Europe Market Open: Cautious APAC trade given the US holiday, awaiting trade & Fed updates

02 Sep 2025, 06:50 by Newsquawk Desk

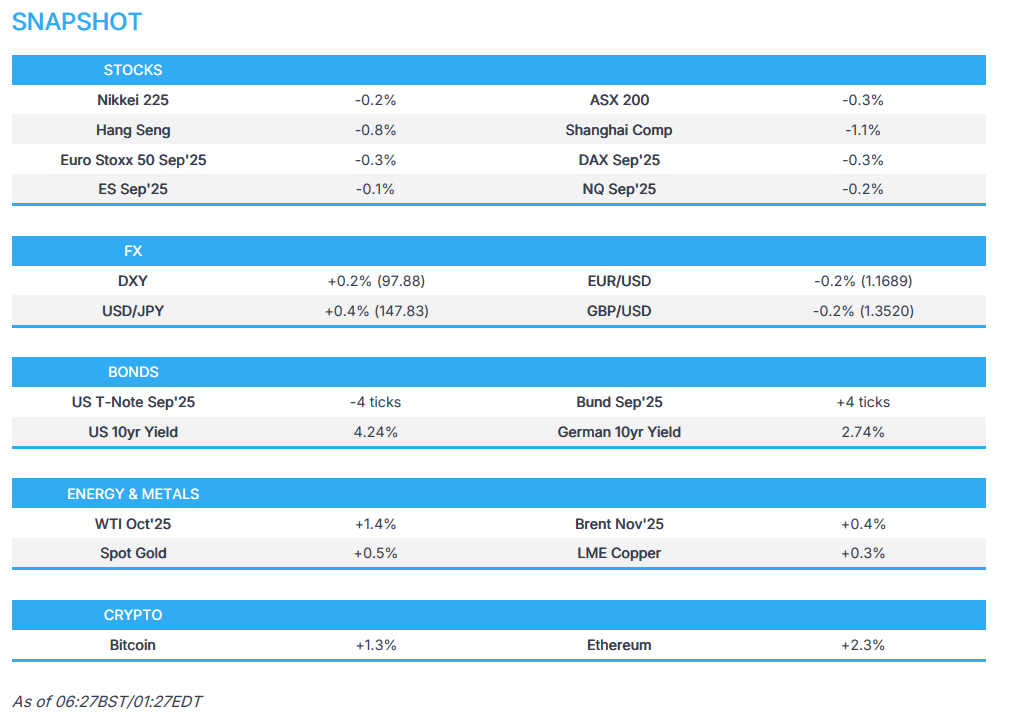

- APAC stocks traded mostly lower with the region cautious amid a lack of fresh drivers and following the holiday lull stateside.

- BoJ Deputy Governor Himino reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy and prices but noted high uncertainty.

- European equity futures indicate a slightly softer cash market open with Euro Stoxx 50 future down 0.2% after the cash market closed with gains of 0.3% on Monday.

- DXY is higher, JPY lags, EUR/USD has reverted back onto a 1.16 handle and antipodeans lag alongside the soft risk tone.

- Bunds are subdued following the prior day's retreat, crude futures extended the prior day's gains, spot gold hit a fresh record high above USD 3.500/oz.

- Looking ahead, highlights include EZ Flash HICP (Aug), US ISM Manufacturing PMI (Aug), Atlanta Fed GDP, Speakers including ECB’s Elderson & Nagel, and Supply from Germany.

US TRADE

EQUITIES

- US stock markets were closed on Monday for Labor Day.

TARIFFS/TRADE

- US Treasury Secretary Bessent said he plans to write a brief for the US Solicitor General to file that defends US President Trump’s tariffs, as well as commented that he is confident the Supreme Court will uphold Trump tariffs and noted there are other statutes that could be used to justify tariffs, but they are not as efficient and not as powerful. Bessent stated the US is making headway with Europe on the need to crack down on India over Russian oil purchases, while he played down the significance of the China-hosted meeting of leaders from non-Western countries as performative, and accused China and India of being ‘bad actors’ by fuelling the Russian war machine.

