Europe Market Open: European equity futures are indicative of a firmer open into Global Flash PMIs, DXY is flat

21 Aug 2025, 07:20 by Newsquawk Desk

- APAC stocks traded mixed, albeit with a mildly positive bias as the region attempted to shrug off the lacklustre lead from Wall St, where sentiment was dampened amid continued tech weakness and hawkish-leaning FOMC Minutes.

- FOMC Minutes from the July meeting noted a majority of participants judged the upside risk to inflation was the greater risk compared with the labour market, although the meeting was conducted prior to the release of the latest NFP report with hefty downward revisions.

- Fed Governor Cook said she has no intention of being bullied to step down from her position because of some questions raised in a tweet by FHFA Director Pulte.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed with losses of 0.2% on Wednesday.

- Looking ahead, highlights include Global Flash PMIs, UK PSNB, US Weekly/Continued Jobless Claims, Philly Fed Index, EZ Consumer Confidence, Fed Jackson Hole Symposium (21st-23rd), Speech from Fed’s Bostic, Supply from France & US, Earnings from Walmart.

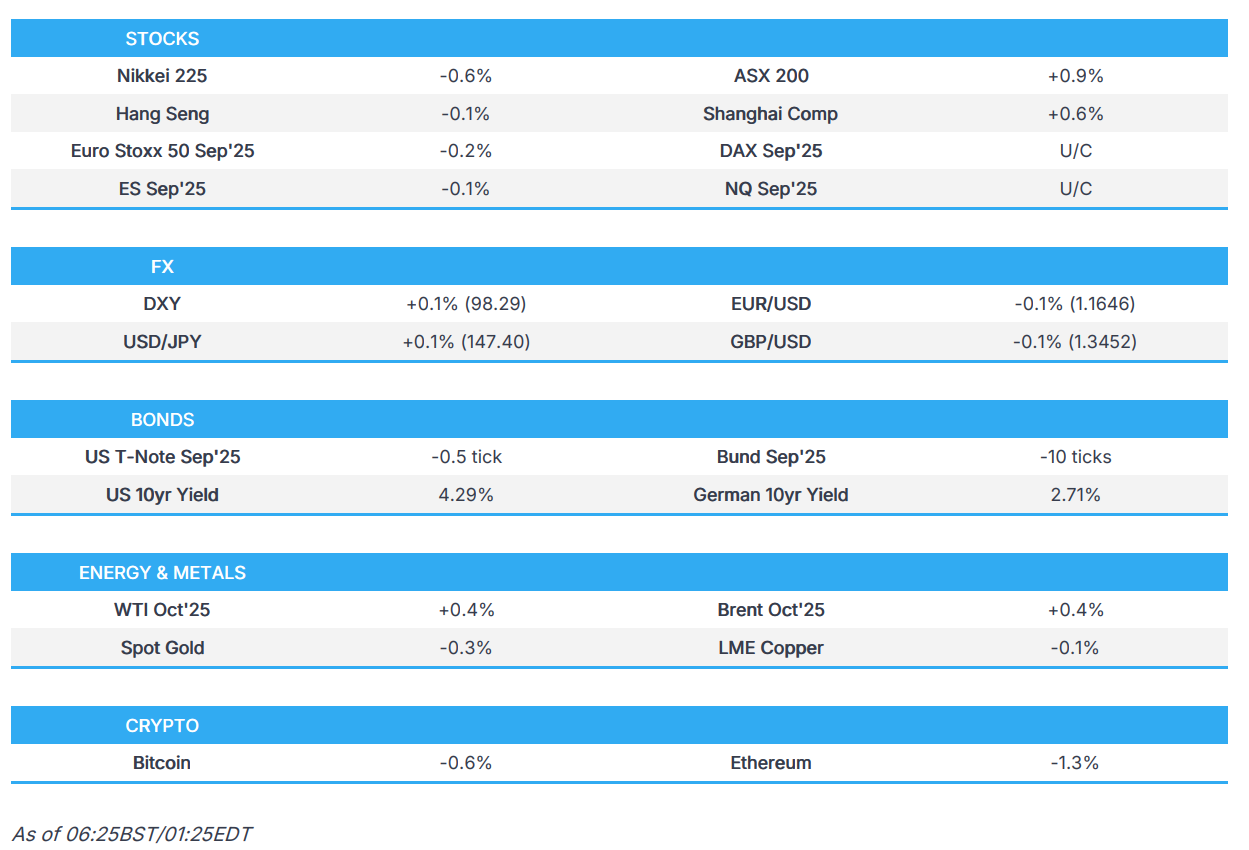

SNAPSHOT

Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks saw two-way price action on Wednesday but ultimately closed mixed with a downward bias as recent big-tech weakness continued to weigh on indices, while the equal-weight S&P was marginally lower. Elsewhere, T-notes were firmer for a lot of the session but ultimately settled little changed, with initial upside led by the front-end after US President Trump called on Fed Governor Cook to resign and reports suggested he is considering firing her amid alleged mortgage fraud.

