US Market Open: Fixed bid & stocks mixed in thin August trade ahead of Trump-Putin summit on Friday

11 Aug 2025, 11:55 by Newsquawk Desk

- US President Trump said he will meet with Russian President Putin on August 15th in Alaska; White House is considering inviting Ukrainian President Zelensky.

- Fed’s Bowman (voter) said that the latest job market data reinforces her forecast for three rate cuts this year.

- Fed Chair list now said to include former St. Louis Fed President Bullard and former George W. Bush adviser Sumerlin, according to WSJ.

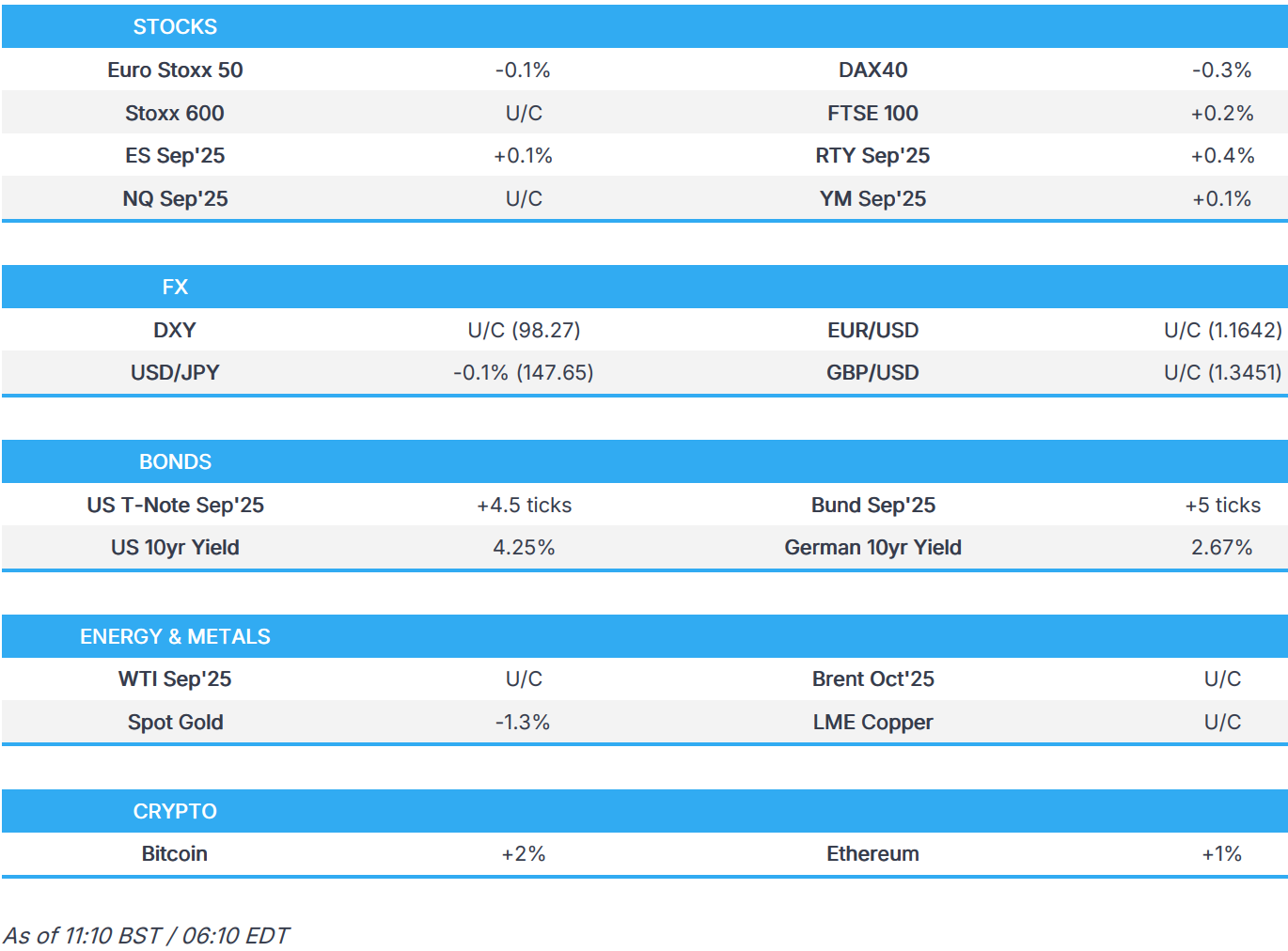

- European bourses opened firmer but dipped lower as the risk tone deteriorated, US futures are mixed; NVIDIA -1% & AMD -2% to pay 15% of Chinese chip sale revenue to US Government.

