US Market Open: NVIDIA -1.7% post earnings after Q3 rev. guidance & China risks; US GDP/PCE (Q2) due

28 Aug 2025, 11:25 by Newsquawk Desk

- European bourses erase early morning strength; NVIDIA (-1.9% pre-market) post-earnings.

- NVIDIA shares are pressured in pre-market trade despite beating on top and bottom lines, as its revenue guidance was not as strong as some were hoping for and with questions remaining regarding chip sales to China.

- USD is flat in quiet trade as FX majors trade in narrow ranges awaiting the next catalyst.

- Bonds see lacklustre trade in quiet newsflow as USTs eye 7yr supply and data.

- Crude choppy, gold on either side of USD 3,400/oz, base metals are mixed in narrow ranges.

- Looking ahead, US GDP 2nd Estimate (Q2), PCE (Q2), Jobless Claims, ECB Minutes, Speech from Fed’s Waller, Supply from the US, Earnings from Marvell, Dell, ULTA Beauty, Best Buy.

LOOKING AHEAD

- Looking ahead, highlights include US GDP 2nd Estimate (Q2), PCE (Q2), Jobless Claims, ECB Minutes, Speech from Fed’s Waller, Supply from the US, Earnings from Marvell, Dell, ULTA Beauty, Best Buy.

- Click for the Newsquawk Week Ahead.

TARIFFS/TRADE

- Chinese Commerce Ministry confirms trade negotiator Li Chenggang will travel to Washington for meetings with US officials.

EUROPEAN TRADE

EQUITIES

- European bourses opened firmer, initially edging higher throughout the morning but have since reversed, which coincided with the US pre-market open.

- European sectors began the session almost entirely in positive territory, though have since moved to show a mixed picture as stocks wane a little. Consumer products and services at the top of the pile, helped by Luxury strength. LVMH (+3.5%), Hermes (+1.7%), Swatch (+2.3%).

