Europe Market Open: European stocks set to rebound after several Fed updates & into NVIDIA earnings

27 Aug 2025, 06:50 by Newsquawk Desk

- US President Trump is considering quickly announcing a nominee to replace Fed Governor Cook with Stephen Miran and former World Bank President Malpass potential candidates, according to WSJ citing sources.

- The Trump administration is reviewing options for exerting more influence over the Federal Reserve’s 12 regional banks that would potentially extend its reach beyond personnel appointments in Washington, according to Bloomberg citing sources.

- US President Trump said he is talking about economic sanctions on Russia if there is no ceasefire; US President Trump thinks oil prices will break below USD 60/bbl soon.

- APAC stocks were mostly in the green but with trade rangebound; European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.3% after the cash market closed with losses of 1.1% on Tuesday.

- Looking ahead, highlights include German GfK Consumer Sentiment, Comments from Fed’s Barkin, Supply from UK & US, Earnings from NVIDIA, Snowflake, CrowdStrike, HP Inc. & Kohl's.

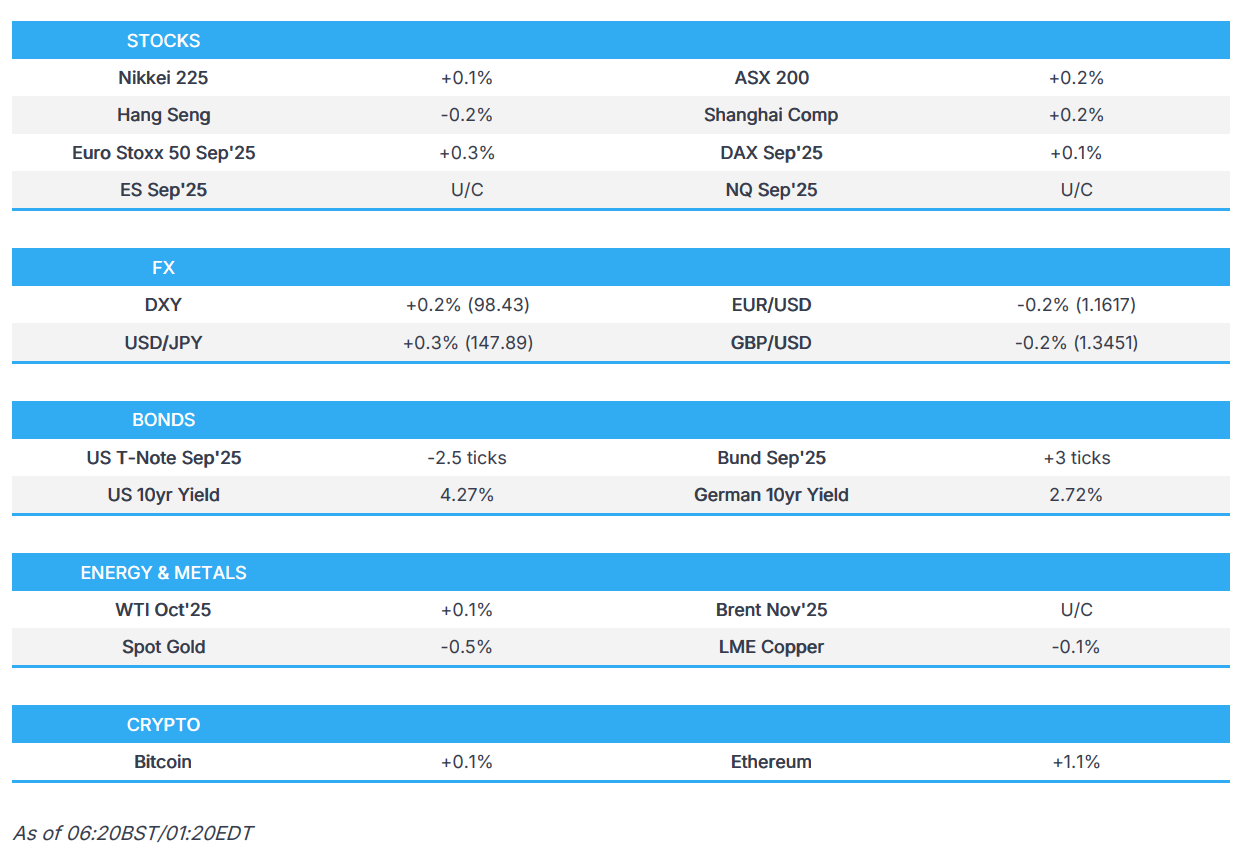

SNAPSHOT

US TRADE

EQUITIES

- US stocks closed higher with outperformance in Industrials, Financials and Tech, while Consumer Staples, Real Estate and Communication lagged, although there was a bout of choppiness in late trade ahead of a last-minute rally as the MSCI August 2025 Index review balance took effect, which might explain some of the volatility.

