Europe Market Open: Kiwi weakened sharply following a dovish RBNZ rate cut; European equity futures indicate a negative cash open; UK CPI ahead

20 Aug 2025, 06:31 by Newsquawk Desk

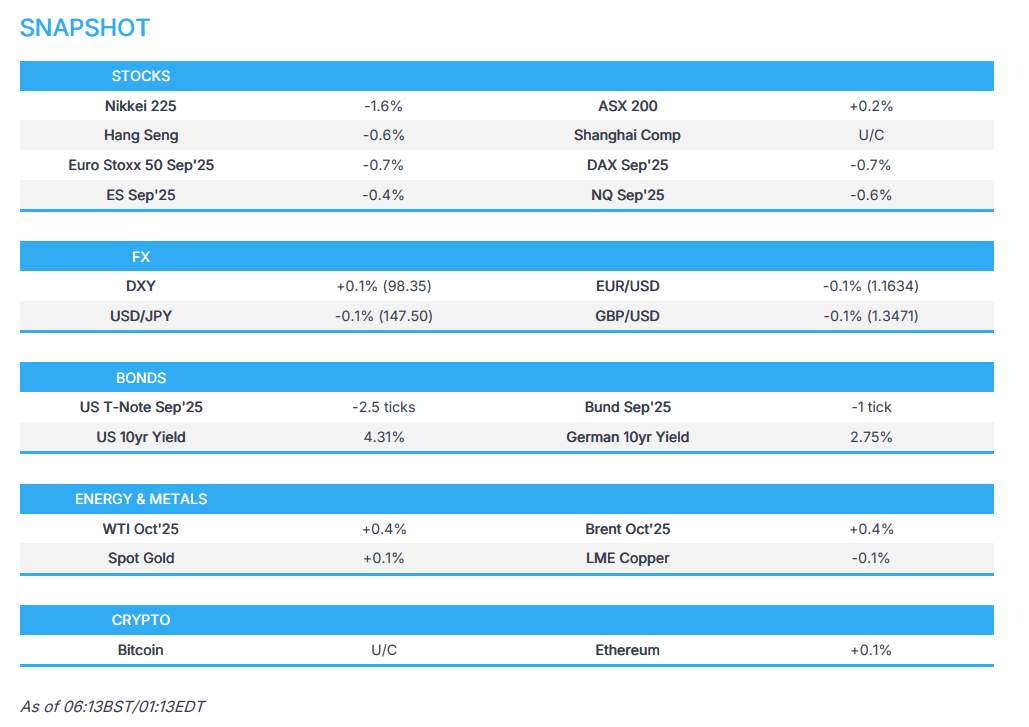

- APAC stocks traded mixed after a lacklustre performance stateside, where mega-cap tech led the declines.

- RBNZ lowered the OCR by 25bps as expected, cut its OCR forecasts across the projection horizon and voted on the options of either a 25bps or 50bps reduction.

- European equity futures indicate a negative cash market open with Euro Stoxx 50 futures down 0.7% after the cash market closed with gains of 0.9% on Tuesday.

- DXY is marginally higher for a third session in a row, NZD lags post-RBNZ, GBP eyes inflation data.

- White House is eyeing Budapest for peace talks with Zelensky and Putin, according to Politico.

- Looking ahead, highlights include UK CPI, EZ HICP (Final), Riksbank Policy Announcement & FOMC Minutes, Speakers including ECB’s Lagarde, Fed’s Bostic & Waller, Supply from Germany & US, Earnings from Target.

SNAPSHOT

US TRADE

EQUITIES

- US stocks were mixed and the major indices finished mostly lower with the declines led by the mega-cap tech stocks which resulted in the underperformance of the Nasdaq, with the FT citing the tech weakness to a MIT paper questioning returns from new technology and noted that “95 per cent of organisations are getting zero return” from their investments in gen AI", while Meta (META) was also reported to downsize its AI division and some executives are expected to leave. As such, Tech and Communication were the laggards weighing on the market, although the DJIA closed flat and the Equal Weight S&P 500 gained amid resilience in defensives such as Real Estate, Consumer Staples and Utilities.

- SPX -0.57% at 6,412, NDX -1.39% at 23,385, DJI +0.02% at 44,922, RUT -0.77% at 2,277.

- Click here for a detailed summary.

TARIFFS/TRADE

- US Treasury Secretary Bessent said the US has had very good talks with China and that China is the biggest revenue line in terms of tariff income, while he added that the status quo on China is working very well.

- Mexico will propose reinstating a North American Steel Committee to improve trade ties with the US, according to Bloomberg.