- Choppy trade in FX amidst quiet newsflow ahead of this week's risk events; DXY is flat.

- Bonds are bid as the risk tone deteriorates ahead of a packed weekly docket; Gilts outperform.

- Crude initially subdued on the US-Russia meeting, but now flat; XAU continues to edge lower currently around USD 3,356/oz.

- Looking ahead, highlights include BoC SLOS (Q2).

TARIFFS/TRADE

- US President Trump posted "China is worried about its shortage of soybeans. Our great farmers produce the most robust soybeans. I hope China will quickly quadruple its soybean orders. This is also a way of substantially reducing China’s Trade Deficit with the USA. Rapid service will be provided. Thank you President XI."

- US Treasury Secretary Bessent expects trade issues to be finished by October, according to Nikkei.

- US licensed NVIDIA (NVDA) to export chips to China after CEO Huang met with US President Trump, while it was also reported that NVIDIA and AMD (AMD) will pay 15% of China chip revenues to the US government, according to FT.

- China wants the US to relax export controls on chips as part of a trade deal, according to FT.

- Mexico’s government said it fixed minimum prices for exports of fresh tomatoes following the end of an antidumping investigation suspension agreement with the US, while it noted that the decision protects producers, prevents market distortions and ensures national supply.

EUROPEAN TRADE

EQUITIES

- European bourses began the session on the front foot, attempting to add to a two-day win streak, though early morning gains pared amid pressure in the risk tone alongside the opening of the US Premarket: NVIDIA (-1.4%), AMD (-2.7%), after reports that they will pay 15% of China chip revenues to the US government, according to FT.

- European sectors opened almost entirely in the green, though in line with the broader risk tone, have since turned more negative. Healthcare outperforms after Novartis (+2.2%) said both Ianalumab Phase III clinical trials met primary endpoints. Utilities lags, dragged down by Orsted (-27%) after a DKK 60bln rights issue.

- US equity futures are mixed, with the NQ flat whilst the RTY outperforms, benefiting from the lower yield environment ahead of the week’s aforementioned risk events, including the Trump-Putin meeting, US CPI and Retail sales.

- Tesla (TSLA) executive said expanding Robotaxi coverage in Austin, Texas; will launch Robotaxi in some Asian markets. Building a service coverage centre with mobile service, collision centre, and remote diagnostics. First service coverage centre expected to open in Mumbai, India, in September. Will set up charging station and an approved collision centre in Bangalore.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is relatively flat intraday during the European morning after kicking off APAC the week, marginally softer in APAC trade with little fresh major macro catalysts from over the weekend, and as participants look ahead to US CPI data due on Tuesday. In terms of Fed speak, there were comments from Fed's Bowman over the weekend who warned that delayed action risks further labour market erosion and the need for a possible bigger cut, as well as noted that the latest job market data reinforces her forecast for three rate cuts this year. Several Fed speakers are scattered throughout the week after Tuesday's US CPI data. Aside from US data and Fed speak this week, attention will also be on the Trump-Putin summit on Friday, which has the intention of ending the war between Russia and Ukraine. DXY is currently confined to a narrow 98.03-98.27 range, still within Friday's 97.95-98.35 parameter.

- EUR/USD mildly strengthened but with price action contained within Friday's parameters amid quiet newsflow from the bloc, albeit potentially underpinned by the Russia-US meeting on efforts to end the war in Ukraine. EUR/USD resides in a 1.1635-1.1675 range, within Friday's 1.1628-1.1679 range.

