US Market Open: DXY & equity futures firmer, Fixed income lacklustre into Powell

22 Aug 2025, 11:15 by Newsquawk Desk

- Chinese President Xi is unlikely to attend ASEAN Leaders' Summit in October, "dashing hopes of a meeting with US President Trump at the summit"; while Premier Li is set to represent China, according to two regional sources cited by Reuters

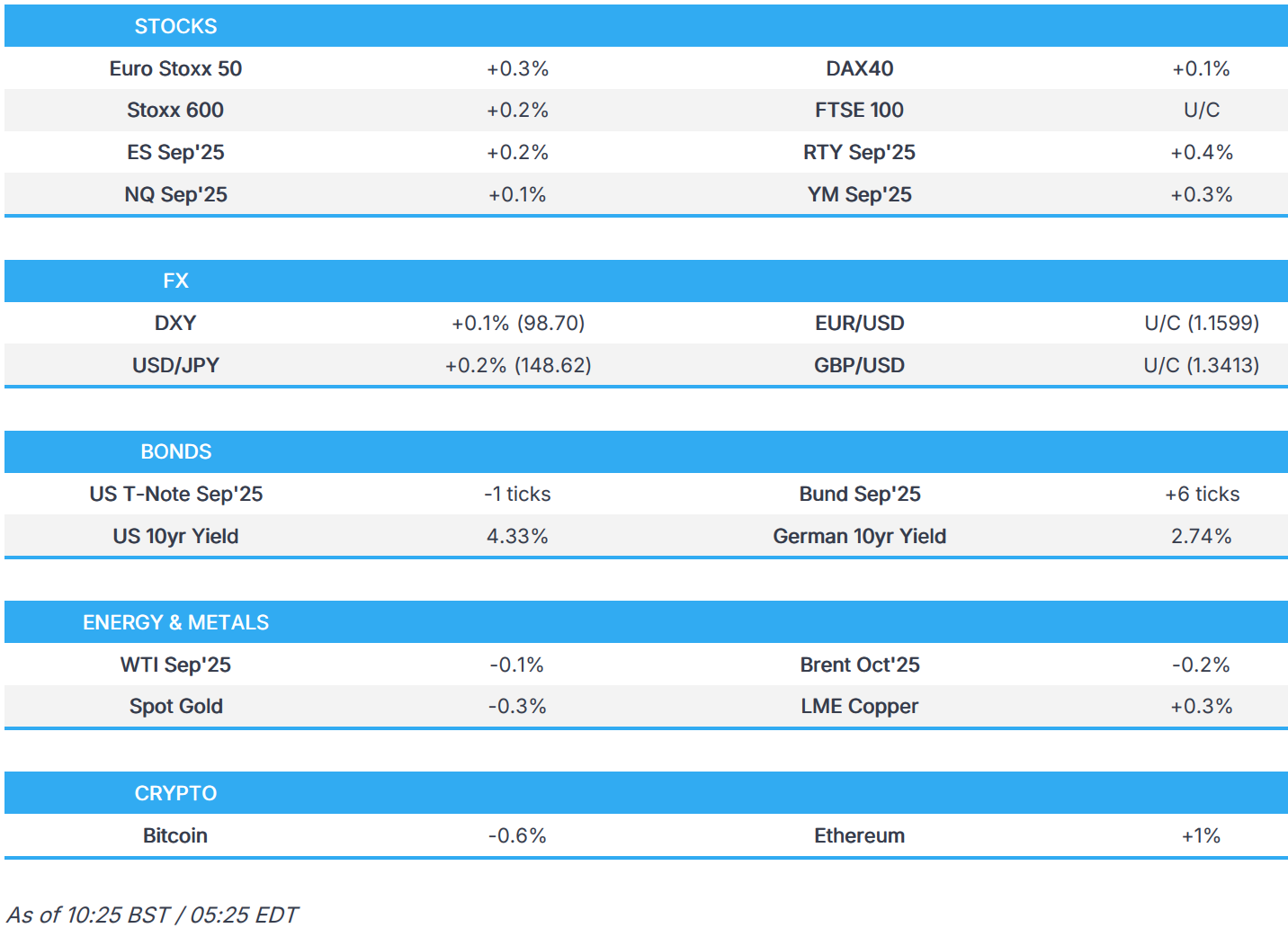

- European bourses move higher; US equity futures also gain as the RTY +0.4% outperforms; NVIDIA -1% after H20 production halt.

- DXY holds an upward bias post-PMIs on Thursday, whilst fixed income trades steady into Fed Chair Powell.