NOTABLE HEADLINES

- US President Trump posted "Could somebody please inform Jerome “Too Late” Powell that he is hurting the Housing Industry, very badly? People can’t get a Mortgage because of him. There is no Inflation, and every sign is pointing to a major Rate Cut. “Too Late” is a disaster!"

- Fed's Bowman (Vice-Chair of Supervision) said de minimis crypto holdings would allow Fed staff to better understand crypto products and Fed staff should be allowed to own small amounts of crypto products, while she added that limits on Fed staff investment activities may hinder recruiting and retaining expert examiners.

- US Treasury Secretary Bessent is reportedly betting the crypto industry will become a crucial buyer of Treasuries in the coming years as Washington seeks to shore up demand for a deluge of new US government debt, according to FT.

- US is looking into taking equity stakes in chip makers in exchange for CHIPS Act funding, similar to the Intel (INTC) plan, according to two sources cited by Reuters.

APAC TRADE

EQUITIES

- APAC stocks traded mixed after a lacklustre performance stateside, where mega-cap tech led the declines amid AI-related concerns, while the region digested earnings and central bank updates including the RBNZ's dovish rate cut.

- ASX 200 was led higher by outperformance in the top-weighted financials sector and with strength also seen in defensives, while participants also reflected on a slew of earnings updates.

- Nikkei 225 retreated beneath the 43,000 level amid continued profit taking from recent record highs and after mixed data in which Machinery Tools topped forecasts but trade data mostly disappointed and showed Japanese Exports suffered the largest decline in four years.

- Hang Seng and Shanghai Comp were varied as participants digested earnings releases including from Xiaomi and XPeng, while there was a lack of surprises from China's benchmark Loan Prime Rates which were maintained at the current levels, although the PBoC continued with its firm liquidity efforts via 7-day reverse repo operations.

- US equity futures (ES -0.3%, NQ -0.5%) remained subdued following recent tech selling stateside and amid tentativeness ahead of key events.

- European equity futures indicate a negative cash market open with Euro Stoxx 50 futures down 0.7% after the cash market closed with gains of 0.9% on Tuesday.

FX

- DXY is a touch firmer following the prior day's intraday recovery, with upside capped ahead of the FOMC Minutes due later and with Fed Chair Powell set to speak at the Jackson Hole on Friday, while there was renewed criticism by US President Trump on Powell who he claimed is hurting the housing industry and stated that every sign is pointing to a major rate cut.

- EUR/USD trickled lower after yesterday's early upward momentum was cut short by resistance near the 1.1700 level.

- GBP/USD remained subdued after its recent failure to sustain the 1.3500 status, while attention turns to UK inflation data.

- USD/JPY traded indecisively around the 147.50 level amid the mixed data releases and risk-off sentiment in Japan.

- Antipodeans retreated with NZD heavily pressured following a dovish rate cut by the RBNZ which lowered the OCR by 25bps to 3.00%, as widely expected, while it also cut its OCR forecasts across the projection horizon and revealed it had voted on the options of either a 25bps or 50bps cut at the meeting.

- PBoC set USD/CNY mid-point at 7.1384 vs exp. 7.1897 (Prev. 7.1359)

FIXED INCOME

- 10yr UST futures slightly pulled back after advancing on a haven bid during US trade, while participants look ahead to a 20yr auction stateside and FOMC Minutes due later today, as well as the Jackson Hole Symposium later in the week.

- Bund futures were little changed after reclaiming the 129.00 status, and as Bund supply and German PPI data loom.

- 10yr JGB futures struggled for direction after mixed data releases and despite the downbeat mood in Japan

COMMODITIES

- Crude futures attempted to nurse some of the prior day's losses but with the recovery limited following mixed private sector inventory data.

- US Private Inventory Data (bbls): Crude -2.4mln (exp. -1.8mln), Distillate +0.5mln (exp. +0.9mln), Gasoline +1.0mln (exp. -0.9mln), Cushing -0.1mln.

- Iraq signed an agreement with Chevron (CVX) for a project that consists of four exploration blocks and the development of other oil fields.

- Spot gold languished around the prior day's trough as participants await Fed policy clues from the incoming FOMC Minutes and Fed Chair Powell's speech at Jackson Hole.

- Copper futures lacked demand following the recent selling pressure and amid the mixed overnight risk appetite.

- US President Trump said it is 'so sad' that opponents are trying to delay the Resolution copper project in Arizona, while he added 'our country needs copper, and now' and an appeal of the Arizona copper mine ruling will take place.

