US Market Open: US equity futures marginally gain; USD is firmer paring some the pressure seen on Trump naming Miran to the Fed

08 Aug 2025, 11:03 by Newsquawk Desk

- POTUS suggested there will be no India tariff talks until things are resolved; Bessent said China tariffs can be on the table "at some point".

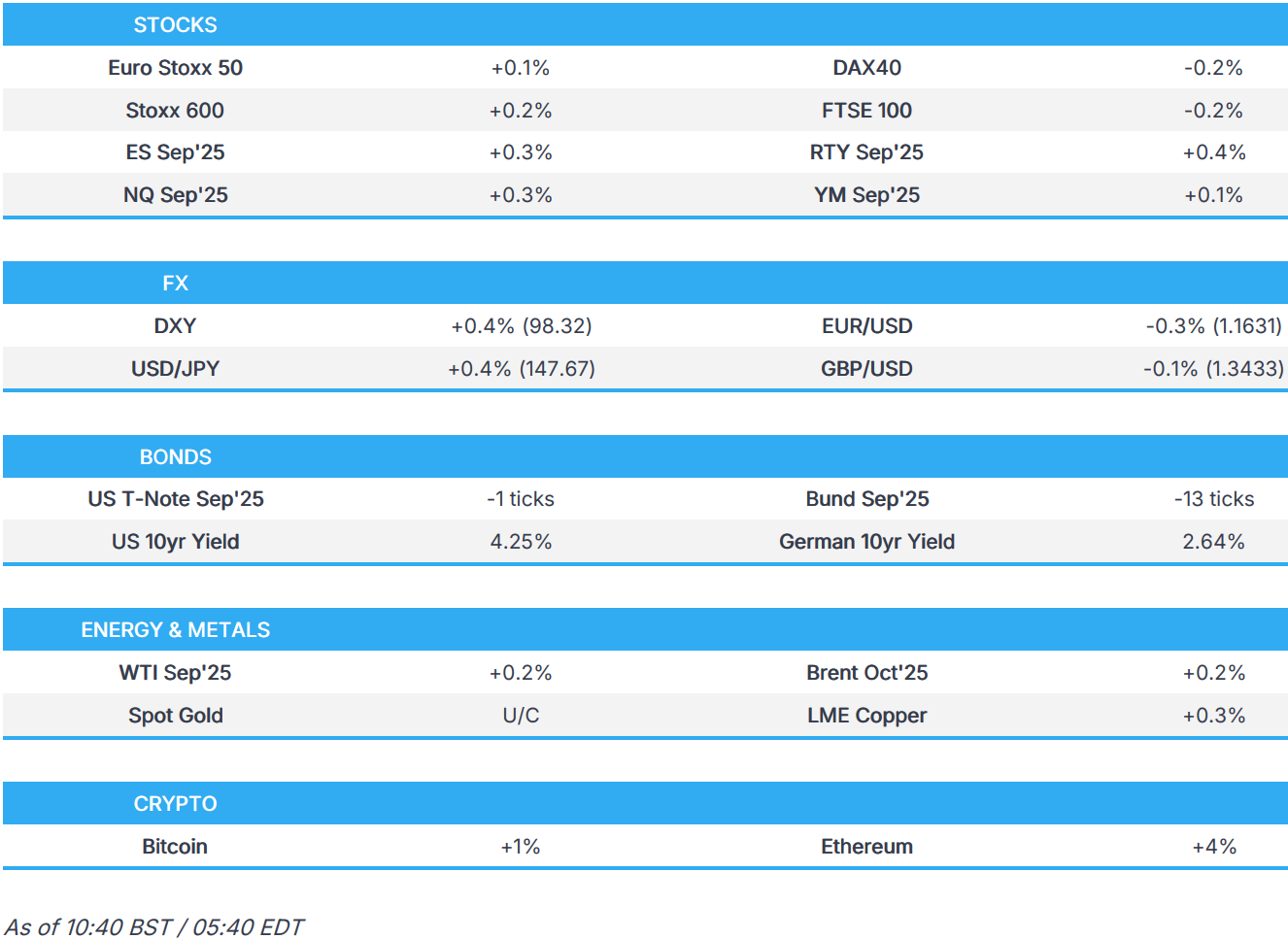

- European bourses are mostly incrementally firmer in quiet newsflow; US futures are also marginally higher, with some mild outperformance in the RTY.

- DXY is modestly higher, paring some of the downside seen in the prior day; JPY underperforms.

- Bonds hold a slight bearish bias, Gilts in focus and lagging pre-Pill.

- Initial downward bias in crude complex has since reversed, to trade slightly higher; XAU flat.

- Looking ahead, Canadian Jobs Report (Jul), Japanese LDP Joint Plenary Meeting, Speakers including BoE's Pill & Fed’s Musalem, Earnings from fuboTV, Tempus AI, Wendy's.

TARIFFS/TRADE

- US President Trump suggested there will be no talk on the India tariff until they get things resolved.

- US Treasury Secretary Bessent said China tariffs can be on the table at some point and that President Trump is using tariffs as an instrument of foreign policy, while he stated the TikTok deal is separate from a China trade deal. Furthermore, Bessent said the BRICs countries' meeting is largely ceremonial and the Fed lacks logic on rates, according to a Fox News interview.

