US Market Open: Stocks firmer, RTY outperforms & DXY extends post-CPI decline

13 Aug 2025, 11:15 by Newsquawk Desk

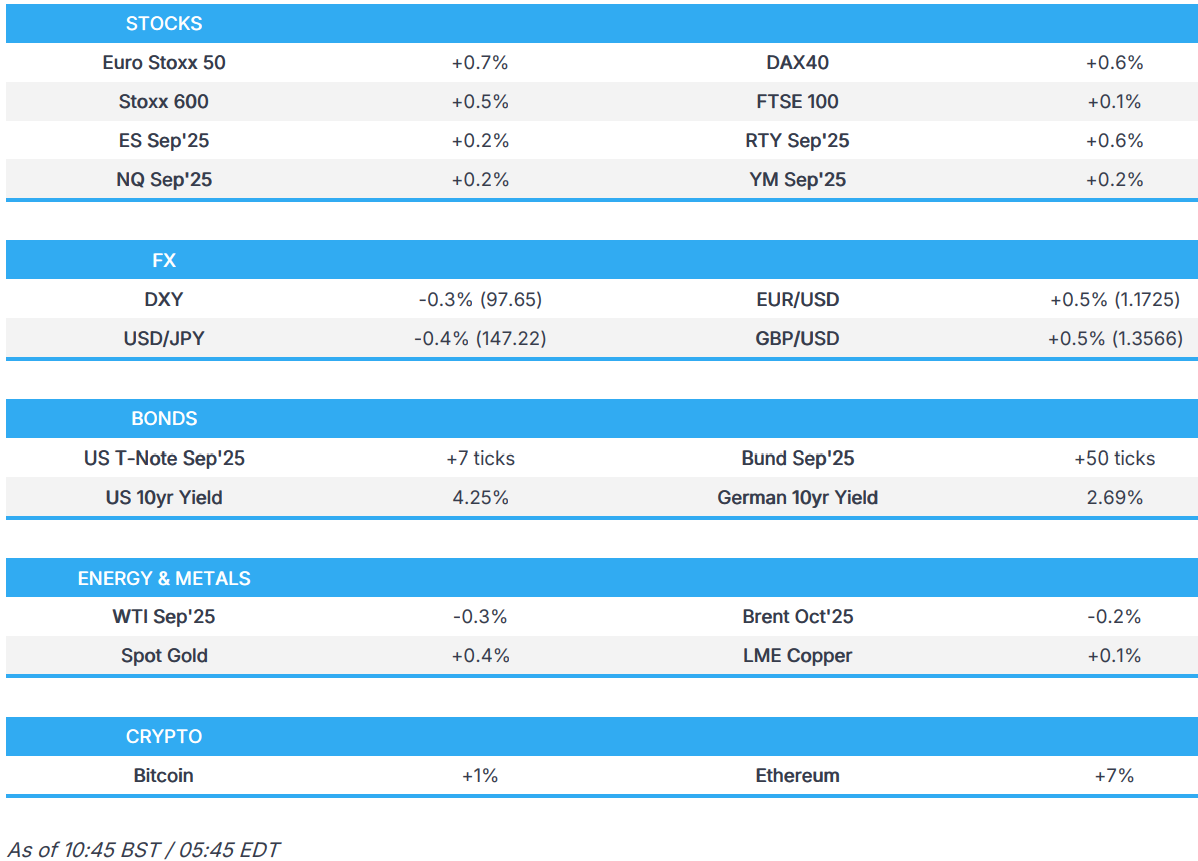

- European bourses are firmer across the board; US futures are also higher, but with outperformance in the RTY.

- Dollar extends its post-CPI decline, leading to broad strength across G10s; Kiwi outperforms.

- Bonds are bid and approaching Tuesday's highs, as focus turns to geopols.

- Crude is subdued, gold kept afloat, and base metals flat; focus on Trump/Putin on Friday.