- Brazil's President Lula called for a virtual BRICS meeting on September 8th to discuss US tariffs.

- EU Council President Costa said it would have been an imprudent risk to escalate trade tensions with the US whilst Europe's eastern border is under threat, and that is why they chose diplomacy over escalation.

- Japan's trade negotiator Akazawa said there is no gap in understanding with the US on the trade deal and the schedule of his next visit is not yet set, while he added it is not true that Japan agreed to cut tariffs on farm products.

NOTABLE HEADLINES

- US Treasury Secretary Bessent said the Fed is and should be independent, but added the Fed has also made a lot of mistakes and commented that ‘we haven’t seen anything yet’ regarding the market reaction to President Trump’s pressure on the Fed. Bessent also commented that Fed Governor Cook should be removed or should step down if mortgage allegations are true and noted that Cook hasn’t denied them. Furthermore, Bessent said he thinks there will be a good chance that Stephen Miran is seated before the September meeting, according to interviews with Reuters and Semafor.

- US Treasury Secretary Bessent said President Trump may declare a national housing emergency this fall to address rising prices and dwindling supply, according to an interview with the Washington Examiner.

APAC TRADE

EQUITIES

- APAC stocks traded mostly lower with the region cautious amid a lack of fresh drivers and following the holiday lull stateside.

- ASX 200 was subdued amid underperformance in the consumer-related sectors, real estate, telecoms and energy, although the downside was somewhat cushioned by gains in the top-weighted financial industry.

- Nikkei 225 initially benefitted from currency weakness but pulled away from best levels following somewhat varied comments from BoJ's Himino who reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy and prices, but also noted high uncertainty surrounding the global economy and trade policy.

- Hang Seng and Shanghai Comp were pressured owing to weakness in tech and with a lack of fresh macro drivers, while participants also digested several automaker monthly updates and there were recent comments from US Treasury Secretary Bessent who downplayed the significance of the China-hosted meeting of leaders from non-Western countries as performative, and accused both China and India of being ‘bad actors’ by fuelling the Russian war machine.

- US equity futures (ES -0.2%, NQ -0.2%) struggled for direction following the recent US holiday closure and as data releases loom.

- European equity futures indicate a slightly softer cash market open with Euro Stoxx 50 future down 0.2% after the cash market closed with gains of 0.3% on Monday.

FX

- DXY gradually strengthened as trade began to pick up following the holiday lull and with participants awaiting upcoming data releases with ISM Manufacturing scheduled later, although the main focus for the potential to influence Fed policy will be Friday's BLS jobs report and next week's CPI data. Nonetheless, there were some recent comments from Treasury Secretary Bessent who commented that ‘we haven’t seen anything yet’ regarding the market reaction to President Trump’s pressure on the Fed and also said he thinks there will be a good chance that Stephen Miran is seated before the September meeting.

- EUR/USD trickled lower and reverted to sub-1.1700 territory amid light catalysts and with EU HICP data scheduled later.

- GBP/USD faded some of its recent gains after hitting resistance at the 1.3550 level but with the pullback contained in the absence of any major drivers, while UK PM Starmer's mini-reshuffle of his Downing Street team had little impact on GBP.

- USD/JPY gained a firmer footing at the 147.00 territory amid the upside in the greenback and following a deluge of comments from BoJ Deputy Governor Himino who stated that despite the three policy interest rate hikes by the central bank thus far, real interest rates have remained at significantly low levels as inflation has stayed strong, while he reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy and prices but noted high uncertainty regarding the global economy and trade.

- Antipodeans were lower amid the cautious overnight mood and with little reaction seen following the marginally better-than-expected Current Account Data and Net Exports Contribution to GDP from Australia.

- PBoC set USD/CNY mid-point at 7.1089 vs exp. 7.1325 (Prev. 7.1072)

FIXED INCOME

- 10yr UST futures remained lacklustre after the US holiday closure and with short-term supply scheduled later today.

