US Market Open: DXY steady & USTs are lower into supply and data; CAC 40 -1.7%, hit by French politics

26 Aug 2025, 10:50 by Newsquawk Desk

- US President Trump threatened to impose substantial additional tariffs on countries that do not remove discriminatory actions such as digital taxes.

- US President Trump posted a letter removing Fed's Cook from her position with immediate effect; Cook says she will not resign.

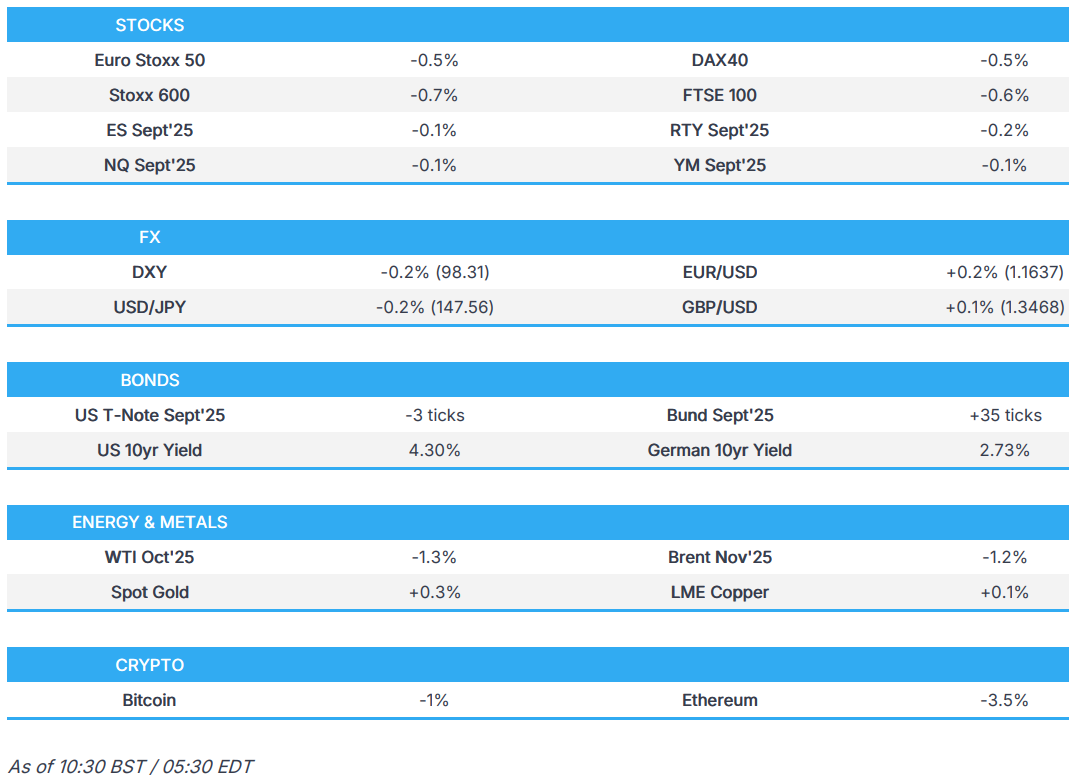

- European bourses are on the backfoot, but with clear underperformance in the CAC 40 as French politics take centre stage; US equity futures are slightly lower.

- USD is steady, EUR digests French political turmoil, JPY marginally outpaces peers.

- USTs pressured in reaction to Trump-Cook saga; Gilts/OATs digest regional political woes.

- XAU outperforms after Trump sends letter to Fed's Cook; Crude gives back geopolitical-driven gains.

- Looking ahead, US Durable Goods (Jul), Consumer Confidence (Aug), Atlanta Fed GDP, NBH Announcement, E3/Iran Nuclear talks, Fed Discount Rate Minutes, Speakers including Fed’s Barkin & BoE’s Mann, Supply from the US.

TARIFFS/TRADE

- US President Trump threatened on Truth Social to impose substantial additional tariffs on countries that do not remove discriminatory actions such as digital taxes, legislation, and rules against US tech companies, while he also threatened export restrictions on tech and chips.