- Looking ahead, BoC Minutes, US President Trump is to meet with E3 and Ukraine, Speakers including Treasury Secretary Bessent, Fed’s Barkin, Goolsbee & Bostic. Earnings from Cisco.

TARIFFS/TRADE

- US Treasury Secretary Bessent said he will meet again with Chinese officials in the next two or three months and that they are solving several variables with China, while he added they will need to see months, if not a year, of progress on fentanyl flows before Chinese tariffs come down. Furthermore, he said India has been a bit recalcitrant in trade negotiations.

- White House said perhaps the chip deal could expand to other companies.

- Brazil's President Lula said he will sign an executive order on Wednesday creating a BRL 30bln credit line for firms affected by tariffs and plans to help Brazilian exporters will include support through Brazilian government purchases, while he noted that they initiated a WTO dispute over US tariffs and will see what they can do in terms of reciprocity. Lula said they cannot be dependent on the dollar and Brazil does not want to interfere with the dollar but noted they can have a currency for trade within BRICS which is an idea that should be tested. Furthermore, he said they are open to discuss ethanol with the US.

- Canada's government said Canada is deeply disappointed with China's preliminary anti-dumping duties on Canadian canola imports and it remains ready to engage in constructive dialogue with Chinese officials to address their respective trade concerns.

- Chinese Commerce Ministry announces countermeasures against two EU financial institutions, UAB Urbo Bankas and AB Mano Bankas, measures come into effect on August 13th. In response to the EU targeting Chinese firms as part of Russia-related sanctions. Urges the EU to stop damaging Chinese interests.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.4%) opened modestly firmer across the board and have continued to gradually march higher as the morning progressed; currently just off session highs.

- European sectors hold a strong positive bias, with only a handful of sectors residing in the red. Tech takes the top spot, joined closely by Healthcare and Utilities; the latter boosted by post-earning upside in E.ON (+1%), where the Co. reported strong H1 metrics and affirmed its guidance. For Healthcare, Novo Nordisk (+1%) benefits from a broker upgrade at BNP Paribas. Travel & Leisure is found right at the foot, dragged down by Swedish-listed Evolution (-8%). Interestingly, Bloomberg reported that the Co. is under investigation for running black-market activities in banned countries, some of which were/are sanctioned by the US (Iran/Syria).

- US Equity Futures (ES +0.2%, NQ +0.2%, RTY +0.5%) are trading in the green to varying degrees, helped by a softer dollar and the general risk environment post-CPI. RTY continues to outperform amid the constructive risk environment, softer yields and the broad underperformance so far this year.

- WSJ writes "the Trump administration relaxed controls on the NVIDIA (NVDA) H20 chip in July, major Chinese tech companies have ordered at least 700,000 of the chips", according to WSJ sources.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- After a steady start to the session, the DXY has taken another leg lower as markets digest Tuesday's CPI report. Overall, it was broadly in-line and judged not to show an alarming increase in goods inflation related to the US tariff policies. As we mentioned in our commentary on Tuesday, the US is very much not out of the woods when it comes to a potential inflation scare. Today's docket is light on data but is expected to see remarks from Treasury Secretary Bessent, Fed’s Barkin (2027 voter), Goolsbee (voter) & Bostic (2027 voter). DXY has delved as low as 97.63 and is now eyeing the 28th July low at 97.49.

- With a soft outturn for ZEW data overlooked on Tuesday, it remains the case that incremental macro drivers for the Eurozone remain light. As such, the USD is very much in the driving seat for EUR/USD with the pair having now advanced onto a 1.17 handle to hit a new high for the month at 1.1729.

- The broad softness in the USD has acted as a drag on USD/JPY, albeit gains for the JPY against the USD have been more limited than some G10 peers. Some of this may be a by-product of the steepening of the US curve on Tuesday with back-end US yields closing higher on the session. USD/JPY has delved as low as 147.19 with the next support level coming via the 147 mark.

