US Market Open: US equity futures are modestly lower into Fed speak, Bunds pressured post-PMI

21 Aug 2025, 11:30 by Newsquawk Desk

- Fed Governor Cook said she has no intention of being bullied to step down from her position because of some questions raised in a tweet by FHFA Director Pulte.

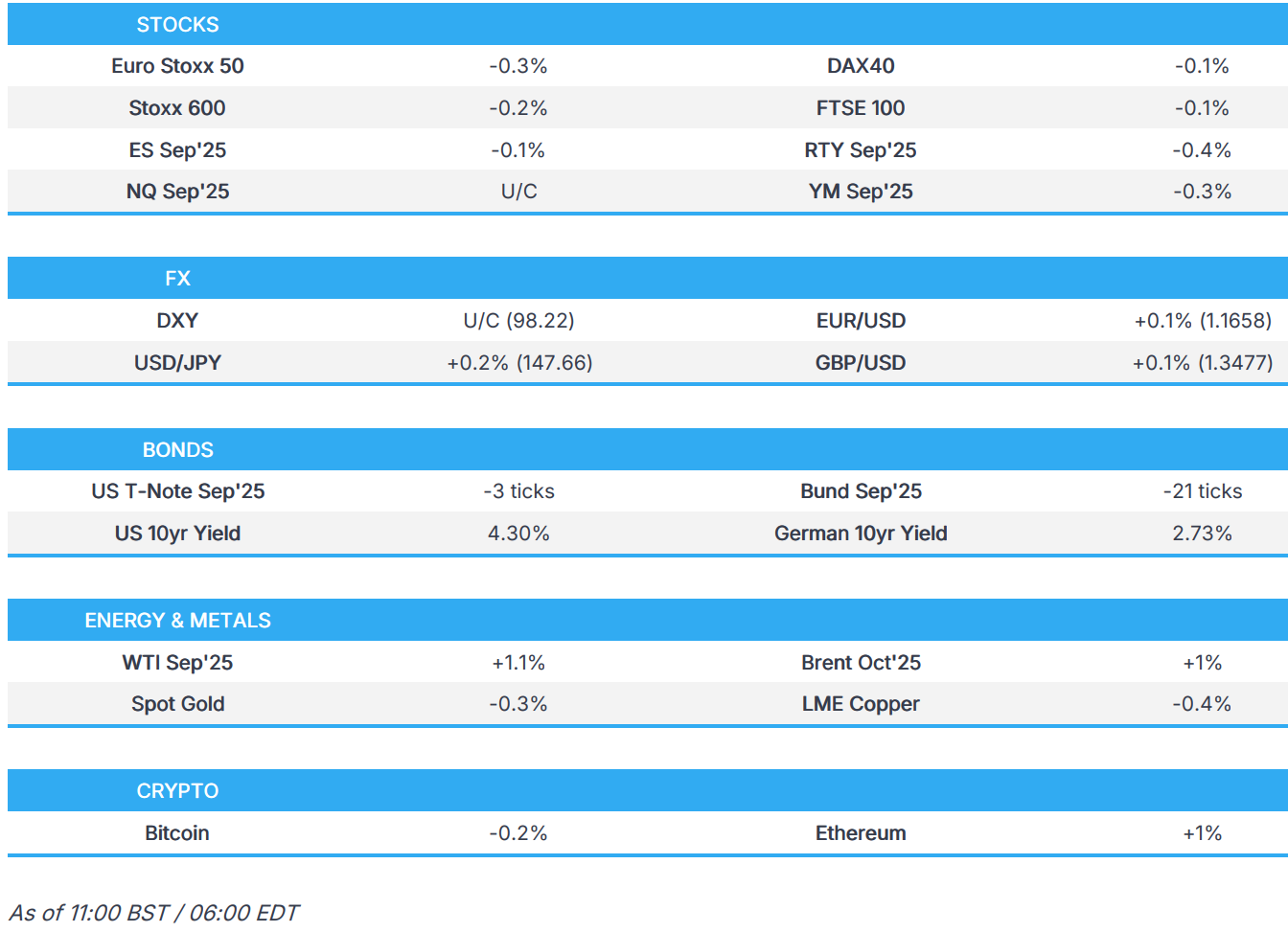

- European bourses tilt lower with the region unable to benefit from better-than-feared PMIs; US equity futures are mixed.

- USD is mixed vs. peers, GBP is top of the G10 leaderboard post-PMI.

