US Market Open: DXY firmer & USTs contained in quiet trade ahead of NVIDIA earnings

27 Aug 2025, 11:15 by Newsquawk Desk

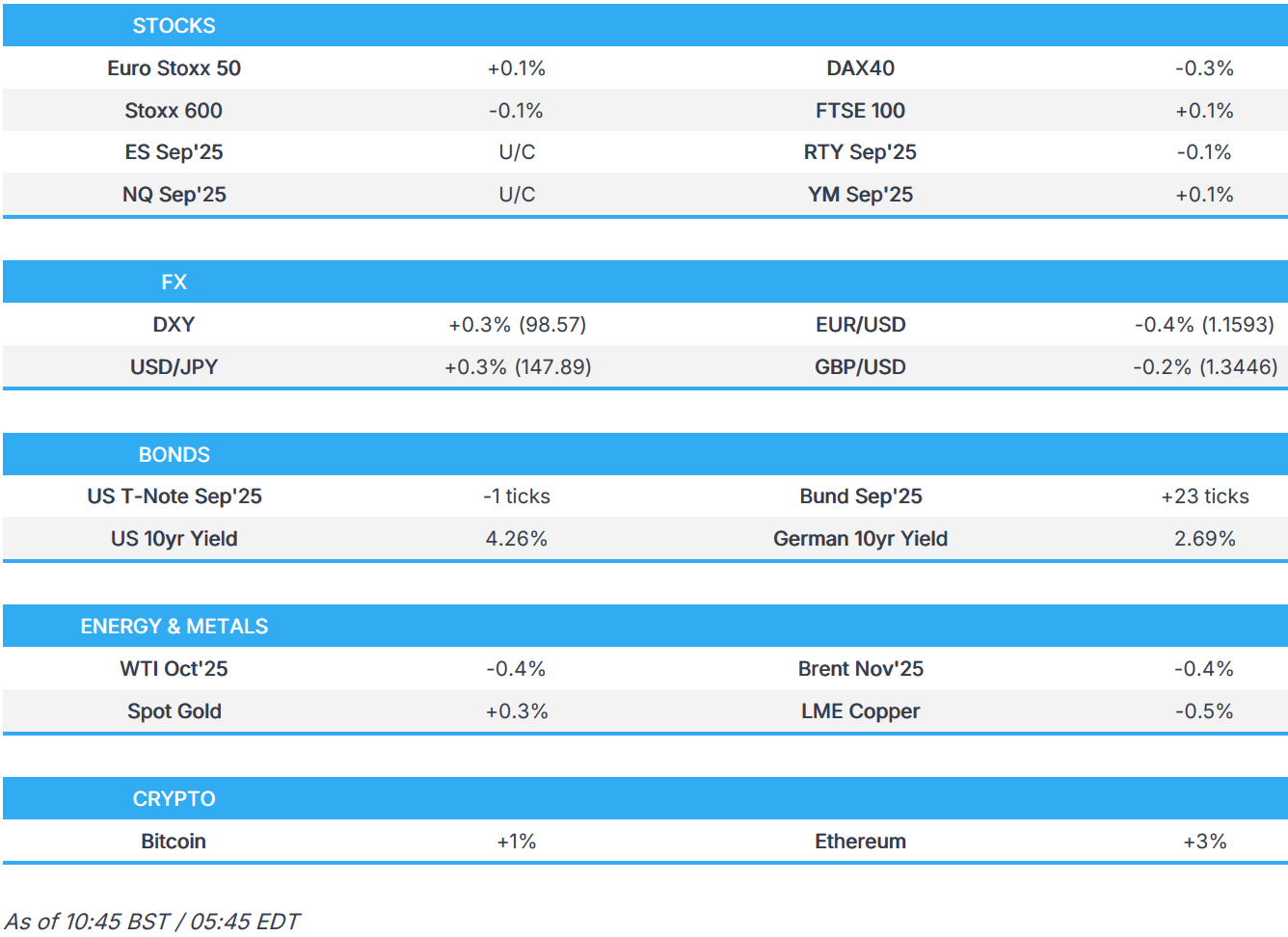

- European bourses opened mostly firmer but now display a mixed picture; NVDA +0.5% into earnings.

- DXY rises following prior day's losses and risk aversion; Aussie fails to benefit from earlier upside post-CPI.

- USTs steady, Bunds/Gilts are bid albeit with little newsflow, but as the risk tone dipped a touch.

- Industrials trade softer on risk aversion, gold holds its ground despite Dollar strength.

- Looking ahead, Comments from Fed’s Barkin, Supply from the US, Earnings from NVIDIA, Snowflake, CrowdStrike, HP Inc. & Kohl's.

TRUMP VS FED

- US President Trump is considering quickly announcing a nominee to replace Fed Governor Cook with Stephen Miran and former World Bank President Malpass potential candidates, according to WSJ citing sources.

- US Senate panel is preparing to hold a hearing next week on Trump's Fed pick Stephen Miran for the seat vacated by former Fed governor Kugler.

- The Trump administration is reviewing options for exerting more influence over the Federal Reserve’s 12 regional banks that would potentially extend its reach beyond personnel appointments in Washington, according to Bloomberg citing sources.