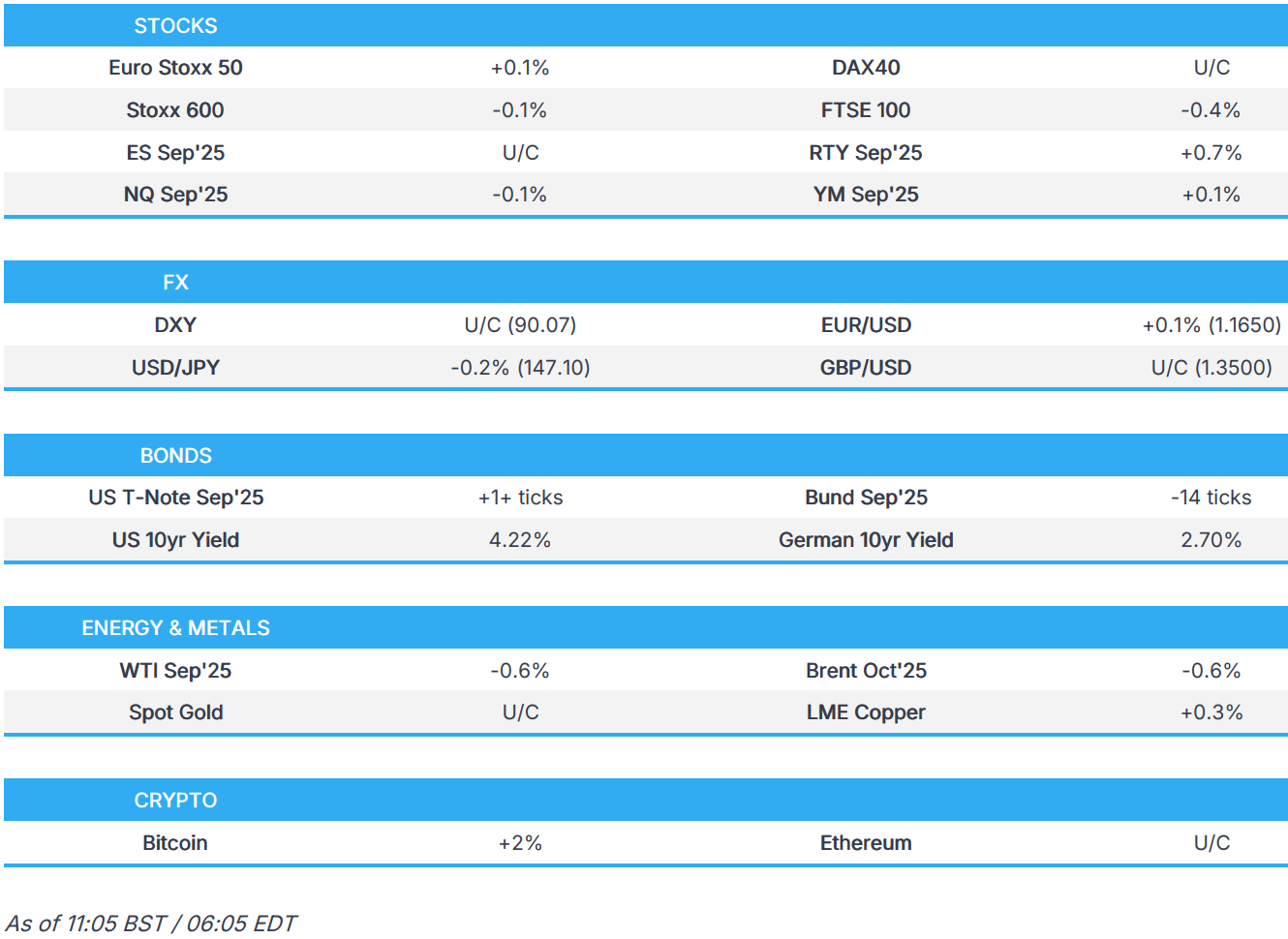

- US equity futures are mixed with the ES/NQ essentially flat whilst the RTY outperforms, building on the prior day's strength. All focus on NVIDIA (-1.9% pre-market), which moves lower after it beat on its top and bottom lines, but with focus on the outlook forecast, which was not as strong as some had expected; Q3 rev. guided at USD 53bln vs some expectations as high as USD 60bln.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY remains confined to a tight range after trading little changed overnight and following the previous day's ultimately flat performance as data and market-moving events for the buck were sparse. Focus today on US data, which includes GDP/PCE (Q2) and Jobless Claims. DXY currently resides in a narrow 98.05-98.21 parameter.

- EUR/USD is moving in tandem with the buck after yesterday's intraday recovery and rebound from a brief dip beneath the 1.1600 handle. There has been little in terms of fresh updates from the French political debacle. French Finance Minister Lombard said the public deficit will be on target in 2025, 2026 budget is almost ready, the text that gets voted will be the "fruit of compromise". EUR/USD resides in a current 1.1631-1.1654 range at the time of writing

- USD/JPY oscillates within a narrow band and struggles for a clear direction after recent fluctuations and amid the indecisive risk appetite in Japan. Comments from BoJ's Nakagawa garnered very little reaction as she reiterated the BoJ will continue to raise the interest rate if the outlook for economic activity and prices is realised. USD/JPY bounced off levels near its 50 DMA (146.98) this morning, notching a current range between 147.01-147.49.

- GBP/USD at the whim of the dollar, having briefly reclaimed 1.3500 status in the overnight session but with upside capped amid quiet newsflow. Aside from that, data and speakers remain on the quieter side for GBP, with Cable currently on either side of its 50 DMA (1.3493) in a 1.3484-1.3518.

- Antipodeans hold a mild upward bias against the dollar in quiet newsflow. Strength was seen overnight after the PBoC continued to strengthen the yuan reference rate.

