Europe Market Open: AUD little changed post-RBA & Trump extends China tariff suspension

12 Aug 2025, 06:45 by Newsquawk Desk

- US President Trump signed an Executive Order that will extend the tariff suspension on China for another 90 days.

- US President Trump announced on Truth Social that gold will not be tariffed.

- Fed Governor Bowman, Fed Vice Chair Jefferson, and Dallas Fed President Logan are reportedly under consideration for Fed Chair, according to Bloomberg.

- APAC stocks traded mostly higher (Japan outperformed post-holiday), Europe expected to open firmer (Eurostoxx 50 future +0.3%).

- DXY steady, AUD little changed after widely expected RBA rate cut, EUR/USD has returned to a 1.16 handle.

- US President Trump said there will be some swapping and changes in land between Russia and Ukraine.

- Looking ahead, highlights include UK Jobs Report (Jun), German ZEW Survey (Aug), US CPI (Jul), EIA STEO, OPEC MOMR, Fed’s Barkin & Schmid, supply from the UK.

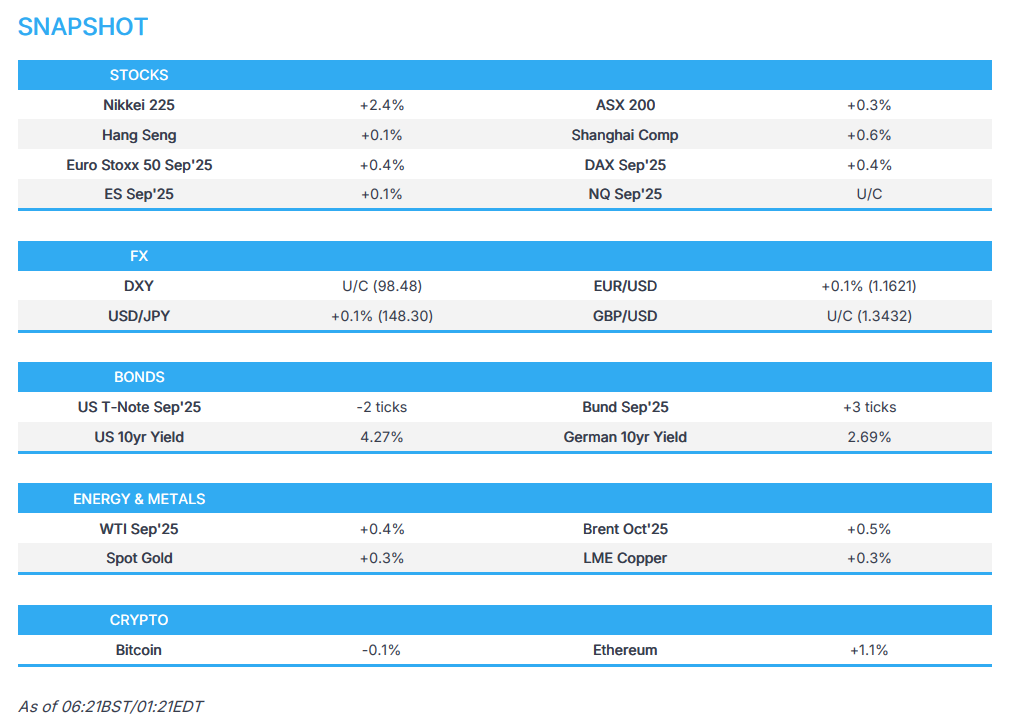

SNAPSHOT

US TRADE

EQUITIES

- US stocks ultimately settled lower to start the week in a day of quiet newsflow, with attention turning to US CPI on Tuesday. Highlights came from over the weekend, whereby US President Trump approved export licenses for NVIDIA (NVDA) and AMD (AMD) to sell chips to China, albeit not tier 1 chips, but in return for 15% of revenue to be paid back to the US government, while the announcement that Trump signed an Executive Order for a 90-day extension to the US-China trade truce was widely expected and garnered little reaction. Meanwhile, sectors were mixed as Consumer Discretionary, Staples, and Health Care outperformed, although Energy, Tech and Real Estate lagged.

