US Market Open: Sentiment bolstered with US-Russia meeting expected; BoE, Trump orders & Speech ahead

07 Aug 2025, 11:30 by Newsquawk Desk

- US President Trump said they are going to be putting a very large tariff on chips and semiconductors, which will be at approximately 100%, but added "if you're building in the US, there will be no charge."

- Kremlin Aide Ushakov says an agreement has been reached to hold a meeting with US President Trump and Russian President Putin in the next few days.

- Stocks have been boosted after a Kremlin aide confirmed Trump and Putin are to meet.

- USD is broadly weaker, Antipodeans lead whilst the GBP eyes BoE rate cut.

- Gilts modestly lower into the BoE; initial upside in Bunds have now since pared.

- Crude was pressured amid optimism surrounding Russia-Ukraine, but downside has since pared.

- Looking ahead, US Jobless Claims, Wholesale Sales (Jun) NY Fed SCE, Atlanta Fed GDP, BoE Announcement, MPR & DMP, CNB & Banxico Announcements, Speakers including BoE's Bailey & Fed’s Bostic, Supply from the US.

TARIFFS/TRADE

- US President Trump said they are going to be putting a very large tariff on chips and semiconductors, which will be at approximately 100%, but added "if you're building in the US, there will be no charge."

- US President Trump posted late on Wednesday that "RECIPROCAL TARIFFS TAKE EFFECT AT MIDNIGHT TONIGHT! BILLIONS OF DOLLARS, LARGELY FROM COUNTRIES THAT HAVE TAKEN ADVANTAGE OF THE UNITED STATES FOR MANY YEARS, LAUGHING ALL THE WAY, WILL START FLOWING INTO THE USA."

- US official said the 15% tariff will stack on top of pre-existing tariff rates applied to imports from Japan, unlike in the case of the European Union, according to Kyodo.

- South Korea claimed Samsung Electronics (005930 KS) and SK Hynix (000660 KS) will not be subject to 100% US tariffs, while Taiwan said TSMC (2330 TT) is exempt from US President Trump's 100% chip tariff.

- Apple (AAPL) suppliers are reportedly betting on a tariff carve-out for India-made iPhones, according to Nikkei sources.

- Maersk (MAERSKB DC): "The effective container-weighted import tariff on US imports is estimated at 24% as per the Presidential Executive Order dated 31 July, up from 5% in 2024"

