Europe Market Open: Mostly firmer APAC trade into the Alaska summit

15 Aug 2025, 06:50 by Newsquawk Desk

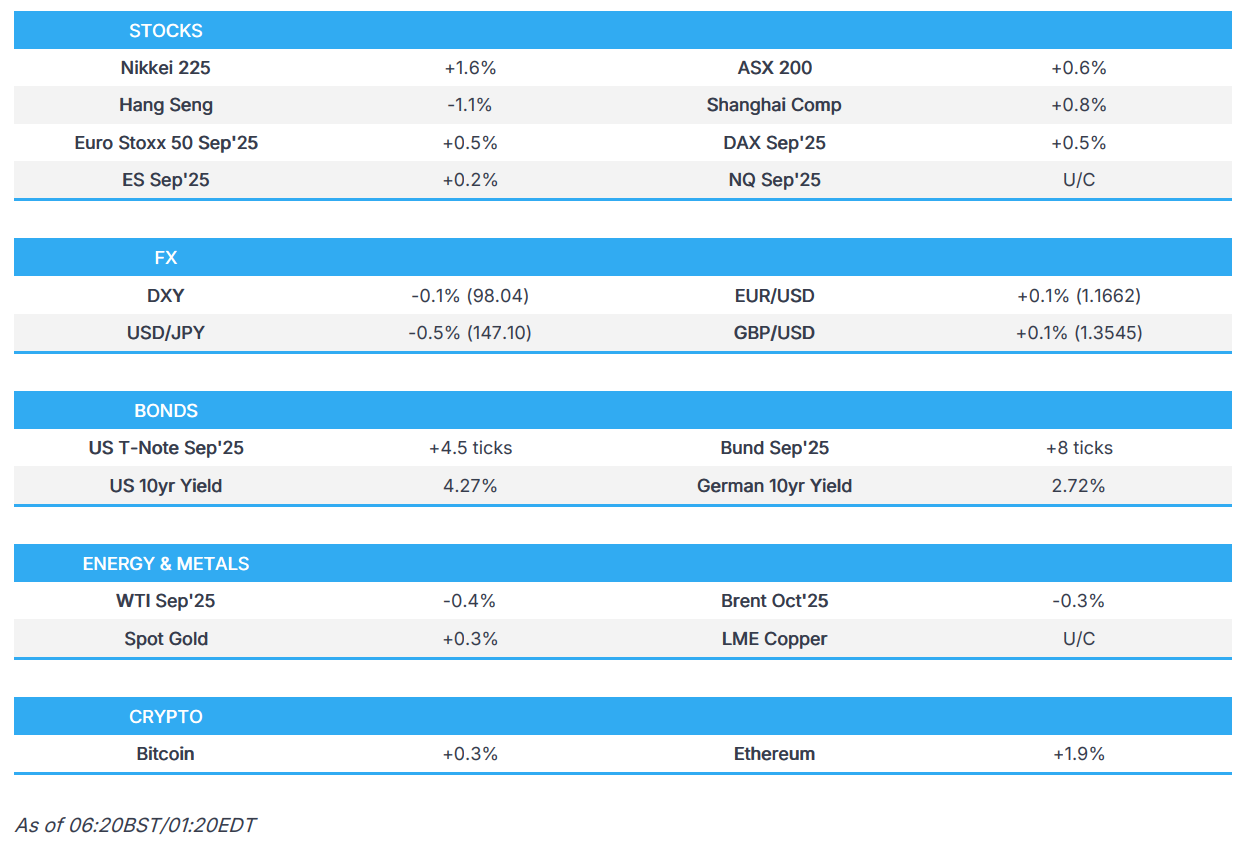

- APAC stocks predominantly traded in the green after the region mostly shrugged off the indecisive performance seen on Wall St.

- US President Trump will participate in a bilateral program with the President of the Russian Federation in Alaska at 11:00 AM (15:00EDT/20:00BST) and will depart Alaska at 17:45 (21:45/02:45BST), according to the White House.

