Europe Market Open: FX rangebound & stocks firm, Europe focused on heavyweight earnings & Trump at 21:30BST

06 Aug 2025, 06:50 by Newsquawk Desk

- APAC stocks traded somewhat mixed following the subdued handover from Wall St post-ISM services.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 future up 0.3% after the cash market closed with gains of 0.1%.

- DXY is flat, EUR/USD remains on a 1.15 handle and capped by its 200DMA, and antipodeans marginally lead.

- RBI kept the Repurchase Rate unchanged at 5.50%, as expected, and maintained a neutral stance.

- Looking ahead, highlights include German Industrial Orders (Jun), EZ Construction PMIs (Jul), EZ Retail Sales (Jun), Italian Industrial Output, Fed’s Collins, Cook and Daly, Supply from Germany & US.

- Earnings from Airbnb, Lyft, Uber, Shopify, Walt Disney, McDonald's, Novo Nordisk, Siemens Energy, Commerzbank, Bayer, Fresenius, Beiersdorf, ABN AMRO & Glencore.

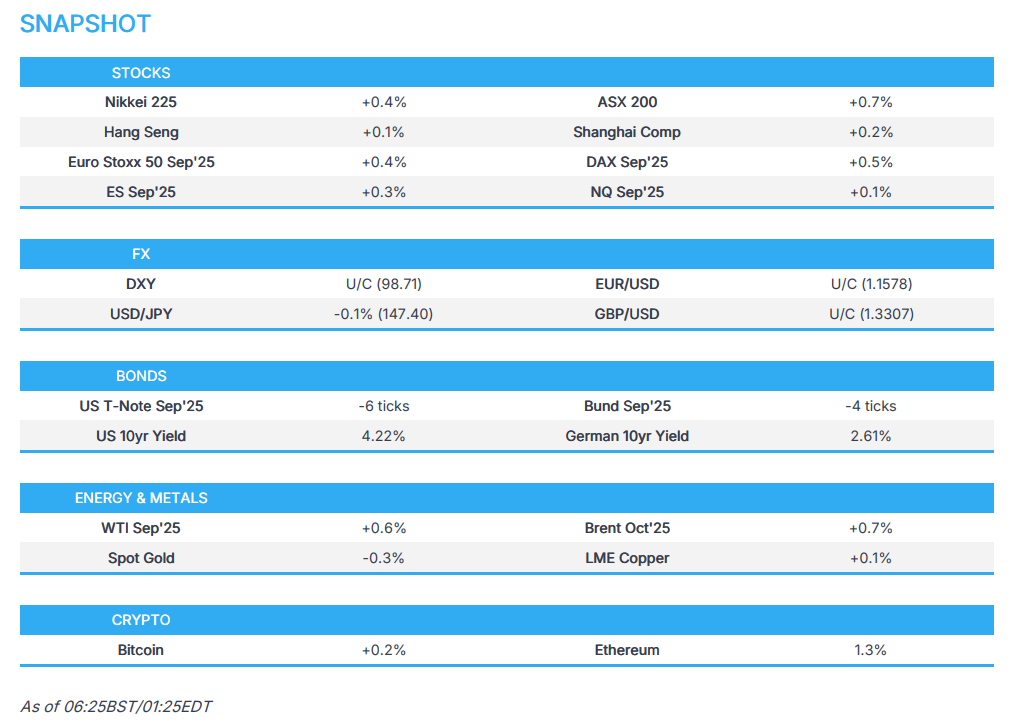

SNAPSHOT

US TRADE

EQUITIES

- US stocks finished mostly lower with the major indices in the red to varying degrees although the small-cap Russell 2000 bucked the trend, while the highlight of the day was US President Trump's interview on CNBC whereby he spoke on a wide range of topics and noted that both Kevin’s (Warsh & Hassett) and two others are the candidates for the next Fed Chair. Trump also commented on trade and warned if the EU does not make the US investments agreed upon in the deal, the EU will pay tariffs of 35%, but if investments are made, tariffs will be cut to 15% (from 30%), while he repeated that he will be raising India tariffs substantially in the next 24 hours as they keep purchasing Russian oil. Data-wise, ISM Services PMI disappointed, with the headline printing below the bottom end of the forecast range, while the employment sub-index fell further into contractionary territory.

