Europe Market Open: NVIDIA beats on top and bottom line, shares fall -3% on revenue guidance

28 Aug 2025, 06:50 by Newsquawk Desk

- US Treasury Secretary Bessent reiterated that there are 11 strong Fed chair candidates, while he added they will start interviews after Labor Day and present a shortlist to President Trump.

- NVIDIA (-3.1%) shares were pressured post-earnings despite beating on top and bottom lines, as its revenue guidance was not as strong as some were hoping for and with questions remaining regarding chip sales to China.

- White House trade advisor Navarro said India can get 25% off tariffs if it stops buying Russian oil.

- APAC stocks were predominantly higher but with mixed trade seen throughout the session; European equity futures indicate a flat/mildly higher cash market open with Euro Stoxx 50 futures up 0.1% after the cash market finished with gains of 0.2% on Wednesday.

- Looking ahead, highlights include Swiss GDP (Q2), EZ Sentiment Survey (Aug), US GDP 2nd Estimate (Q2), PCE (Q2), Jobless Claims, ECB Minutes, Speech from Fed’s Waller, Supply from Italy & US, Earnings from Marvell, Dell, ULTA Beauty, Best Buy & Pernod Ricard.

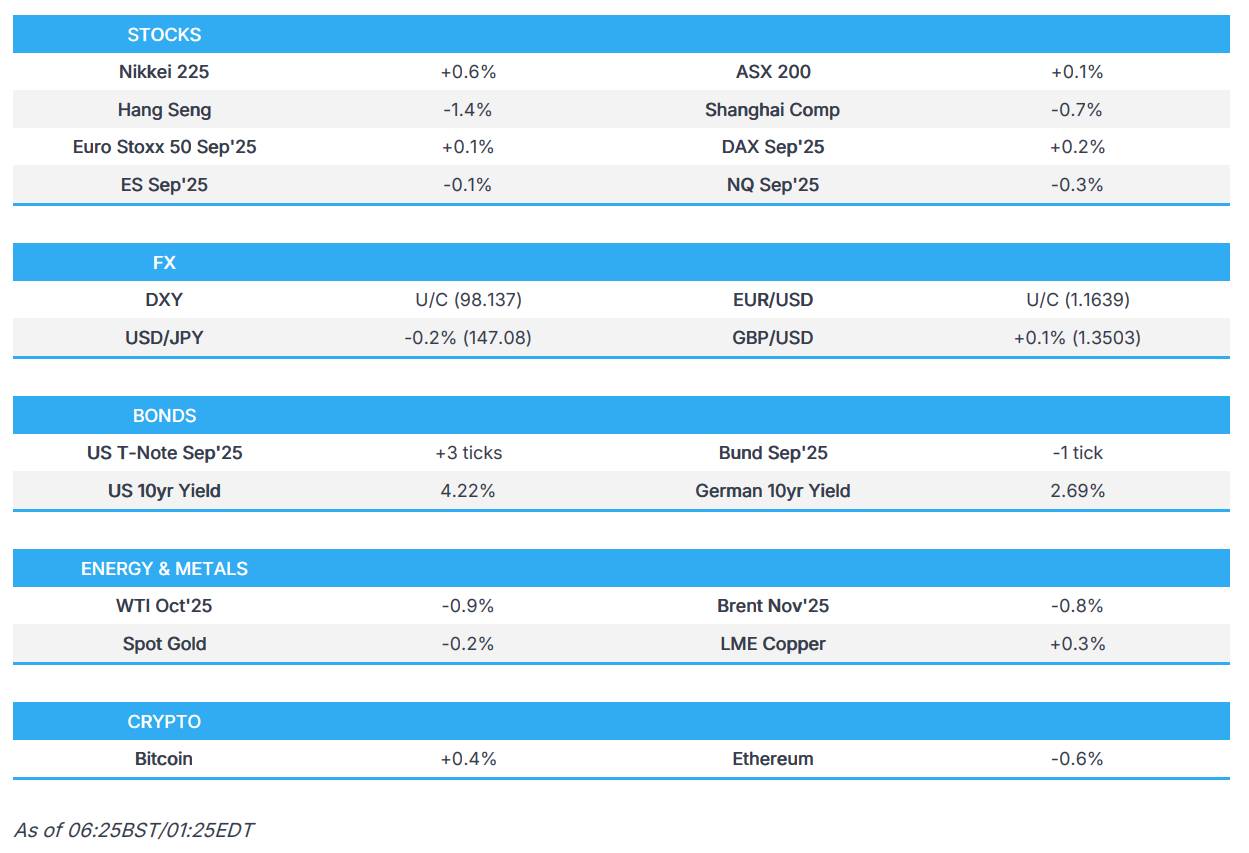

SNAPSHOT

US TRADE

EQUITIES

- US stocks were ultimately bid in which the Russell 2000 outperformed and the S&P 500 printed a fresh intraday record high, while sectors were predominantly firmer with Energy leading the advances, although Communication lagged. Tech was also bid ahead of NVDA earnings after-hours, and T-notes continued to steepen with focus on Fed independence, while there were comments from Fed Williams who was somewhat dovish and thinks that it will be appropriate to reduce rates over time but will have to watch the data.

- Nonetheless, futures briefly wobbled after-hours as NVIDIA shares were pressured post-earnings despite beating on top and bottom lines, as its revenue guidance was not as strong as some were hoping for and with questions remaining regarding chip sales to China.

- SPX +0.24% at 6,481, NDX +0.17% at 23,566, DJI +0.32% at 45,565, RUT +0.64% at 2,374.

- Click here for a detailed summary.

TARIFFS/TRADE

- White House trade advisor Navarro said India can get 25% off tariffs if it stops buying Russian oil.

- India's government decided to extend the import duty exemption on cotton from September 30th to December 31st this year.

- Japanese government source said Japan's top trade negotiator Akazawa cancelled his US trip and eyes a visit as early as next week.

- Mexico's government plans to increase tariffs on China as part of its 2026 budget proposal next month with tariff hikes expected on imports from China, including cars, textiles and plastics, according to Bloomberg.