- Potential Fed Chair pick Zervos backed aggressive interest rate cuts, according to CNBC; Fed Chair Powell is to speak 10:00EDT/15:00BST on August 22nd at Jackson Hole, according to the Fed schedule.

- Nikkei 225 rallied above the 43,000 level and JPY was boosted with sentiment lifted following stronger-than-expected Japanese GDP data.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.5% after the cash market closed with gains of 0.9% on Thursday.

- Looking ahead, highlights include German WPI (Jul), US Retail Sales (Jul), US University of Michigan Prelim (Aug), Import/Export Prices (Jul), Industrial Production (Jul), Atlanta Fed GDP, Trump-Putin summit & Joint Press Conference.

US TRADE

EQUITIES

- US stocks were choppy and the major indices ultimately finished flat, although the Russell 2000 underperformed, with index futures initially pressured in the premarket as recent bets of a Fed September rate cut were slightly trimmed on inflationary fears following a hot US PPI report.

- However, stocks then staged a recovery during US trade, albeit in a choppy fashion, as participants turned their attention to the Trump-Putin meeting on Friday.

- SPX +0.01% at 6,467, NDX -0.07% at 23,832, DJI +0.01% at 44,927, RUT -1.35% at 2,297.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said Brazil is one of the worst trade partners and imposes 'tremendous tariffs' on US goods.

- China is warning western companies against stockpiling rare earths or risk even greater shortages, according to FT.

NOTABLE HEADLINES

- Fed Chair Powell is to speak 10:00EDT/15:00BST on August 22nd at Jackson Hole, according to the Fed schedule.

- Fed's Barkin (2027 voter) said business sentiment has picked up in some ways, but not yet on the hiring side, while credit card and other data are providing a sense that July consumer data may be stronger. Furthermore, Barkin said it is still early days for companies adapting supply chains to account for tariffs.

- Potential Fed Chair pick Zervos backed aggressive interest rate cuts, according to CNBC.

- US President Trump said inflation is down to a perfect number and there is hardly any inflation at all, while he added that 401(k)s and the stock market are soaring.

- Trump admin is said to discuss the US taking a stake in Intel (INTC) and is discussing with Intel a plan that would bolster Ohio expansion, according to Bloomberg.

APAC TRADE

EQUITIES

- APAC stocks predominantly traded in the green after the region mostly shrugged off the indecisive performance seen on Wall St in the aftermath of the much hotter-than-expected PPI report, although the upside was capped overnight amid disappointing Chinese activity data and as participants await the Trump-Putin meeting on Friday.

- ASX 200 extended on record highs with the advances led by outperformance in mining, energy and the utilities sectors.

- Nikkei 225 rallied above the 43,000 level with sentiment lifted following stronger-than-expected Japanese GDP data.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark dragged lower by losses in tech as JD.com's shares were pressured following a drop in its earnings, while the mainland ultimately weathered the miss on Chinese activity data which showed retail sales fell short of the most pessimistic of analyst forecasts.

- US equity futures were somewhat mixed overnight following the prior day's indecisive performance but with Dow futures climbing on the back of a double-digit surge in UnitedHealth shares after-hours as 13F filings showed Berkshire Hathaway purchased over 5mln shares in the insurer during Q2.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.5% after the cash market closed with gains of 0.9% on Thursday.

FX

- DXY marginally softened but remained above the 98.00 level after having recently climbed on the back of the hot PPI data, which exceeded all analyst expectations and saw a slight unwinding of Fed rate cut bets although money market pricing is still heavily leaning towards a 25bps rate cut in September, but it is no longer fully priced in.

- EUR/USD regained some composure after it recently gave way to the resurgence in the dollar with the single currency not helped by the mixed data releases from the EU.

- GBP/USD attempted to claw back some losses after retreating from resistance just shy of the 1.3600 level yesterday despite firmer-than-expected UK GDP data.