EUROPEAN TRADE

EQUITIES

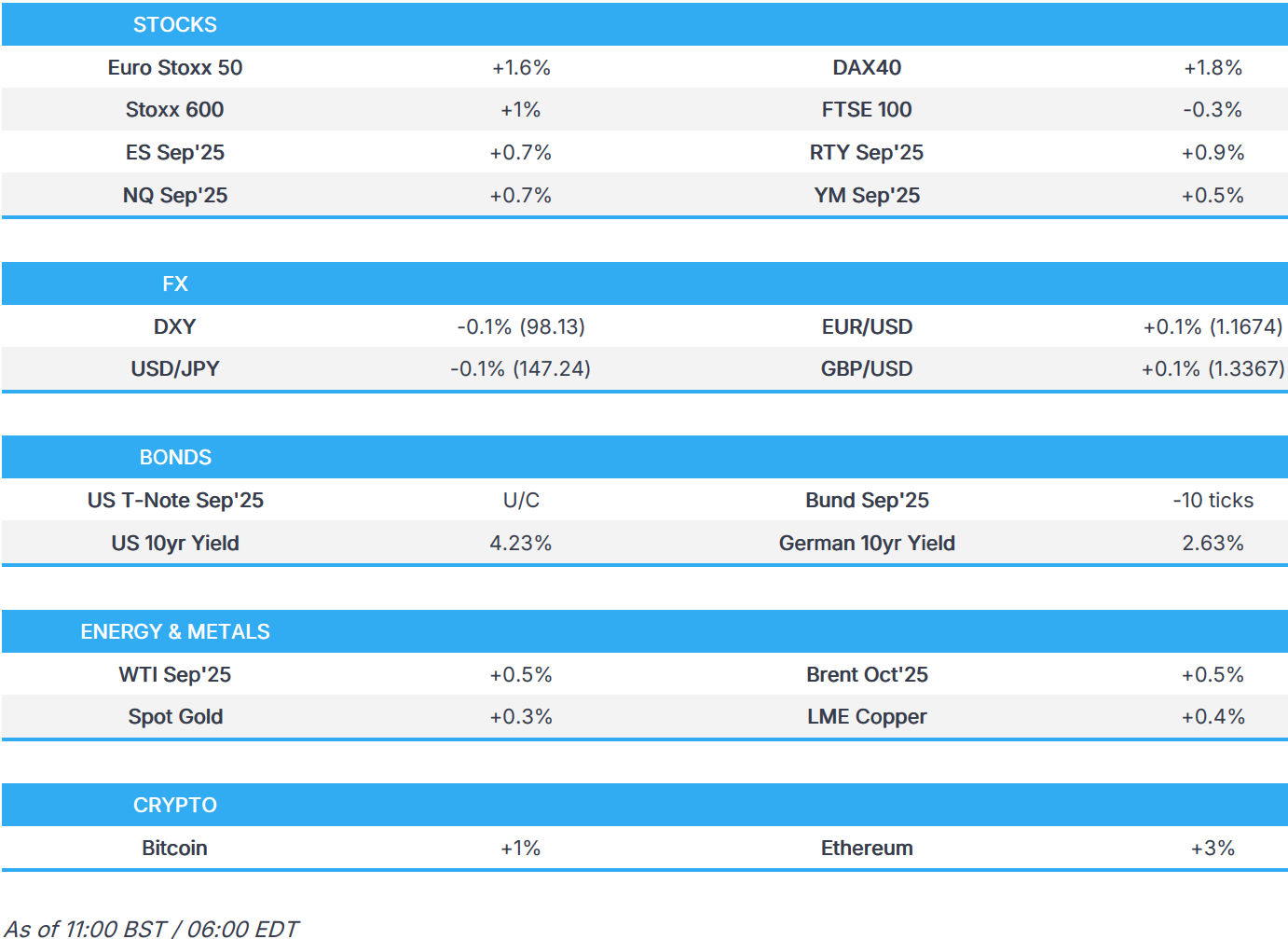

- European bourses (STOXX 600 +0.9%) opened mostly higher, albeit with very modest gains. Since then, indices gradually edged higher, then followed by a more pronounced bid following commentary from a Russian Kremlin aide, who said an agreement had been made for a Presidential meeting between Trump and Putin, in the next few days.

- European sectors opened mixed but now hold a slight positive bias. Insurance takes the top spot, lifted by post-earnings strength in the likes of Allianz (+2%) and Zurich Insurance (+1%). Elsewhere, Travel & Leisure has been buoyed by upside in IHG, after it reported strong H1 metrics; European gambling names are also broadly higher today, in tandem with upside in US-peer DraftKings which reported a record rev. and EBITDA. The Tech sector finishes off the top 3, benefiting from a) the risk tone and, b) US President Trump announcing that the US will slap 100% tariffs on imported chips, but will exempt those firms who manufacture in the US/have committed to do so. On this, ASML (+2%) has gained, given the proposition incentivises relocating to the US, which may boost demand for manufacturing units.

- US equity futures (ES +0.7% NQ +0.7% RTY +0.9%) are in the green and currently trading towards session highs, in tandem with European equities; a recent bid seen amidst the earlier mentioned Putin-Trump meeting.

- Apple (AAPL) suppliers are reportedly betting on a tariff carve-out for India-made iPhones, according to Nikkei sources.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

KEY EARNINGS

- DraftKings (+6% pre-market) - Q2 adj. EPS 0.38 (exp. 0.41), Q2 revenue USD 1.513bln (exp. 1.43bln). CEO highlighted record revenue, net income, and adj. EBITDA with 37% Y/Y revenue growth.

- Maersk (+2%) - Q2 (USD): Revenue 13.1bln (exp. 12.47bln); upgrades FY25 guidance

- Deutsche Telekom (-5%) - Q2 2025 (EUR) Revenue 28.7bln (exp. 28.7bln), Adj. EBITDAaL 11bln (prev. 10.82bln Y/Y).

- Rheinmetall (-4%) - H1 2025 (EUR): Revenue 4.7bln (exp. 4.89bln), EPS 3.79 (exp. 3.75); confirms guidance.