TARIFFS/TRADE

- Japan's trade negotiator Akazawa is to visit the US from Thursday to discuss Japan's investment in the US.

- Spanish Government told Politico its digital tax “applies equally to all large digital companies, regardless of their country of origin. Our commitment is to fair and effective taxation of the digital economy.”

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 U/C) opened modestly firmer across the board, but sentiment did dip a little bit off best levels to currently show a mixed picture.

- European sectors hold a slight positive bias. Consumer Products takes the top spot joined thereafter by Healthcare whilst Banks lag; the latter pressured by Commerzbank (-2.6%) and Deutsche Bank (-2.5%) after the pair received broker downgrades.

- US equity futures are mixed/flat, with the ES and NQ trading around the unchanged mark whilst the RTY lags a touch. All focus will be on NVIDIA results after-hours, shares are currently higher by around 0.5% in pre-market trade.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is on a firmer footing and continuing to gain this morning amid a weaker EUR (see below) and following the prior day's marginal losses owing to Fed independence concerns after President Trump moved to fire Fed Governor Cook who will be challenging the attempt in court. On top of that, it was also reported that the Trump administration is reviewing options for exerting more influence over the Federal Reserve’s regional banks that would potentially extend its reach beyond personnel appointments in Washington. DXY trades in a 98.24-98.70 range.

- EUR/USD pared recent gains amid a lack of fresh catalysts from the bloc and with France facing political uncertainty. Losses accumulated for the EUR despite a lack of headlines around the European equity open, with market contacts noting of potential stops tripped under 1.1600 after the pair found support near the level in the prior two session. German GfK Consumer Sentiment did little to sway the EUR at the time, which printed below expectations. EUR/USD currently sits in a 1.1578-1.1651 range.

- USD/JPY steadily advanced towards the 148.00 handle as the dollar regained poise with newsflow on the lighter end, but the pair influenced by a rebound in the Buck. USD/JPY trades in a 147.29-147.97 range.

- GBP is softer amid the firmer Dollar but losses cushioned by a weaker EUR. On the inflation front, UK's Ofgem raises energy price cap by 2% for Oct-Dec (vs exp. 1% by forecaster Cornwall Insight). The price cap limits the amount suppliers can charge per unit of energy and is revised every three months. Cable trades in a 1.3431-1.3482 parameter and sandwiched between its 50 DMA (1.3493) and 100 DMA (1.3436).

- AUD/USD failed to sustain the initial knee-jerk uplift seen following hot Monthly CPI data and stronger-than-expected Construction Work which feeds into Australia's GDP data.

- PBoC set USD/CNY mid-point at 7.1108 vs exp. 7.1559 (Prev. 7.1188)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs traded with a negative bias earlier but caught a slight bid as the risk tone deteriorated a touch; in a very narrow 112-02+ to 112-06+ range. Price action overnight was lacklustre, as US paper took a breather following the bull steepening seen on Tuesday, spurred by US President Trump’s move to oust Fed Governor Cook. Today’s session has seen yields rise across the curve, generally to a similar degree. Recent newsflow has not really had too much of an impact on price action today; US President Trump is considering quickly announcing a nominee to replace Fed Governor Cook with Stephen Miran and former World Bank President Malpass potential candidates, according to WSJ citing sources.

- Bunds are outperforming vs peers; initial trade was sloppy in-fitting with global peers but has recently picked up a little to trade higher by a handful of ticks. Currently trading at the upper end of a 129.33 to 129.71 range. The docket is void of any pertinent European data/ECB speakers. German GfK earlier saw sentiment drop a little from the prior, and more than expected. Germany's new 2032 line which was very weak, had little impact on price action.

- Gilt price action today has been dictated by global peers; initially opened lower amid the subdued trade seen in USTs/Bunds, but then reversed, but without a clear driver. Currently higher by around 17 ticks, and trades in a 90.26-62 range.

- UK sells GBP 5bln 4.375% 2028 Gilt: b/c 3.16x (prev. 3.71x), average yield 3.991% (prev. 3.941%) & tail 0.2bps (prev. 0.2bps).

- Germany sells EUR 2.675bln vs exp. EUR 4.0bln 2.50% 2032 Bund: b/c 1.2x, average yield 2.46% and retention 33.13%.

- Click for a detailed summary

COMMODITIES

- Crude futures have tilted lower following a flat overnight session and after retreating throughout the prior day and with demand not helped by the narrower-than-expected headline crude draw in private sector inventory data, while there were also bearish views on oil including from US President Trump who thinks oil will fall beneath the USD 60/bbl level soon and with Goldman Sachs forecasting Brent to decline to the low USD 50s by late 2026. WTI currently resides in a 62.99-63.46/bbl range while Brent sits in a USD 66.40-66.91/bbl range.

- Spot gold pulled back from near the USD 3,400/oz level after advancing yesterday amid a softer dollar. The yellow metal has been unfazed by the recent bout of Dollar strength, suggesting deteriorating risk across the market. Spot gold trades in a USD 3,373.78-3,393.55/oz parameter within Tuesday's 3,351.33-3,393.75/oz range.