- Bonds are pressured after PMIs, lower UK borrowing fails to lift spirits ahead of the Autumn Budget

- Crude is firmer as geopolitics remain in the limelight; Ukraine's Air Force said Russia used 574 drones and 40 missiles in an overnight attack.

- Looking ahead, US Flash PMIs, US Weekly/Continued Jobless Claims, Philly Fed Index, EU Consumer Confidence, Fed Jackson Hole Economic Symposium (21st-23rd), Speech from Fedʼs Bostic, Schmid, Goolsbee, Supply from US, Earnings from Walmart.

TARIFFS/TRADE

- China’s Commerce Minister talked with Kazakhstan’s Trade Minister and said China is ready to work with Kazakhstan to promote the upgrading of bilateral trade, while China is ready to strengthen cooperation in emerging fields and accelerate the cultivation of new trade formats.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) are trading with little in the way of a clear bias. Geopolitical tensions resurfaced early doors after Ukraine's Air Force stated that Russia used 574 drones and 40 missiles in an overnight attack. Focus also on EZ PMIs which saw the saw the composite move further into expansionary territory.

- European equity sectors show a mostly negative tilt with stock-specific updates relatively light. Energy names sit at the top of the leaderboard amid upside in underlying crude prices. To the downside, Media names lag with Wolters Kluwer (-2.2%) a notable underperformer in the sector following a PT reduction at Morgan Stanley.

- US equity futures are trading mixed/flat (ES -0.1%, NQ U/C, RTY -0.4%) after Wednesday's mostly soft close, which saw a continuation of big-tech weakness.

- Tesla (TSLA) partially evacuates German plant following fire in battery pack processing facility, according to Handelsblatt.

- NVIDIA (NVDA) - Beijing summoned Chinese tech companies like ByteDance, Alibaba, Tencent and Baidu to discuss their use of NVIDIA chips and encourage them to use more homegrown options, according to Nikkei sources.

- Apple (AAPL) will open a new store in India’s southern tech hub of Bangalore early next month, "ramping up its push into a key growth market", according to Bloomberg

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- Steady trade for DXY after a session yesterday, which was dominated by newsflow surrounding the Fed. US rates markets endured a steepening of the curve, led by the front-end amid reporting that President Trump could fire Fed Governor Cook amid alleged mortgage fraud. Thereafter, attention pivoted to the account of the July policy announcement, which was viewed with a hawkish lens. DXY sits towards the mid-point of Wednesday's 98.07-44 range.

- EUR saw some pressure early doors after comments from Ukraine's Air Force that Russia used 574 drones and 40 missiles in an overnight attack. This has helped reinforce the message that despite a more encouraging direction of travel for peace talks, the reality on the ground remains tense between Russia and Ukraine. Some of the pessimism was faded following flash PMI metrics from across the Eurozone with a solid report from France kickstarting the recovery and followed by a mostly positive German release. The EZ-wide print saw the composite move further into expansionary territory. EUR/USD sits just above its 50DMA at 1.1645.

- JPY is fractionally weaker vs. the USD after a session of gains on Wednesday, which were in part driven by a refocus on interest-rate differentials as the front-end of the US curve was dragged lower by the possibility of Fed Governor Cook being removed from her position. Overnight, there was little follow-through seen from mixed flash Japanese PMI metrics for August, which saw the manufacturing metric tick higher from its prior (but remain sub-50) and services fall from its previous (but remain above 50). USD/JPY sits within Wednesday's 146.87-147.81.

- GBP is the marginal outperformer across the majors following a better-than-expected outturn for flash August services and composite PMIs, which rose further into expansionary territory. Cable has picked up from its 1.3436 session low with a current session peak at 1.3476.

- Antipodeans are both are a touch softer vs. the USD with NZD unable to launch much of a recovery from Wednesday's RBNZ-induced losses and AUD failing to garner any support from upticks in flash PMI metrics for August. AUD/USD is at its lowest level since June 23rd with focus on a test of the 0.64 mark and the 200DMA @ 0.6386.

- PBoC set USD/CNY mid-point at 7.1287 vs exp. 7.1748 (Prev. 7.1384)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs began the European session around the unchanged mark, with price action fairly tentative in a continuation of the lacklustre trade seen overnight. As the European morning kicked off, trade has largely been dictated by Bunds, which have had a number of regional PMIs to digest (more in Bunds below). US paper currently trades lower by a handful of ticks, in a 111-24 to 111-29 range, currently contained within the prior day's confines. Looking ahead, weekly initial jobless claims and US PMIs alongside Fed speak from Bostic and Schmid.

