US Market Open: DXY soars as GBP & JPY sinks, US equity futures also lower into ISM Manufacturing PMI

02 Sep 2025, 11:30 by Newsquawk Desk

- US Treasury Secretary Bessent said he plans to write a brief for the US Solicitor General to file that defends US President Trump’s tariffs.

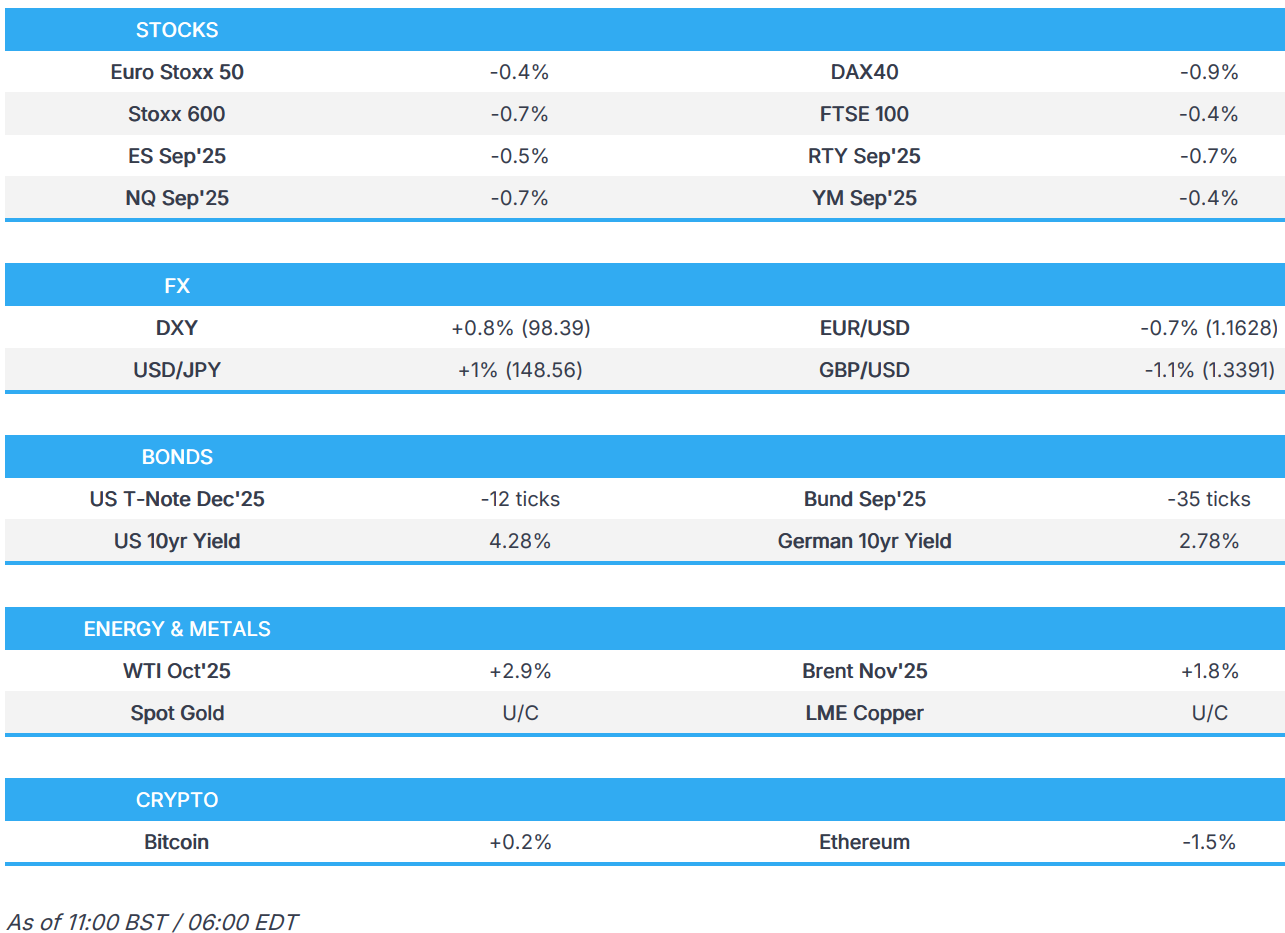

- European bourses opened mixed but are now mostly lower; US futures also slip, with underperformance in the RTY.

- GBP and JPY selling helps support DXY into key US data.