- JPY was initially modestly firmer in choppy trade despite a relatively flat Dollar in a move that coincided with a rise in US Treasuries. This comes after JPY lacks demand overnight amid the absence of Japanese participants due to the Mountain Day holiday closure. USD/JPY resides in a 147.33-147.79 range with Friday's range between 146.71-147.90, and with the 21 DMA also at 147.90 today.

- GBP remains afloat and takes a breather around last week's best levels, albeit with trade muted alongside a quiet calendar for today, which is set to pick up on Tuesday, including with the release of the latest UK employment data.

- Antipodeans struggled for direction in APAC trade owing to a lack of drivers overnight, and with the RBA kick-starting its 2-day policy meeting, which is unanimously expected to result in a 25bps cut.

- RBI has reportedly sold at least USD 5bln to boost FX in a bid to prop up the INR after it weakened to a record low, according to Bloomberg.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- UST futures are trading higher by just under 5 ticks in very quiet newsflow and after a lacklustre session overnight, given JGB cash trade was shut as Japan enjoyed its Mountain Day holiday. Price action this morning has only really been upwards, alongside global peers. Nothing quite behind the upside, but potentially amid a deterioration in the risk tone (stocks moving lower & JPY bid). Upside in fixed income could be explained by: a) latest dovish commentary from Fed’s Bowman, b) Russia-US meeting, c) trade updates (and lack of US-China updates). Currently trading towards the upper end of a 111-25+ to 112-00 range; the peak for the day is just shy of last Friday’s best at 112-02 – further upside could see the potential test of the high from a day earlier at 112-04+.

- Bunds are currently firmer but have waned off best levels in recent trade, in a 129.67 to 130.00 range. As above, nothing behind the upside today, but in line with the risk tone. For Europe specifically, the move could also be explained by less demand for defence-related spending, should a Russia-Ukraine deal be struck on Friday.

- Gilts are also firmer, and are outperforming vs peers. Nothing quite behind the marginal outperformance, particularly in the context of slow UK-specific newsflow. UK paper is currently trading towards the upper end of a 92.00 to 92.37 range; this has breached last Friday’s high at 92.31, with the next level to the upside at 92.66 (8th Aug high).

- Click for a detailed summary

COMMODITIES

- Crude futures were initially pressured as focus was on the US-Russia meeting, but is now flat. Initial pressure due to some geopolitical risk premia unwinds ahead of the Trump-Putin meeting scheduled for this coming Friday, with no sanctions imposed against Russia after Trump's deadline passed last Friday. US President Trump said he will meet with Russian President Putin on August 15th in Alaska, while Russia’s Kremlin confirmed an agreement was reached to organise a meeting between Russian President Putin and US President Trump. The White House is reportedly considering inviting Ukrainian President Zelensky to the Alaska summit, and President Trump is open to a trilateral meeting in Alaska, although the White House is currently planning for a bilateral summit as requested by Russian President Putin. WTI currently resides in a 63.02-63.91/bbl range while Brent sits in a USD 65.81-66.66/bbl range.

- Spot gold pulled back after the choppy performance on Friday, and with resistance around the USD 3,400/oz level. The yellow metal may also be experiencing a geopolitical risk unwind ahead of the Trump-Putin summit in Alaska this coming Friday. Price action this morning has seen the yellow metal slide from a USD 3,401.40/oz peak to a current low at USD 3,358.80/oz, with the 50 DMA seen at USD 3,349.80/oz.

- Copper futures traded indecisively overnight in the absence of major catalysts and after mixed inflation data from its largest buyer, China. Thereafter, the base metals complex tilted mostly lower shortly after the European open as risk waned further.

- Iraq set September Basrah medium crude official selling price to Asia at plus USD 2.15/bbl vs Oman/Dubai average and to Europe at minus USD 1.30/bbl vs Dated Brent, while it set the OSP to North and South America at minus USD 1.00/bbl vs ASCI, according to SOMO.

- Chile’s Codelco said the El Teniente copper mine was approved for a restart by the labour authority and it later announced that it restarted sectors of the El Teniente mine, plant and smelter.