- SPX -0.49% at 6,299, NDX -0.73% at 23,019, DJI -0.14% at 44,112, RUT +0.60% at 2,226.

- Click here for a detailed summary.

TARIFFS/TRADE

- Canadian PM Carney said Canada will provide up to CAD 700mln in loan guarantees to the softwood lumber industry to help it cope with US duties and Canada will provide CAD 500mln to help speed the lumber industry's product development and market diversification. Furthermore, they will look at other opportunities to remove tariffs to help Canadian industries work more effectively.

- Canada's Foreign Minister Anand said they agreed to build a work plan between Canada and Mexico to focus on supply chains, energy security and others, while she added that trade talks with the US continue to be constructive.

- Brazilian President Lula said US President Trump did not have the right to announce taxation how he did, and Brazil wants to trade with everyone. Lula said he will not call Trump because he does not want to talk, but would call to invite Trump to the COP-30 and will use all applicable means including the WTO to defend their interests.

- South Korea's Industry Minister said they need to hold further discussions on the timing of US tariff cuts on autos.

NOTABLE HEADLINES

- US President Trump is to make an announcement at 16.30EDT/21:30BST at the Oval Office on Wednesday, according to his public schedule.

- US President Trump said the Fed Governor decision will be made by the end of the week and they have a couple of candidates, while he added that they are looking at the Fed Chair which is down to four people with 'two Kevins and two other people'.

APAC TRADE

EQUITIES

- APAC stocks traded somewhat mixed following the subdued handover from Wall St, where the attention was on the various comments from US President Trump and with sentiment dampened amid disappointing ISM Services data.

- ASX 200 gained at the open with strength in the materials, mining and resources sectors spearheading the advance in the index to a fresh record high.

- Nikkei 225 pared its opening losses and gradually extended higher amid gains in the heavy industry stocks, while softer-than-expected labour cost data and negative real cash earnings supports the case for the BoJ to continue to refrain from resuming its policy normalisation.

- Hang Seng and Shanghai Comp were varied in rangebound trade with little fresh drivers and after the PBoC reiterated China's support pledges including to strengthen macroeconomic policy orientation and optimise the environment for policy implementation.

- US equity futures (ES +0.2%, NQ +0.1%) modestly rebounded following yesterday's retreat and as participants now look ahead to any trade-related developments and the scheduled 'announcement' by US President Trump on Wednesday afternoon at the Oval Office.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 future up 0.3% after the cash market closed with gains of 0.1%.

FX

- DXY was rangebound following the recent soft ISM Services PMI report and wide-ranging comments from US President Trump including on trade in which he threatened the EU with 35% tariffs if they didn't adhere to the agreed-upon US investments, and stated the substantial tariff raise on India from 25% is to come in the next 24 hours. Furthermore, Trump stated that the Fed Governor decision will be made by the end of the week and they have a couple of candidates, while they are also looking at the Fed Chair which is down to four people

- EUR/USD lacked direction after somewhat mixed PMI data from the bloc and comments from ECB's Holzmann who advocated for keeping rates unchanged and said he would not exclude that the next rate move will be a hike.

- GBP/USD kept afloat in the aftermath of recent UK Services PMI data but with the upside capped amid quiet newsflow.

- USD/JPY slightly pulled back but held on to the 147.00 status with a muted reaction seen to the softer-than-expected wages.

- Antipodeans marginally outperformed against G10 peers and were unfazed by the mixed risk appetite, as well as the varied jobs and labour cost data from New Zealand.

FIXED INCOME

- 10yr UST futures were lacklustre after the choppy performance so far this week and with demand hampered by supply, including a 10yr auction due later.

- Bund futures traded little changed amid quiet catalysts and with German Industrial Orders and Bund supply scheduled today.

- 10yr JGB futures marginally pulled back as risk sentiment in Japan improved despite the softer wage growth data from Japan.

COMMODITIES

- Crude futures nursed some of the prior day's losses after declining amid comments from US President Trump regarding lower energy prices and with Russia reportedly weighing a Ukraine air-truce offer to President Trump.