- Choppy trade in the crude complex, as traders digest halts to the Druzhba pipeline; sideways trade across precious metals.

- Looking ahead, highlights include Canadian Retail Sales, Fed's Jackson Hole Symposium (August 21st-23rd); Speakers include Fed Chair Powell, Hammack and Collins.

TARIFFS/TRADE

- Chinese President Xi is unlikely to attend ASEAN Leaders' Summit in October, "dashing hopes of a meeting with US President Trump at the summit"; while Premier Li is set to represent China, according to two regional sources cited by Reuters.

- South Korea's Foreign Minister Cho is expected to meet with US Secretary of State Rubio as early as today before the Trump summit with South Korea President Lee, according to Yonhap. South Korean top security adviser confirms discussions with US on increasing defence spending, citing NATO framework as reference; said US investment and weapons purchases are under review. In talks about nuclear power cooperation with the US.

- South Korean top security adviser confirms discussions with US on increasing defence spending, citing NATO framework as reference; said US investment and weapons purchases are under review.

EUROPEAN TRADE

EQUITIES

- European stocks (STOXX 600 +0.1%) are little changed, albeit with a positive bias amid a lack of newsflow into Fed Chair Powell’s speech in the European afternoon. A bout of risk aversion, with no specific fundamental driver, was seen pre-cash open. Nonetheless, this did little to inflict sustained pressure on European bourses, which have been edging higher since the lacklustre open.

- European sectors opened mostly in the red after a quiet open. However, positivity has since dominated across the board as sentiment improved. Chemicals sits at the top, led by Akzo Nobel (+5%), after the FT reported that Activist Cevian acquired a more than 3% (EUR 300ln) stake in the company. Banks also underperform, though they are off their worst levels; this comes after Bloomberg reported that Poland is planning to increase corporate income tax for banks, proposing to increase the tax to 30% from 19%.

- US equity futures (ES +0.2%, NQ +0.2%, RTY +0.4%) have been moving in tandem with those across the Atlantic. RTY outperforms as investors continue optimism about the YTD underperforming small-cap index.

- UBS Global Wealth Management forecasts 2025 Eurozone earnings growth to contract by 3% (prev. 0%).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is firmer on Friday in the run-up to Fed Chair Powell's speech at 15:00BST /10:00 EDT, which is expected to see a text release. Attention will focus on whether Chair Powell’s Jackson Hole remarks indicate any shift in views since recent US data and if he signals a September rate cut, which markets price at ~70% probability. DXY trades in a 98.58-98.83 intraday range after finding support at the 50 DMA (at 98.09 today) earlier in the week. Powell aside, there will be commentary from Collins and Hammack.

- Softer in tandem with the firmer Dollar. EUR remains subdued by the diminishing optimism surrounding Russia-Ukraine, in which US President Trump said, "we will know in about two weeks regarding Russia-Ukraine". Meanwhile, Ukrainian President Zelensky said Russia's overnight attacks show that Moscow is trying to avoid the need for meetings aimed at ending the war. On the data front, German GDP for Q2 was revised lower across the board, albeit this prompted little EUR move at the time, with eyes turning to Fed Chair Powell's speech at 15:00 BST for a dollar-induced impulse. EUR/USD currently sits in a 1.1583-1.1668 range.

- Choppy trade overall in which USD/JPY initially extended on Thursday's advances overnight after returning to the 148.00 territory and was unfazed by the Japanese inflation data, in which Core CPI printed firmer-than-expected. Inflows into the JPY were seen around 15 minutes before the European equity cash open, in tandem with some broader risk aversion despite a lack of fresh catalysts at the time, though it was short-lived. USD/JPY trades in a 148.27-148.77 parameter.

- Not much in the way of Sterling-specific catalysts nor newsflow, with Cable moving in tandem with the Dollar ahead of a long weekend (UK bank holiday on Monday).

- PBoC set USD/CNY mid-point at 7.1321 vs exp. 7.1871 (Prev. 7.1287).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are flat and have been trading in a very narrow 111-16 to 111-20 range, as traders await an appearance from Fed Chair Powell at 15:00 BST / 10:00 EDT. On that, focus will be on whether Chair Powell’s Jackson Hole remarks indicate any shift in views since recent US data and if he signals a September rate cut, which markets price at ~70% probability. In terms of price action, currently contained in a minuscule 4 tick range, and within the confines made in the prior session.