- Nonetheless, focus was largely on Trump vs the Fed after the US President announced he is firing Cook, albeit she refused and will challenge the decision by Trump. This saw the Dollar sold and the Treasury curve steepen on prospects of a more dovish Fed, which benefited low-yielding currencies like the Franc and Yen.

- SPX +0.40% at 6,465, NDX +0.43% at 23,525, DJI +0.30% at 45,418, RUT +0.81% at 2,358.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said the furniture tariff will be done pretty quickly and will be very substantial, while Trump said the EU, Japan and South Korea trade deals are done and that they kept the same deal with South Korea. It was separately reported that Trump said he is getting on very well with China and President Xi.

- Japan's trade negotiator Akazawa is to visit the US from Thursday to discuss Japan's investment in the US.

NOTABLE HEADLINES

- Fed Discount Rate Minutes stated that Federal Reserve Bank directors noted stable economic conditions, but most also cited concerns about the economic impact of tariffs and about the potential effects of recent legislative changes, especially on the healthcare sector. Some directors observed that despite continuing uncertainty, customers and businesses were cautiously proceeding with investments or other projects, and several directors noted increased pass-through of tariff-related import costs, while comments on labour market conditions were mixed, with some directors noting signs of softening in hiring and others reporting steady activity and resilience.

- Fed's Barkin (2027 voter) warned US workforce growth is basically zero without immigration, while he also commented that his forecast is for a modest adjustment in interest rates, given what he expects will be little variation in economic activity over the remainder of the year but noted the forecast could change.

- Fed spokesperson said Congress, through the Federal Reserve Act, directs that governors serve in long, fixed terms and may be removed by the President only “for cause", while long tenures and removal protections for governors serve as a vital safeguard, ensuring that monetary policy decisions are based on data, economic analysis, and the long-term interests of the American people. The spokesperson added the Federal Reserve will continue to carry out its duties as established by law and Lisa Cook has indicated through her personal attorney that she will promptly challenge this action in court.

- US President Trump said if Powell gets out quickly, they will have a majority shortly on the Fed and might switch Miran to another longer-term Fed spot, while he added that interest rates must come down for housing costs. Trump said regarding the Fed statement on Cook, that he will abide by the courts, while he earlier commented that they have good people for Fed's Cook replacement and have somebody in mind.

- US President Trump is considering quickly announcing a nominee to replace Fed Governor Cook with Stephen Miran and former World Bank President Malpass potential candidates, according to WSJ citing sources.

- US Senate panel is preparing to hold a hearing next week on Trump's Fed pick Stephen Miran for the seat vacated by former Fed governor Kugler.

- The Trump administration is reviewing options for exerting more influence over the Federal Reserve’s 12 regional banks that would potentially extend its reach beyond personnel appointments in Washington, according to Bloomberg citing sources.

- US Treasury Secretary Bessent said Fed independence comes from a political arrangement, and public trust is the only thing giving the Fed credibility. Bessent added they will see a bigger capex boom from here, and that the Treasury is taking in record tariff revenues.

APAC TRADE

EQUITIES

- APAC stocks were mostly in the green but with trade rangebound amid recent Fed independence concerns and as participants braced for NVIDIA's earnings.

- ASX 200 was kept afloat amid outperformance in the mining and materials industries, although gains are capped by heavy losses in consumer staples and tech, with supermarket operator Woolworths suffering a double-digit percentage drop after it reported a 19% decline in profits.

- Nikkei 225 traded indecisively, swinging between gains and losses before eventually recovering on currency weakness.

- Hang Seng and Shanghai Comp lacked firm conviction as the focus turns to earnings releases with the big banks set to report tomorrow, while participants are also awaiting the resumption of US-China talks later in the week.

- US equity futures traded steadily after yesterday's rebound and as the attention turns to upcoming earnings from NVIDIA.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.3% after the cash market closed with losses of 1.1% on Tuesday.

FX

- DXY eked mild gains after the prior day's marginal losses owing to Fed independence concerns after President Trump moved to fire Fed Governor Cook who will be challenging the attempt in court, while it was also reported that the Trump administration is reviewing options for exerting more influence over the Federal Reserve’s regional banks that would potentially extend its reach beyond personnel appointments in Washington.

- EUR/USD pared recent gains amid a lack of fresh catalysts from the bloc and with France facing political uncertainty.

- GBP/USD marginally softened but remained in tight parameters owing to quiet newsflow and with a sparse data calendar.

- USD/JPY steadily advanced towards the 148.00 handle as the dollar regained poise.