- According to Politico, citing Top Trade MEP Lange, the European Commission is expected to reveal its proposals to lift tariffs on US industrial goods and cars.

- South Korean President Lee's office said Lee and US President Trump talked about shipbuilding and that Trump stressed his support for Lee, while it added that the mood from the meeting was good enough that a written joint statement was unnecessary and the meeting was an opportunity for the leaders to get close to each other, rather than discussing the specifics on trade.

- South Korean adviser Wi said details on trade talks still need to be determined and progress has been made on modernising the alliance, while Wi added that Trump and Lee had meaningful talks about nuclear energy.

- Chinese top trade negotiator Li Chenggang is set to head to the US as talks resume and will meet with US Trade Representative Greer and senior Treasury Department officials later this week, according to WSJ. It was later reported that a US government spokesperson said Washington welcomes Chinese efforts to reduce its persistent and massive trade surplus with the US.

- US President Trump’s administration reportedly weighs visa sanctions for EU and EU member state officials over the bloc's digital services act, according to Reuters citing sources.

- Canadian and US officials are to meet after Canada removes some tariffs, according to Bloomberg News.

- Brazil's Foreign Minister Vieira said Canada and the South American bloc Mercosur are to resume negotiations for a free trade agreement, while he added a joint decision was made to resume the negotiations and there will be an important meeting in October regarding Canada-Mercosur talks.

- Indonesia's chief tariff negotiator says the US agrees in principle to exempt palm oil, cocoa and rubber from 19% tariffs.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.7%) began the session on the backfoot and continue to languish around these levels, driven lower by notable underperformance in Paris; France's Government is at risk of collapse after PM Bayrou called for a confidence vote.

- European sectors opened almost entirely in the red and continued their bearish bias throughout the morning. The underperformers are led lower by French heavyweights, hurting the likes of Banks, Construction and Insurance. French listed Socgen, BNP Paribas, Vinci, AXA and Alstom are the underperformers in the CAC, with losses ranging between -8% to -4%.

- US equity futures are mostly lower, led by losses in Europe. RTY underperforms following recent stellar performance, and as global yields rise on French political instability.

- Apple (AAPL) tells Indian government it has no intention of slowing down its expansion in India, is committing an estimated USD 2.5bln to boost iPhone production capacity from over 40mln units annually to around 60mln, India's Economic Times reports

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is steady after Monday's paring of the post-Powell downside. The DXY took a brief leg lower overnight after US President Trump posted a letter removing Fed Governor Cook from her position. If successful, this would put Trump on course for a majority on the Fed board. That being said, Cook has been defiant in stating that she will not resign and that President Trump has no authority to fire her. For today's docket, US durable goods orders and consumer confidence are both due on deck. DXY held above support via its 50DMA at 98.06.

- EUR is resilient despite an unfavourable Eurozone risk backdrop over the past 24 hours. French politics is back in the headlines after French PM Bayrou called for a vote of no confidence on his government's fiscal plans on September 8th. Whilst the EUR is unfazed today, French assets are showing greater concern with the CAC 40 down over 2% and the FR/GE spread at its widest level since April. EUR/USD is back below its 50DMA 1.1651 and towards the bottom end of Monday's 1.1603-1.1723 range.

- JPY is slightly firmer vs. the USD but unable to hold onto the bulk of its APAC gains that were seen as the risk mood soured post-Trump/Cook. A decline in services PPI had little follow-through to the JPY. USD/JPY delved as low as 147.00 overnight, with the pair unable to test its 50DMA to the downside at 146.91.

- GBP is slightly firmer vs. the USD as UK participants return to market after the long weekend. UK traders return to little in the way of positivity however, with the latest BRC shop price data showing that UK food inflation in August rose to its highest level since February 2024. That being said, ING writes that EUR/GBP looks to stay offered this week as French politics prompts some reassessment of long euro exposure. Cable ran out of steam ahead of its 50DMA at 1.3492.

