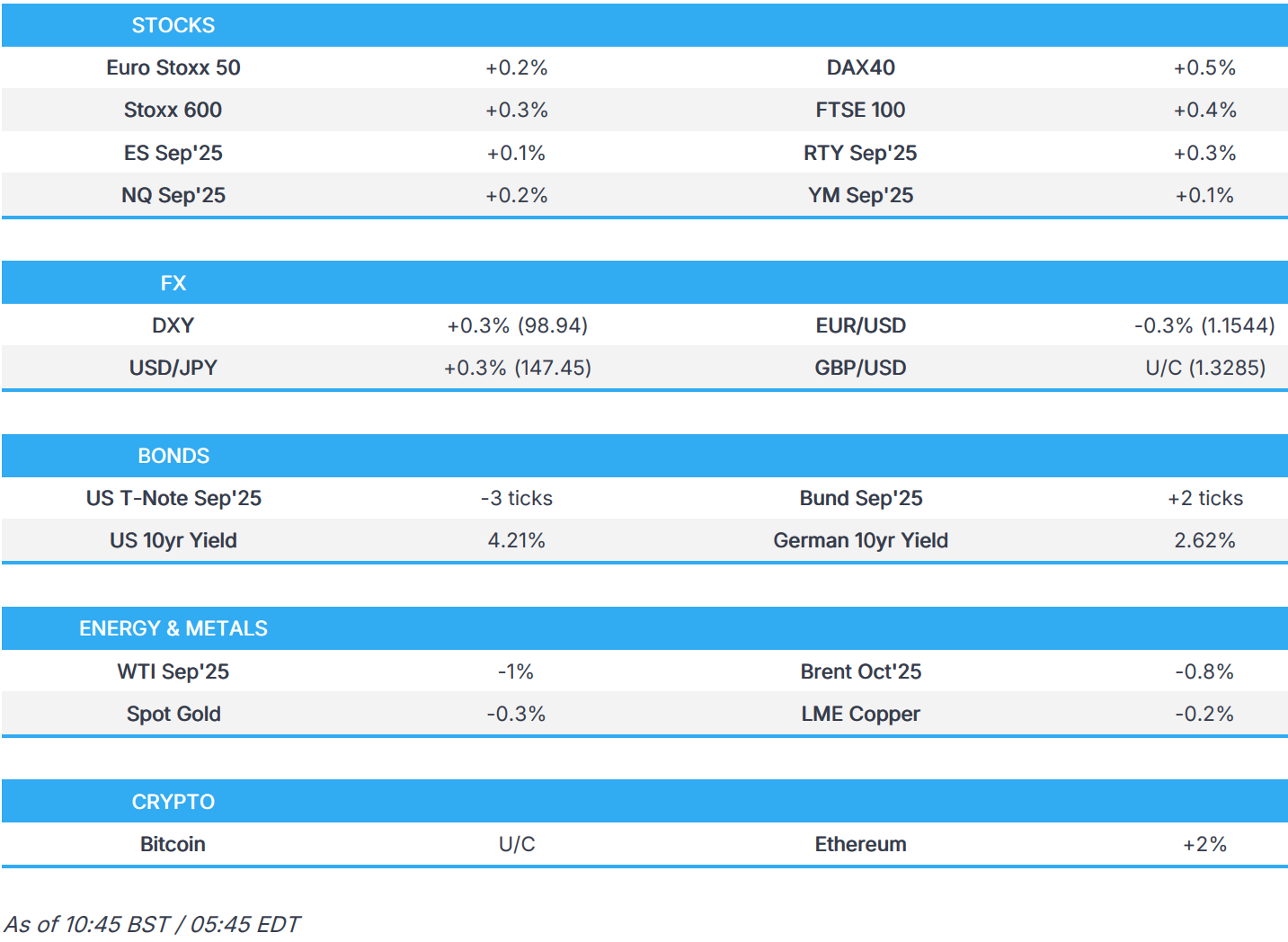

- European and US equity futures are modestly firmer, into a slew of earnings.

- USD is firmer vs. peers but still very much lower post-NFP; havens lag a touch.

- Bonds trade with a marginally bearish bias into a packed afternoon.

- Crude complex is on the backfoot and currently at lows, with XAU pressured by the Dollar.

- Looking ahead, Global Composite and Services Final PMIs, Canadian Trade, US ISM Services, International Trade Balance, RCM/TIPP Economic Optimism, Atlanta Fed GDPNow, New Zealand Jobs, Supply from the US. Earnings from AMD, Arista Networks, Snap, Pfizer, Caterpillar, Bper Banca & Telecom Italia.