- PBoC set USD/CNY mid-point at 7.1063 vs exp. 7.1479 (Prev. 7.1108)

- PBoC extended bilateral currency swap agreement with the RBNZ for five years.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are firmer by a handful of ticks, with a slight bid caught soon after the European equity cash open, but seemingly without a fresh driver. Currently trading towards the upper end of a 112-12 to 112-17+ range. Peak for the day marks the weekly high, now currently trading at levels not seen since 1st May 2025 (112-23 was the best from that day). On the data front, markets will have US GDP 2nd Estimate (Q2), PCE (Q2) and Jobless Claims to digest. As for supply, a 7yr auction is on the docket, which follows on from a strong 2yr on Tuesday but a mixed 5yr outing on Wednesday.

- Bunds are slightly lower in what has been a very choppy trade so far. Caught a bid soon after the European cash open, which saw Bunds make a fresh WTD high at 129.90; next level to the upside includes the round 130.00 mark and then 130.06 (Aug 14th high).

- On Wednesday, German-French spreads widened to as high as 81.89 – approaching the high of this year at 84.5bps. Today, yields are tightening a touch back down below 80.00. Most recently, the French Finance Minister said the public deficit will be on target in 2025 and 2026, and the budget is almost ready. Adding that the budget we are preparing does not have a surtax on big companies.

- Gilts marginally outperform today, gapped higher at the open, by around 20 ticks before paring some of that move. Markets have an interesting report via The Times to digest; the UK Treasury is said to be considering a tax hike on landlords by imposing national insurance on rental income ahead of Chancellor Reeves’ autumn budget. This report has helped to lift Gilts, but also as UK paper plays catch-up to some of the strength seen in the prior session in USTs after Gilts shut. Gilts trade in a 90.68 to 90.83 range.

- Italy sells EUR 6bln vs exp. EUR 5.25-6.0bln 2.70% 2030, 3.65% 2035, 3.60% 2035 BTP & EUR 1.25bln vs exp. EUR 1.5-2.0bln 2034 CCTeu.

- Click for a detailed summary

COMMODITIES

- Softer trade across crude contracts, although some upside was seen shortly after reports that the EU mission HQ in Kyiv was struck by Russian missiles, although delegate staff are safe according to the European Commission, which prompted an unwind of those earlier modest gains. Some upticks were seen recently alongside reports from IRNA that "It seems that Europe will activate the "snapback" mechanism against Iran this week". WTI currently resides in a 63.48-64.00/bbl range while Brent sits in a USD 67.40-67.48/bbl range.

- Spot gold edges higher in quiet trade to test USD 3,400/oz to the upside with the yellow metal in a USD 3,384.62-3,401.11/oz range at the time of writing. Upward tilt in prices also comes amid narrowing prospects of a Russia-Ukraine peace deal, with both sides still carrying out heavy strikes.

- Flat/mostly firmer trade across base metals with no real conviction amid a tentative Dollar and a similarly non-committal risk tone. 3M LME copper trades in a USD 9,775.75-9,833.00/t range.

- Hungary's MOL says crude supplies have arrived in Hungary and Slovakia after the Druzhba pipeline restarted; Slovak Economy Minister says supplies have resumed to the nation.

- Click for a detailed summary

NOTABLE HEADLINES

- UK Treasury is said to be considering a tax hike on landlords by imposing national insurance on rental income ahead of Chancellor Reeves’ autumn budget, according to The Times.

- ECB's Rehn says EZ growth more resilient than expected, inflation is slowing to below 2% target; consider rapid and significant weakening of USD dominance as unlikely EZ inflation being at 2% target is linked to ECB's independent decision making. US President Trump pressure on Fed could have global effects on markets and real economy. ECB will keep close eye on economy and stand ready to act if needed.