CRYPTO

- Bitcoin mildly rebounded overnight and returned to above the USD 113k level.

NOTABLE ASIA-PAC HEADLINES

- Chinese Loan Prime Rate 1Y (Aug) 3.00% vs. Exp. 3.00% (Prev. 3.00%)

- Chinese Loan Prime Rate 5Y (Aug) 3.50% vs. Exp. 3.50% (Prev. 3.50%)

- Chinese Foreign Minister Wang Yi said regarding a meeting with Indian PM Modi that after comprehensive and in-depth communication, China and India reached an agreement to restart dialogue mechanisms in various fields.

- India’s Foreign Ministry said India and China agreed to resume direct flight connectivity between the Chinese mainland and India at the earliest, while they agreed to the re-opening of border trade through the three designated trading points. Furthermore, they agreed to facilitate trade and investment flows between the two countries through concrete measures.

- RBNZ cut the OCR by 25bps to 3.00%, as expected, while it lowered OCR projections and stated if medium-term inflation pressures continue to ease as expected, there is scope to lower the OCR further. RBNZ stated that with spare capacity in the economy and declining domestic inflation pressure, headline inflation is expected to return to around the 2% target midpoint by mid-2026, and further data on the speed of New Zealand’s economic recovery will influence the future path of the OCR. RBNZ lowered the Official Cash Rate projection for December 2025 to 2.71% (prev. 2.92%) and to 2.59% in September 2026 (prev. 2.90%). The RBNZ Minutes revealed that the rate decision was made by a majority of 4 votes to 2 and the committee discussed three policy options: keeping the OCR on hold at 3.25%, cutting the OCR by 25bps to 3% or cutting by 50bps to 2.75%, but voted on the options of either reducing the OCR by 25bps or reducing the OCR by 50bps, while the case for lowering the OCR by 25bps was based on the upside and downside risks around the central projection being broadly balanced. Furthermore, RBNZ Governor Hawkesby said during the Q&A that the next two meetings are live but no decisions have been made, as well as stated that the OCR projection troughs at 2.5% and is consistent with further cuts, while whether they go faster or slower on cuts is up to the data.

DATA RECAP

- Japanese Machinery Orders MM (Jun) 3.0% vs. Exp. -1.0% (Prev. -0.6%)

- Japanese Machinery Orders YY (Jun) 7.6% vs. Exp. 5.0% (Prev. 4.4%)

- Japanese Trade Balance Total Yen (Jul) -117.5B vs. Exp. 196.2B (Prev. 153.1B, Rev. 152.1B)

- Japanese Exports YY (Jul) -2.6% vs. Exp. -2.1% (Prev. -0.5%)

- Japanese Imports YY (Jul) -7.5% vs. Exp. -10.4% (Prev. 0.2%, Rev. 0.3%)

GEOPOLITICS

MIDDLE EAST

- Syrian Foreign Affairs Minister Al-Shaibani discussed de-escalation talks in Paris with the Israeli delegation and discussed "Strengthening stability in southern Syria", according to Al-Hadath citing SANA.

RUSSIA-UKRAINE

- US President Trump said he wants to see what goes on when Zelensky and Putin meet, while he added they are in the process of setting the meeting up. Trump also said he gets along with Russian President Putin which is a good thing and commented that two nuclear powers getting along is a good thing.

- White House Press Secretary said Russian President Putin has agreed to begin the next stage of the peace process, while US Secretary of State Rubio, VP Vance and US Envoy Witkoff will coordinate with Ukraine. It was separately reported that the White House is eyeing Budapest, Hungary for peace talks with Ukrainian President Zelensky and Russian President Putin, according to Politico.

- White House official said US President Trump and Hungarian PM Orban discussed on Monday Ukraine's EU accession talks and Budapest as a potential venue for the Zelensky-Putin meeting.

- US Special Envoy Witkoff said progress was made on how to achieve a peace deal, according to a Fox News Interview.

- Senior officials from the US, Ukraine and several European countries are expected to work in the coming days on a detailed proposal for security guarantees for Ukraine, likely involving US air power, according to Axios citing sources.

- EU Foreign Policy Chief Kallas said the next sanctions package against Moscow should be ready by next month.

OTHER

- North Korean leader Kim's sister said South Korea cannot be a diplomatic counterpart to North Korea and South Korean President Lee cannot turn the tide of history, while she also stated that relations between the two Koreas will never return to the way South Korea wants, according to Yonhap and KCNA.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Reeves is drawing up plans to hit owners of high-value properties with capital gains tax when they sell their homes as she seeks to fill a GBP 40bln hole in the public finances, according to The Times.