US Market Open: Stocks firmer whilst USTs dip into 10yr supply & a Trump announcement at 16:30 EDT

06 Aug 2025, 11:10 by Newsquawk Desk

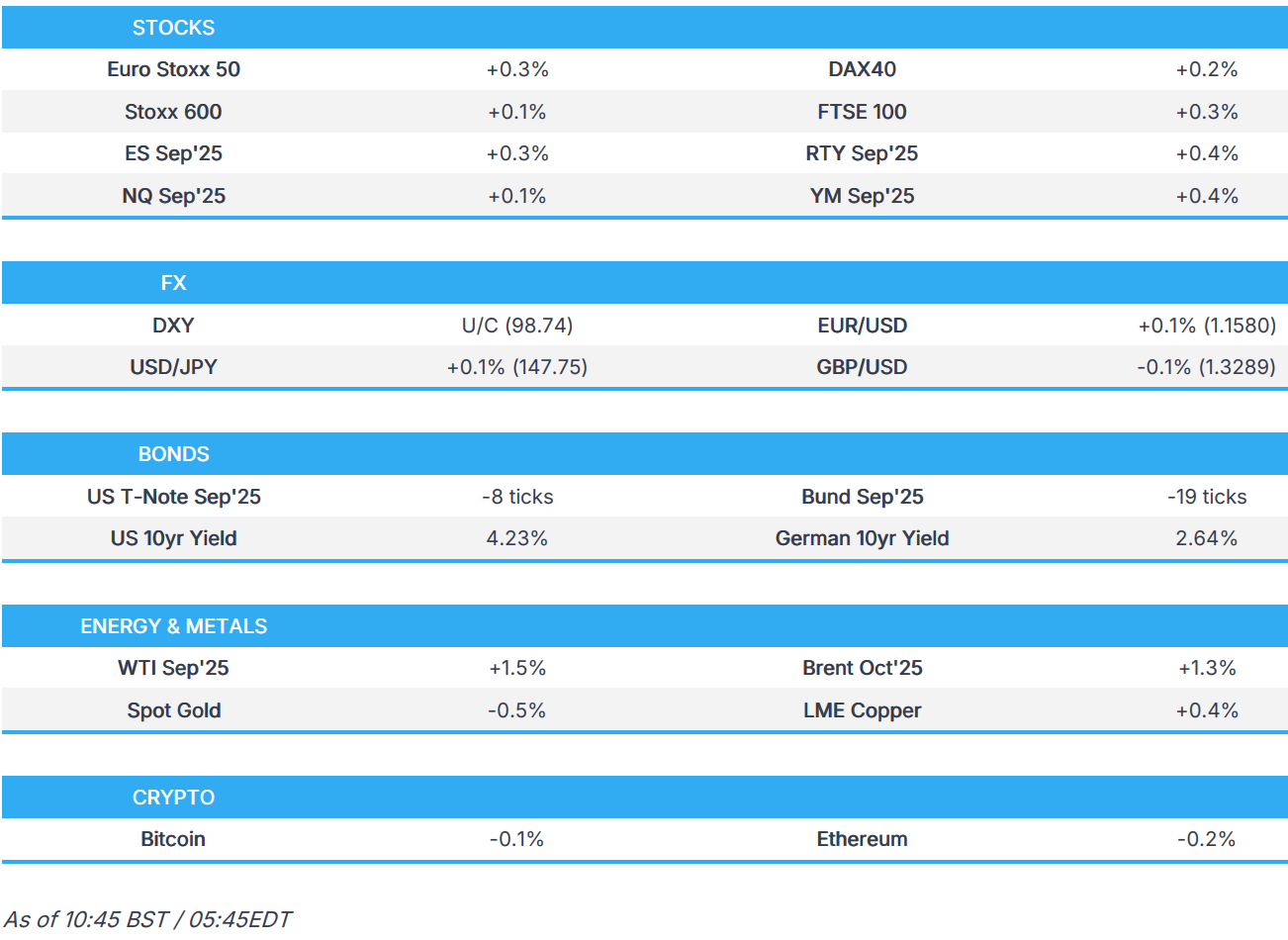

- European bourses are modestly higher alongside US futures, RTY outperforms a touch.

- USD is steady as markets ponder Trump's Fed Chair nominee; Antipodeans lead whilst havens lag.