TARIFFS/TRADE

- EU official says already seeing implementation of EU-US framework trade deal, says in the US executive order, seeing all-including tariff rate of 15%. Means most favoured nation rate is included within the US 15% rate. 15% rate on section 232 such as Pharma will kick in once US investigation is complete. 15% rate applies on cars. Steel discussions taking longer, need to discuss volumes. Talks are "pretty advanced" on a deal. Joint statement "pretty much ready"; "waiting for US to get back to us". Cannot say when statement will be released. The joint statement is not legally binding (reiteration). Alternative to a US deal would be an escalation of tariffs.

- EU Trade Chief Sefcovic says he is in contact with US Commerce Secretary Lutnick and USTR Greer; talks continue in a "constructive spirit".

- US is exploring better location trackers for AI chips to curtail flows to China, according to Bloomberg.

- Canada said Canadian ministers Anand and Champagne are to travel to Mexico this week.

- Brazil's Supreme Court Justice ordered a house arrest of former Brazilian President Bolsonaro, while the US State Department later condemned the order imposing house arrest on Bolsonaro and said it will hold accountable all those aiding and abetting sanctioned conduct.

- Russian Kremlin, on US pressure against India, says that the US' attempt to stop nations from trading with Russia is illegal.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) opened broadly in modest positive territory, but have marginally slipped off best levels as the morning progressed. News flow recently has been very light, and we are still awaiting details regarding who US President Trump’s new Fed/BLS appointees will be, after one walked and the other got the boot. Trump is due to speak on CNBC at 13:00 BST / 08:00 EDT.

- European sectors hold a strong positive bias, with only a handful of sectors residing in marginal negative territory. Food Beverage and Tobacco tops the pile, with Diageo (the third largest weighting in the sector), popping at the open. Energy follows closely behind, as heavyweight BP benefits from strong results and as it initiates further cost reviews.

- US equity futures (ES +0.1%, NQ +0.2%, RTY +0.3%) are modestly higher across the board, with the RTY ever so slightly outperforming. Ahead, a busy US docket with ISM Services, RCM TIPP and Atlanta Fed’s GDPNow due.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has mildly extended on Monday's attempted recovery, albeit, upside is modest in comparison to the hefty sell-off seen post-NFP on Friday. The rally in the USD remains tempered by the recent downside in the US rates space as markets continue to price in the likelihood of a September rate cut. Note, markets still await Trump's replacement for Fed's Kugler and the head of the BLS. On the Fed, non-voter Daly stated that she is of the view that the FOMC cannot wait to be certain there is no inflation persistence and need to make a call based on what's most likely. For today's docket, the main highlight is the July ISM services report with the headline expected to rise to 51.5 from 50.8. DXY has ran into resistance at the 99.0 mark. If breached, there is clean air until the 100 level.

- EUR/USD is lower with the pair continued to primarily be led by fluctuations in the USD. Incremental macro drivers for the Eurozone remain on the light side asides from commentary by an EU official that it is already seeing the implementation of the EU-US framework trade deal, which is providing an all-including tariff rate of 15%. As a caveat, the official reiterated the EU's line that the joint statement is not legally binding. EUR/USD remains on a 1.15 handle with the pair currently capped by its 200DMA at 1.1586.

- JPY softer vs. the broadly firmer USD and back on a 147 handle after USD/JPY delved as low as 146.63 overnight. On the trade front, Japanese trade negotiator Akazawa is to leave for Washington today, looking to press US President Trump into signing of an executive order that would bring an agreed cut to tariffs on Japanese auto imports into effect, according to Reuters. BoJ minutes passed with little in the way of fanfare given they were from the June meeting.

- GBP steady vs. the USD as newsflow surrounding the UK remains light with an upward revision to services and composite PMI data unable to stoke a reaction in GBP. That will change on Thursday with the latest BoE policy announcement and MPR, which is 82% priced for a 25bps reduction. Cable remains tucked within Monday's 1.3254-3331 range.

- Antipodeans are both are on the backfoot vs. the USD after an indecisive session yesterday. The USD is providing the greatest source of traction for AUD/USD and NZD/USD amid the absence of tier-1 data from Australia and New Zealand, while the latest Chinese PMI data was somewhat mixed.