- Bunds are also flat/incrementally firmer and trade in a very narrow 128.94 to 129.12 range; the trough today was made in the moments after the release of German GDP revisions, which were lower than the prelim; Q/Q revised down to 0.2% (prev. 0.4%) whilst the Y/Y metric declined 0.3% (prev. no growth).

- Gilts are on the back foot today and underperforming vs peers, albeit within narrow ranges. Nothing really fresh driving things at the moment for UK paper, but perhaps as fiscal-related fears resurge into the Autumn Budget. From a yield perspective, the 10yr has been knocking on the door of the 4.75% mark; traders tout levels above 4.80% as the “danger zone” for Chancellor Reeve’s and her “black hole”.

- Click for a detailed summary

COMMODITIES

- Modest gains across the crude complex despite the firmer Dollar and alongside the choppy mood across the stock market, with equity bourses swinging from modest losses to mild gains. Upside in the crude complex comes amid diminishing optimism surrounding Russia-Ukraine, in which US President Trump said, "We will know in about two weeks regarding Russia-Ukraine". Meanwhile, Ukrainian President Zelensky said Russia's overnight attacks show that Moscow is trying to avoid the need for meetings aimed at ending the war. On that note, the Hungarian Foreign Minister said oil deliveries to Hungary via the Druzhba pipeline have been halted due to attacks near the Russia-Belarus border. Deliveries seem to be suspended for at least five days, according to reports. WTI currently resides in a 62.05-62.68/bbl range while Brent sits in a USD 67.44-67.95/bbl range.

- Mostly subdued trade across precious metals amid the firmer Dollar as participants look ahead to Fed Chair Powell's speech at 15:00BST /10:00 EDT which is expected to see a text release. Spot gold trades under its 50 DMA (3,346.01) in a USD 3,325.38-3,340.14/oz range.

- Mixed within narrow ranges amid a lack of pertinent drivers this morning ahead of risk events. 3M LME copper prices reside in a USD 9,714.05-9,781.00/t range.

- Hungary and Slovakia call on European Commission to guarantee energy supply security. As a consequence, deliveries seem to be suspended for at least five days.

- Germany said there is no impact on German energy supply security from the Druzhba pipeline disruption.

- Click for a detailed summary

NOTABLE DATA RECAP

DATA RECAP

- German GDP Detailed YY SA (Q2) 0.2% vs. Exp. 0.4% (Prev. 0.4%)

- German GDP Detailed QQ SA (Q2) -0.3% vs. Exp. -0.1% (Prev. -0.1%)

- German GDP Detailed YY NSA (Q2) -0.2% vs Exp. 0.0% (Prev. 0.0%)

- UK GfK Consumer Confidence (Aug) -17.0 vs. Exp. -20.0 (Prev. -19.0)

- Swedish Unemployment Rate SA (Jul) 8.9% vs. Exp. 8.6% (Prev. 8.3%)

NOTABLE EUROPEAN HEADLINES

- German Economy Minister said Q2 GDP figures show "urgent need for action"; Further and courageous reforms are unavoidable to make the German economy competitive.

NOTABLE US HEADLINES

- Fed's Collins (2025 voter) signalled an openness for a rate cut as soon as next month amid labour market concerns and flagged that higher tariffs might squeeze consumers’ purchasing power, which could weaken spending. Furthermore, Collins said she expects inflation to continue rising through the end of the year before resuming a decline in 2026, according to a Wall Street Journal article that noted divisions grow inside the Fed ahead of the September rate cut decision and cited Fed's Hammack (2026 voter) opposing cuts due to rising inflation.

- Fed's Goolsbee (2025 voter) said the September FOMC meeting is a live meeting and the Fed has been getting mixed messages on the economy, while he added that the most recent inflation data wasn't great and the Fed still has time to take in more data. Goolsbee responded he doesn't want to get his hands tied, when asked about a September rate cut, as well as commented that a rise in services inflation is a dangerous data point and reacting to a stagflation shock is very difficult. Furthermore, he said central bank independence is critically important, and that tariff increases don't seem close to being done and risk persistent inflation.

- WSJ's Timiraos wrote "Powell Plans U-Turn on an Economic Strategy That Soured" and "The Fed unveiled a strategy five years ago for worries that the economy outgrew. Now, it will formally reset". Fed officials are reportedly readying to quietly pull back from a signature policy innovation announced five years ago in which they focused on the risks brought on by near-zero interest rates and low prices, with officials to abandon that approach as it is now seen as no longer relevant given the backdrop of high and more volatile inflation. Furthermore, Timiraos noted that Powell is expected to unveil the shift at Jackson Hole on Friday, although changes won’t impact near-term policy decisions and are instead part of the framework the Fed uses to interpret its mandate inflation and employment mandates.