- Contemporary Amperex Technology (300750 CH) suspended production at a major lithium mine in China’s Jiangxi province for at least three months, according to sources familiar with the matter.

- China's Baosteel (600019 CH) said it is to lift hot and cold rolled coil prices for September delivery by USD 200/metric ton and USD 300/metric ton respectively.

- Saudi Crude supply to China set to fall to around 43mln barrels in September, according to Reuters sources.

- Salzgitter (SZG GY) expects muted steel demand through 2025 but forecasts a rebound in 2026 due to German fiscal stimulus and increased EU construction and defence spending. Record-high Chinese steel exports to Europe intensify competitive pressures despite rising domestic prices since July 2025.

- Click for a detailed summary

NOTABLE DATA RECAP

- Norwegian Core Inflation YY (Jul) 3.1% vs. Exp. 3.0% (Prev. 3.1%)

- Norwegian Consumer Price Index MM (Jul) 0.8% vs. Exp. 0.3% (Prev. 0.2%)

- Norwegian Core Inflation MM (Jul) 0.8% vs. Exp. 0.7% (Prev. 0.5%)

- Norwegian Consumer Price Index YY (Jul) 3.3% vs. Exp. 3.0% (Prev. 3.0%)

- Norwegian Producer Price Index YY (Jul) -0.3% (Prev. -1.0%)

- Norwegian CPI Index Number (Jul) 138.9 (Prev. 137.8)

- Italian CPI (EU Norm) Final MM (Jul) -1.0% vs. Exp. -1.0% (Prev. -1.0%); YY (Jul) 1.7% vs. Exp. 1.7% (Prev. 1.7%)

NOTABLE US HEADLINES

- Fed’s Bowman (voter) said core PCE inflation appears to be moving much closer to the 2% target than is shown in the data and it is appropriate to look through temporarily elevated inflation, while she added that upside risks to inflation have diminished and she has more confidence that tariffs won’t mean persistent inflation. Furthermore, Bowman said delayed action risks further labour market erosion and the need for a possible bigger cut, as well as noted that the latest job market data reinforces her forecast for three rate cuts this year.

- US President Trump administration officials are looking at Heritage Foundation chief economist E.J. Antoni, among others, to lead the Bureau of Labor Statistics, according to The Wall Street Journal.

- US President Trump is expected to activate hundreds of National Guard troops for Washington DC, while a final number and what role they could play are still being decided, according to Reuters citing a US official.

- US President Trump’s administration is considering reclassification of marijuana as a less dangerous category of drug, according to WSJ.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu said Israel has no choice but to complete the job and defeat Hamas due to the group’s refusal to lay down its arms, while the new Gaza offensive plans aim to tackle two remaining Hamas strongholds and Israel expects to conclude the new Gaza offensive plan fairly quickly.

- Israeli PM Netanyahu spoke with US President Trump and discussed Israel’s plan to take control of the remaining Hamas strongholds in Gaza to bring an end to the war in Gaza.

- White House Special Envoy Witkoff was reported to meet with Qatar’s PM on Saturday for discussions regarding an end to the Gaza war and the release of hostages.

- Australia's PM Albanese said Australia will recognise the state of Palestine at the UN General Assembly in September, while recognition will be predicated on commitments from the Palestinian Authority. Furthermore, Albanese said the situation in Gaza has gone beyond the world's worst fears and that Israel continues to defy international law, while it was also reported that New Zealand is considering recognition of the state of Palestine with the New Zealand cabinet to make a formal decision in September.

- Iran said an IAEA official is to visit for talks to determine a framework for cooperation, although there are no plans for the IAEA to visit Iranian nuclear sites until there is a framework for cooperation.

- Jordan said it will host a Jordanian-Syrian-American meeting on Tuesday to discuss ways to support the rebuilding of Syria.

- Iranian Foreign Ministry said Tehran may agree to specific restrictions on nuclear activities in exchange for lifting sanctions, via Al Arabiya. Channels with the US still open, via an intermediary

RUSSIA-UKRAINE

- US President Trump said he will meet with Russian President Putin on August 15th in Alaska, while Russia’s Kremlin confirmed an agreement was reached to organise a meeting between Russian President Putin and US President Trump.