- Bund Sept’25 started the European session around the unchanged mark and then slipped on both the French and then German PMI metrics, which overall highlighted the ongoing strength in the Manufacturing sector, whilst Services was a little more subdued. The EZ wide figure confirmed the strong Manufacturing / slightly softer Services picture, with the former surprisingly climbing into expansionary territory. In terms of the commentary, it highlighted that “U.S. trade policy is leaving its mark. Foreign orders in the eurozone manufacturing sector have declined for the second month in a row”.

- Gilts traded subdued throughout the European morning, taking leads from the hotter-than-expected PMI metrics in Europe. Into the region’s own figures, UK paper traded lower by around 15 ticks. Thereafter, on the region’s own PMI metrics, Gilts fell from 90.99 to 90.91 before trimming half of the move; currently trading in a 90.82 to 91.22 range. Unlike in Europe, the upside in Composite was thanks to strength in the Services sector whilst Manufacturing was subdued. It is worth highlighting that the accompanying release was fairly downbeat; “Payroll numbers also continue to be cut at an aggressive rate”; “the demand environment remains both uneven and fragile”.

- France sells EUR 10.499bln vs exp. EUR 8.5-10.5bln 2.40% 2028, 2.50% 2030, and 2.70% 2031 OAT.

- Click for a detailed summary

COMMODITIES

- Modestly positive trade in the crude complex in what has been a quiet session thus far, but with eyes remaining on geopolitics amid a couple of notable updates. WTI resides in a USD 62.78-63.40/bbl range while Brent sits in a USD 66.88-67.49/bbl parameter.

- Softer trade across precious metals, albeit modest in spot gold and silver, with newsflow on the lighter side and with the metals largely moving in tandem with the dollar. Price action this morning sees the precious metals complex subdued, with spot gold on either side of its 50 DMA (~3,348.10/oz) in a USD 3,334.28.56-3,352.30/oz range.

- Subdued price action across the base metals complex - in fitting with the broader market mood as traders look ahead to the Jackson Hole Symposium. 3M LME copper prices reside in a USD 9,689.45-9,739.40/t range.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HCOB Manufacturing Flash PMI (Aug). 50.5 vs. Exp. 49.5 (Prev. 49.8); EU HCOB Services Flash PMI (Aug). 50.7 vs. Exp. 50.8 (Prev. 51); EU HCOB Composite Flash PMI (Aug). 51.1 vs. Exp. 50.7 (Prev. 50.9); US trade policy is leaving its mark. Foreign orders in the eurozone manufacturing sector have declined for the second month in a row"

- French HCOB Manufacturing Flash PMI (Aug), 49.9 vs. Exp. 48 (Prev. 48.2); Services Flash PMI (Aug), 49.7 vs. Exp. 48.5 (Prev. 48.5); Composite Flash PMI (Aug), 49.8 vs. Exp. 48.5 (Prev. 48.6)

- German HCOB Manufacturing Flash PMI (Aug), 49.9 vs. Exp. 48.8 (Prev. 49.1); Services Flash PMI (Aug), 50.1 vs. Exp. 50.3 (Prev. 50.6); Composite Flash PMI (Aug), 50.9 vs. Exp. 50.2 (Prev. 50.6)

- UK Flash Composite PMI (Aug), 53.0 vs. Exp. 51.6 (Prev. 51.5); Manufacturing PMI (Aug), 47.3 vs. Exp. 48.3 (Prev. 48); Services PMI (Aug), 53.6 vs. Exp. 51.8 (Prev. 51.8)

- UK PSNB Ex Banks GBP (Jul) 1.054B GB vs. Exp. 2.6B GB (Prev. 20.684B GB, Rev. 22.560B GB).

- UK PSNCR, GBP (Jul) 3.002B GB (Prev. -16.108B GB, Rev. -16.367B GB)

- Norwegian GDP Growth Mainland (Q2) 0.6% vs. Exp. 0.3% (Prev. 1.0%)

- Norwegian GDP Growth (Q2) 0.8% (Prev. -0.1%)

- Swiss Trade (Jul) 4.591B (Prev. 5.790B, Rev. 5.726B); Watch Exports +6.9% Y/Y (prev. -5.6%)

NOTABLE US HEADLINES

- Fed Governor Cook said she learned from the media that FHFA Director Pulte posted he was making a criminal referral based on a mortgage application from four years ago, before she joined the Fed, while she has no intention of being bullied to step down from her position because of some questions raised in a tweet. Furthermore, she intends to take any questions about her financial history seriously as a member of the Federal Reserve and is gathering accurate information to answer any legitimate questions and provide the facts.