- Political and fiscal turmoil drives yields higher, no move to EZ HICP, USTs await ISM.

- Crude edges higher despite risk aversion and a firmer dollar, with geopolitics in focus.

- "The Israeli prime minister is holding a meeting to discuss the possibility of full control of the West Bank and measures against the Palestinian Authority", according to Iran International citing i24

- Looking ahead, US ISM Manufacturing PMI (Aug), Atlanta Fed GDP, Speakers including ECB’s Elderson, Muller & Nagel.

TARIFFS/TRADE

- US Treasury Secretary Bessent said he plans to write a brief for the US Solicitor General to file that defends US President Trump’s tariffs, as well as commented that he is confident the Supreme Court will uphold Trump tariffs and noted there are other statutes that could be used to justify tariffs, but they are not as efficient and not as powerful. Bessent stated the US is making headway with Europe on the need to crack down on India over Russian oil purchases, while he played down the significance of the China-hosted meeting of leaders from non-Western countries as performative, and accused China and India of being ‘bad actors’ by fuelling the Russian war machine.

- Brazil's President Lula called for a virtual BRICS meeting on September 8th to discuss US tariffs.

- EU Council President Costa said it would have been an imprudent risk to escalate trade tensions with the US whilst Europe's eastern border is under threat, and that is why they chose diplomacy over escalation.

- Japan's trade negotiator Akazawa said there is no gap in understanding with the US on the trade deal and the schedule of his next visit is not yet set, while he added it is not true that Japan agreed to cut tariffs on farm products.

- Indian Trade Minister says India is in talks with the US over bilateral trade agreement.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.6%) opened mixed, trading on either side of the unchanged mark. But sentiment took a hit seemingly after UK assets (GBP/Gilts) took a beating. As it stands, bourses are lower across the board and trading near lows – the CAC 40 manages to hold afloat, with the Luxury sector doing much of the heavy lifting.

- European sectors hold a strong negative bias; initially opening with a very narrow breadth, but has widened, particularly as the losers slip further. Real Estate is found right at the foot of the pile, dragged lower by the higher yield environment, which has been sparked by continued pressure in Gilts. Thereafter, a couple of cyclical sectors (Retail / Travel & Leisure) take a beating amidst the risk-off tone. Despite the subdued sentiment, Consumer Products tops the pile – this is thanks to a couple of broker upgrades for the Luxury sector. HSBC upgraded both LVMH (2.8%) & Kering (+3.3%), whilst Hermes (U/C) was downgraded.

- US equity futures (ES -0.5% NQ -0.7% RTY -0.7%) are lower across the board, with some underperformance in the RTY given the higher yield environment. US traders return from Labor Day holiday, and have a number of moving parts to digest, including; a) US court ruling Trump tariffs as illegal, b) geopolitical uncertainty, c) Bessent suggesting there is a good chance Miran will be seated at the Fed for the September meeting, d) US Commerce Department revoked waivers for Intel/Samsung/SK Hynix, making it harder to produce chips in China.

- Nestle -1.8%; Co. ousts CEO for having an affair with a company employee; Navratil will replace, who has over two decades of experience at the Co.

- Tencent’s open-source translation model beats Google, OpenAI in top global AI competition, via SCMP.

- CPCA reports Tesla (TSLA) sold 839k China-made vehicles in August (vs. July 67.8k).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is very much on the front foot following Monday's market holiday with the dollar showing the greatest gains vs. JPY and GBP. In terms of fresh fundamental drivers from the US, there hasn't been much fallout from the US appeals court ruling that most tariffs issued by US President Donald Trump are illegal. US Treasury Secretary Bessent has since noted that other statutes could be used to justify tariffs, but they are not as efficient and not as powerful. Market focus this week is set to be dominated by the data slate with today's highlight coming via ISM Manufacturing PMI metrics. Current session high at 98.44. Next target comes via the 27th August peak at 98.73.

- EUR is in-fitting with the performance seen in peers, EUR is on the backfoot vs. the USD. Albeit with some support provided by cross-related flows into EUR/GBP. Today's Eurozone inflation data showed an unexpected uptick in inflation to 2.1% from 2.0%, super-core held steady at 2.3% (Exp. 2.2%) and services ticked low to 3.1% from 3.2%. The data is non-incremental for the near-term policy outlook with an unchanged rate next week priced at 99%. EUR/USD has reverted back onto a 1.16 handle and slipped below its 50DMA at 1.1660. Current session low sits at 1.1624 with focus on a potential test of 1.16.