- White House is reportedly considering inviting Ukrainian President Zelensky to the Alaska summit and President Trump is open to a trilateral meeting in Alaska, although the White House is currently planning for a bilateral summit as requested by Russian President Putin.

- US VP Vance said the US is in the process of scheduling when Russian President Putin and Ukrainian President Zelensky can sit down and discuss an end to the conflict, while the US will keep dialogue open with Ukraine but doesn’t think it will be productive to have Putin sit down with Zelensky ahead of a meeting with Trump. Furthermore, Vance said President Trump is thinking about tariffs on China for buying Russian oil but hasn’t made any firm decisions, according to a Fox News interview.

- Ukrainian President Zelensky said Ukraine cannot violate the constitution on territory and Ukrainians will not give their land to occupiers, while he added that any solutions without Ukraine will be solutions against peace.

- Russian President Putin was reported on Friday to demand that Ukraine cede Donetsk, Luhansk and Crimea, for Russia to halt the war, while Putin told Witkoff he would agree to a complete ceasefire if Ukraine agreed to withdraw forces from all of Ukraine's Eastern Donetsk region, according to WSJ citing Ukrainian and European officials.

- Joint statement from several EU and UK leaders stated they welcome US President Trump’s work to stop the killing in Ukraine and end Russia’s war of aggression, as well as achieve just and lasting peace and security for Ukraine. Furthermore, the joint statement noted they are convinced that only an approach that combines active diplomacy, support to Ukraine and pressure on the Russian Federation to end the war can succeed.

- Joint statement of the leaders of the Nordic-Baltic eight said they stand ready to contribute diplomatically, while maintaining substantial military and financial support to Ukraine. The joint statement also stated that they will continue to uphold and impose restrictive measures against the Russian Federation.

- Ukraine’s military said on Sunday that it struck an oil refinery in Russia’s Saratov region overnight, while it also announced that Russia attacked Zaporizhzhia with guided aerial bombs which hit residential areas, a bus station and a clinic.

- Polish PM Tusk said Russia must recognise the West rejects demands for Ukraine to cede territory.

OTHER

- Thai soldiers were injured in a landmine blast near the Cambodia border.

- South Korea’s military said North Korea is dismantling loudspeakers from the border area.

- North Korea condemned upcoming US-South Korea joint military drills and said it will exercise its sovereign right against provocation regarding military drills, according to Yonhap.

CRYPTO

- Bitcoin is a little firmer today currently trading around USD 121k; Ethereum soared over the past few days, currently just shy of USD 4.3k.

APAC TRADE

- APAC stocks were mostly in the green but with gains limited and price action contained in the absence of notable catalysts from over the weekend and with Japanese markets closed for a holiday.

- ASX 200 notched a fresh intraday record high with lithium miners boosted after CATL temporarily suspended operations at the Jianxiawo lithium mine in China.

- Hang Seng and Shanghai Comp kept afloat following reports that the US licenced NVIDIA to export chips to China, with the Co. and AMD to pay 15% of China chip revenue to the US government, although gains were capped as participants continued to await an extension to the US-China tariff truce deadline which expires on Tuesday, while inflation data from China was mixed as CPI topped estimates to print flat Y/Y but coincided with a deeper-than-expected deflation in factory gate prices.

NOTABLE ASIA-PAC HEADLINES

- Chinese Industry Association said July vehicle sales +14.7% Y/Y (vs +13.8% in June); January-July vehicle sales +12% Y/Y (prev. +4.4% in January-July 2024). New energy vehicle (NEV) sales +27.4% Y/Y in July. January-July NEV sales +38.5% Y/Y

DATA RECAP

- Chinese CPI MM (Jul) 0.4% vs. Exp. 0.3% (Prev. -0.1%)

- Chinese CPI YY (Jul) 0.0% vs. Exp. -0.1% (Prev. 0.1%)

- Chinese PPI YY (Jul) -3.6% vs. Exp. -3.3% (Prev. -3.6%)