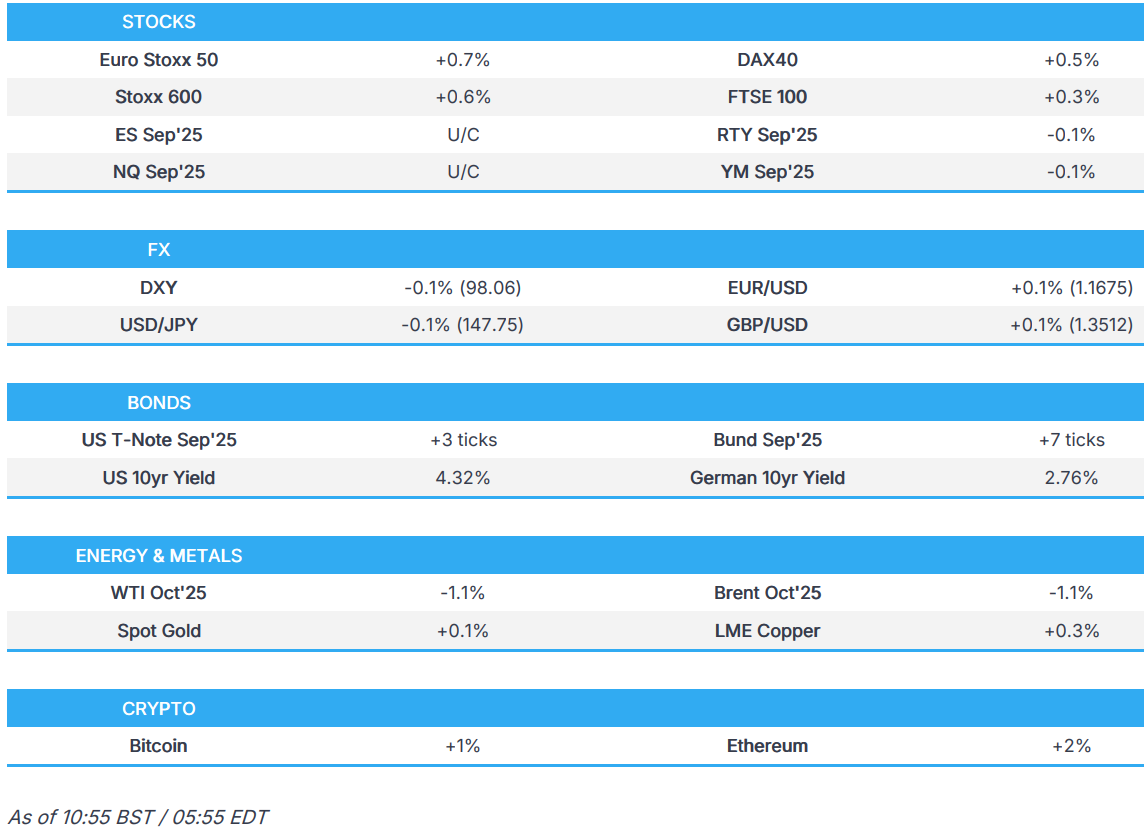

US Market Open: Cautious optimism following the Zelensky/Trump meeting into Fed speak

19 Aug 2025, 11:19 by Newsquawk Desk

- US President Trump posted that he had a very good meeting with Ukrainian President Zelensky and European leaders, which ended in a further meeting in the Oval Office and during the meeting, they discussed security guarantees for Ukraine, which would be provided by the various European countries with coordination with the US. In the aftermath, crude trades lower.

- Russia's Kremlin said US President Trump and Russian President Putin held a phone call in which they discussed the idea of exploring the possibility of raising the level of Russian and Ukrainian representatives in the negotiations.

- S&P affirmed the US at AA+; Outlook Stable, S&P added that the revenue from President Trump's tariffs will offset the fiscal hit from his recent tax-cut and spending bill.

- European bourses opened cautiously optimistic in the aftermath of the Trump/Zelensky/EU leaders meeting, but have gradually climbed higher; US equity futures trade tentatively.

- Tentative trade across FX while CAD eyes CPI. Fixed Income also trade tentatively, but have been moving higher in recent trade.

- Looking ahead, US Building Permits & Housing Starts, Canadian CPI, Atlanta Fed GDPNow, Comments from Fed's Bowman, Earnings from Home Depot.