- US President Trump said the US is leading the AI race and that AI is the hottest thing in decades.

- US President Trump's administration reportedly considers a plan to reallocate USD 2bln in CHIPS Act funding for critical minerals and aims to give Commerce Secretary Lutnick greater oversight of minerals financing decisions, according to Reuters citing sources.

- US Secretary of State Rubio said the US is pausing all issuances of worker visas for commercial truck drivers with immediate effect. It was separately reported that President Trump's administration said it is reviewing all 55mln people with US visas for potential deportable violations, according to AP.

NOTABLE US STOCKS STORIES

- NVIDIA (NVDA) ordered a halt to H20 chip production after China's directive against purchases, according to The Information. NVIDIA (NVDA) said in a statement sent to the Global Times on Friday: "We constantly manage our supply chain to address market conditions", when asked about reports that NVIDIA ordered a halt to H20 production following China’s directive against purchases. NVIDIA (NVDA) said in a statement sent to the Global Times on Friday: "We constantly manage our supply chain to address market conditions", when asked about reports that NVIDIA ordered a halt to H20 production following China’s directive against purchases

- Meta (META) is said to be hiring another key Apple (AAPL) AI executive, according to Bloomberg sources.

- Starbucks (SBUX) expects non-binding bids for its China business within two weeks, according to Reuters sources.

- Tesla (TSLA) plans to integrate DeepSeek and Dubao voice controls for its vehicles in China, according to Bloomberg.

GEOPOLITICS

MIDDLE EAST

- Iran's Foreign Minister said he will have a joint phone call with French, British and German counterparts on Friday to discuss nuclear talks and sanctions, according to IRNA.

- "Israeli Defence Minister: We have approved the army's plans to eliminate Hamas and evacuate the population in Gaza", according to Al Arabiya.

RUSSIA-UKRAINE

- Hungarian Foreign Minister said oil deliveries to Hungary via the Druzhba pipeline have been halted due to attacks near the Russia-Belarus border.

- North Korean leader Kim lauded military officers who participated in overseas military operations as heroes and said soldiers at Kursk proved the might of the North Korean military in the world's eyes, according to KCNA.

- Russia conducts naval exercises in the Baltic Sea, according to the defence ministry.

OTHER

- China condemned US military build-up off Venezuela coast as foreign interference in regional affairs, according to Fox News. China's Concord Resources plans to invest over USD 1bln in two oilfields in Venezuela, according to Reuters sources, and plans to produce 60k BPD by end-2026.

CRYPTO

- Bitcoin is modestly firmer but sits just shy of the USD 113k mark.

- EU reportedly speeds up plans for a digital Euro after the US passed the stablecoin law last month, according to FT.

APAC TRADE

- APAC stocks traded mixed amid cautiousness heading into Fed Chair Powell's remarks at Jackson Hole and following the subdued handover from Wall St, where participants digested a slew of data and mostly hawkish Fed comments.

- ASX 200 marginally declined with price action choppy around the 9,000 focal point as participants continue to mull over the latest earnings releases.

- Nikkei 225 swung between gains and losses with participants indecisive after recent yen weakness and somewhat mixed Japanese inflation data, which mostly matched estimates, aside from the slightly hotter-than-expected Core CPI reading.

- Hang Seng and Shanghai Comp were kept afloat with strength seen following recent earnings releases and with chipmakers supported after Beijing summoned Chinese tech companies to discuss their use of NVIDIA (NVDA) chips and encourage them to use more homegrown options, while NVIDIA ordered a halt to H20 production following China’s directive against purchases.

NOTABLE ASIA-PAC HEADLINES

- Japan 2026 budget requests to total around JPY 120tln, according to Kyodo.

- China's Industry Ministry said it has issued interim measures for controlling and managing rare earth mining, smelting, and separation.

- PBoC seeks feedback on draft regulations for interbank FX market.

DATA RECAP

- Japanese National CPI YY (Jul) 3.1% vs Exp. 3.1% (Prev. 3.3%)

- Japanese National CPI Ex. Fresh Food YY (Jul) 3.1% vs Exp. 3.0% (Prev. 3.3%)

- Japanese National CPI Ex. Fresh Food & Energy YY (Jul) 3.4% vs Exp. 3.4% (Prev. 3.4%)

- Chinese FDI (YTD) (Jul) -13.4% (Prev. -15.2%)