- PBoC set USD/CNY mid-point at 7.1366 vs exp. 7.1667 (Prev. 7.1395)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A modestly softer start to the day for USTs. Newsflow thus far has been light and the morning’s price action is seemingly just a slight pullback from the marginal extension above post-NFP highs seen on Monday, rather than any overt bearish move. Thus far, USTs are down to a 112-07+ low, pulling back from Monday’s 112-14 peak but still clear of the WTD 111-31+ base. Ahead, a busy US docket with ISM Services, RCM TIPP, Atlanta Fed’s GDPNow and a 3yr Note auction all scheduled. Additionally, POTUS will be appearing on CNBC at 13:00BST. From Trump, we are attentive to any clues as to who the Fed board, and by extension Chair, nominees will be after Trump said on the weekend that he would be making an announcement on it this week, in addition to the new BLS head.

- Bunds began the morning on the front foot, with Bunds up to a 130.60 peak with gains in excess of 30 ticks at one point. However, this has been gradually paring across the morning with the benchmark down to a 130.16 trough with downside of just over 10 ticks at most. Initial upside was seemingly an extension of the strength seen on Monday, with the benchmark picking up into the European cash equity open. Thereafter, a modest pullback began into the morning’s Final PMIs. Though, to be clear, the PMIs do not appear to have driven the action. In brief, the final releases have been subject to two-way revisions. For the bloc as a whole, both Composite and Services were subject to modest revisions lower. PPI printed in-line with consensus, no sustained reaction scene on the release though the subsequent UK auction result (strong, see below) appears to have lifted the fixed complex from lows across the board. German auction was also fairly decent, but sparked no move.

- UK specific newsflow a little light once again as we count down to the BoE later in the week. Markets currently almost fully price in a rate cut, though the actual decision is unlikely to be that simple with a three-way split very possible. UK PMIs were revised a little higher but had limited impact on UK paper. In terms of today’s action, Gilts opened a tick lower at 92.64 before extending to a 92.84 peak acknowledging the initial upward bias seen in EGBs. Thereafter, gradually drifted across the morning to a 92.48 low with downside of just under 20 ticks at most. Supply this morning was strong, with a 3.33x b/c (prev. 2.89x), helping lift the benchmark from the above low by around 15 ticks and back to essentially unchanged on the session

- UK sells GBP 4.5bln 4.5% 2035 Gilt: b/c 3.33x (prev. 2.89x), average yield 4.522% (prev. 4.635%) & tail 0.1bps (prev. 0.2bps

- Germany sells EUR 3.916bln vs exp. EUR 5bln 1.90% 2027 Schatz: b/c 2.50x (prev. 2.3x), average yield 1.90% (prev. 1.87%) and retention 21.68% (prev. 22.02%

- Click for a detailed summary

COMMODITIES

- Initial choppy trade in the crude complex, but has recently traded with a downward bias; currently trading at lows. WTI resides in a 65.50-66.39/bbl range while Brent sits in a USD 68.205-69.87/bbl range.

- Precious metals are mostly lower trade as the dollar regains some composure with DXY back on a 99.00 handle. Price action this morning has been contained for the yellow metal, with support found on Monday near its 50 DMA (USD 3,344.59/oz today), as spot gold resides in a USD 3,365.79-3,382.37/oz range at the time of writing.

- Mostly softer trade across base metals amid the firmer dollar, although macro newsflow this morning has been rather light. Overnight, copper was kept afloat alongside the mostly positive risk environment and after the latest PMI data from China, which was somewhat mixed but showed an acceleration in China's services industry. 3M LME copper prices reside in a USD 9,659.95-9,751.00/t range.

- Libya's National Oil Corporation signed an MoU with Exxon (XOM) following a decade-long halt in activity.

- Saudi Aramco says it anticipates oil demand in H2 to be over 2mln BPD above H1 levels; continue to invest in various initiatives, incl. new energies and digital innovation focused on AI.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HCOB Services Final PMI (Jul) 51.0 vs. Exp. 51.2 (Prev. 51.2); Composite Final PMI (Jul) 50.9 vs. Exp. 51.0 (Prev. 51.0)

- Spanish Services PMI (Jul) 55.1 vs. Exp. 52.5 (Prev. 51.9)

- Italian HCOB Services PMI (Jul) 52.3 vs. Exp. 52.6 (Prev. 52.1); Composite PMI (Jul) 51.5 (Prev. 51.1)