- US Private Inventory Data (bbls): Crude -4.2mln (exp. -0.6mln), Distillate +1.6mln (exp. +0.8mln), Gasoline -0.9mln (exp. -0.4mln), Cushing +1.7mln.

- Russia's crude output was slightly above the OPEC+ target in July.

- Spot gold Marginally pulled back after climbing yesterday in the aftermath of the weak ISM Services data.

- Copper futures regained some composure following recent selling pressure but with the recovery limited amid the somewhat mixed risk appetite in Asia.

CRYPTO

- Bitcoin gradually retreated overnight after slipping beneath the USD 114k level.

NOTABLE ASIA-PAC HEADLINES

- RBI kept the Repurchase Rate unchanged at 5.50%, as expected, and maintained a neutral stance with the MPC vote on the repo rate and policy stance made unanimously. RBI Governor Malhotra stated geopolitical uncertainties have somewhat abated and growth is robust but below aspirations and tariff uncertainties are still evolving. Malhotra also stated that monetary policy transmission is still continuing and that current macroeconomic conditions and the outlook call for a continuation of the policy rate at current levels. Furthermore, he stated the Indian economy is navigating a steady growth path and monetary policy has appropriately used available space to support growth, while he also revealed that the FY26 real GDP growth view was retained at 6.5% and the FY26 CPI inflation view was cut to 3.1% from 3.7% previously.

- South Korea is to offer visa-free entry to Chinese tourists from September 29th.

- New Zealand announced steps to replace the petrol tax in the coming years with road user charges and is to pass the legislation in 2026.

DATA RECAP

- Japanese Labour Cash Earnings (Jun) 2.5% vs Exp. 3.1% (Prev. 1.4%)

- Japanese Real Cash Earnings YY (Jun) -1.3% vs Exp. -0.7%

- New Zealand HLFS Job Growth QQ (Q2) -0.1% vs. Exp. -0.1% (Prev. 0.1%)

- New Zealand HLFS Unemployment Rate (Q2) 5.2% vs. Exp. 5.3% (Prev. 5.1%)

- New Zealand HLFS Participation Rate (Q2) 70.5% vs. Exp. 70.7% (Prev. 70.8%)

- New Zealand Labour Cost Index QQ (Q2) 0.6% vs. Exp. 0.6% (Prev. 0.4%)

- New Zealand Labour Cost Index YY (Q2) 2.2% vs. Exp. 2.3% (Prev. 2.5%)

GEOPOLITICS

MIDDLE EAST

- Israel's Channel 12 said the plan to occupy Gaza in its entirety will be presented on Thursday to the Council of Ministers for approval, according to Sky News Arabia.

RUSSIA-UKRAINE

- US President Trump reportedly readies fresh sanctions against Russia’s shadow fleet if Russian President Putin does not agree to a ceasefire in Ukraine by Friday, according to FT. It was later reported that President Trump said he will make a determination on sanctions on countries that purchase Russian energy after the Wednesday meeting with Russia.

- US Special Envoy Witkoff will be in Moscow on Wednesday to meet with the Russian leadership, while it was later reported that Witkoff landed in Moscow and was greeted by Russian President Putin's envoy Dmitriev.

- Russia is reportedly weighing a Ukraine air-truce offer to US President Trump on war, according to Bloomberg.

- Russia's Kremlin spokesman Peskov said improving Russia-US relations requires overcoming existing inertia which will take time, according to TASS.

OTHER NEWS

- Russian and Chinese ships will conduct joint patrols in the Asia-Pac region following exercises in the Sea of Japan.

- North Korea received Russia's help in modernising nuclear weapons carriers, according to Yonhap citing Ukrainian news.

- US President Trump will host leaders from Armenia and Azerbaijan for peace talks at the White House on Friday.

EU/UK

NOTABLE HEADLINES

- ECB's Holzmann reiterated in an interview that there is no reason to cut rates again.

- UK Chancellor Reeves needs to raise taxes immediately to fill a GBP 50bln hole in the public finances, according to NIESR via the Telegraph. NIESR's Deputy Director said the scale of tax rises required would be equivalent to a 5p increase to the basic and higher rates of income.