Europe Market Open: APAC stocks traded mixed amid broader cautiousness & DXY firm awaiting Powell comments

22 Aug 2025, 07:00 by Newsquawk Desk

- APAC stocks traded mixed amid cautiousness heading into Fed Chair Powell's remarks at Jackson Hole and following the subdued handover from Wall St, where participants digested a slew of data and mostly hawkish Fed comments.

- US President Trump said we will know in about two weeks regarding Russia-Ukraine. Ukrainian President Zelensky said Russia's overnight attacks show that Moscow is trying to avoid the need for meetings aimed at ending the war.

- Chinese President Xi is unlikely to attend ASEAN Leaders' Summit in October, "dashing hopes of a meeting with US President Tump at the summit", according to Reuters sources.

- European equity futures indicate a marginally lower cash market open with Euro Stoxx 50 futures down 0.1% after the cash market closed with losses of 0.2% on Thursday.

- Looking ahead, highlights include Canadian Retail Sales, Fed's Jackson Hole Symposium (August 21st-23rd); Speakers include Fed Chair Powell & BoE Governor Bailey.

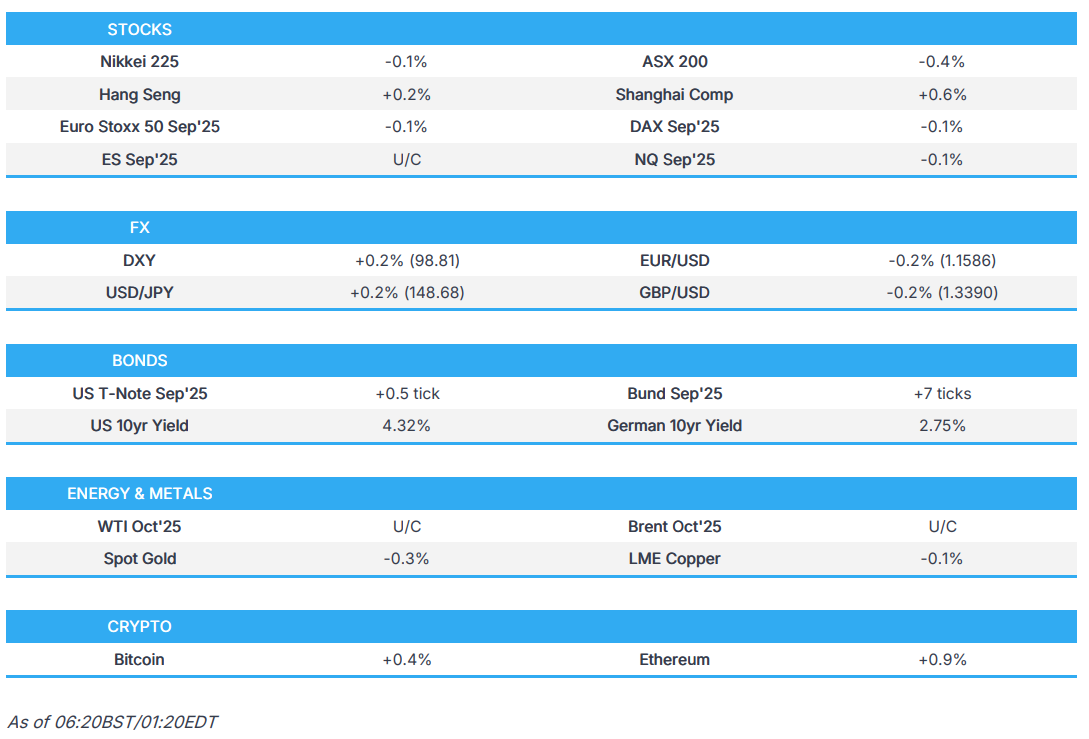

SNAPSHOT

Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks ultimately closed lower after a choppy session amid cautiousness ahead of Jackson Hole and after hawkish commentary, although the Russell 2000 outperformed, while sectors were predominantly lower with underperformance in Consumer Staples and Consumer Discretionary after retailer earnings in which Walmart missed on EPS and Coty (COTY) tumbled post-earnings.

- The highlights of the day were the US data releases and Fed speak, including a strong S&P Global Flash PMI report for the US which was accompanied by hawkish commentary within the report, while comments from Fed officials including Hammack, Schmid and to some extent Bostic, were hawkish on inflation and mostly pointed to a lack of urgency to cut rates.