TARIFFS/TRADE

- Brazil's government submitted its response to the US Section 301 investigation and said it urges the USTR to reconsider the initiation of the Section 301 investigation and to engage in constructive dialogue. It was separately reported that Brazil's Finance Minister Haddad said Brazil is deadlocked with the US over 50% tariffs and reduction in high levies depends on Washington being open to talks, according to FT.

- India exempted import duty on cotton between August 19th to September 30th, according to a government order.

- Japan-India framework to focus on chips, mineral resources, and AI, according to reports citing Nikkei

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.4%) opened modestly firmer across the board, with cautious optimism stemming from the recent US President Trump/Ukrainian President Zelensky/EU Leaders meeting. On that, Trump described it as a very good meeting, while he also called Russian President Putin to begin arrangements for a Putin-Zelensky meeting, which would be followed by a trilateral meeting with Trump. Reportedly, security agreements were discussed; on territorial developments, Zelensky suggested it would be a discussion between Ukraine and Russia. As the morning progressed, stocks have gradually climbed higher and currently sit at highs.

- European sectors hold a positive bias, but the breadth of the market is fairly narrow. Consumer Products takes the top spot, joined closely by Basic Resources and Retail; nothing really company-specific is driving the upside in these sectors, but largely benefiting from the slightly positive risk tone.

- US equity futures (ES U/C, NQ U/C, RTY -0.1%) are modestly lower/flat across the board, with sentiment a little downbeat in comparison to the upside seen across Europe.

- NVIDIA (NVDA) is reportedly working on a new AI chip for China which outperforms the H20, via Reuters citing sources; likely deliver half of the computing power as the B300. Samples potentially to be delivered for testing in September.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is relatively rangebound this morning with a slight negative bias and price action contained to either side of the 98.00 mark. Currently in a narrow 97.99-98.32 parameter vs Monday's 97.77-98.19 range. The theme over the last couple of days has been geopolitics, with deliberations over the Russia-Ukraine war in Washington concluding for now. Overall, there has been no breakthrough in Monday's discussions, although talks may advance with a possible Zelensky–Putin meeting in two weeks, their first since the war began. Despite the mild optimism, betting markets remain pessimistic, with Polymarket pointing to a 38% chance of a Russia-Ukraine ceasefire this year.

- EUR/USD is holding a mild upward bias after finding support at its 50 DMA (1.1641) following Monday's slide under 1.1700, with very little newsflow from the bloc aside from the comments from various European leaders following the multilateral meeting on Ukraine at the White House. EUR/USD resides in a current 1.1640-1.1685 range with the 50 DMA at 1.1641.

- Modest gains in the JPY, albeit in tandem with USD weakness, with little in terms of fresh catalysts from Japan. USD/JPY trades in either side of 148.00 in a 147.53-148.11 parameter, vs Monday's 147.06-147.99 range, with the 50 DMA at 146.60 and the 200 DMA at 149.22.

- GBP continues to struggle for direction as newsflow from the UK remains very quiet, although there were reports that UK Chancellor Reeves is considering replacing stamp duty with a new property tax. GBP/USD trades in a 1.3486-1.3529 range (vs Monday's 1.3501-1.3568), with the 50 DMA at 1.3501 today.

- Antipodeans are essentially flat vs the Dollar today, continuing the tentative risk tone seen in overnight trade.

- PBoC set USD/CNY mid-point at 7.1359 vs exp. 7.1846 (Prev. 7.1322)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A contained start to the day for USTs after the pressure that began towards the end of the European day and intensified into the mid-US morning. The pullback occurred as the White House meetings got underway and, ultimately, as the tone from the meeting was a positive one with progress made towards a trilateral summit and then security guarantees. On the guarantees, they are seemingly set to be formed of a coalition of the willing, which will be coordinated by the US. Currently, USTs are at a 111-15 trough, near enough unchanged on the session. If USTs conform to the bearish bias in EGBs, then Monday’s 111-13+ base is the first focal point before a bit of a gap until 110-23+ from the first week of August.

- As mentioned above, EGBs were slightly softer at this moment in time. Lower by as much as 10 ticks at worst. Pressure is seemingly a function of two bearish supply-side factors: 1) upcoming issuance, with Germany selling EUR 4.5bln of 2030 debt; 2) the funding security guarantees for Ukraine. Currently, the low point is 128.73. If we return to and move below this, Monday’s 128.70 base and then last week’s 128.64 trough comes into view. The German 2030 auction was well received, drawing a better-than-prior b/c - which helped to flip Bunds into positive territory.