- Gilts hit by the latest assessment of Reeves' fiscal situation, USTs await supply & Fed speak.

- Crude rises as secondary Russian oil sanctions loom alongside US-Russia talks.

- Looking ahead, Fed’s Collins, Cook and Daly, Supply from the US, Earnings from AppLovin, DraftKings, Airbnb, Lyft, Uber, Shopify, Walt Disney, McDonalds.

TARIFFS/TRADE

- Canada's Foreign Minister Anand said they agreed to build a work plan between Canada and Mexico to focus on supply chains, energy security and others, while she added that trade talks with the US continue to be constructive.

- South Korea's Industry Minister said they need to hold further discussions on the timing of US tariff cuts on autos.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) opened modestly firmer across the board and have traded at elevated levels throughout the morning. Though, the European benchmarks and US futures have been gradually fading from best into the arrival of US participants.

- European sectors hold a strong positive bias, with only really two clear underperformers today. Healthcare sits right at the foot of the pile, dragged down by post-earning losses in Novo Nordisk (-1%). The Danish Ozempic-maker initially opened higher after its Q2 metrics, but then gradually dipped into the red. Most headline metrics were weaker than expected, but Wegovy sales marginally beat expectations. Real Estate leads, lifted after Vonovia (+5%) posted strong H1 metrics and lifted guidance.

- US equity futures (ES +0.3% NQ +0.1% RTY +0.4%) are firmer across the board, with the RTY marginally outperforming vs peers. AMD is currently lower by 5% in pre-market trade after Q2 sales beat estimates, but adj. EPS missed, and it flagged uncertainty over sales of its Instinct MI308 AI chip in China, complicating its otherwise upbeat outlook.

- Tesla (TSLA) CEO Musk says Tesla is training a new FSD model; "Probably ready for public release end of next month if testing goes well”.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

KEY EARNINGS

- Novo Nordisk (-2%): Q2 metrics mostly lower, but Wegovy sales beat expectations.

- Siemens Energy (-1%): Q3 figures beat expectations across the board.

- Glencore (-3%): Mixed set of results, with a surprise Net Loss in H1'25; does not believe a US listing would be "value accretive”.

FX

- DXY is flat in what has been a relatively indecisive start to the week for the USD alongside (relatively) quiet market conditions. Tuesday's soft outturn for ISM services was not enough to nudge the dollar lower with some mindful of the increase in the prices paid component as the impact of the Trump administration's tariff policy filters into the US economy. Focus remains on personnel at the Fed with US President Trump stating that the Fed Governor decision will be made by the end of the week. Today's data docket is a light one, whilst the speaker slate sees comments from Fed voters Collins and Cook, and non-voter Daly (who spoke earlier in the week). DXY is currently contained within Tuesday's 98.58-99.07 range.

- EUR is steady vs. the USD as updates from the Eurozone remain relatively non-incremental in the wake of last week's EU-US trade agreement. Retail Sales data for June showed a M/M and Y/Y improvement and upward revisions to the priors. However, this had little follow-through into the EUR. EUR/USD remains on a 1.15 handle and capped by its 200DMA at 1.1592.

- JPY is fractionally softer vs. the USD after losing out on Tuesday, to the greenback. Macro focus for Japan overnight was on the latest domestic wage data, which saw Labour Cash Earnings rise to 2.5% from 1.4% (Exp. 2.5%). USD/JPY continues to eye a test of 148 to the upside. If breached, the high from Monday kicks in at 148.08.

- GBP is marginally softer vs. the USD in the run up to tomorrow's BoE policy announcement and MPR. Expectations are unanimous in expecting a 25bps reduction in the Base Rate. Within the vote split, Morgan Stanley expects a 1:7:1 outcome with Mann voting for a hold and Dhingra voting for a 50bp cut. UK press has been focusing today on the fiscal situation with a report from the NIESR Institute suggesting that UK Chancellor Reeves needs to raise taxes immediately to fill a GBP 50bln hole in the public finances. NIESR's Deputy Director said the scale of tax rises required would be equivalent to a 5p increase to the basic and higher rates of income tax. GBP/USD remains within Tuesday's 1.3260-3316 range.