- French Finance Minister Lombard says the public deficit will be on target in 2025, 2026 budget almost ready, text that gets voted will be the "fruit of compromise" Do not see possibility of French financial crisis. Tap the markets regularly, no problem financing economy. Budget we are preparing does not have a surtax on big companies. Everything is up for discussion on the 2026 budget as we reduce the deficit and protect companies.

NOTABLE DATA RECAP

- Swiss GDP QQ (Q2) 0.1% vs. Exp. 0.1% (Prev. 0.5%, Rev. 0.4%); due to value added of the chemical-pharmaceutical industry, -4.8% as a result of falling exports.

- Swiss GDP YY (Q2) 1.2% vs. Exp. 1.4% (Prev. 2.0%, Rev. 1.8%)

- Swedish Overall Sentiment (Aug) 96.0 (Prev. 94.3)

- EU Money-M3 Annual Growth (Jul) 3.4% vs. Exp. 3.5% (Prev. 3.3%)

- Italian Mfg. Business Confidence (Aug) 87.4 vs. Exp. 87.2 (Prev. 87.8, Rev. 87.8); Consumer Confidence (Aug) 96.2 vs. Exp. 96.6 (Prev. 97.2)

- EU Business Climate (Aug) -0.72 (Prev. -0.72, Rev. -0.71); EU Consumer Confid. Final (Aug) -15.5 vs. Exp. -15.5 (Prev. -15.5); EU Economic Sentiment (Aug) 95.2 vs. Exp. 96.0 (Prev. 95.8, Rev. 95.7); EU Industrial Sentiment (Aug) -10.3 vs. Exp. -10.0 (Prev. -10.4, Rev. -10.5); EU Services Sentiment (Aug) 3.6 vs. Exp. 3.9 (Prev. 4.1); EU Selling Price Expec (Aug) 6.7 (Prev. 9.2, Rev. 8.9); EU Cons Infl Expec (Aug) 25.9 (Prev. 25.1)

- Italian Industrial Sales YY WDA (Jun) 0.3% (Prev. -1.8%); Industrial Sales MM SA (Jun) 1.2% (Prev. -2.2%, Rev. -2.1%); Industrial Sales MM SA (Jun) 1.2% (Prev. -2.2%)

NOTABLE US HEADLINES

- US Vice President Vance said Fed's Cook does not meet the standard and President Trump can legally fire Cook.

- White House Trade Advisor Navarro said it appears to be a slam dunk case against Fed's Cook, while he added this is due process and that Cook weaponised the Fed.

- NVIDIA Corp (NVDA) Q2 2026 (USD): Adj. EPS 1.05 (exp. 1.00), Revenue 46.74bln (exp. 45.51bln). Q3 revenue view 54bln (exp. 53bln), announces additional USD 60bln buyback. Co. said in its earnings call that US government officials expressed expectation that the government will receive 15% of revenue generated from licensed H20 sales, but added that any request for a percentage of revenue may subject them to litigation and increase their costs. Furthermore, it stated the US has not published a regulation codifying such a requirement that the US government will get 15% of revenue generated from licensed H20 sales. Co. shares fell 3.2% after-market.

TARIFFS/TRADE

- French President Macron reportedly told his ministers that the EU should consider retaliatory measures against the US digital sector, according to Politico.

- White House trade advisor Navarro said India can get 25% off tariffs if it stops buying Russian oil.

- India's government decided to extend the import duty exemption on cotton from September 30th to December 31st this year.

- Japanese government source said Japan's top trade negotiator Akazawa cancelled his US trip and eyes a visit as early as next week.

- Mexico's government plans to increase tariffs on China as part of its 2026 budget proposal next month with tariff hikes expected on imports from China, including cars, textiles and plastics, according to Bloomberg.

- China's top trade negotiator Li Chenggang co-chaired the Joint Economic and Trade Committee in Ottawa, while MOFCOM noted that China and Canada had frank and pragmatic and constructive exchanges on improving and developing bilateral economic and trade relations. MOFCOM also stated that both sides agreed to follow-up communication and that China is ready to manage differences through constructive methods and pragmatic actions.