- Antipodeans are both are marginally weaker vs. the USD alongside the downbeat risk tone. There was little follow-through into AUD from the RBA minutes release, which showed that the board saw a strong case for a 25bps cut in the Cash Rate and judged some further reduction in the Cash Rate is likely needed over the coming year.

- PBoC set USD/CNY mid-point at 7.1188 vs exp. 7.1670 (Prev. 7.1161)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are trading on the back foot today and lower by a handful of ticks, to currently trade in a 111-25+ to 112-03+ range. A tinderbox of catalysts for markets to digest on Monday and overnight, including trade developments and US President Trump’s decision to fire Cook. On the latter, ING highlights that “the US 2-30 year yield curve broke to a new cyclical high overnight at 122bp”, levels not seen since the start of the Russia-Ukraine war. Ahead, some Tier 2 US data, and with more focus on 2yr supply.

- Bunds are outperforming across global paper today, seemingly catching a “safety” bid, following on from the increasing risks of a French government collapse (discussed in OAT section). Currently trading in a 129.15 to 129.45 range, with price action fairly muted throughout the morning.

- OATs are lower today to the tune of around 10 ticks, extending on the prior day’s losses where French paper reacted to PM Bayrou’s calls for a confidence vote – it doesn’t seem likely he will get that (discussed below). In terms of price action today, OATs have traded in a 121.54 to 121.98 range. As it stands, the 10y German-French spread sits at 78.06bps, heading back towards levels seen on Liberation Day. As a reminder, in the prior session the spread widened roughly 4.3bps, a move which has continued slightly to make a total widening of 12.8bps at most (from Monday's open to current).

- Gilts are the clear underperformer today as UK paper returns from holiday, and plays catch-up to the broader losses seen in the prior session. Of course, French/US political uncertainty is factoring, but also as UK fiscal woes gradually come into the forefront of traders’ minds. As it stands, political commentary has been exceptionally downbeat on how Chancellor Reeves will enact her high growth/no tax increase budget this autumn.

- Click for a detailed summary

COMMODITIES

- Crude futures trade with losses near USD 0.90/bbl amid a downbeat mood across global markets, and a broad reversal of geopolitical gains made on Monday as Ukrainian Strikes on a Russian oil terminal did not have a great impact to any barrels.

- Spot gold is boasting gains, and is the clear outperformer in the metals space, with Silver flat and Palladium and Platinum continuing losses. The yellow metal benefits after US President Trump ordered the removal of Fed Governor Lisa Cook, alleging false mortgage statements. XAU/USD is currently trading around 3,375/oz.

- Copper outperforms in the base metals space, as it catches up to Chinese optimism after LME trade was closed on Monday. The industrial metal trades within USD 9,792.35-9,867.38/t parameters.

- Chile's mining regulator added requirements to restart sectors of Codelco's El Teniente copper mine affected by the collapse.

- Shanghai Futures Exchange lowers price limits and trading margins for aluminium alloy futures effective from close of settlement on 28 August

- Click for a detailed summary

NOTABLE DATA RECAP

- UK BRC Shop Price Index YY (Aug) 0.9% vs Exp. 0.9% (Prev. 0.7%)

- French Consumer Confidence (Aug) 87.0 vs. Exp. 89.0 (Prev. 89.0, Rev. 88)

NOTABLE EUROPEAN HEADLINES

- UK think tank Resolution Foundation's analysis highlighted a rapid weakening of the jobs market and warned the UK unemployment rate could hit 5% in the three months to August which would be the highest level since the start of 2021, according to FT.

- French Finance Minister Lombard says certainly not resigned to Government falling on September 8; needs to find path to prepare the 2026 budget which will be a recovery budget.

NOTABLE US HEADLINES

- US President Trump posted on Truth Social a letter removing Fed's Cook from her position with immediate effect.

- Fed's Cook (voter) said no cause exists for her to be fired and she will not resign, while she added that President Trump has no authority to fire her and she will continue to carry out her duties. It was also reported that Bloomberg Intelligence noted that Fed's Cook was likely to challenge the firing and could win reinstatement, while it added that mere allegations of fraud are not enough to meet the cause for removal standard.