- JPY sits near the foot of the majors following a combination of BoJ rhetoric and political instability. On the former, remarks from Deputy Governor Himino appeared at first glance hawkish with the central banker noting that despite the three policy interest rate hikes by the central bank thus far, real interest rates have remained at significantly low levels as inflation has stayed strong. He subsequently reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy. On the political front, reports suggest that following the party's poor electoral performance, LDP sec gen Moriyama and policy chief Onodera will resign from their positions. USD/JPY has ripped through the 148 mark and is approaching its 200DMA at 148.85

- GBP is getting hit pretty hard this morning with ongoing focus on the UK's desperate fiscal outlook. This has been reflected in fixed income markets with the UK 30yr yield hitting its highest level since 1998. In terms of what has changed since the start of the week, focus has been on PM Starmer's decision to bring in several economic advisers to oversee the Autumn budget. The changes have been framed by the PM as a move to help improve economic growth. However, as the budget comes into view, markets are becoming increasingly concerned over the prospect of higher taxation and other market-unfriendly policies given the lack of scope to cut spending further. The timing of the budget is yet to be confirmed. Cable has crashed through the 1.35 mark and briefly made its way onto a 1.33 handle with a session low at 1.3376.

- Antipodeans are softer vs. the dollar alongside the soft risk tone and broadly stronger USD. Overnight, little reaction was seen following the marginally better-than-expected Current Account Data and Net Exports Contribution to GDP from Australia.

- PBoC set USD/CNY mid-point at 7.1089 vs exp. 7.1325 (Prev. 7.1072)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs opened higher by a couple of ticks before treading water into supply, an outing that was strong with a b/c near 4x. This lifted JGBs by over 20 ticks to a 137.62 peak for the session, with gains of just under 40 ticks at most. However, much of this then pared and JGBs have since reverted back to pre-auction levels of c. 137.40. Since, though not spurring any significant JGB action thus far but potentially driving some of the post-supply pullback, LDP members Moriyama and Onodera reportedly intend to resign. Resignations seemingly framed as the LDP taking responsibility for the recent Upper House defeat, and adds pressure on PM Ishiba to resign.

- Gilts opened in the red by a handful of ticks but have since slumped to downside of 40 ticks at worst in 90.16-89.82 confines. A bout of pressure that has been reflected across the broader fixed income space with significant moves seen across assets as well (USD bid, Equities hit). The move appeared to begin with UK assets, despite a lack of fresh newsflow at the time. Action has propelled the 30yr yield to yet another multi-year high, at 5.69%, and taken the 10yr yield to 4.806% and approaching the zone which, at the time of the Spring Statement, was seen as sufficient to erode Reeves headroom via heightened funding costs.

- Bunds are lower and currently trading off by around 30 ticks, in a 128.77 to 129.24 range. A couple of ECB speakers today, but not really adding too much - Simkus said that additional negative information could see the Bank discuss a cut in October. Today's Flash HICP data will alleviate some of those fears as it came in hotter-than-expected for the headline and super-core Y/Y metrics while the core printed as forecast and the services figure moderated from the prior. No reaction to ECB pricing, implies just 6bps of further easing this year.

- On France, we continue to count down to Monday’s confidence vote. Major updates a little light since Sunday’s media rounds from PM Bayrou, though National Rally (RN) has reportedly begun preparing for the possibility of the vote sparking a snap election, according to Les Echos. OAT-Bund 10yr yield spread is wider today, but thus far remains around the 80bps mark

- USTs are also lower, following peers. Overnight focus was on trade and Fed commentary from US officials. Firstly, Treasury Secretary Bessent said they are confident the Supreme Court will uphold Trump’s tariffs and highlighted that there are other ways of justifying tariffs. On the Fed, Bessent said we haven’t seen anything yet’ regarding the market reaction to President Trump’s pressure on the Fed, and believes there is a good chance Miran is in place before the September FOMC. USTs lower by 11 ticks at most, holding just off lows in a 112-05 to 112-16 band. Focus for the day is on any further trade updates, developments on Fed’s Cook (court document submission deadline) and ISM Manufacturing.

- Price guidance for UK's 4.75% Oct 2035 Gilt set at 8.25bps above March 2035 Gilt; Books set to close at 09:30BST, according to bookrunner cited by Reuters.

- Germany sells EUR 3.552bln vs exp. EUR 4.5bln 1.90% 2027 Schatz: b/c 2x (prev. 2.50x), average yield 1.96% (prev. 1.90%) and retention 21.07% (prev. 21.68%).