- Bund futures demand was subdued following the prior day's retreat and as participants await EU inflation data, while there is also a EUR 4.5bln Schatz issuance scheduled later, followed by a EUR 5bln Bund auction tomorrow.

- 10yr JGB futures nursed some losses with support seen following stronger demand at the latest 10yr JGB auction.

COMMODITIES

- Crude futures extended on the prior day's gains amid the ongoing geopolitical tensions with Israel's recent strikes across Gaza and after Yemen's Houthis recently vowed retaliation for the killing of their PM and other senior officials last week.

- European Union countries are looking to ways to plug any remaining loopholes to ensure that Russian gas won’t be furtively mixed into the bloc’s supplies once a ban takes effect by the end of 2027, according to Bloomberg News.

- Spot gold briefly breached through the USD 3,500/oz level and printed a fresh record high amid the expectations for a Fed rate cut this month.

- Copper futures rebounded from Monday's trough but with price action kept relatively rangebound amid the mixed overnight risk appetite.

CRYPTO

- Bitcoin steadily gained throughout the session and returned to above the USD 110k level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Deputy Governor Himino said despite the three policy interest rate hikes by the central bank thus far, real interest rates have remained at significantly low levels as inflation has stayed strong, while he reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy and prices. Himino said there are various upside and downside risks to the economy and prices, as well as noted the baseline scenario is for Japan’s corporate profits to come under pressure from the global slowdown and the impact of trade policy. Himino said uncertainty surrounding the global economy remains high, and there is uncertainty over how trade policies could affect the economy and the fate of China’s ongoing trade negotiations with the US. Furthermore, he commented that as tapering moves forward, there may be a need to start exploring the amount of JGB monthly buying that is consistent with appropriate reserve levels, and it would be prudent to reduce the size of the BoJ’s balance sheet over time.

- Japanese PM Ishiba is reportedly making arrangements to instruct ministers as early as this week to compile economic measures to address inflation and Trump tariffs, according to Sankei newspaper. It was separately reported that Japanese Finance Minister Kato said the government will continue monitoring the impact of inflation and US tariff policies on corporate profits, while he added that he is not aware of plans for new economic stimulus package.

- South Korea and the US agreed to increase South Korea's defence budget from 2.4% to 3.5% of GDP, costing KRW 30tln, according to Dong-A Ilbo.

DATA RECAP

- Australian Current Account Balance SA (AUD) -13.7B vs. Exp. -16.0B (Prev. -14.7B)

- Australian Net Exports Contribution (Q2) 0.1% vs. Exp. 0.0% (Prev. -0.1%)

- New Zealand Terms of Trade QQ (Q2) 4.1% vs. Exp. 1.9% (Prev. 1.9%)

- New Zealand Export Volumes SA (Q2) -3.7% vs. Exp. -0.4% (Prev. 4.6%)

- New Zealand Export Prices SA (Q2) 0.2% vs. Exp. 1.5% (Prev. 7.1%)

- New Zealand Import Prices SA (Q2) -3.7% vs. Exp. -1.3% (Prev. 5.1%)

GEOPOLITICS

MIDDLE EAST

- Huge explosions reportedly shook Gaza City and northern areas, according to Al-Haddath via X.

RUSSIA-UKRAINE

- Russian President Putin stated that for a Ukrainian settlement to be sustainable and lasting, the root causes of the crisis that he has spoken about many times before must be addressed, and a fair balance in the sphere of security must be restored.

- French President Macron said he has spoken to the NATO Secretary General about preparations for the "Alliance of the Willing" meeting on Thursday in Paris. Macron also said they will move forward with their partners and in cooperation with NATO to define strong security guarantees for Ukraine, while he added that Ukraine's security guarantees are a prerequisite for real progress towards peace.

OTHER

- Chinese President Xi met with Russian President Putin, while Putin commented that Russia-China close communication reflects the strategic nature of Russia-China relations which are at an unprecedentedly high level. Furthermore, it was also reported that North Korean leader Kim travelled to China via train ahead of China's Victory Day Parade.