- China's top trade negotiator Li Chenggang co-chaired the Joint Economic and Trade Committee in Ottawa, while MOFCOM noted that China and Canada had frank and pragmatic and constructive exchanges on improving and developing bilateral economic and trade relations. MOFCOM also stated that both sides agreed to follow-up communication and that China is ready to manage differences through constructive methods and pragmatic actions.

NOTABLE HEADLINES

- US Vice President Vance said Fed's Cook does not meet the standard and President Trump can legally fire Cook.

- White House Trade Advisor Navarro said it appears to be a slam dunk case against Fed's Cook, while he added this is due process and that Cook weaponised the Fed.

- US Treasury Secretary Bessent reiterated that there are 11 strong Fed chair candidates, while he added they will start interviews after Labor Day and present a shortlist to President Trump.

- NVIDIA Corp (NVDA) Q2 2026 (USD): Adj. EPS 1.05 (exp. 1.00), Revenue 46.74bln (exp. 45.51bln). Q3 revenue view 54bln (exp. 53bln), announces additional USD 60bln buyback. Co. said in its earnings call that US government officials expressed expectation that the government will receive 15% of revenue generated from licensed H20 sales, but added that any request for a percentage of revenue may subject them to litigation and increase their costs. Furthermore, it stated the US has not published a regulation codifying such a requirement that the US government will get 15% of revenue generated from licensed H20 sales. Co. shares fell 3.2% after-market.

APAC TRADE

EQUITIES

- APAC stocks were predominantly higher but with mixed trade seen throughout the session as risk appetite was clouded post-NVIDIA earnings despite the AI darling beating on top of bottom lines, with investors wary as guidance was not as strong as some had hoped and questions remained regarding China chip sales.

- ASX 200 lacked conviction amid another deluge of earnings and with sentiment not helped by disappointing capex data.

- Nikkei 225 edged higher but with price action indecisive after Japan's top trade negotiator postponed a planned US trip.

- Hang Seng and Shanghai Comp traded mixed with underperformance seen in Hong Kong following recent earnings including Meituan which reported a substantial drop in profits, while participants look ahead to results from China's largest lenders.

- US equity futures nursed some of the losses seen in the aftermath of NVIDIA's earnings after wobbling on guidance and China sales uncertainty.

- European equity futures indicate a flat/mildly higher cash market open with Euro Stoxx 50 futures up 0.1% after the cash market finished with gains of 0.2% on Wednesday.