- Gilts trade similar to Bunds but modestly underperforming. Thus far, to a 90.43 base with downside of just over 15 ticks at most. Taking out Monday’s 90.52 base and bringing levels from May into view. Given this, the UK 10yr yield is at a fresh WTD peak of 4.76%, approaching 4.69% from end-May.

- UK sells GBP 1.6bln 1.125% 2035 I/L Gilt: b/c 3.1x (prev. 3.35x) & real yield 1.728% (prev. 1.588%).

- Click for a detailed summary

COMMODITIES

- Crude oil trades softer following the Washington confabs between the US, Ukraine, EU, and NATO. Overall, there has been no breakthrough in Monday's discussions, although talks may advance with a possible Zelensky–Putin meeting in two weeks, their first since the war began. The main obstacle remains Russia’s demand for full control of Donetsk and Luhansk, which Ukraine rejects. WTI currently resides in a 62.05-62.68/bbl range while Brent sits in a USD 66.58-66.02/bbl range.

- Mostly flat trade across precious metals amid quiet markets and with little fallout seen in the yellow metal from the deliberations on Russia-Ukraine, as traders await a clearer hint of what will result from the talks. Price action this morning sees the precious metals complex eking mild gains, with spot gold trading under its 50 DMA (3,349.61/oz) in a USD 3,326.28-3,341.88/oz range.

- Flat/mixed trade across base metals amid the broader tentative mood across the markets. 3M LME copper prices reside in a USD 9,739.40-9,782.00/t range.

- Equinor (EQNR NO) preparations for start up of Norway's Hammerfest LNG terminal after outage are underway.

- Ukraine's Energy Ministry says Russian attacks damaged gas transport infrastructure.

- Germany sells EUR 3.424bln vs exp. EUR 4.5bln 2.20% 2030 Bobl: b/c 1.90x (prev. 1.50x), average yield 2.32% (prev. 2.28%) & retention 23.19% (prev. 24.24%).

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Current Account SA, EUR (Jun) 35.8B (Prev. 32.3B); Current Account NSA,EUR (Jun) 38.9B (Prev. 1.02B)

NOTABLE EUROPEAN HEADLINES

- UK's ONS says Friday's scheduled retail sales data release has been delayed until September 5th

NOTABLE US HEADLINES

- S&P affirmed the US at AA+; Outlook Stable, while it stated the US outlook indicates fiscal deficit outcomes will not meaningfully improve, but does not project persistent deterioration over the next several years. S&P added that the revenue from President Trump's tariffs will offset the fiscal hit from his recent tax-cut and spending bill.

GEOPOLITICS

RUSSIA-UKRAINE

Morning update:

- US and Europe to work immediately on Ukraine security guarantees, via Bloomberg.

- Poland PM Tusk will take part in meeting of the Coalition of the Willing at 11:00BST/06:00EDT, according to a spokesperson.

- Ukraine Foreign Minister says future trilateral leaders meeting can bring a breakthrough on the path to peace.

Overnight

- US President Trump posted that he had a very good meeting with Ukrainian President Zelensky and European leaders, which ended in a further meeting in the Oval Office and during the meeting, they discussed security guarantees for Ukraine, which would be provided by the various European countries with coordination with the US. Trump added everyone is very happy about the possibility of peace for Russia and Ukraine, and at the conclusion of the meetings, he called Russian President Putin and began the arrangements for a meeting, at a location to be determined, between President Putin and President Zelensky. Furthermore, Trump said after that meeting takes place, they will have a trilateral between Trump, Putin and Zelensky, as well as noted that this was a very good, early step for a war that has been going on for almost four years and that VP Vance, Secretary of State Rubio, and Special Envoy Witkoff are coordinating with Russia and Ukraine.

- Russia's Kremlin said US President Trump and Russian President Putin held a phone call which lasted 40 minutes and they discussed the idea of exploring the possibility of raising the level of Russian and Ukrainian representatives in the negotiations, while Putin warmly thanked Trump for the hospitality and well-organized meeting in Alaska, as well as for progress achieved at the summit. Furthermore, Putin and Trump spoke in favour of the continuation of direct talks between the Russian and Ukrainian delegations, while they agreed to continue close contact with each other on the Ukrainian crisis and other issues.