- Antipodeans are both are stronger vs. the USD and at the top of the G10 leaderboard alongside the firmer risk tone. NZ jobs data overnight was mixed as the unemployment rate ticked higher and wage gains outpaced analyst consensus. Overall, further easing from the RBNZ is expected given the muted inflation outlook with 52bps of loosening seen within the next year.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are on the backfoot, into a 10yr supply. US docket is weighted towards the end of the day with supply, earnings and Fed speak from Collins, Cook and Daly. Into this, USTs are softer given the modestly constructive risk tone and as the benchmark continues to ease from post-NFP highs; though, once again, magnitudes are modest with USTs in a thin six+ tick range. If the downside picks up and the current 112-00+ base is breached, then support resides at the 111-31+ Monday WTD low, below this a bit of a gap before the figure and then lows from the last few weeks below 111-00.

- Bunds follow global peers, but with magnitudes much more contained. Bunds spent the overnight session contained before picking up to a 130.41 peak early doors with gains of six ticks at best. Thereafter, the benchmark began to gradually fade in limited newsflow but experienced a pickup in bearish pressure on a Bloomberg report that Germany is preparing a EUR 100bln fund for investment in strategic assets. Since, newsflow has been light aside from Retail Sales for the bloc which printed mixed vs consensus while the priors were revised higher, but spurred no move.

- Gilts are underperforming today, as it reacts to the NIESR’s latest forecast on the UK economy, which estimates a current fiscal deficit of GBP 41.2bln in the 2029-30 period. UK press is heavily focussed on this report, largely running with headlines that Reeves will need to find just over GBP 51bln in the Autumn Budget; a figure formed of the above deficit, and an assumed desire to restore headroom to around the GBP 9.9bln figure. Gapped lower by 33 ticks before extending another six to a 92.36 trough. A move that took the benchmark to within reach of Monday’s 92.24 WTD base; below that, support features at 91.96, 91.70 and 91.44 from the week before.

- Germany sells EUR 1.262bln vs exp. EUR 1.5bln 1.00% 2038 and EUR 0.782bln vs exp. EUR 1bln 3.25% 2042 Bund

- Click for a detailed summary

COMMODITIES

- Firmer trade in the crude complex despite a lack of fresh catalysts during the European morning, but as traders deal with the uncertainty of US secondary tariffs for the purchase of Russian oil - US Special Envoy is currently meeting with Russian President Putin, regarding Trump's peace deadline. WTI resides in a 65.11-66.26/bbl range while Brent sits in a USD 67.74-68.78/bbl range.

- Precious metals trade lower across the board with global haven assets on a slightly softer footing this morning. Price action this morning has been contained for the yellow metal, in a USD 3,364.97-3,385.36/oz range, compared to Tuesday's USD 3,349.89-3,390.60/oz parameter, and with the 50 DMA today at USD 3,346.41/oz.

- Base metals regain some composure following recent selling pressure, but the recovery is limited amid the mixed risk appetite in Asia and Europe. 3M LME copper prices reside in a USD 9,625.20-9,692.00/t range.

- US Private Inventory Data (bbls): Crude -4.2mln (exp. -0.6mln), Distillate +1.6mln (exp. +0.8mln), Gasoline -0.9mln (exp. -0.4mln), Cushing +1.7mln.

- Russia's crude output was slightly above the OPEC+ target in July.

- Iraqi Oil Minister says bp (BP/ LN) will begin developing Kirkuk oil fields in less than a month.

- Nigeria's Dangote oil refinery (650k bpd) is planning a 15 day maintenance on its gasoline-making RFCC unit from Aug 10, IIR says.

- Iraq Oil Minister says oil exports through Turkey's Ceyhan pipeline to resume on Wednesday or Thursday.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HCOB Construction PMI (Jul) 44.7 (Prev. 45.2)

- French HCOB Construction PMI (Jul) 39.7 (Prev. 41.6)

- German HCOB Construction PMI (Jul) 46.3 (Prev. 44.8)

- Italian HCOB Construction PMI (Jul) 48.3 (Prev. 50.2)

- UK S&P Global Construction PMI (Jul) 44.3 vs. Exp. 48.8 (Prev. 48.8)

- Italian Industrial Output MM SA (Jun) 0.2% vs. Exp. -0.1% (Prev. -0.7%, Rev. -0.8%)

- EU Retail Sales MM (Jun) 0.3% vs. Exp. 0.4% (Prev. -0.7%, Rev. -0.3%); Retail Sales YY (Jun) 3.1% vs. Exp. 2.6% (Prev. 1.8%, Rev. 1.9%)

NOTABLE EUROPEAN HEADLINES

- ECB's Holzmann reiterated in an interview that there is no reason to cut rates again.