- Morgan Stanley expects Fed to cut rates by 25bps in September and December (prev. saw no rate cuts in 2025); now expects 25bps cut in March, June, Sept and Dec in 2026, taking terminal target range to 2.75-3.00%

GEOPOLITICS

MIDDLE EAST

- Australian PM Albanese said the Iranian government directed at least two antisemitic attacks in Australia and the Iranian ambassador will be expelled, while he added that operations at Australia’s embassy in Tehran have been suspended and Australian diplomats are now safe in a third country. Furthermore, the government will legislate to list Iran’s Islamic Revolutionary Guard Corps as a terrorist organisation.

RUSSIA-UKRAINE

- US and Russian government officials have discussed several energy deals on the sidelines of negotiations in August that sought to achieve a peace deal in Ukraine, according to multiple sources, via Reuters; talks included Russia purchases of US equipment

OTHER

- South Korean President Lee said he agreed to work closely with US President Trump for peace in the Korean peninsula and noted that North Korea keeps developing its weapons programme as a result of sanctions. Furthermore, Lee said problems cannot be solved solely by pressuring North Korea and that North Korea reached a stage with capabilities of making 10-20 nuclear weapons per year, while it was separately reported that South Korean President Lee invited US President Trump to APEC to pursue a meeting with North Korean leader Kim, according to Newsis.

- North Korea's military said US-South Korea drills prove a US intention to occupy the Korean peninsula, according to KCNA.

CRYPTO

- Bitcoin is a little lower and hovers around USD 110k whilst Ethereum continues to unwind recent underperformance and holds around USD 4.4k.

APAC TRADE

- APAC stocks traded mostly lower after global markets faded last Friday's post-Powell dovish reaction, while Trump also moved to fire Fed Governor Cook and threatened to impose substantial additional tariffs on countries that do not remove digital taxes and regulations against US tech companies.

- ASX 200 retreated amid a continued deluge of earnings releases including from the likes of Coles and Fortescue.

- Nikkei 225 underperformed with notable weakness seen in power names including TEPCO, and with Nissan pressured as Mercedes-Benz is to offload its 3.8% stake in the Japanese automaker, while participants also digested Services PPI data and Japan's top tariff negotiator is set to travel to the US as early as this week.

- Hang Seng and Shanghai Comp pared early losses and returned to flat territory with some resilience seen after another firm liquidity operation by the PBoC, while it was also reported that China's top trade negotiator Li Chenggang is set to head to the US and will meet with US Trade Representative Greer and senior officials at the Department of the Treasury later this week.

NOTABLE ASIA-PAC HEADLINES

- RBA Minutes from the August meeting stated the board saw a strong case for a 25bps cut in the Cash Rate and judged some further reduction in the Cash Rate is likely needed over the coming year, while the stance of policy was still judged somewhat restrictive and it noted the pace of rate cuts would be determined by incoming data and the balance of global risks. RBA Minutes also stated that the board saw arguments for both a gradual pace of easing and for a faster pace, as well as noted the labour market was still a little tight, inflation remained above the midpoint, and domestic demand was recovering. Furthermore, it said uncertainty about spare capacity and the neutral rate also argued for gradual easing, but faster easing might be needed if the labour market was already in balance, risking inflation undershooting the midpoint.

- Japan will invest USD 68bln in India over 10 years including in AI and chips, while India and Japan's PMs intend to revise their countries' joint declaration on security cooperation for the first time in 17 years, according to Nikkei.

- China is to hold an NPC Standing Committee meeting in Beijing from 8-12th September, according to Xinhua.

- Japanese Industry Ministry proposes 5-year corporate tax cut scheme starting FY26 to boost domestic investment, according to Kyodo.

- China's State Council issues guidelines for deep implementation of AI-plus initiatives, targeting full integration by 2027. China to strengthen financial and fiscal support for AI sector, fostering long-term strategic investment.

DATA RECAP

- Japanese Services PPI (Jul) 2.90% (Prev. 3.20%)