- GBP is on the front foot vs. the USD and towards the top end of the G10 leaderboard. Cable is building on Tuesday's gains, which were triggered by the not-as-bad-as-feared UK labour market report and the US CPI release. Cable has ventured as high as 1.3563 and is now eyeing the July 28th peak at 1.3588.

- Antipodeans are both are benefiting from the pick-up in risk sentiment, which has been seen since Tuesday's US CPI release.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are firmer, but thus far comfortably within Tuesday’s 111-19+ to 112-06 parameters which also mark the WTD high and low, thus far at least. Today’s docket is headlined by geopolitics as European leaders and Ukraine’s Zelensky meet virtually and speak with US President Trump and VP Vance ahead of the one-on-one between Trump and Russian President Putin on Friday; a leaders-only event that has already been downplayed as a listening exercise for POTUS. Docket includes Fed's Barkin and comments from Treasury Secretary Bessent.

- Bunds are bid, outperforming USTs but also shy of Tuesday’s 129.70 peak with a session best thus far of 129.65. If the strength continues and that peak is breached, we look to 130.00 from Monday before 130.26 from last Friday. Strength comes after the ultimately softer session on Tuesday, given the significant turnaround seen after the CPI report. No move to final German CPI/HICP (unrevised) or the July Wholesale Price Index which came in cooler than previous. Bunds were gaining into the German 2035 outing, which garnered fairly weak demand, leading to Bunds dipping off best levels by around 10 ticks.

- Gilts are firmer, broadly in-fitting with the above. Also awaiting the leaders meeting, UK PM Starmer is part of the virtual event and US VP Vance will also be dialling in from the UK. Opened higher by a handful of ticks and has, in-fitting with EGBs/USTs, been extending since to a 92.00 peak but shy of 92.12 from Tuesday. If breached, we look to 92.37 from Monday before 92.66, 92.77 and 92.84 from last week.

- Germany sells EUR 3.885bln vs exp. EUR 5bln 2.60% 2035 Bund: b/c 1.4x (prev. 1.5x), average yield 2.69% (prev. 2.62%), retention 22.3% (prev. 23.36%).

- Click for a detailed summary

COMMODITIES

- Softer trade across the crude complex after declining on Tuesday as participants await the upcoming Trump/Putin meeting in Alaska on Friday. At the same time, demand is not helped by bearish private sector crude inventory data, and it was also reported that the first vessel to load crude bound for the US after the new license had docked at Venezuela's José port. WTI currently resides in a 62.77-63.3.4/bbl range while Brent sits in a USD 65.80-66.32/bbl range.

- Mostly firmer trade across precious metals as the Dollar eases further following Tuesday's US CPI and Trump's threat to sue Fed Chair Powell. Spot gold resides in a USD 3,342.63-3,360.98/oz range, compared to Tuesday's USD 3,331.17-3,359.34/oz parameter, with the 50 DMA at USD 3,349.02/oz.

- US Private Inventory Data (bbls): Crude +1.5mln (exp. -0.3mln), Distillates +0.3mln (exp. +0.7mln), Cushing -0.6mln.

- CPC says oil exports +3% to 6.55mln T in July, according to Reuters sources.

- IEA OMR: Lowers 2025 and 2026 demand growth forecasts; trims 2025 oil demand growth forecast to 680k BPD (prev. 700k BPD); trims 2026 forecast at 700k BPD (prev. 720k BPD); IEA says oil market to face a record supply glut next year

- Click for a detailed summary

NOTABLE DATA RECAP

- German CPI Final MM (Jul) 0.3% vs. Exp. 0.3% (Prev. 0.3%); German CPI Final YY (Jul) 2.0% vs. Exp. 2.0% (Prev. 2.0%)

- Spanish HICP Final MM (Jul) -0.3% vs. Exp. -0.4% (Prev. -0.4%); YY (Jul) 2.7% vs. Exp. 2.7% (Prev. 2.7%)

NOTABLE EUROPEAN HEADLINES

- German Economy Ministry says despite the basic agreement on US tariffs, there are no signs of noticeable economic recovery.