- Antipodeans slightly weakened after AUD/USD failed to sustain the initial knee-jerk uplift seen following hot Monthly CPI data and stronger-than-expected Construction Work which feeds into Australia's GDP data.

- PBoC set USD/CNY mid-point at 7.1108 vs exp. 7.1559 (Prev. 7.1188)

- BoC Governor Macklem said the Bank will not revisit its 2% inflation target for the monetary policy framework review next year. Macklem also stated that steep new US tariffs and the unpredictability of US policy have reduced economic efficiency and increased uncertainty, as well as noted that headwinds that limit supply could mean more upward pressure on inflation going forward.

FIXED INCOME

- 10yr UST futures took a breather following the recent bull steepening that was spurred by President Trump's move to fire Fed Governor Cook although questions remain on the legality of the move which sets up a historic legal battle.

- Bund futures lingered around the prior best levels but with further upside capped by resistance around the 129.50 level and with a light calendar ahead for Europe aside from German GfK Consumer Confidence data.

- 10yr JGB futures edged marginally amid the indecisive risk appetite and lack of data from Japan.

COMMODITIES

- Crude futures were constrained after retreating throughout the prior day and with demand not helped by the narrower-than-expected headline crude draw in private sector inventory data, while there were also bearish views on oil including from US President Trump who thinks oil will fall beneath the USD 60/bbl level soon and with Goldman Sachs forecasting Brent to decline to the low USD 50s by late 2026.

- US President Trump thinks oil prices will break below USD 60/bbl soon.

- US Private Energy Inventories (bbls): Crude -1.0mln (exp. -1.9mln), Distillate -1.5mln (exp. +0.9mln), Gasoline -2.1mln (exp. -2.2mln), Cushing -0.5mln.

- Spot gold pulled back from near the USD 3,400/oz level after advancing yesterday amid a softer dollar.

- Copper futures slightly trickled lower in rangebound traded amid a somewhat tentative mood.

CRYPTO

- Bitcoin saw two-way price action and returned to relatively flat territory after bouncing off support at the USD 111k level.

NOTABLE ASIA-PAC HEADLINES

- Chinese Commerce Ministry official Sheng Qiuping said China is to announce policies to broaden services consumption in September.

DATA RECAP

- Chinese Industrial Profits YY (Jul) -1.5% (Prev. -4.3%)

- Chinese Industrial Profits YTD (Jul) -1.7% (Prev. -1.8%)

- Australian Weighted CPI YY (Jul) 2.8% vs. Exp. 2.3% (Prev. 1.9%)

- Australian Annual Trimmed Mean CPI YY (Jul) 2.70% (Prev. 2.10%)

- Australian Construction Work Done (Q2) 3.0% vs. Exp. 0.7% (rev. 0.0%)

GEOPOLITICS

MIDDLE EAST

- US special envoy Witkoff said they are negotiating multiple entries into peace accords with Israel, while Witkoff said President Trump will chair a meeting on Gaza at the White House on Wednesday.

- US Secretary of State Rubio is to meet with Israeli Foreign Minister Sa'ar at the State Department on Wednesday.

- Hamas said all Palestinians killed by Israel in Gaza’s Nasser Hospital attack on Monday were civilians and that two of the six Palestinians identified by Israel as alleged militants were killed in separate attacks away from the hospital.

- Iran's Foreign Ministry spokesperson said Tehran and the E3 will continue nuclear talks in the coming day and noted that Tehran's demands regarding lifting of sanctions and nuclear rights were clearly and explicitly conveyed to the E3 during the meeting, while it warned the E3 over potential consequences of reviving the nuclear deal's snapback mechanism.

- IAEA Director General Grossi has been receiving round-the-clock protection for weeks following a specific Iranian threat, with Tehran accusing IAEA's Grossi of helping spark Israel's June attack, according to WSJ.

RUSSIA-UKRAINE

- US President Trump said he is talking about economic sanctions on Russia if there is no ceasefire.

- US special envoy Witkoff said he is meeting with Ukrainians in New York this week and that Russian President Putin made a good-faith effort to engage.

EU/UK

NOTABLE HEADLINES

- EU is preparing emergency measures to support the ailing aluminium industry amid recycling plants in the bloc shutting down capacity due to US producers paying more for European scrap metal, according to FT.

- SNB's Martin said the SNB does not see a risk of deflationary developments and forecasts show a jump in inflation in coming quarters, adds inflation dynamics in Switzerland should not be dramatically disrupted by recent dollar movements. Martin added the current Swiss franc value is more due to dollar weakness than franc strength, but forex market interventions may be necessary to ensure price stability. The SNB currently has no reason to increase or reduce gold holdings. The bar for taking rates into negative territory is higher than for cutting rates when above zero.