US Market Open: Modestly firmer risk tone into Tier 1 US data points & Alaska summit

15 Aug 2025, 11:25 by Newsquawk Desk

- Trump and Putin will meet in Alaska at 20:00BST/15:00ET, Trump will then depart just under seven hours later.

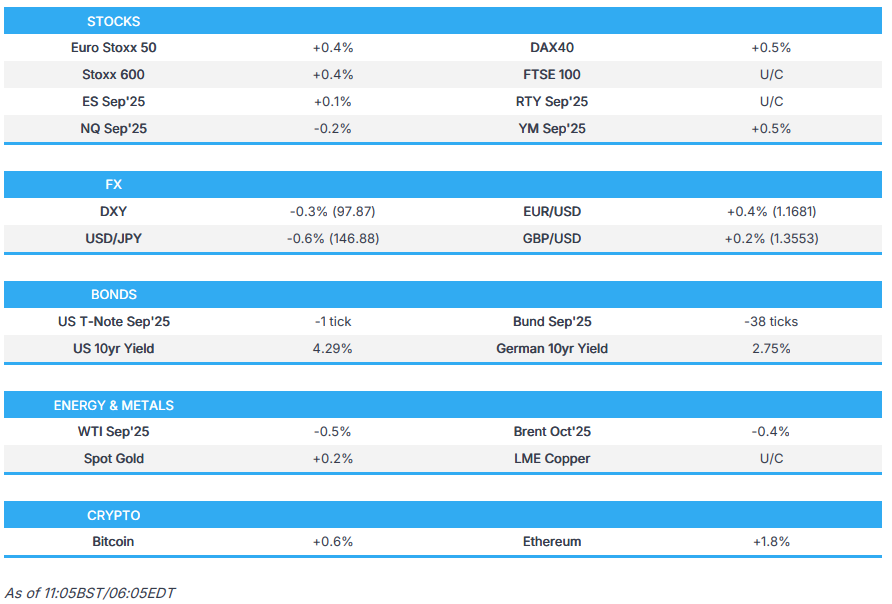

- European bourses began with gains, Euro Stoxx 50 +0.4%; follows a mostly higher APAC handover as soft Chinese data was shrugged off.

- US futures firmer, but have drifted off best in the European morning, ES +0.1%; UNH +12% and INTC +4.5% in the pre-market.

- USD gives back some of its PPI-inspired gains, JPY tops the G10 leaderboard after domestic data.

- A contained start for USTs into Tier 1 data points and the Alaska summit, Bunds dipped on the constructive European risk tone.

- Crude benchmarks lower despite the tone and USD, looking to the Putin-Trump meeting; XAU firmer.

- Looking ahead, highlights include US Retail Sales (Jul), US University of Michigan Prelim (Aug), Import/Export Prices (Jul), Industrial Production (Jul), Atlanta Fed GDP, Fed's Goolsbee, Trump-Putin summit & Press Conference.

ALASKA SUMMIT

- White House said US President Trump will participate in a bilateral program with the President of the Russian Federation in Alaska at 11:00 AM (15:00EDT/20:00BST) and will depart Alaska at 17:45 (21:45/02:45BST).

- Russian Foreign Ministry says Moscow expects Trump to visit Russia after the Alaska summit, according to Al Arabiya; "We have a clear position that we will present at the Alaska summit and hope to continue the dialogue" and "We do not speculate on anything in the future and we have clear arguments and positions that we will present during the Alaska summit".

- Click for the Newsquawk preview on the Alaska summit.

TARIFFS/TRADE

- China is warning western companies against stockpiling rare earths or risk even greater shortages, according to FT.

- China's MOFCOM files WTO lawsuit against Canada, regarding import restrictions on steel and other products.

EUROPEAN TRADE

EQUITIES

- European bourses began with gains, Euro Stoxx 50 +0.4%; with the STOXX 600 and Euro Stoxx 50 both set for a second straight week of advances.

- Follows a mixed Wall St. finish and a mostly higher APAC handover, as China was strong despite domestic data underwhelming for July and the Nikkei 225 was bolstered by Japanese GDP; though, the Hang Seng succumbed after JD.com earnings.