NOTABLE US HEADLINES

- US Authorities said to have embedded location trackers in AI chip shipments to catch illegal diversions to China, according to Reuters sources; trackers found in Dell (DELL), Super Micro (SMCI), NVIDIA (NVDA) & AMD (AMD) shipments.

GEOPOLITICS

MIDDLE EAST

- Hamas said a delegation of the Hamas leadership headed by Khalil al-Haya arrived in Cairo for talks with Egyptian officials, while talks in Cairo will focus on ways to stop the war and bring aid to Gaza, according to Sky News Arabia and Al Hadath.

- France, Germany and the UK are willing to reimpose sanctions on Iran with the E3 telling the UN it is ready to trigger snapback mechanisms if Tehran doesn't resume nuclear talks, according to FT.

- Israeli Military Chief of Staff approved a "main concept" for an attack plan in the Gaza Strip.

- Russian Foreign Minister Lavrov will hold talks with the Indian Foreign Minister on August 21st.

RUSSIA-UKRAINE

- Russia says US President Trump and Russian President Putin are to discuss all of the accumulated issues in bilateral relations.

- US Secretary of Interior Burgum said President Trump targets Russia's oil customers and will shut down Russian oil earnings, according to Fox Business.

- Russian President Putin held a phone call with North Korean leader Kim and updated him on talks with US President Trump, while it was also reported that Kim and Putin pledged deeper cooperation and Putin expressed appreciation for North Korea's help in liberating the Russian Kursk region.

CRYPTO

- Bitcoin is a little firmer and just shy of USD 120k; Ethereum outperforms, now above USD 4.6k.

APAC TRADE

- APAC stocks were mostly higher as the region took impetus from the gains stateside where CPI data was not as hot as feared and kept a September Fed rate cut on the table.

- ASX 200 bucked the trend and was dragged lower by underperformance in Utilities and the top-weighted Financial sector, with the latter suffering amid losses in CBA post-earnings.

- Nikkei 225 continued its advances and rallied to fresh record highs above the USD 43,000 level, while the somewhat varied PPI data from Japan had little influence on price action.

- Hang Seng and Shanghai Comp were underpinned alongside the mostly upbeat mood across the Asia-Pac region and with a briefing by Chinese officials on supporting consumption, while China had announced on Tuesday to provide interest subsidies for qualifying personal consumption loans in the country's latest effort to boost consumption.

NOTABLE ASIA-PAC HEADLINES

- China's Vice Finance Minister said they will support domestic consumption to become a major driving force for the economy, while a Mofcom official said service consumption has big growth potential and supporting service consumption will help expand domestic demand and employment. Furthermore, a PBoC official said they will guide financial institutions to increase credit issuance to the service consumption sector and to streamline the approval process of consumer loans.

- Tencent (700 HK) Q2 2025 (CNY): Revenue 184.50bln (exp. 178.94bln); Adj. Net 63.1bln (exp. 62bln). Operating Profit 60.1bln (exp. 58.5bln). Co. does not declare dividend.

DATA RECAP

- Japanese Corp Goods Price MM (Jul) 0.2% vs. Exp. 0.2% (Prev. -0.2%, Rev. -0.1%); YY (Jul) 2.6% vs. Exp. 2.5% (Prev. 2.9%)

- Australian Wage Price Index QQ (Q2) 0.8% vs. Exp. 0.8% (Prev. 0.9%); YY (Q2) 3.4% vs. Exp. 3.3% (Prev. 3.4%)

- China M2 Money Supply (Jul) +8.8% Y/Y (exp. +8.2%); New Yuan Loans (Jul) CNY -50bln (exp. +300bln); End-July Yuan Lending +6.9% Y/Y (exp. 7.0%); Total Social Financing (Jul) 1.16tln (exp. 1.504tln)