- Japan's trade negotiator Akazawa said it is regrettable that the US stacked tariffs despite the trade deal but added that they have been able to confirm a non-stacking stance from the US and there is no discrepancy between the US and Japan that there is no tariff stacking. Furthermore, he noted that the US said it will refund any extra tariffs retroactively going back to August 7th and the US side expressed regret over the erroneous citation in the executive order.

- Japan's government said top tariff negotiator Akazawa held talks with US Commerce Secretary Lutnick for 3 hours and Treasury Secretary Bessent for 30 minutes on Thursday in which both sides reaffirmed the importance of steadily implementing measures that benefit the interests of both Japan and the US under the Japan-US agreement. Furthermore, Akazawa urged the US side to correct the executive order regarding reciprocal tariffs and Japan will continue to maintain close communication with the US side at various levels.

- Brazil's VP Alckmin said a plan with measures to mitigate the effects of US tariffs is expected to be announced by Tuesday.

- US Customs Border Protection agency said one-kilo and 100-ounce gold bars should be classified under a customs code subject to levies which is a fresh blow to Switzerland, according to FT citing a ruling letter dated July 31st.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) opened mostly modestly firmer and have traded sideways throughout the session, in very quiet newsflow.

- European sectors hold a very slight positive bias. Basic Resources top the pile – nothing specific driving the upside, simply just a case of upside across the underlying metals complex. The clear underperformer today is Insurance, which has been hit by post-earning losses in Munich Re (-8%), where the Co. slashed its Insurance rev. forecast.

- US equity futures (ES & NQ +0.3%, RTY +0.4%) are very modestly firmer across the board, as price action stabilises a touch from the mixed performance on Thursday, with modest outperformance in the RTY.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is on a firmer footing today. The US macro narrative remains primarily focused on personnel changes at the Fed after reporting that CEA Chair Miran is to fill ex-Governor Kugler's position on the FOMC, albeit temporarily. Consensus suggests that he will join Waller and Bowman in backing rate cuts during his tenureship. In terms of the top job at the Fed, reporting via Bloomberg has suggested that Waller is now the frontrunner. Waller has been a dovish outlier on the Fed but will be perceived more positively than either of the two Kevins. Today's docket is light on data, whilst the speaker slate contains 2025 Musalem, albeit the subject matter suggests it may be light on monetary policy guidance. DXY is just about holding above the 98 mark and moved back above its 200DMA at 98.18.

- EUR/USD is lower but contained within Tuesday's 1.1610-99 range after the pair ran out of steam ahead of the 1.17 mark. It has been an exceptionally quiet week for the Eurozone, with the USD very much in the driving seat for the pair. Some traders are mindful of events surrounding Russia-Ukraine and whether this could have some positive read across for EUR. To the upside, 1.17 remains the key source of focus for the pair. To the downside, support is provided by the 200DMA at 1.1606.

- JPY is softer vs. the USD amidst a relatively indecisive week for the pair. In what has been a confusing few days on the trade front between Japan and the US, Japanese trade negotiator Akazawa has confirmed the non-stacking stance from the US, and there is no discrepancy between the US and Japan that there is no tariff stacking. On the BoJ, the Summary of Opinions from the July meeting showed the Bank debated the chance of resuming rate hikes. USD/JPY is currently tucked within Thursday's 146.69-147.71.

- GBP has faltered after yesterday's BoE-induced gains vs. the USD. To recap, the BoE pulled the trigger on another 25bps rate cut. However, the decision to do so was subject to more hawkish dissent than the market was positioned for and subsequently saw traders push back their expectations for policy loosening. Greater clarity could be provided today by comments from Chief Economist Pill, who backed a hold yesterday. The next upside target for Cable comes via the 1.35 mark with the 200DMA just north of this level at 1.3504.

- Antipodeans are both are fractionally softer vs. the USD in what has been a solid showing for AUD/USD and NZD/USD this week.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A slightly softer start to the day, but once again, movement at this point is very thin in a sub-five tick range. Note, while action has intensified in the latter part of sessions this week that may not be the case today, as the docket is very light; however, any update on the Fed Chair, tariffs or geopols, among other topics, could see action intensify once again in the latter half of the day. In a narrow 112-00+ to 112-04 band so far. Newsflow since the Fed updates yesterday has been light. In brief, Trump appointed Miran to the Fed taking Kugler’s spot until the term ends in January.

- Softer start to the day for Bunds also, though magnitudes are marginally more eventful than those outlined above. In a 130.01-26 band, getting back towards but still shy of Thursday’s 130.37 best. As above, drivers are light today after a packed week for markets. The European-specific docket is devoid of Tier 1 events, as such impetus may be drawn from any update to the potential catalysts outlined in UST.

- Gilts are directionally in-fitting with the above but magnitudes are slightly more pronounced. Opened lower by just under 20 ticks and then slipped a handful further to a 92.15 trough, but has since reverted back to between today’s 92.22 open and Thursday’s 92.40 close. Remarks from Chief Economist Pill just after midday will be in particular focus. Pill was part of the four who voted to leave rates at 4.25% (decision was, ultimately, a 25bps cut), the four’s main point of justification was “a slower loosening of policy would reduce the risk of inflation not meeting the target sustainably.”.