- In Europe, sectors have a positive bias with Basic Resources, Chemicals, and Autos leading; the latter support by the Volkswagen–Xpeng partnership expansion. Utilities hit by Fortum (-2.5%) numbers while Luxury has been tarnished by Chinese retail sales and Pandora (-12%) missing Q2 expectations.

- US futures in the green though have dipped from best across the European morning, ES +0.1%. Supported by a softer dollar, stable yields, and a constructive tone into the Trump–Putin meeting.

- YM +0.5% leads after 13F filings showed Berkshire Hathaway purchased over 5mln shares in UnitedHealth (+12.5%) during Q2. Elsewhere, Intel (+4.5%) gains in the pre-market after a Bloomberg report just before the US close that the Trump administration is in talks to take a stake, in order to support the Ohio chip facility.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is giving back some of its PPI-inspired gains, after the DXY briefly eclipsed its 200 DMA at 98.10 on Thursday. Currently, the index is towards lows in a 97.85-98.21 band, holding above Thursday's 97.63 base. Ahead, we look to Retail Sales (headline and control seen slowing to 0.5% and 0.6% M/M respectively). Additionally, UoM, Industrial Production and Import & Export prices scheduled.

- However, the main focus is on the Alaska summit (preview available), though updates on this are not likely to hit until after-hours as the summit commences at 20:00BST/15:00ET.

- EUR is firmer though macro drivers for the bloc are light once again. Focus for the currency on the mentioned summit and US data, as such the dollar-side of the equation may well dictate price action. Currently, EUR/USD is at highs of 1.1688 within Thursday's 1.1632-1.1715 range.

- USD/JPY under pressure after strong Japanese GDP metrics, with JPY currently topping the G10 leaderboard. Thus far, USD/JPY has delved as low as 146.76 but is still north of the 200DMA @ 146.47 and yesterday's low @ 146.21.

- As is the case with the EUR, newsflow for the UK is very light. Cable is firmer and above the 1.3550 mark but remains within yesterday's 1.3520-95 range.

- AUD/USD has made its way back onto a 0.65 handle with a current session peak @ 0.6514 vs. yesterday's best @ 0.6568. Interim resistance is provided by the 200DMA @ 0.6520. NZD/USD sits towards the bottom end of yesterday's 0.5908-91 range.

- PBoC set USD/CNY mid-point at 7.1371 vs exp. 7.1852 (Prev. 7.1337).

- CBRT Survey: end-2025 CPI 29.69% (prev. 29.66%)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A contained start to the day for USTs, a session that is bookended by Import Prices/Retail Sales and the Alaska summit. Holding around the unchanged mark in narrow 111-24+ to 111-30+ parameters, matching the low from Thursday and holding just ahead of 111-23 and 111-19+ from Wednesday and Tuesday respectively.

- Similarly, Bunds held around 129.56 opening levels for the first part of the session. However, the benchmark has come under gradual but notable pressure throughout the morning. Down to a 129.19 low and softer by c. 30 ticks at most. No clear or specific catalysts behind the move; instead, it appears to be a function of the constructive European risk tone discussed in Equities.

- For Bunds, if the 129.19 base is taken out, we look to 129.06 from Wednesday and below that the figure and then the 128.98 WTD low Tuesday.

- No specific market-moving newsflow for the UK today, with Gilts conforming to the bearish-bias seen in EGBs though to a lesser extent thus far. Potentially a function of the relatively underperformance seen in the FTSE 100; but, magnitudes are minimal and it is probably not worth reading too much into the action at this point in the session.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are softer, despite the weaker USD and risk-on tone, as participants sites are firmly set on the summit between US President Trump and Russian President Putin later today; full primer available. In brief, the meeting has been repeatedly downplayed, Trump on Thursday sad there was a 25% chance the meeting is not a success and placed the emphasis on the importance of a 2nd meeting.

- Notably, Trump said a joint press conference is not something that has been discussed yet, a point that contrasts with the line from the WH Press Secretary and other reports heading into the summit.

- WTI currently resides in a 63.42-64.15/bbl range while Brent sits in a USD 66.36-67.06/bbl range, lower by around USD 0.50/bbl but around USD 0.25/bbl off worst levels.