- SPX -0.40% at 6,370, NDX -0.46% at 23,143, DJI -0.34% at 44,786, RUT +0.21% at 2,274.

- Click here for a detailed summary.

TARIFFS/TRADE

- Chinese President Xi is unlikely to attend ASEAN Leaders' Summit in October, "dashing hopes of a meeting with US President Tump at the summit"; while Premier Li is set to represent China, according to two regional sources cited by Reuters.

- Canadian PM Carney spoke with US President Trump and the two discussed trade challenges and opportunities, while they agreed to reconvene shortly, according to Bloomberg.

NOTABLE HEADLINES

- Fed's Collins (2025 voter) signalled an openness for a rate cut as soon as next month amid labour market concerns and flagged that higher tariffs might squeeze consumers’ purchasing power, which could weaken spending. Furthermore, Collins said she expects inflation to continue rising through the end of the year before resuming a decline in 2026, according to a Wall Street Journal article that noted divisions grow inside the Fed ahead of the September rate cut decision and cited Fed's Hammack (2026 voter) opposing cuts due to rising inflation.

- Fed's Goolsbee (2025 voter) said the September FOMC meeting is a live meeting and the Fed has been getting mixed messages on the economy, while he added that the most recent inflation data wasn't great and the Fed still has time to take in more data. Goolsbee responded he doesn't want to get his hands tied, when asked about a September rate cut, as well as commented that a rise in services inflation is a dangerous data point and reacting to a stagflation shock is very difficult. Furthermore, he said central bank independence is critically important, and that tariff increases don't seem close to being done and risk persistent inflation.

- WSJ's Timiraos wrote "Powell Plans U-Turn on an Economic Strategy That Soured" and "The Fed unveiled a strategy five years ago for worries that the economy outgrew. Now, it will formally reset". Fed officials are reportedly readying to quietly pull back from a signature policy innovation announced five years ago in which they focused on the risks brought on by near-zero interest rates and low prices, with officials to abandon that approach as it is now seen as no longer relevant given the backdrop of high and more volatile inflation. Furthermore, Timiraos noted that Powell is expected to unveil the shift at Jackson Hole on Friday, although changes won’t impact near-term policy decisions and are instead part of the framework the Fed uses to interpret its mandate inflation and employment mandates.

- DoJ official urged Fed Chair Powell to remove Fed Governor Cook, according to Bloomberg.

- US President Trump said the US is leading the AI race and that AI is the hottest thing in decades.

- US President Trump's administration reportedly considers a plan to reallocate USD 2bln in CHIPS Act funding for critical minerals and aims to give Commerce Secretary Lutnick greater oversight of minerals financing decisions, according to Reuters citing sources.

- US Secretary of State Rubio said the US is pausing all issuances of worker visas for commercial truck drivers with immediate effect. It was separately reported that President Trump's administration said it is reviewing all 55mln people with US visas for potential deportable violations, according to AP.

- California Senate passed a redistricting plan aimed at giving Democrats five more seats in the US House of Representatives, countering a similar Trump-backed move in Texas, while the redrawn map in California advanced to the state assembly and would ultimately require voter approval.

- Meta (META) is said to be hiring another key Apple (AAPL) AI executive, according to Bloomberg sources.

APAC TRADE

EQUITIES

- APAC stocks traded mixed amid cautiousness heading into Fed Chair Powell's remarks at Jackson Hole and following the subdued handover from Wall St, where participants digested a slew of data and mostly hawkish Fed comments.

- ASX 200 marginally declined with price action choppy around the 9,000 focal point as participants continue to mull over the latest earnings releases.

- Nikkei 225 swung between gains and losses with participants indecisive after recent yen weakness and somewhat mixed Japanese inflation data, which mostly matched estimates, aside from the slightly hotter-than-expected Core CPI reading.

- Hang Seng and Shanghai Comp were kept afloat with strength seen following recent earnings releases and with chipmakers supported after Beijing summoned Chinese tech companies to discuss their use of NVIDIA (NVDA) chips and encourage them to use more homegrown options, while NVIDIA ordered a halt to H20 production following China’s directive against purchases.

- US equity futures lacked direction as participants await policy clues from Fed Chair Powell's looming speech.

- European equity futures indicate a marginally lower cash market open with Euro Stoxx 50 futures down 0.1% after the cash market closed with losses of 0.2% on Thursday.