- Siemens (-1%) - Q3 2025 (EUR): Revenue 19.4bln (exp. 19.32bln), Net Income 2.05bln (exp. 1.97bln, prev. 2.13bln Y/Y), Industrial Profit 2.82bln (co. consensus 2.82bln), Comparable Revenue Growth +5% (exp. +3.85%); affirms guidance.

FX

- DXY is down for a second day in a row and extending its move below its 200DMA at 98.21. The USD is continuing to be hampered as markets contemplate Trump's next move with regards to personnel at the Fed. Note, the USD may also be losing ground as geopolitical tensions recede a touch with the Russia and Ukraine conflict potentially nearing a conclusion. Today's data docket includes weekly claims data, the Atlanta Fed GDPNow Tracked and the NY Fed SCE release. Next downside target for DXY comes via the 29th July low at 97.49.

- EUR is a touch firmer vs. the broadly weaker USD in a week that has been lacking in incremental drivers for the Eurozone. Some positivity for the bloc may be gleaned from developments on the geopolitical front following Wednesday's discussion between the US and Russia, which was said to have made progress and with President Trump intending to meet Russian President Putin as soon as next week. EUR/USD has extended its rise on a 1.16 handle but is yet to crack the 1.17 mark with the pair topping out at 1.1698.

- In what has been an indecisive start to the week for USD/JPY, the Yen is eking out mild gains vs. the greenback. This comes in spite of comments from a US official that the now-effective 15% tariff will stack on top of pre-existing tariff rates applied to imports from Japan, unlike in the case of the European Union. USD/JPY delved as low as 146.70 overnight but has since made its way back onto a 147 handle.

- GBP is relatively steady vs. the USD as markets brace for the upcoming BoE rate decision, minutes and MPR. Analysts are virtually unanimous in expecting the BoE to lower the Base Rate by 25bps to 4.0% with markets assigning a 93% probability of such an outcome. The move would follow the MPC’s preference for cutting at a quarterly pace and alongside MPR meetings. With regards to the decision to lower rates, consensus looks for a 7-2 outcome. With the likes of Mann and potentially one of Pill or Greene to vote for an unchanged rate. However, when looking at the magnitude of the vote split, this could lead to a three-way split in the event that MPC dove Dhingra and one of Ramsden or Taylor backs a larger 50bps reduction.

- Antipodeans are both are building on the gains seen on Wednesday vs. the USD with upside today following on from encouraging Chinese trade data which showed a surprise growth in imports and a larger-than-expected increase in exports.

- PBoC set USD/CNY mid-point at 7.1345 vs exp. 7.1709 (Prev. 7.1409)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are flat and ultimately awaiting today's risk events which include; jobless claims, unit labour costs, Atlanta Fed GDP Now and then a 30yr auction. As a reminder, the prior day saw a soft 10yr outing after a poor 3yr earlier. No further insight into the potential fat finger in USTs seen on Wednesday in the run-up to supply, where 30 minute volume spiked to over 300k from sub-100k throughout the session to that point. As a reminder, the move also occurred alongside a move in the implied odds (via Polymarket) for the next Fed Chair, with NEC Director Hassett’s jumping by just under bp and overtaking former Fed Governor Warsh as the front-runner. his morning, action (and volumes) has been much more minimal with USTs in a very narrow 112-03+ to 112-07 band.

- Bunds are a little lower. No reaction to the morning’s Industrial and Trade data from Germany for June. Though, Bunds did pick up a little bit a handful of minutes after the data came through. The soft set of Industrial data, to the lowest since May 2020, potentially influenced; a series that may have factored into the pressure seen in the DAX 40 future at the time. Since, newsflow has slowed a little but more recently Bunds have edged a little lower back towards lows.

- Gilts were flat but more recently some pressure has been seen. The BoE is expected to cut rates and likely via a 7-2 split to ease. However, the full vote breakdown could see a three-way split. Mann and potentially one other (possibly Pill or Greene) likely to vote for unchanged, while Dhingra and possibly the likes of Taylor and/or Ramsden voting for a 50bps cut. Leaving a majority of Bailey, Lombardelli, Breeden and then possibly one or more of Pill, Green, Taylor or Ramsden; depending on the above. Benchmark opened lower by 14 ticks before extending another six to a 92.45 trough. Since, it has reverted back towards Wednesday’s 92.65 close into the BoE.

- Spain sells EUR 5bln vs exp. EUR 4.0-5.0bln 2.40% 2028, 3.20% 2035 & 3.45% 2043 Bono and EUR 0.49bln vs exp. EUR 0.25-0.75bln 1.0% 2030 I/L Bono.