- SPX -0.20% at 6,377, NDX -0.36% at 23,527, DJI -0.45% at 43,976, RUT -0.04% at 2,217.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said regarding China trade that they've been dealing nicely and that he has a very good relationship with Chinese President Xi. It was later announced that President Trump signed an Executive Order that will extend the tariff suspension on China for another 90 days and all other elements of the agreement will remain the same.

- China issued a statement on US economic and trade ties in which it stated that China will suspend tariffs for 90 days and will retain an additional 10% tariff rate, while it will adopt and maintain all necessary measures to suspend or remove non-tariff measures taken against the US.

- China updated its export control lists and noted firms can apply to trade with entities under the list and it halted measures on 12 US entities on the export list, while it said it will grant licences if exporters meet requirements and it is suspending adding some US firms to the export control list for 90 days.

- US President Trump said regarding NVIDIA (NVDA) and AMD (AMD) chips that it involves an old chip that China already has and he would not make a deal with NVIDIA’s new advanced chips, while he confirmed a 15% payment on H20 chips to China.

- China urges firms not to use NVIDIA (NVDA) H20 chips in new guidance, according to Bloomberg

- US President Trump announced on Truth Social that gold will not be tariffed.

- Brazilian Finance Minister Haddad said a virtual meeting with US Treasury Secretary Bessent has been called off and no fresh date has been scheduled.

NOTABLE HEADLINES

- Fed Governor Bowman, Fed Vice Chair Jefferson, and Dallas Fed President Logan are reportedly under consideration for Fed Chair, while the White House is on track for a Fed Chair announcement this fall, according to Bloomberg.

- US President Trump is nominating economist Dr. E.J. Antoni as the next Commissioner of the Bureau of Labor Statistics, while he added "Our Economy is booming, and E.J. will ensure that the Numbers released are HONEST and ACCURATE".

- US President Trump posted that he met with Intel (INTC) CEO Lip-Bu Tan along with Commerce Secretary Lutnick and Treasury Secretary Bessent, while he stated "The meeting was a very interesting one. His success and rise is an amazing story. Mr. Tan and my Cabinet members are going to spend time together, and bring suggestions to me during the next week."

APAC TRADE

EQUITIES

- APAC stocks shrugged off the weak lead from Wall St and traded mostly higher with outperformance in Japan on return from the extended weekend and following a deluge of earnings, while participants also reflected on the recent US-China trade truce extension.

- ASX 200 eked slight gains and extended on record highs with only mild tailwinds seen after the RBA delivered a widely expected 25bps rate cut.

- Nikkei 225 surged on return from the long weekend and followed suit to the record-setting performance in the TOPIX with the index underpinned following a slew of earnings releases and recent currency weakness.

- Hang Seng and Shanghai Comp kept afloat following the confirmation of a 90-day extension to the US-China tariff truce with the new deadline set for November 9th.

- US equity futures (ES U/C, NQ U/C) lacked firm direction after the prior day's weakness and with US CPI data on the horizon.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with losses of 0.3% on Monday.

FX

- DXY was little changed but held on to most of the prior day's spoils as participants awaited US CPI data while there were several recent developments but had little sway on price action for the dollar including US President Trump signing an Executive Order to extend the US/China trade truce for 90 days to November 9th, while he announced that gold would not be tariffed, and it was also reported that Fed Governor Bowman, Fed Vice Chair Jefferson, and Dallas Fed President Logan are all under consideration for the Fed Chair with the White House on track for a Fed Chair announcement in the fall.

- EUR/USD regained some composure after a recent brief dip to sub-1.1600 territory but with the rebound limited amid light catalysts from the bloc and as geopolitics remained in the spotlight ahead of the Trump/Putin meeting on Friday.

- GBP/USD lacked direction but is off the prior day's lows after bouncing off support at the 1.3400 level and with UK employment and average earnings data due today.

- USD/JPY marginally extended on recent gains at the 148.00 handle amid the outperformance in Japanese stock markets.

