US Market Open: GBP firmer on jobs data; DXY flat into US CPI and Fed speak

12 Aug 2025, 11:15 by Newsquawk Desk

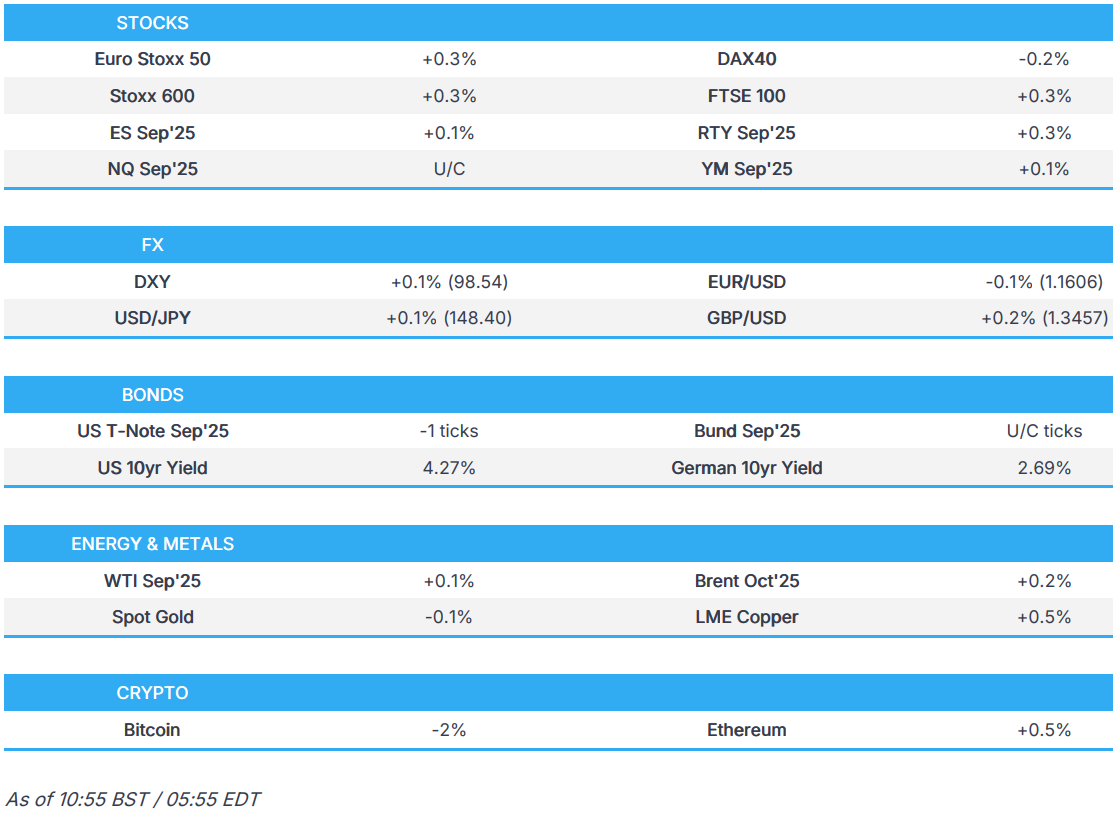

- European bourses are modestly firmer, whilst US futures trade on either side of the unchanged mark into US CPI.

- DXY flat, GBP rises post-data, EUR choppy, and AUD narrowly lag post RBA.

- USTs/Bunds rangebound into US CPI, whilst Gilts lag after jobs data.

- Crude is choppy with focus on Russia-Ukraine with Zelensky flagging a fresh Russian offensive ahead of Friday talks.

- Looking ahead, US CPI (Jul), EIA STEO, OPEC MOMR, Speakers including, Fed’s Barkin & Schmid, Earnings from CoreWeave.

TARIFFS/TRADE

- China issued a statement on US economic and trade ties in which it stated that China will suspend tariffs for 90 days and will retain an additional 10% tariff rate, while it will adopt and maintain all necessary measures to suspend or remove non-tariff measures taken against the US.