- France sells EUR 10.499bln vs exp. EUR 8.5-10.5bln 1.25% 2034, 1.25% 2036, 0.50% 2040, and 4.00% 2055 OAT.

- Click for a detailed summary

COMMODITIES

- Crude futures are firmer after choppy trade earlier. This follows the decline on Wednesday amid Russia/Ukraine optimism following the discussion between the US and Russia, which is said to have made progress and with President Trump intending to meet Russian President Putin as soon as next week. Russia's Kremlin this morning confirmed that US President Trump and his Russian counterpart, Putin, will meet, and preparations for a summit in the next few days are underway. WTI currently resides in a 64.12-65.08/bbl range while Brent sits in a USD 66.70-67.58/bbl range.

- Precious metals are rebounding following the prior day's losses, with spot gold marginally gaining after recent dollar weakness and as reciprocal tariffs took effect. Some pressure seen on the aforementioned Trump-Putin meeting announcement, which saw the yellow-metal swing from highs back towards overnight ranges. Currently in a USD 3,365.30-3,397.58/oz range.

- Copper futures are rangebound with a slightly firmer tilt amid the softer dollar, risk appetite in stocks, and the encouraging Chinese trade data overnight, which showed stronger-than-expected exports and surprise growth in the nation's imports. 3M LME copper prices reside in a USD 9,672.90-9,740.00/t range.

- Kuwait's oil minister expects crude prices to remain above USD 72/bbl; says the market is healthy with moderate demand growth.

- Click for a detailed summary

NOTABLE DATA RECAP

- Swedish CPI YY Flash (Jul) 0.8% vs. Exp. 0.9% (Prev. 0.7%); MM (Jul) 0.3% vs. Exp. 0.4% (Prev. 0.5%)

- Swedish CPIF Ex Energy Flash YY (Jul) 3.1% vs. Exp. 3.2% (Prev. 3.3%); MM (Jul) 0.2% vs. Exp. 0.2% (Prev. 0.7%)

- German Trade Balance, EUR, SA (Jun) 14.9B vs. Exp. 17.3B (Prev. 18.4B); Exports MM SA (Jun) 0.8% vs. Exp. 0.5% (Prev. -1.4%); Imports MM SA (Jun) 4.2% vs. Exp. 1.0% (Prev. -3.8%)

- French Imports, EUR (Jun) 58.253B (Prev. 56.654B, Rev. 56.595B); Exports, EUR (Jun) 50.63B (Prev. 48.888B, Rev. 48.962B); Current Account (Jun) -3.4B (Prev. -3.1B, Rev. -2.6B)

NOTABLE EUROPEAN HEADLINES

- Germany's VDA says the EU-US trade deal has brought no clarity or improvement for the German auto industry.

NOTABLE US HEADLINES

- Fed's Daly (2027 voter) said there's cautiousness which is tempering growth but not stalling out, while she commented that they will likely need to adjust policy in the coming months and can't wait for perfect clarity to act. Daly also commented that tariffs are unlikely to boost inflation persistently in a way that monetary policy would need to offset. She also noted that the labour market has softened and additional slowing would be unwelcome. Furthermore, Daly said they need to recalibrate monetary policy to match risks to the Fed’s goals.

- US President Trump said, regarding the Fed pick, that the interview process has started and it is probably down to three candidates, while he added that the two Kevins are very good, and a temporary governor is to be named in the next few days.

- US President Trump confirmed that Apple (AAPL) is to invest USD 600bln into the US and said Apple is to manufacture chips in Texas, Utah, Arizona and New York.

- US President Trump is scheduled to sign executive orders on Thursday at 12:00EDT/17:00BST.

GEOPOLITICS

RUSSIA-UKRAINE

- Kremlin Aide Ushakov says an agreement has been reached to hold a meeting with US President Trump and Russian President Putin in the next few days. Meeting venue has been agreed and will be announced later. US Envoy Witkoff touched on an idea of a three-way meeting between Trump-Zelensky-Putin; Moscow left it without comment.

- US President Trump said they had very good talks with Russian President Putin and there's a good chance that there will be a meeting very soon, while he also commented that more secondary sanctions are coming regarding Russia.