- However, the upside then faded into the FOMC Minutes, which leaned hawkish, with the majority of participants more concerned about risks to inflation over the labour market, although the minutes do not incorporate the latest NFP data with chunky two-month revisions.

- SPX -0.24% at 6,396, NDX -0.58% at 23,250, DJI +0.04% at 44,938, RUT -0.32% at 2,269.

- Click here for a detailed summary.

FOMC MINUTES

- FOMC Minutes stated that almost all participants viewed it as appropriate to maintain the benchmark interest rate in the 4.25-4.5% range, as well as noted that it would take time to have more clarity on the magnitude and persistence of higher tariffs' effects on inflation. Regarding the balance of risks, participants assessed that the downside risk to employment had meaningfully increased. However, a majority judged that upside risks to inflation were the greater risk when compared to the labour market, while several viewed the two risks as roughly balanced, and a couple considered the downside risk to employment the more salient risk. Several participants, drawing on information provided by business contacts or business surveys, expected that many companies would increasingly have to pass through tariff costs to end-customers over time. However, a few participants reported that business contacts and survey respondents described a mix of strategies as being undertaken to avoid fully passing on tariff costs to customers. Furthermore, several participants commented that the current target range for the federal funds rate may not be far above its neutral level; among the considerations cited in support of this assessment was the likelihood that broader financial conditions were either neutral or supportive of stronger economic activity.

TARIFFS/TRADE

- China’s Commerce Minister talked with Kazakhstan’s Trade Minister and said China is ready to work with Kazakhstan to promote the upgrading of bilateral trade, while China is ready to strengthen cooperation in emerging fields and accelerate the cultivation of new trade formats.

NOTABLE HEADLINES

- Fed Governor Cook said she learned from the media that FHFA Director Pulte posted he was making a criminal referral based on a mortgage application from four years ago, before she joined the Fed, while she has no intention of being bullied to step down from her position because of some questions raised in a tweet. Furthermore, she intends to take any questions about her financial history seriously as a member of the Federal Reserve and is gathering accurate information to answer any legitimate questions and provide the facts.

- WSJ's Timiraos wrote "The Fed minutes suggest broad support for last month's decision to hold rates steady. They imply that had it not been for the crummy payroll revisions two days after the meeting, a rate cut in September could very much be in doubt."

- Texas House approved the Trump-backed congressional map that would give Republicans more seats on Capitol Hill, igniting national redistricting fights, according to Reuters.

APAC TRADE

EQUITIES

- APAC stocks traded mixed, albeit with a mildly positive bias as the region attempted to shrug off the lacklustre lead from Wall St, where sentiment was dampened amid continued tech weakness and hawkish-leaning FOMC Minutes.

- ASX 200 outperformed amid a slew of earnings releases and breached the 9,000 level for the first time in history.

- Nikkei 225 was dragged lower by weakness in pharmaceuticals and automakers, with the latter not helped by reports that Japanese automakers are passing some of the expense of US tariffs through to American car buyers, which is a change from their strategy of absorbing the impact.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark led lower by underperformance in tech stocks including Baidu and Xiaomi, despite both recently reporting a jump in profits, while the mainland remained propped up following the PBoC's liquidity efforts.

- US equity futures traded rangebound amid ongoing tentativeness as participants continued to await Fed Chair Powell's comments at Jackson Hole.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed with losses of 0.2% on Wednesday.

FX

- DXY kept within tight parameters after softening yesterday with mild headwinds seen amid Fed independence concerns as President Trump was said to be considering attempting to fire Fed Governor Cook due to accusations of mortgage fraud. Nonetheless, the downside was cushioned owing to the hawkish-leaning FOMC Minutes from the July meeting which noted a majority of participants judged the upside risk to inflation was the greater risk compared with the labour market, although the meeting was conducted prior to the release of the latest NFP report with hefty downward revisions.

- EUR/USD remained flat after recent indecision and with little fresh drivers from the bloc to spur price action.

- GBP/USD languished around the prior day's trough after slipping back beneath the 1.3500 level as participants looked through the recent hotter-than-expected CPI report whereby a surge in airfares triggered the larger-than-expected services CPI print and ONS attributed some of this to the timing of school holidays, while ING noted this is a component the BoE is less concerned with in terms of overall inflationary pressure and that food inflation, which the Bank is more concerned with, hasn't changed much.