- China updated its export control lists and noted firms can apply to trade with entities under the list and it halted measures on 12 US entities on the export list, while it said it will grant licences if exporters meet requirements and it is suspending adding some US firms to the export control list for 90 days.

- China urges firms not to use NVIDIA (NVDA) H20 chips in new guidance, according to Bloomberg

- China’s Commerce Ministry has launched an anti-dumping investigation into Canadian pea starch and announced preliminary investigation results on Canadian canola seed. The ministry also released preliminary findings on imports of halogenated butyl rubber from Canada, Japan, and India. Meanwhile, the Chinese Foreign Ministry urged the US to take practical steps to stabilise global chip supply chains.

- South Africa’s Trade Minister stated the country stands ready to utilise its trade remedy measures to safeguard and protect domestic industry.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) began the session firmer, and continue to hold this bias but in rangebound trade into US CPI.

- European sectors traded mostly in the green (bar Tech) for the entire morning, given the slightly upbeat tone ahead of CPI. Energy trades at the top of the pile with Basic resources nipping at its heels for most of the morning - the latter lifted by strength in underlying iron ore prices.

- US equity futures (ES +0.1% NQ U/C RT+0.3%) are trading mixed. RTY continues to outperform whilst the NQ/RTY hold around the unchanged mark, with traders ultimately focused on US CPI later.

- AMD (AMD) executive said Co. will provide 100k hours of GPU cloud computing at no cost to Malaysian researchers and developers.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is broadly flat vs. peers in the run-up to today's eagerly anticipated US inflation report. Expectations are for core M/M inflation to rise to 0.3% from 0.2% with the Y/Y rate seen rising to 3.0% from 2.9%. On the Fed, Bloomberg reports that Fed Governor Bowman, Fed Vice Chair Jefferson, and Dallas Fed President Logan are now also in the running for the Chair position. Elsewhere, on the trade front, US President Trump has signed an Executive Order that will extend the tariff suspension on China for another 90 days, as expected. DXY is contained within Monday's 98.03-99.67 range.

- EUR is steady vs. the USD as the narrative surrounding the Eurozone remains the same. That narrative being that the ECB is holding policy steady with inflation under control but mindful of any potential growth headwinds in Q3 as the impact of the US tariffs on the Bloc filters through into the data. Today's ZEW deteriorated from the priors and also missed expectations, although it prompted no move in the EUR. EUR/USD has made its way back onto a 1.16 handle, but still some way off Monday's best at 1.1675.

- JPY is fractionally weaker vs. the USD as Japanese participants returned to the market and sent the Nikkei 225 to a record high. Incremental macro drivers for Japan are lacking. USD/JPY has eclipsed Monday's best at 148.25 with a current session high at 148.44.

- Cable is higher in the wake of the latest UK jobs report, which failed to show a marked deterioration in the labour market that some had been positioned for. The ILO unemployment rate held steady at 4.7%, employment change showed a larger-than-expected pick up to 238k from 134k, the contraction in HRMC payrolls change slowed to -8k from -26k and wage growth came in a touch softer than forecast on a headline basis. Overall, the takeaway is that the UK labour market is softening, but the rate of change appears to be slowing. Cable has advanced further on a 1.34 handle but is still shy of Monday's 1.3477 peak.

- AUD is the marginal laggard across the majors in the wake of the latest RBA policy announcement, which saw the central bank pull the trigger on a widely expected 25bps rate cut. The decision to do so was unanimous, and the accompanying policy statement reiterated language that inflation has continued to moderate and the outlook remains uncertain. The central bank also simultaneously released its Quarterly Statement on Monetary Policy which showed a downgrade to the estimate of Australia’s long-run productivity growth to 0.7% from 1.0% and with trend GDP growth now seen around 2.0%, down from 2.25%. AUD/USD has slipped onto a 0.64 handle with a session low at 0.6494.