- US Secretary of State Rubio said it was a good day regarding efforts to end the Ukraine war but there is still a lot of work ahead and many impediments to overcome.

- Ukrainian President Zelensky said he discussed Witkoff's visit to Moscow in a call with Trump and said that Russia should end this war, while he also commented that pressure on Russia is working and it's crucial they do not deceive them, as well as commented that it looks like Russia is more inclined to a ceasefire.

- Ukrainian President Zelensky calls on Russian President Putin to hold meeting to 'end war', via Al Arabiya.

OTHER

- South Korean military said South Korea and the US are to conduct major joint military exercises beginning on August 18th although an official stated that some parts of the joint drills are postponed to September, while the military drills will test an upgraded response to a heightened North Korea nuclear threat.

CRYPTO

- Bitcoin is a little firmer and trades just shy of USD 115k whilst Ethereum sees gains to a larger magnitude; currently USD 3.7k.

APAC TRADE

- APAC stocks traded mixed as reciprocal tariffs took effect overnight and following the latest tariff threat from US President Trump who plans to impose 'approximately 100%' tariffs on chips and semiconductors unless manufacturers build in the US.

- ASX 200 pulled back from record highs despite the surprise growth of imports from Australia's largest trading partner.

- Nikkei 225 pared initial losses and briefly reclaimed 41,000 amid a busy slate of earnings and as markets shrugged off comments from a US official that the US will not exempt Japan from stacking 15% tariffs on top of existing levies.

- Hang Seng and Shanghai Comp ultimately kept afloat after the latest Chinese trade data which showed stronger-than-expected exports and surprise growth in the nation's imports.

NOTABLE ASIA-PAC HEADLINES

- BoK Governor Rhee said the US trade deal takes a huge burden off monetary policy at the August meeting.

- SoftBank Group (9984 JT) Q1 2025 (JPY): Net Sales 1.82tln (exp. 1.82tln), Net Income 421.82bln (exp. 158.23bln), sees FY dividend at 44.0 (exp. 44.00)

- Baidu (9888 HK) to launch new advanced reasoning model by end of month, according to WSJ.

- Magnitude 6.2 earthquake hits sea off Taiwan's north-eastern coast, according to central weather administration.

- Japan Government Official says, a private-sector member of Government Economic Council, says, are worried that the BoJ being behind the curve vs inflation, which is already affecting the livelihood of people.

- S&P affirms China's Sovereign rating at A+/A-; Outlook Stable. Overview: Strong fiscal stimulus will help keep China's economic growth resilient amid continued headwinds from the weak property sector and new pressures on external trade. "We affirmed our 'A+' long-term and 'A-1' short-term foreign and local currency sovereign credit ratings on China." The stable outlook on the long-term rating reflects our view that the Chinese economy will return to self-sustaining growth of above 4% over the next few years, paving the way for smaller annual increases in net general government debt. Downside scenario: "We could lower the ratings if we believe the government will continue with larger fiscal stimulus measures than we currently expect over the next three to five years. This would likely stem from more persistent downward pressure on economic growth than we currently expect. The resulting fiscal impact would cause the net change in general government debt to stay close to, or above, 6% of GDP annually." Upside scenario: "We may raise our ratings on China if fiscal consolidation is faster than what we anticipate, resulting in a persistent decline in net general government debt to below 30% of GDP, or government interest payments falling below 5% of revenue consistently, or both."

DATA RECAP

- Chinese Trade Balance (USD)(Jul) 98.2B vs. Exp. 105.0B (Prev. 114.8B)

- Chinese Exports YY (USD)(Jul) 7.2% vs. Exp. 5.4% (Prev. 5.8%); Imports YY (USD)(Jul) 4.1% vs. Exp. -1.0% (Prev. 1.1%)

- Chinese Trade Balance (CNY)(Jul) 705.1B (Prev. 826.0B)

- Chinese Exports YY (CNY)(Jul) 8.0% (Prev. 7.2%); Imports YY (CNY)(Jul) 4.8% (Prev. 2.3%)

- Australian Balance on Goods (Jun) 5,365M vs. Exp. 3,400M (Prev. 2,238M)

- Australian Goods/Services Exports (Jun) 6.0% (Prev. -2.7%); Imports (Jun) -3.1% (Prev. 3.8%)

- New Zealand Inflation Forecast 1 Yr (Q3) 2.37% (Prev. 2.41%)