- Spot gold is firmer, nursing some of the losses seen on Thursday amid USD strength and elevated yields post-PPI. XAU at the upper-end of a USD 3332-3348/oz band, within Thursday's USD 3,329.85-3,374.80/oz range.

- Copper is rangebound but with a modest bullish bias, as the tailwinds from the risk tone have offset the disappointing Chinese data; retail sales (+3.7% Y/Y vs exp. 4.6%), factory output, and investment all slowing; factory and mining production rose 5.7% Y/Y (exp. 5.9%), the weakest since November, reflecting pressure from price war crackdowns and lingering Trump-era tariffs.

- Chile's Codelco announced the smelter at the El Teniente copper mine has restarted.

- NHC says Erin is forecast to become a Hurricane today.

- Qatar lowers October term price for Al-Shaheen oil to USD 2.52/bbl above Dubai quotes, according to Reuters sources.

- Algeria is nearing a deal with Exxon (XOM) and Chevron (CVX) in a shale gas push, according to Bloomberg.

- LME publishes decision notice on market reports to boost liquidity; LME decided to implement, with some modification, all of the proposals set in the consultation on liquidity. Timeline for measures to come into force is February and March 2026.

- Click for a detailed summary

NOTABLE EUROPEAN HEADLINES

- CNB Minutes (Aug): Governor Michl emphasised the need to keep real rates positive, particularly in a situation of elevated general government deficits

NOTABLE US HEADLINES

- Fed Chair Powell is to speak 10:00EDT/15:00BST on August 22nd at Jackson Hole, according to the Fed schedule.

GEOPOLITICS

- US President Trump reiterated a second meeting with Putin and Zelensky will be more important and thinks they will make peace, while he added the Putin meeting is not a reward and they will get peace in the near future if it is a good meeting.

CRYPTO

- Bitcoin is in the green, at the upper-end of parameters for the day but currently just shy of the USD 120k mark.

APAC TRADE

- APAC stocks predominantly traded in the green after the region mostly shrugged off the indecisive performance seen on Wall St in the aftermath of the much hotter-than-expected PPI report, although the upside was capped overnight amid disappointing Chinese activity data and as participants await the Trump-Putin meeting on Friday.

- ASX 200 extended on record highs with the advances led by outperformance in mining, energy and the utilities sectors.

- Nikkei 225 rallied above the 43,000 level with sentiment lifted following stronger-than-expected Japanese GDP data.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark dragged lower by losses in tech as JD.com's shares were pressured following a drop in its earnings, while the mainland ultimately weathered the miss on Chinese activity data which showed retail sales fell short of the most pessimistic of analyst forecasts.

NOTABLE ASIA-PAC HEADLINES

- China's stats bureau said China's economy maintained a steady trend in July, despite external changes and extreme weather conditions, but added the external environment remains complex and severe. The stats bureau said China is to effectively unlock potential domestic demand and will keep employment, the market and expectations stable, as well as promote interplay between domestic and international economic flows. It also stated that high temperatures and floods in some regions created short-term hits on economic growth in July and the survey-based jobless rate rose in July due to factors including the college graduation season. Furthermore, it said efforts are needed to consolidate the foundation of economic recovery and that China's exports face some pressure due to external uncertainties and some firms face more difficulties.

DATA RECAP

- Chinese Industrial Output YY (Jul) 5.7% vs. Exp. 5.9% (Prev. 6.8%)

- Chinese Retail Sales YY (Jul) 3.7% vs. Exp. 4.6% (Prev. 4.8%)

- Chinese Urban Investment (YTD)YY (Jul) 1.6% vs. Exp. 2.7% (Prev. 2.8%)

- Chinese Unemployment Rate Urban Area (Jul) 5.2% (Prev. 5.0%)

- Chinese China House Prices MM (Jul) -0.3% (Prev. -0.3%); YY (Jul) -2.8% (Prev. -3.2%)

- Japanese GDP QQ (Q2) 0.3% vs. Exp. 0.1% (Rev. 0.1%)

- Japanese GDP QQ Annualised (Q2) 1.0% vs. Exp. 0.4% (Prev. -0.2%, Rev. 0.6%)