FX

- DXY traded little changed after the previous day's ultimately flat performance as data and market-moving events for the buck were sparse, while the attention now turns to incoming US data including GDP and Initial Jobless Claims scheduled today, followed by the latest PCE data on Friday.

- EUR/USD eked slight gains after yesterday's intraday recovery and rebound from a brief dip beneath the 1.1600 handle, while there is a slew of incoming sentiment surveys from the bloc, as well as the ECB Minutes from the July conclave.

- GBP/USD edged marginally higher after reclaiming the 1.3500 status but with upside capped amid quiet newsflow.

- USD/JPY struggled for direction after recent fluctuations and amid the indecisive risk appetite in Japan, while comments from BoJ's Nakagawa garnered very little reaction as she reiterated the BoJ will continue to raise the interest rate if the outlook for economic activity and prices is realised.

- Antipodeans remained mildly firmer against the dollar after the PBoC continued to strengthen the yuan reference rate, with the currencies unfazed by weaker-than-expected Australian private capex data and mixed New Zealand business surveys.

- PBoC set USD/CNY mid-point at 7.1063 vs exp. 7.1479 (Prev. 7.1108)

- PBoC extended bilateral currency swap agreement with the RBNZ for five years.

FIXED INCOME

- 10yr UST futures took a breather after the prior day's continued bull steepening alongside the ongoing Trump vs Fed debacle, while further upside was limited ahead of supply including a 7-year note auction stateside.

- Bund futures held on to recent spoils after yesterday's whipsawing and eventual rebound, while participants look ahead to the release of several confidence surveys from the bloc and the ECB Minutes.

- 10yr JGB futures initially tracked the recent upside in global peers but then faded some of the gains after a dismal 2yr JGB auction which resulted in the weakest demand ratio since 2009.

COMMODITIES

- Crude futures gradually pulled back overnight amid a lack of energy-specific drivers and after having gained yesterday amid anticipation of further sanctions on Iran and following a larger-than-expected weekly EIA headline crude draw.

- Spot gold trickled lower after the prior day's intraday rebound was stalled by resistance near the USD 3,400/oz level.

- Copper futures traded sideways with demand constrained after this week's declines and amid the mixed risk appetite.

CRYPTO

- Bitcoin gradually edged higher and returned to above the USD 112k level.

NOTABLE ASIA-PAC HEADLINES

- China issued plans to stabilise growth in the steel sector between 2025 and 2026, while it aims to speed up production commencement, capacity and output expansion for key domestic iron ore projects. Furthermore, China will enhance management of steel exports and will promote the reduction of steel output.

- BoK maintained the Base Rate at 2.50%, as expected, with the decision not unanimous as board member Shin Sung-hwan dissented and saw a need to cut rates to aid growth. BoK said domestic demand is expected to sustain a modest recovery and it will maintain a rate cut stance to mitigate downside risks to economic growth, while it will adjust the timing and pace of any further base rate cuts. BoK Governor Rhee stated that a majority of the seven-member board assessed there is a need to work in tandem with government policies to stabilise local property prices, as well as noted that five board members said the door for an imminent rate cut should be open and one board member said the current policy rate should be maintained for the next three months. Furthermore, Rhee said the easing stance will stay through at least the first half of next year and it is difficult to comment on the terminal policy rate, but added that faster policy rate easing risks overstimulating the local property market at this stage.

DATA RECAP

- Australian Capital Expenditure (Q2) 0.2% vs. Exp. 0.7% (Prev. -0.1%)

- New Zealand ANZ Business Outlook (Aug) 49.7% (Prev. 47.8%)

- New Zealand ANZ Own Activity (Aug) 38.7% (Prev. 40.6%)

GEOPOLITICS

MIDDLE EAST

- Israel launched a series of strikes on former army barracks in the southwestern Damascus countryside, while a Syrian army source said the Israeli army landed a special force in a strategic hilltop southwest of the Damascus area in a two-hour operation.

RUSSIA-UKRAINE

- EU is reportedly considering secondary sanctions to hit Russia's war effort with EU foreign ministers to meet in Copenhagen later this week and are expected to have a discussion on a range of options, according to Bloomberg.

EU/UK

NOTABLE HEADLINES

- UK Treasury is said to be considering a tax hike on landlords by imposing national insurance on rental income ahead of Chancellor Reeves’ autumn budget, according to The Times.