- Antipodeans were choppy following the RBA rate decision which delivered a widely expected 25bps rate cut to lower the Cash Rate to 3.60% and signalled further easing ahead which is in line with the current market consensus.

- PBoC set USD/CNY mid-point at 7.1418 vs exp. 7.1901 (Prev. 7.1405)

FIXED INCOME

- 10yr UST futures remained subdued after the prior day's lacklustre performance heading into US CPI data, while it was also reported that the Trump administration widened potential candidates for Fed Chair with Fed's Bowman, Jefferson, and Logan reportedly under consideration for the position.

- Bund futures traded little changed with price action contained following a failed attempt to reclaim the 130.00 level and as German ZEW data looms.

- 10yr JGB futures conformed to the humdrum mood seen in global counterparts with demand hampered amid a lack of tier-1 data and as Japanese stocks outperformed.

COMMODITIES

- Crude futures were rangebound amid light energy-specific newsflow and as participants await upcoming key events including the Trump/Putin meeting on Friday.

- Spot gold nursed some losses after yesterday's retreat and with an indecisive reaction seen to President Trump's announcement that the precious metal will not be tariffed.

- Copper futures edged higher amid the mostly positive risk appetite in Asia and the 90-day US-China tariff truce extension.

- Chile's Codelco copper production rose 17.3% Y/Y in June to 120.2k tons, while Escondida copper production fell 33% Y/Y in June to 76.4k tons and Collahuasi copper production fell 29.1% Y/Y in June to 34.3k tons.

CRYPTO

- Bitcoin eked slight gains with price action choppy throughout the session on both sides of the USD 119k level.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi held talks with Brazilian President Lula, with the call said to have lasted about an hour and both presidents highlighted willingness to identify new business opportunities between the two economies.

- US President Trump and South Korean President Lee are to hold a summit on August 25th where they will discuss economic cooperation and economic security partnership, as well as the evolving strategic alliance between the two countries.

- RBA cut the Cash Rate by 25bps to 3.60%, as expected with the decision unanimous, while it reiterated that inflation has continued to moderate and the outlook remains uncertain as well as noted that maintaining price stability and full employment is the priority. RBA stated that underlying inflation will continue to moderate to around the midpoint of the 2–3% range, with the cash rate assumed to follow a gradual easing path, and it noted that monetary policy is well placed to respond decisively to international developments if they have material implications for activity and inflation in Australia. Furthermore, it stated the cut was due to underlying inflation continuing to decline back towards the midpoint of the 2–3% range and labour market conditions easing slightly.

DATA RECAP

- Australian NAB Business Confidence (Jul) 7.0 (Prev. 5.0)

- Australian NAB Business Conditions (Jul) 5.0 (Prev. 9.0)

- Singapore GDP QQ (Q2 F) 1.4% (Prelim. 1.4%)

- Singapore GDP YY (Q2 F) 4.4% (Prelim. 4.3%)

GEOPOLITICS

RUSSIA-UKRAINE

- US President Trump said regarding the upcoming meeting with Russian President Putin that it is a feel-out meeting and he is going to tell Putin to end the war, while he thinks they will have a constructive conversation and he will speak with Ukrainian President Zelensky. Furthermore, Trump said the next meeting will be with Zelensky, or with Putin and Zelensky, and there will be some swapping and changes in land.

- Russian Deputy Foreign Minister Ryabkov said he hopes the upcoming meeting between Russian President Putin and US President Trump will give momentum to normalisation of Russia-US relations, according to TASS.

- EU Foreign Policy Chief Kallas said EU foreign ministers expressed support for US steps that will lead to peace in Russia and Ukraine, while they will work on more Russian sanctions and more military support for Ukraine.

EU/UK

DATA RECAP

- UK BRC Retail Sales YY (Jul) 1.8% (Prev. 2.7%)

- UK BRC Total Sales YY (Jul) 2.5% (Prev. 3.1%)

- Barclays UK July Consumer Spending rose 1.1% Y/Y (prev. -0.1% Y/Y in June)