- Click for a detailed summary

COMMODITIES

- WTI and Brent price action has been choppy today, but are currently slightly firmer. To recap, nothing really behind the downside this morning, but seemingly a continuation of overnight/this week’s price action as markets continue to price out the cooling geopolitical risk premia in the complex. The reversal also lacked catalysts, but perhaps as traders turn their attention to the developments in Gaza/Israel, whereby Israel’s Security Cabinet approved plans to occupy Gaza City. In terms of the US-Russia meeting, the White House pushed back on comments from Russia's Kremlin, which suggested a meeting had been agreed to. WTI and Brent currently sit in a USD 63.19-97/bbl and USD 65.80-66.57/bbl range respectively; currently towards highs.

- Gold is contained, holding around the USD 3.4k/oz mark in USD 3381-3409/oz parameters. The main point of newsflow was a report in the FT that the US Customs Border Protection agency is to classify 1 kilo and 100 ounce gold bars as subject to levies, according to the FT citing a July 31st ruling.

- Base metals are broadly contained. Specifics light and the APAC handover was a mixed one caught between earnings and trade uncertainty into next week’s deadlines. At best, 3M LME Copper has breached USD 9.7k but has failed to make any real traction above it with ranges from earlier in the week also fairly lacklustre.

- Russia has increased repair activity at some oil refineries, via Ifx.

- Click for a detailed summary

NOTABLE DATA RECAP

- Swiss Consumer Confidence (Q3) -28.0 (Prev. -39.0)

NOTABLE US HEADLINES

- UK CMA has decided not to refer to Boeing (BA) and Spirit Aerosystems (SPR) merger to a Phase 2 investigation.

GEOPOLITICS

MIDDLE EAST

- Israel's security cabinet approved PM Netanyahu's proposal for the occupation of Gaza City to defeat Hamas and the IDF will prepare to take control of Gaza City while providing humanitarian aid to the civilian population outside the combat zones, according to Axios's Ravid.

- Israeli media said the army intends to impose a siege on Gaza City from all sides and the army will begin a large-scale campaign to call up the reserve forces, according to Sky News Arabia.

RUSSIA-UKRAINE

- US President Trump said regarding a Russia-Ukraine ceasefire that it is up to Russian President Putin and that Putin doesn't have to agree to meet with Ukrainian President Zelensky to meet with him.

- Polish PM Tusk says "I think a pause in the conflict in Ukraine could be close".

OTHER

- US President Trump posted that he looks forward to hosting the President of Azerbaijan and the Prime Minister of Armenia at the White House on Friday for a historic peace summit.

CRYPTO

- Bitcoin is a little firmer today, trading above USD 116k; Ethereum outperforms and touches levels not seen since December 2024.

APAC TRADE

- APAC stocks traded mixed following the mostly lacklustre handover from Wall St and amid a deluge of earnings releases.

- ASX 200 was rangebound with the index contained as gains in the mining, resources and materials sectors were offset by losses in tech, healthcare, telecoms and financials.

- Nikkei 225 outperformed and briefly reclaimed the 42,000 status, while the TOPIX hit a fresh record high with sentiment underpinned after Japan was able to confirm a non-stacking stance regarding tariffs from the US and with momentum also helped by earnings releases including from SoftBank, whose shares surged by a double-digit percentage after its profit beat.

- Hang Seng and Shanghai Comp were mixed amid ongoing uncertainty heading into next week's tariff truce deadline.

NOTABLE ASIA-PAC HEADLINES

- BoJ Summary of Opinions from the July meeting stated a member said the BoJ is likely to continue raising rates if the economy and prices move in line with its forecasts, while a member said that given high uncertainty on whether the BoJ's forecast materialises, it must judge the outlook without preconception. It was also noted that there was no change to the view that underlying inflation will stall before re-accelerating despite the Japan-US tariff agreement, and it was stated that US monetary policy and the direction of FX moves may change sharply depending on US consumer inflation and labour data, so policy must be judged after looking at more data. Furthermore, a member said they need at least two to three months to gauge the impact of US tariff policy and it there was also the opinion that the BoJ must proceed with further rate hikes when the chance opens up, as Japan's policy rate is still below neutral and it must raise rates in a timely fashion to avoid being forced to hike rapidly and cause huge damage to Japan's economy.

- China Auto Industry CPCA says China sold 1.852mln passenger cars in July, +6.9% Y/Y; Tesla (TSLA) exported 27,269 in July.

- China Q2 Prelim Current Account Balance 135.1bln (prev. 165.3bln).

DATA RECAP

- Japanese All Household Spending MM (Jun) -5.2% vs. Exp. -3.0% (Prev. 4.6%)

- Japanese All Household Spending YY (Jun) 1.3% vs. Exp. 2.6% (Prev. 4.7%)

- Japanese Current Account NSA JPY (Jun) 1348.2B vs. Exp. 1480.0B (Prev. 3436.4B)