- Ukrainian President Zelensky said we need not a pause in the war, but real peace and territorial issues will be decided between Russia and Ukraine. Zelensky said he discussed security guarantees with Trump and European leaders, and received an important signal from the US on being part of security guarantees and help in coordinating it. Furthermore, he said the US offers to have a trilateral meeting as soon as possible and that Ukraine is ready for any format to meet with Putin.

- Ukraine reportedly offered a USD 100bln weapons deal to US President Trump in an effort to win security guarantees, according to the Financial Times citing documents laying out Kyiv's proposal to Trump at the White House meeting.

- US Secretary of State Rubio told Fox News that they will work with European allies and non-European countries to build security guarantees for Ukraine. Rubio said he was in the room when Trump and Putin spoke, while he added that Trump suggested to Putin that he meet with Zelensky.

- NATO Secretary General Rutte said it was a very successful day in Washington where security guarantees were discussed and more details on security guarantees will be discussed in the coming days, while he added it is a breakthrough that the US will get involved and they are discussing some Article 5-type arrangement.

- European Commission President Von der Leyen said after the White House meeting that they are here as allies and friends for peace in Ukraine and in Europe, while she added this is an important moment as they continue to work on strong security guarantees for Ukraine.

- German Chancellor Merz that he feels these are decisive days for Ukraine and is not sure if Russian President Putin will have the courage to come to a summit with Zelensky present, while he added that expectations were not only met but were exceeded from this meeting. Merz also stated that US President Trump spoke with Russian President Putin and agreed that a Putin-Zelenskiy meeting will happen within two weeks, while the location is yet undecided, and that will be followed by a three-way meeting involving Trump.

- Finland's President Stubb said they agreed on security guarantees and steps forward, as well as noted that talks were constructive and the Coalition of the Willing has already worked on security guarantees which they will build upon. Stubb also stated there is nothing concrete about US participation in security guarantees and that US President will inform them, with details of security guarantees to be ironed out in the next week or so.

- Debris from a destroyed Ukrainian drone sparked a fire at an oil refinery and hospital in Russia's Volgograd, according to the regional administration.

OTHER

- North Korea leader Kim said joint US-South Korea military drills show willingness for war provocation, while he also stated that the security environment requires North Korea to expand its nuclear armament rapidly.

- "Israeli media: The Chief of Staff will present today to the Minister of Defense the plan to occupy Gaza City", according to Al Arabiya.

CRYPTO

- Bitcoin is a little firmer and trades around USD 115k whilst Ethereum trades just above USD 4.2k.

APAC TRADE

- APAC stocks traded mixed following the ultimately flat performance stateside amid a lack of fresh macro catalysts, as focus centred on geopolitical updates and amid cautiousness ahead of Powell's speech at Jackson Hole on Friday.

- ASX 200 pulled back from record highs with heavy losses in healthcare as CSL shares fell by a double-digit percentage after the announcement to spin-off its flu vaccine business and cut 15% of its workforce, while tech was at the other end of the spectrum and miners also gained post-BHP earnings despite the mining giant reporting a 26% drop in FY underlying profit.

- Nikkei 225 swung between gains and losses after failing to sustain the initial upward momentum that had lifted the index to a fresh record high.

- Hang Seng and Shanghai Comp kept afloat following a firm liquidity effort by the PBoC which injected CNY 580bln through its 7-day reverse repo operation, while there were also comments on Monday by Chinese Premier Li who said the nation should consolidate and expand the positive trend in the economy, as well as stabilise market expectations and should continue to stimulate consumption potential.

NOTABLE ASIA-PAC HEADLINES

- China’s Foreign Minister Wang Yi held talks with his counterpart in India and said their countries should establish a correct strategic understanding, as well as regard each other as partners and opportunities, not as rivals or threats, while he added that China is ready to uphold the principle of cordiality and mutual benefit.

- China Jan-July Fiscal Revenue +0.1% Y/Y; Expenditures +3.4% Y/Y.

- XPeng (9868 HK) Q2 (CNY) Adj. EPS -0.20 (exp. -0.36, prev. -0.19 Y/Y), Revenue 18.27bln (exp. 18.11bln); Q3 deliveries: Vehicles to be between 113-118k.

- Russian Defence Ministry says they have conducted strikes on oil refinery supplying fuel to Ukrainian armed forces, according to Ifax.