- USD/JPY eked slight gains after rebounding off support near the 147.00 level but with the upside capped amid the downbeat mood and lack of tier-1 data in Japan.

- Antipodeans proceeded sideways around this week's lows with little pertinent drivers to inspire a recovery from the recent RBNZ-triggered decline.

- PBoC set USD/CNY mid-point at 7.1287 vs exp. 7.1748 (Prev. 7.1384)

FIXED INCOME

- 10yr UST futures traded rangebound after recent two-way price action owing to the hawkish FOMC Minutes and with President Trump calling for Fed governor Cook to resign over mortgage fraud allegations. However, Cook has stated she will not be bullied into resigning, while price action was not helped by a relatively average 20yr auction.

- Bund futures pared some of yesterday's gains after ascending in tandem with US counterparts and following deflationary German PPI data.

- 10yr JGB futures faded most of its opening gains amid a lack of tier-1 data and after weaker demand at the enhanced liquidity auction for longer-dated JGBs.

COMMODITIES

- Crude futures extended on gains after advancing yesterday with the upside facilitated by bullish crude inventory data.

- Spot gold marginally pulled back and took a breather following its recent climb to around the USD 3,350/oz level and was unfazed by the hawkish-leaning FOMC Minutes.

- Copper futures lacked conviction amid the mixed risk appetite and as participants await Jackson Hole.

- Chile's Codelco estimates copper output for the El Teniente mine at 316k tonnes this year.

CRYPTO

- Bitcoin marginally declined and tested support at the USD 114k level.

NOTABLE ASIA-PAC HEADLINES

- Chinese Foreign Minister Wang Yi said on a trilateral with Pakistan and Afghanistan that the three sides should expand development cooperation and expand trade and investment exchanges, while he added it is necessary to improve the security dialogue mechanism and deepen law enforcement and security cooperation. Furthermore, he said the three sides should further strengthen exchanges at all levels and consolidate strategic mutual trust.

- Leading municipalities in China are reportedly seeking to achieve at least 70% self-sufficiency in AI chips by 2027 and are looking to redraw a national supply chain dominated by Nvidia (NVDA), according to Nikkei.

DATA RECAP

- Japanese S&P Global Manufacturing PMI Flash (Aug). 49.9 (Prev. 48.9)

- Japanese S&P Global Services PMI Flash (Aug). 52.7 (Prev. 53.6)

- Japanese S&P Global Composite PMI Flash (Aug). 51.9 (Prev. 51.6)

- Australian S&P Global Manufacturing PMI Flash (Aug). 52.9 (Prev. 51.3)

- Australian S&P Global Services PMI Flash (Aug). 55.1 (Prev. 54.1)

- Australian S&P Global Composite PMI Flash (Aug). 54.9 (Prev. 53.8)

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu ordered a reduction in timelines for taking control of Hamas strongholds and defeating the group, according to the PM’s office.

- Israeli military spokesman said after a clash with Hamas, that Israel entered the first stage of its planned attack on Gaza City and Israeli forces already have a hold on the outskirts of Gaza City.

- Israeli army targeted the beach camp in Gaza, according to an Al Arabiya correspondent.

- UN Secretary General Guterres called for an immediate ceasefire in Gaza to avoid massive death and destruction in Gaza City, while he called for Israel to reverse its decision to expand the illegal settlement expansion in the West Bank.

RUSSIA-UKRAINE

- Ukrainian President Zelensky's Chief of Staff warned against repeating mistakes of the 1994 Budapest memorandum on security guarantees and said Ukraine's allies have started active work on the military aspect of security guarantees, while a contingency plan is being developed with partners in case Russia extends the war or violates agreements from leaders' meetings.

- US VP Vance said on Fox News that Europeans are going to have to take the lion’s share of the burden in security. It was separately reported that a Pentagon top policy official told a small group of allies Tuesday night that the US plans to play a minimal role in any Ukraine security guarantees, according to POLITICO citing Defence Undersecretary for Policy Colby.

- Western official said a small group of military leaders were continuing discussions in Washington to work out options for security guarantees for Ukraine.

- Italian PM Meloni offered a plan to aid Ukraine in a day if Russia resumes war, according to Bloomberg.

OTHER

- North Korea has a heavily fortified, covert military base that could house its newest long-range ballistic missiles, which are potentially capable of striking the US mainland, according to a new report cited by the WSJ.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Reeves is said to be mulling cutting the tax-free pension lump sum in a move that would be expected to raise more than GBP 2bln a year, according to Telegraph sources.