- UK Chancellor Reeves needs to raise taxes immediately to fill a GBP 50bln hole in the public finances, according to NIESR via the Telegraph. NIESR's Deputy Director said the scale of tax rises required would be equivalent to a 5p increase to the basic and higher rates of income.

- Germany reportedly readies EUR 100bln fund to invest in strategic assets, according to Bloomberg; in a bid to secure sectors such as defence, critical raw materials, and energy

NOTABLE US HEADLINES

- US President Trump is to make an announcement at 16.30EDT/21:30BST at the Oval Office on Wednesday, according to his public schedule.

- US President Trump said the Fed Governor decision will be made by the end of the week and they have a couple of candidates, while he added that they are looking at the Fed Chair which is down to four people with 'two Kevins and two other people'.

- Punchbowl News reports "Senate Democrats are pressing for new data on the fallout if boosted Obamacare subsidies are allowed to lapse at the end of the year."

GEOPOLITICS

- Russia's Kremlin spokesman Peskov said improving Russia-US relations requires overcoming existing inertia which will take time, according to TASS.

- Russian and Chinese ships will conduct joint patrols in the Asia-Pac region following exercises in the Sea of Japan.

- North Korea received Russia's help in modernising nuclear weapons carriers, according to Yonhap citing Ukrainian news.

- US President Trump will host leaders from Armenia and Azerbaijan for peace talks at the White House on Friday.

CRYPTO

- Bitcoin is a little lower and trades around USD 114k.

APAC TRADE

- APAC stocks traded somewhat mixed following the subdued handover from Wall St, where the attention was on the various comments from US President Trump and with sentiment dampened amid disappointing ISM Services data.

- ASX 200 gained at the open with strength in the materials, mining and resources sectors spearheading the advance in the index to a fresh record high.

- Nikkei 225 pared its opening losses and gradually extended higher amid gains in the heavy industry stocks, while softer-than-expected labour cost data and negative real cash earnings supports the case for the BoJ to continue to refrain from resuming its policy normalisation.

- Hang Seng and Shanghai Comp were varied in rangebound trade with little fresh drivers and after the PBoC reiterated China's support pledges including to strengthen macroeconomic policy orientation and optimise the environment for policy implementation.

NOTABLE ASIA-PAC HEADLINES

- RBI kept the Repurchase Rate unchanged at 5.50%, as expected, and maintained a neutral stance with the MPC vote on the repo rate and policy stance made unanimously. RBI Governor Malhotra stated geopolitical uncertainties have somewhat abated and growth is robust but below aspirations and tariff uncertainties are still evolving. Malhotra also stated that monetary policy transmission is still continuing and that current macroeconomic conditions and the outlook call for a continuation of the policy rate at current levels. Furthermore, he stated the Indian economy is navigating a steady growth path and monetary policy has appropriately used available space to support growth, while he also revealed that the FY26 real GDP growth view was retained at 6.5% and the FY26 CPI inflation view was cut to 3.1% from 3.7% previously.

- South Korea is to offer visa-free entry to Chinese tourists from September 29th.

- New Zealand announced steps to replace the petrol tax in the coming years with road user charges and is to pass the legislation in 2026.

- South Korean Finance Minister says in talks with US finance authorities on FX; South Korean Finance Minister says FX rates should be determined by markets in principle; does not have specific direction in mind for FX rates.

DATA RECAP

- Japanese Labour Cash Earnings (Jun) 2.5% vs Exp. 3.1% (Prev. 1.4%)

- Japanese Real Cash Earnings YY (Jun) -1.3% vs Exp. -0.7%

- New Zealand HLFS Job Growth QQ (Q2) -0.1% vs. Exp. -0.1% (Prev. 0.1%)

- New Zealand HLFS Unemployment Rate (Q2) 5.2% vs. Exp. 5.3% (Prev. 5.1%)

- New Zealand HLFS Participation Rate (Q2) 70.5% vs. Exp. 70.7% (Prev. 70.8%)

- New Zealand Labour Cost Index QQ (Q2) 0.6% vs. Exp. 0.6% (Prev. 0.4%)

- New Zealand Labour Cost Index YY (Q2) 2.2% vs. Exp. 2.3% (Prev. 2.5%)