- French HCOB Composite PMI (Jul) 48.6 vs. Exp. 49.6 (Prev. 49.6); Services PMI (Jul) 48.5 vs. Exp. 49.7 (Prev. 49.7)

- German HCOB Composite Final PMI (Jul) 50.6 vs. Exp. 50.3 (Prev. 50.3); Services PMI (Jul) 50.6 vs. Exp. 50.1 (Prev. 50.1)

- UK S&P Global PMI: Composite Output (Jul) 51.5 vs. Exp. 51.0 (Prev. 51.0); Services PMI (Jul) 51.8 vs. Exp. 51.2 (Prev. 51.2)

- French Industrial Output MM (Jun) 3.8% vs. Exp. 0.6% (Prev. -0.5%, Rev. -0.7%)

- Spanish Ind Output Cal Adj YY (Jun) 2.3% (Prev. 1.7%)

- EU Producer Prices YY (Jun) 0.6% vs. Exp. 0.6% (Prev. 0.3%); Producer Prices MM (Jun) 0.8% vs. Exp. 0.8% (Prev. -0.6%)

NOTABLE EUROPEAN HEADLINES

- UK FCA head warned UK lenders must stop “haggling” over a planned multibillion-pound redress scheme for consumers mis-sold car finance, according to FT.

NOTABLE US HEADLINES

- Fed's Daly (2027 voter) said she is comfortable with the Fed's July decision, but is less comfortable in making that same decision again and again, while she added that they can't wait to be certain there is no inflation persistence and need to make a call based on what's most likely. Daly said there is still a lot of uncertainty over whether a September rate cut would be appropriate and she was willing to wait another cycle regarding the July Fed decision, but cannot wait forever. Furthermore, she said every meeting going forward is 'live' for thinking about policy adjustments and they may do fewer than two rate cuts, but the more likely thing is that they need to do more, and two rate cuts this year still seems to be the appropriate amount of recalibration.

- White House is preparing an executive order that would fine banks for dropping customers for political reasons, according to the WSJ.

GEOPOLITICS

- Russia's Medvedev blamed NATO countries for the end of the moratorium on short and medium-range missiles, while he stated that Moscow will take further steps.

- Russia's Kremlin says Russia no longer considers itself bound by any limits on intermediate-range missile deployment.

- Israel PM Netanyahu will convene a meeting on Gaza and the hostage deal, via journalist Stein citing an Israeli official; official adds, US Envoy Witkoff returned to the US with "a broad consensus that a deal must include all of the hostages".

CRYPTO

- Bitcoin is flat and trades around USD 114k, whilst Ethereum outperforms a touch and holds just shy of USD 3.6k.

- US CFTC acting chairman announced CFTC will launch an initiative for trading spot crypto asset contracts listed on CFTC-registered futures exchanges.

APAC TRADE

- APAC stocks were mostly higher following the rally on Wall St where the major indices clawed back post-NFP losses amid rate cut hopes.

- ASX 200 ascended with every sector in the green and outperformance in real estate, tech, and consumer discretionary.

- Nikkei 225 took impetus from global peers and shrugged off a firmer currency with earnings releases remaining a driver for individual stocks.

- Hang Seng and Shanghai Comp were ultimately kept afloat after the latest S&P Global PMI figures which showed a strong acceleration in Services PMI, while Composite PMI cooled but remained in expansionary territory.

NOTABLE ASIA-PAC HEADLINES

- BoJ Minutes from the June Meeting stated many members said inflation is somewhat overshooting forecasts, but must scrutinise economic developments due to downside risk to growth from US tariff policy and members shared the view that the BoJ is expected to continue raising the policy rate if the economy and prices move in line with its forecast. Furthermore, one member said must support economy with current rate level as underlying inflation likely to stagnate temporarily and a member said the rate hike phase may be on pause for time being, but the BoJ must respond nimbly and resume hiking rates depending on US policy development.

- Japanese Cabinet Office lowered its FY25 GDP forecast amid the impact of the US tariff policy, according to Nikkei.

- Foxconn (2317 TT) July revenue +7.25% Y/Y (vs. +10.09% Y/Y in June).

- China's Auto Industry CPCA revises up 2025 car sales forecast by 300k units to 24.35mln units; revises up China car exports forecast by 160k to 5.46mln units

DATA RECAP

- Chinese S&P Global Services PMI (Jul) 52.6 vs. Exp. 50.4 (Prev. 50.6); Composite PMI (Jul) 50.8 (Prev. 51.3)