- Softer trade across base metals amid the deteriorating risk and broader Dollar strength. 3M LME copper resides in a USD 9,785.00-9,865.00/t range.

- US President Trump thinks oil prices will break below USD 60/bbl soon.

- US Private Energy Inventories (bbls): Crude -1.0mln (exp. -1.9mln), Distillate -1.5mln (exp. +0.9mln), Gasoline -2.1mln (exp. -2.2mln), Cushing -0.5mln.

- Kazakhstan holds talks to resume oil transit via BTC, according to Tass citing the energy ministry; oil supplies to Europe are proceeding without delays.

- Two Chinese investors are interested in taking a stake in Vietnam’s largest tungsten business, via Reuters citing sources.

- Ukraine's Energy Ministry said Russia attacked energy and gas transit infrastructure in six Ukrainian regions overnight.

- Click for a detailed summary

NOTABLE EUROPEAN HEADLINES

- UK's Ofgem raises energy price cap by 2% for Oct-Dec (vs exp. 1% by forecaster Cornwall Insight).

- EU is preparing emergency measures to support the ailing aluminium industry amid recycling plants in the bloc shutting down capacity due to US producers paying more for European scrap metal, according to FT.

- SNB's Martin said the SNB does not see a risk of deflationary developments and forecasts show a jump in inflation in coming quarters, adds inflation dynamics in Switzerland should not be dramatically disrupted by recent dollar movements. Martin added the current Swiss franc value is more due to dollar weakness than franc strength, but forex market interventions may be necessary to ensure price stability. The SNB currently has no reason to increase or reduce gold holdings. The bar for taking rates into negative territory is higher than for cutting rates when above zero.

- UK ONS said June 2025 Producer output Price inflation estimated to be -1.0% Y/Y.

NOTABLE DATA RECAP

- German GfK Consumer Sentiment (Sep) -23.6 vs. Exp. -22.0 (Prev. -21.5, Rev. -21.7); German consumers’ inflation expectations rose for the second month in a row in August.

NOTABLE US HEADLINES

GEOPOLITICS

MIDDLE EAST

- US special envoy Witkoff said they are negotiating multiple entries into peace accords with Israel, while Witkoff said President Trump will chair a meeting on Gaza at the White House on Wednesday.

- US Secretary of State Rubio is to meet with Israeli Foreign Minister Sa'ar at the State Department on Wednesday.

- Hamas said all Palestinians killed by Israel in Gaza’s Nasser Hospital attack on Monday were civilians and that two of the six Palestinians identified by Israel as alleged militants were killed in separate attacks away from the hospital.

- WSJ's Norman posts "If SnapBack happens this week, very strong odds it happens tomorrow"; in relation to the Iranian snapback mechanism. "If no SnapBack, either things change dramatically or extension. Odds of dropping SnapBack without extension are tiny at this point. There is still a very real possibility that SnapBack triggered but extension agreed during 30-day process. Depends on Iran".

RUSSIA-UKRAINE

- US special envoy Witkoff said he is meeting with Ukrainians in New York this week and that Russian President Putin made a good-faith effort to engage.

- "Moscow: No agreement yet to upgrade the level of Russian and Ukrainian negotiating delegations", according to Al Arabiya.

- Ukrainian President Zelensky said Russians are currently sending negative signals regarding meetings and further developments.

CRYPTO

- Bitcoin is a little firmer today and trades around USD 110k whilst Ethereum outperforms a touch to trade above USD 4.5k.

APAC TRADE

- APAC stocks were mostly in the green but with trade rangebound amid recent Fed independence concerns and as participants braced for NVIDIA's earnings.

- ASX 200 was kept afloat amid outperformance in the mining and materials industries, although gains are capped by heavy losses in consumer staples and tech, with supermarket operator Woolworths suffering a double-digit percentage drop after it reported a 19% decline in profits.

- Nikkei 225 traded indecisively, swinging between gains and losses before eventually recovering on currency weakness.

- Hang Seng and Shanghai Comp lacked firm conviction as the focus turns to earnings releases with the big banks set to report tomorrow, while participants are also awaiting the resumption of US-China talks later in the week.

NOTABLE ASIA-PAC HEADLINES

- Chinese Commerce Ministry official Sheng Qiuping said China is to announce policies to broaden services consumption in September.

- Mitsubishi Motor (7211 JT) cuts guidance (JPY): net seen at 10bln (prev. 40bln); operating at 70bln (prev. 100bln), recurring 60bln (prev. 90bln); Co. cites US tariffs, decline in sales volume, increase in selling expenses, competition, inflation.

DATA RECAP

- Chinese Industrial Profits YY (Jul) -1.5% (Prev. -4.3%)

- Chinese Industrial Profits YTD (Jul) -1.7% (Prev. -1.8%)

- Australian Weighted CPI YY (Jul) 2.8% vs. Exp. 2.3% (Prev. 1.9%)

- Australian Annual Trimmed Mean CPI YY (Jul) 2.70% (Prev. 2.10%)

- Australian Construction Work Done (Q2) 3.0% vs. Exp. 0.7% (rev. 0.0%)