- PBoC set USD/CNY mid-point at 7.1418 vs exp. 7.1901 (Prev. 7.1405)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs trade with a very mild negative bias, ultimately trading just under the unchanged mark as traders position themselves ahead of today’s US CPI. Price action today has been incredibly boring – rangebound in a tight 111-23 to 111-27+ range. The low for today has breached the trough from Monday (111-24+). Delving into the day’s key risk event, all focus on the US inflation data. US July CPI is expected to rise by 0.2% M/M at the headline level (prev. +0.3%), with the annual rate seen rising to 2.8% Y/Y from 2.7%.

- Bunds trade with a slight negative bias, but ultimately in rangebound trade ahead of US CPI. Currently trading in a 129.49-70 range, with the trough for the day around about 8 ticks below the low from Monday. As was the case in the prior session, the docket from an EZ-perspective has been exceptionally thin and is unlikely to pick up throughout the week. There was German ZEW data earlier, which showed a dip in sentiment in August - likely with participants disappointed by the EU-US trade deal.

- Gilts are underperforming today and lower by around 35 ticks, to trade towards the bottom end of a 91.86 to 92.12 range. This comes after the region’s job report, which overall highlighted a cooling labour market but nothing quite alarming enough for the BoE to accelerate the cutting cycle - as such the report has been considered as more conducive to the Bank's "gradual" monpol approach. Gilt 2030 auction passed without issue, garnering a fairly strong b/c; not entirely surprising given the short-dated maturity of the auction.

- UK sells GBP 4.75bln 4.375% 2030 Gilt: b/c 3.15x (prev. 3.12x), average yield 4.022% (prev. 4.078%) & tail 0.1bps (prev. 0.2bps)

- Click for a detailed summary

COMMODITIES

- Crude futures are rangebound amid light energy-specific newsflow and as participants await US CPI and geopolitical updates. Earlier today, Russian security services reported that an attack on a senior Defence Ministry official was foiled on the outskirts of Moscow, according to Al Arabiya. This did not influence prices at the time, with a wider focus likely on the Trump-Putin meeting this Friday. WTI currently resides in a 64.12-65.08/bbl range while Brent sits in a USD 66.70-67.58/bbl range.

- Spot gold ekes out mild gains after it nursed some losses overnight after yesterday's retreat, and with an indecisive reaction to President Trump's announcement that the precious metal will not be tariffed. Spot gold resides in a USD 3,340.69-3,357.94/oz range, compared to Monday's USD 3,340.09-3,404.19/oz range.

- Copper futures edged higher amid the mostly positive risk appetite in Asia and the 90-day US-China tariff truce extension, which was as expected. 3M LME copper prices reside in a USD 9,733.22-9,789.00/t range.

- Turkey’s Minister of Energy and Natural Resources stated that all options are being studied to increase gas exports to Syria from 3.4 million to 6 million cubic meters per day, according to Sky News Arabia.

- Chile's Codelco copper production rose 17.3% Y/Y in June to 120.2k tons, while Escondida copper production fell 33% Y/Y in June to 76.4k tons and Collahuasi copper production fell 29.1% Y/Y in June to 34.3k tons.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK Avg Wk Earnings 3M YY (Jun) 4.6% vs. Exp. 4.7% (Prev. 5.0%)

- UK ILO Unemployment Rate (Jun) 4.7% vs. Exp. 4.7% (Prev. 4.7%)

- UK Avg Earnings (Ex-Bonus) (Jun) 5.0% vs. Exp. 5.0% (Prev. 5.0%)

- UK Claimant Count Unem Chng (Jul) -6.2k (Prev. 25.9k, Rev. -15.5k)

- UK BRC Retail Sales YY (Jul) 1.8% (Prev. 2.7%)

- UK BRC Total Sales YY (Jul) 2.5% (Prev. 3.1%)

- Barclays UK July Consumer Spending rose 1.1% Y/Y (prev. -0.1% Y/Y in June)

- German ZEW Economic Sentiment (Aug) 34.7 vs. Exp. 39.8 (Prev. 52.7)

- German ZEW Current Conditions (Aug) -68.6 vs. Exp. -65.0 (Prev. -59.5)

- EZ ZEW Survey Expectations (Aug) 25.1 (Prev. 36.1)

NOTABLE US HEADLINES

- US President Trump is nominating economist Dr. E.J. Antoni as the next Commissioner of the Bureau of Labor Statistics, while he added "Our Economy is booming, and E.J. will ensure that the Numbers released are HONEST and ACCURATE".