GEOPOLITICS

MIDDLE EAST

- Israel says its forces are operating in "all combat zones", after Syrian state media reports a raid by Israeli ground troops on a site it had already bombed outside Damascus, according to AFP.

RUSSIA-UKRAINE

- Russian drones reportedly flying over US weapons routes in Germany, according to officials cited by NYT.

- "European Union announces that its mission headquarters in Kyiv was damaged by the Russian attack", according to Al Arabiya.

- European Commission President von der Leyen says "Delegation staff are safe", in reference to Russian attack which damaged EU mission HQ in Kyiv.

- Ukrainian President Zelensky says Russian attack on Kyiv killed at least eight, including a child, adds the attack demonstrates Russian answer to diplomacy and he called for stronger sanctions against Russia.

- Fire at unit of Afipsky oil refinery in Russia's Krasnodar region extinguished, according to local authorities; Fire broke out following Ukrainian drone strike.

- Ukrainian Energy Ministry says Russia's combined attack damaged energy facilities in several regions.

- EU Diplomat told Politico "Thursday's EU meetings aim to increase the pressure on Russia".

- Ukrainian Air Force says Russia attacked Ukrainian with 598 drones and 31 missiles overnight.

CRYPTO

- Bitcoin is a little firmer today and trades just shy of the USD 113k mark; Ethereum is steady around USD 4.58k.

APAC TRADE

- APAC stocks were predominantly higher but with mixed trade seen throughout the session as risk appetite was clouded post-NVIDIA earnings despite the AI darling beating on top of bottom lines, with investors wary as guidance was not as strong as some had hoped and questions remained regarding China chip sales.

- ASX 200 lacked conviction amid another deluge of earnings and with sentiment not helped by disappointing capex data.

- Nikkei 225 edged higher but with price action indecisive after Japan's top trade negotiator postponed a planned US trip.

- Hang Seng and Shanghai Comp traded mixed with underperformance seen in Hong Kong following recent earnings including Meituan which reported a substantial drop in profits, while participants look ahead to results from China's largest lenders.

NOTABLE ASIA-PAC HEADLINES

- Japan's MOF sounds out dealers of reducing super-long JGBs, according to Nikkei.

- China issued plans to stabilise growth in the steel sector between 2025 and 2026, while it aims to speed up production commencement, capacity and output expansion for key domestic iron ore projects. Furthermore, China will enhance management of steel exports and will promote the reduction of steel output.

- BoK maintained the Base Rate at 2.50%, as expected, with the decision not unanimous as board member Shin Sung-hwan dissented and saw a need to cut rates to aid growth. BoK said domestic demand is expected to sustain a modest recovery and it will maintain a rate cut stance to mitigate downside risks to economic growth, while it will adjust the timing and pace of any further base rate cuts. BoK Governor Rhee stated that a majority of the seven-member board assessed there is a need to work in tandem with government policies to stabilise local property prices, as well as noted that five board members said the door for an imminent rate cut should be open and one board member said the current policy rate should be maintained for the next three months. Furthermore, Rhee said the easing stance will stay through at least the first half of next year and it is difficult to comment on the terminal policy rate, but added that faster policy rate easing risks overstimulating the local property market at this stage.

- BoJ's Nakagawa says will make policy decisions based on hard data, including Tankan survey; risks of being behind the curve not high right now.

- Mainland investors sell a record USD 2.6bln of Hong Kong stocks on Thursday, via Bloomberg.

DATA RECAP

- Australian Capital Expenditure (Q2) 0.2% vs. Exp. 0.7% (Prev. -0.1%)

- New Zealand ANZ Business Outlook (Aug) 49.7% (Prev. 47.8%)

- New Zealand ANZ Own Activity (Aug) 38.7% (Prev. 40.6%)