- Texas House approved the Trump-backed congressional map that would give Republicans more seats on Capitol Hill, igniting national redistricting fights, according to Reuters.

GEOPOLITICS

MIDDLE EAST

- UN Secretary General Guterres called for an immediate ceasefire in Gaza to avoid massive death and destruction in Gaza City, while he called for Israel to reverse its decision to expand the illegal settlement expansion in the West Bank.

RUSSIA-UKRAINE

- Ukraine's Air Force said Russia used 574 drones and 40 missiles in an overnight attack.

- Moscow to host first nuclear summit on September 25", according to Al Arabiya.

- Ukraine President Zelensky said Kyiv wants to have an understanding of security guarantees within 7-10 days, followed by bilateral and trilateral leaders meetings. If Russia is not ready for a bilateral leaders meeting, Ukraine and Europe want to see strong US reaction. ‘Flamingo’ missile is Ukraine’s most successful missile, mass production expected by early next year. Ukrainian proposal for US drone deal entails production worth USD 50bln over five years. Ten million drones expected to be produced yearly as part of the deal. China not included in security guarantees because China did not help after the Russian invasion. On Budapest as venue for peace talks: “For now, this is challenging.”Ukraine will not legally recognise Russia's occupation of its territories. There is no signal that Moscow is prepared to end the war and have substantial conversations. Ukraine has tested a new long-range missile.

- Ukrainian President Zelenksy's Chief of Staff warned against repeating mistakes of the 1994 Budapest memorandum on security guarantees and said Ukraine's allies have started active work on the military aspect of security guarantees, while a contingency plan is being developed with partners in case Russia extends the war or violates agreements from leaders' meetings.

- US VP Vance said on Fox News that Europeans are going to have to take the lion’s share of the burden in security. It was separately reported that a Pentagon top policy official told a small group of allies Tuesday night that the US plans to play a minimal role in any Ukraine security guarantees, according to POLITICO citing Defense Undersecretary for Policy Colby.

- Turkish defence ministry source said ceasefire between Russia and Ukraine needed before discussing peacekeeping mission framework, via Reuters citing sources.

- Russia attacked a key Ukrainian gas compressor station vital for storage operations, according to Reuters sources.

- Ukraine military said it hit a Russian oil refinery, drone warehouse and fuel base overnight.

OTHER

- North Korea has a heavily fortified, covert military base that could house its newest long-range ballistic missiles, which are potentially capable of striking the US mainland, according to a new report cited by the WSJ.

CRYPTO

- Bitcoin is a little lower and trades around USD 113k, whilst Ethereum gains and trades around USD 4.2k.

APAC TRADE

- APAC stocks traded mixed, albeit with a mildly positive bias as the region attempted to shrug off the lacklustre lead from Wall St, where sentiment was dampened amid continued tech weakness and hawkish-leaning FOMC Minutes.

- ASX 200 outperformed amid a slew of earnings releases and breached the 9,000 level for the first time in history.

- Nikkei 225 was dragged lower by weakness in pharmaceuticals and automakers, with the latter not helped by reports that Japanese automakers are passing some of the expense of US tariffs through to American car buyers, which is a change from their strategy of absorbing the impact.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark led lower by underperformance in tech stocks including Baidu and Xiaomi, despite both recently reporting a jump in profits, while the mainland remained propped up following the PBoC's liquidity efforts.

DATA RECAP

- Japanese S&P Global Manufacturing PMI Flash (Aug). 49.9 (Prev. 48.9)

- Japanese S&P Global Services PMI Flash (Aug). 52.7 (Prev. 53.6)

- Japanese S&P Global Composite PMI Flash (Aug). 51.9 (Prev. 51.6)

- Australian S&P Global Manufacturing PMI Flash (Aug). 52.9 (Prev. 51.3)

- Australian S&P Global Services PMI Flash (Aug). 55.1 (Prev. 54.1)

- Australian S&P Global Composite PMI Flash (Aug). 54.9 (Prev. 53.8)