- US President Trump posted that he met with Intel (INTC) CEO Lip-Bu Tan along with Commerce Secretary Lutnick and Treasury Secretary Bessent, while he stated "The meeting was a very interesting one. His success and rise is an amazing story. Mr. Tan and my Cabinet members are going to spend time together, and bring suggestions to me during the next week."

GEOPOLITICS

MIDDLE EAST

RUSSIA-UKRAINE

- Ukrainian President Zelensky posts "We see that the Russian army is not preparing to end the war. On the contrary, they are making movements that indicate preparations for new offensive operations.".

- Russian Deputy Foreign Minister Ryabkov said he hopes the upcoming meeting between Russian President Putin and US President Trump will give momentum to normalisation of Russia-US relations, according to TASS.

- Russian security services reported that an attack on a senior Defence Ministry official was foiled on the outskirts of Moscow, according to Al Arabiya.

CRYPTO

- Bitcoin is on the backfoot today, cooling from recent upside and trades just above USD 118k; Ethereum continues to rise, and holds around USD 4.3k

APAC TRADE

- APAC stocks shrugged off the weak lead from Wall St and traded mostly higher with outperformance in Japan on return from the extended weekend and following a deluge of earnings, while participants also reflected on the recent US-China trade truce extension.

- ASX 200 eked slight gains and extended on record highs with only mild tailwinds seen after the RBA delivered a widely expected 25bps rate cut.

- Nikkei 225 surged on return from the long weekend and followed suit to the record-setting performance in the TOPIX with the index underpinned following a slew of earnings releases and recent currency weakness.

- Hang Seng and Shanghai Comp kept afloat following the confirmation of a 90-day extension to the US-China tariff truce with the new deadline set for November 9th.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi held talks with Brazilian President Lula, with the call said to have lasted about an hour and both presidents highlighted willingness to identify new business opportunities between the two economies.

- US President Trump and South Korean President Lee are to hold a summit on August 25th where they will discuss economic cooperation and economic security partnership, as well as the evolving strategic alliance between the two countries.

- RBA cut the Cash Rate by 25bps to 3.60%, as expected with the decision unanimous, while it reiterated that inflation has continued to moderate and the outlook remains uncertain as well as noted that maintaining price stability and full employment is the priority. RBA stated that underlying inflation will continue to moderate to around the midpoint of the 2–3% range, with the cash rate assumed to follow a gradual easing path, and it noted that monetary policy is well placed to respond decisively to international developments if they have material implications for activity and inflation in Australia. Furthermore, it stated the cut was due to underlying inflation continuing to decline back towards the midpoint of the 2–3% range and labour market conditions easing slightly.

- RBA Governor Bullock stated there had been no discussions of a larger rate cut, while noting that current forecasts imply the Cash Rate may need to be lower to ensure price stability, with the Board to take decisions on a meeting-by-meeting basis and not ruling out back-to-back rate cuts. She added that the recovery in house prices has been gradual so far, though forecasts are dependent on further rate cuts, and without these, targets would likely be missed. Governor Bullock also said she places little emphasis on the neutral rate, while noting that if the Fed were to lower rates too quickly, it would have global implications. Furthermore, she highlighted that policy remains forward-looking, with the assumption that rates can continue to be lowered.

- Italy PM Meloni seeks to shrink Chinese holdings at key Italian companies, according to Bloomberg.

DATA RECAP

- Australian NAB Business Confidence (Jul) 7.0 (Prev. 5.0)

- Australian NAB Business Conditions (Jul) 5.0 (Prev. 9.0)

- Singapore GDP QQ (Q2 F) 1.4% (Prelim. 1.4%)

- Singapore GDP YY (Q2 F) 4.4% (Prelim. 4.3%)