- USD/JPY pulled back overnight with the Japanese currency supported following stronger-than-expected Japanese GDP.

- Antipodeans languished around this week's lows with price action constrained following disappointing Chinese activity data.

- PBoC set USD/CNY mid-point at 7.1371 vs exp. 7.1852 (Prev. 7.1337).

- Russian government abolished mandatory repatriation and sale of foreign currency proceeds by exporters, according to Interfax.

FIXED INCOME

- 10yr UST futures got some slight reprieve after yesterday's data-triggered bear flattening that saw prices slump beneath the 112.00 level, while participants now await more US data releases, including Retail Sales, Industrial Production, Empire State Manufacturing, University of Michigan, Export & Import prices, as well as the US-Russia summit in Alaska.

- Bund futures attempted to pick themselves up from the prior day's trough after falling back beneath the 130.00 level.

- 10yr JGB futures were lacklustre with demand hampered by stronger-than-expected GDP data and after a weaker-than-previous 10yr inflation-indexed JGB auction.

COMMODITIES

- Crude futures paused after recent advances heading into the Trump-Putin meeting and with the White House tempering expectations for any breakthrough at today's talks.

- Russian Deputy PM Novak supported the energy ministry's idea to extend the ban on gasoline exports through September.

- Spot gold nursed some losses after declining yesterday alongside a firmer dollar and higher yields due to the hot PPI data.

- Copper futures were rangebound as tailwinds from the mostly positive risk tone were offset by disappointing Chinese data.

- Chile's Codelco announced the smelter at the El Teniente copper mine has restarted.

CRYPTO

- Bitcoin gradually rebounded from the prior day's trough and returned to above the USD 119k level.

NOTABLE ASIA-PAC HEADLINES

- China's stats bureau said China's economy maintained a steady trend in July, despite external changes and extreme weather conditions, but added the external environment remains complex and severe. The stats bureau said China is to effectively unlock potential domestic demand and will keep employment, the market and expectations stable, as well as promote interplay between domestic and international economic flows. It also stated that high temperatures and floods in some regions created short-term hits on economic growth in July and the survey-based jobless rate rose in July due to factors including the college graduation season. Furthermore, it said efforts are needed to consolidate the foundation of economic recovery and that China's exports face some pressure due to external uncertainties and some firms face more difficulties.

- Japan is to propose an Africa-Indian Ocean logistics network for trade and resources, according to Nikkei.

DATA RECAP

- Chinese Industrial Output YY (Jul) 5.7% vs. Exp. 5.9% (Prev. 6.8%)

- Chinese Retail Sales YY (Jul) 3.7% vs. Exp. 4.6% (Prev. 4.8%)

- Chinese Urban Investment (YTD)YY (Jul) 1.6% vs. Exp. 2.7% (Prev. 2.8%)

- Chinese Unemployment Rate Urban Area (Jul) 5.2% (Prev. 5.0%)

- Chinese China House Prices MM (Jul) -0.3% (Prev. -0.3%)

- Chinese China House Prices YY (Jul) -2.8% (Prev. -3.2%)

- Japanese GDP QQ (Q2) 0.3% vs. Exp. 0.1% (Rev. 0.1%)

- Japanese GDP QQ Annualised (Q2) 1.0% vs. Exp. 0.4% (Prev. -0.2%, Rev. 0.6%)

GEOPOLITICS

MIDDLE EAST

- Iran said it is working with Russia and China to stop European sanctions, according to journalist Elster.

RUSSIA-UKRAINE

- US President Trump reiterated a second meeting with Putin and Zelensky will be more important and thinks they will make peace, while he added the Putin meeting is not a reward and they will get peace in the near future if it is a good meeting.

- White House said US President Trump will participate in a bilateral program with the President of the Russian Federation in Alaska at 11:00 AM (15:00EDT/20:00BST) and will depart Alaska at 17:45 (21:45/02:45BST).