FX

- DXY remained firm and held on to recent gains after strong PMI data stateside which included hawkish commentary within the report, while there was also recent rhetoric from Fed officials including Hammack and Schmid who were both hawkish on inflation and suggested a lack of urgency to cut rates. Furthermore, Goolsbee noted the September FOMC meeting is a live meeting, but responded that he didn't want to get his hands tied when asked about a September rate cut, while all eyes now turn to Powell at the Jackson Hole Symposium.

- EUR/USD breached beneath the prior day's trough to a sub-1.1600 level after giving up ground to the recent dollar strength, while participants also look ahead to comments from ECB President Lagarde who will participate in a panel discussion with BoE Governor Bailey and BoJ Governor Ueda on Saturday at Jackson Hole.

- GBP/USD was subdued and tested the 1.3400 level to the downside, after recent tailwinds from strong UK Services and Composite PMI data proved to be short-lived.

- USD/JPY extended on yesterday's advances after returning to the 148.00 territory and was unfazed by the Japanese inflation data in which Core CPI printed firmer-than-expected.

- Antipodeans traded sideways amid a lack of pertinent data and with markets tentative as all focus turns to Fed Chair Powell.

- PBoC set USD/CNY mid-point at 7.1321 vs exp. 7.1871 (Prev. 7.1287).

FIXED INCOME

- 10yr UST futures attempted to nurse losses after retreating in the aftermath of strong US PMI data and hawkish Fed comments ahead of Powell's highly-awaited speech.

- Bund futures rebounded off the prior day's lows after finding support near the 129.00 level but with the recovery limited by a lack of pertinent drivers.

- 10yr JGB futures recouped early losses and returned to flat territory amid the flimsy risk appetite in Tokyo, but with demand contained following the latest inflation data from Japan which mostly printed in line with estimates aside from the firmer-than-expected Core CPI reading.

COMMODITIES

- Crude futures took a breather following the two-way price action and an intraday rebound seen yesterday amid pessimism regarding a Russia and Ukraine deal.

- Spot gold softened amid a firmer dollar, with price action contained as markets await Powell's Jackson Hole speech.

- Copper futures plateaued overnight following the prior day's recovery which was facilitated by strong US Manufacturing PMI data, but with further upside capped amid some cautiousness heading into Fed Chair Powell's key speech.

CRYPTO

- Bitcoin mildly gained and returned to above the USD 113k level after rebounding from this month's trough.

- EU reportedly speeds up plans for a digital Euro after the US passed the stablecoin law last month, according to FT.

NOTABLE ASIA-PAC HEADLINES

- US President Trump could raise a "sensitive" China-related topic in the upcoming summit with South Korean President Lee, according to an expert cited by Yonhap.

- NVIDIA (NVDA) ordered a halt to H20 chip production after China's directive against purchases, according to The Information.

DATA RECAP

- Japanese National CPI YY (Jul) 3.1% vs Exp. 3.1% (Prev. 3.3%)

- Japanese National CPI Ex. Fresh Food YY (Jul) 3.1% vs Exp. 3.0% (Prev. 3.3%)

- Japanese National CPI Ex. Fresh Food & Energy YY (Jul) 3.4% vs Exp. 3.4% (Prev. 3.4%)

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu said Israel will begin Gaza ceasefire negotiations to end the war and release hostages.

- US President Trump’s administration has asked Israel to reduce "non-urgent" military action in Lebanon to bolster the Lebanese government's decision to start the process of disarming Hezbollah, according to two sources with direct knowledge cited by Axios.

- Iran's Foreign Minister said he will have a joint phone call with French, British and German counterparts on Friday to discuss nuclear talks and sanctions, according to IRNA.

- United States imposed sanctions on ships and entities connected to Iran.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said Russia's overnight attacks show that Moscow is trying to avoid the need for meetings aimed at ending the war.

- US President Trump said we will know in about two weeks regarding Russia-Ukraine.

- North Korean leader Kim lauded military officers who participated in overseas military operations as heroes and said soldiers at Kursk proved the might of the North Korean military in the world's eyes, according to KCNA.

OTHER

- China condemned US military build-up off Venezuela coast as foreign interference in regional affairs, according to Fox News.

EU/UK

DATA RECAP

- UK GfK Consumer Confidence (Aug) -17.0 vs. Exp. -20.0 (Prev. -19.0)