- Click for a detailed summary

COMMODITIES

- Crude is firmer and edging higher this morning, totally ignoring headwinds from a firmer dollar and broader risk aversion, with the gap in intraday price changes between WTI and Brent a function of yesterday's lack of settlement amid the US Labor Day holiday. Focus appears to be on the lack of peace progress between Russia-Ukraine and as Israel intensifies its attack on Gaza. WTI currently resides in a 63.66-65.35/bbl range while Brent sits in a USD 68.15-68.83/bbl range.

- Mixed fortunes for precious metals but with outperformance in gold vs peers. Spot silver pulls back after yesterday's outperformance, whilst palladium succumbs to broader risk aversion. Spot gold eked a fresh record high overnight at USD 3,508.79/oz before pulling back towards lows on USD strength, albeit losses remain cushioned.

- Mostly lower trade across base metals amid the firmer dollar and broader risk aversion across the complex. 3M LME copper resides in a USD 9,850.00-9,944.85/t.

- European Union countries are looking to ways to plug any remaining loopholes to ensure that Russian gas won’t be furtively mixed into the bloc’s supplies once a ban takes effect by the end of 2027, according to Bloomberg News.

- Gazprom CEO Miller states Power of Siberia 2 gas supply deal with China agreed for 30 years, with pricing below European levels; Russia and China continue work on new possibilities in gas supplies.

- Russian oil product loadings from the Black Sea Port of Tuapse planned at 1.098mln tonnes in September (vs 1.068mln tonnes in August), according to traders cited by Reuters.

- Commerzbank expects gold to reach USD 3,600/oz by end the of next year (unchanged from June).

- Shell (SHEL LN) will begin a major turnaround at its Pernis refinery (404k BPD capacity) from mid-September, according to a statement.

- Click for a detailed summary

NOTABLE DATA RECAP

- French Budget Balance (Jul) -142.0B (Prev. -100.4B)

- EU HICP Flash YY (Aug) 2.1% vs. Exp. 2.0% (Prev. 2.0%); Services 3.1% (prev. 3.2%)

- EU HICP-X F,E,A&T Flash YY (Aug) 2.30% vs. Exp. 2.20% (Prev. 2.30%); HICP-X F&E Flash YY (Aug) 2.3% vs. Exp. 2.3% (Prev. 2.4%); HICP-X F, E, A, T Flash MM (Aug) 0.30% (Prev. -0.20%)

NOTABLE EUROPEAN HEADLINES

- ECB's Schnabel says rates are already mildly accommodative; Tariffs are on balance inflationary; Do not see a reason for a further rate cut. Less worried about the exchange rate. Inflation risks are tilted to the upside. Global rate hikes may come earlier than people think. Highly unlikely inflation expectations de-anchor to the downside.

- ECB's Kocher advocates caution ahead of next rate decision.

- ECB's Simkus says, "additional negative information might lead us to discuss a cut again in October", via Econostream on X. "More true than not" that another cut is coming, and it is just a matter of timing. Many force now at work that point to lower future inflation. Risks to the economy and to inflation are tilted to the downside. Some risks are already materialising.

- Santander expects the BoE to keep rates at 4% until end-2026 (prev. saw two cuts in 2026).

NOTABLE US HEADLINES

- US Treasury Secretary Bessent said the Fed is and should be independent, but added the Fed has also made a lot of mistakes and commented that ‘we haven’t seen anything yet’ regarding the market reaction to President Trump’s pressure on the Fed. Bessent also commented that Fed Governor Cook should be removed or should step down if mortgage allegations are true and noted that Cook hasn’t denied them. Furthermore, Bessent said he thinks there will be a good chance that Stephen Miran is seated before the September meeting, according to interviews with Reuters and Semafor.

- US Treasury Secretary Bessent said President Trump may declare a national housing emergency this fall to address rising prices and dwindling supply, according to an interview with the Washington Examiner.

- US Senate Republicans are on track to trigger the so-called “nuclear option” to make it easier for the Senate to confirm Trump’s nominees, according to Punchbowl.

- Punchbowl reports that a continuing resolution will be needed to avoid a US government shutdown on October 1st, adding that there is no way Congress can pass 12 spending bills by then as there are just 14 legislative days left.

GEOPOLITICS

MIDDLE EAST

- "The Israeli prime minister is holding a meeting to discuss the possibility of full control of the West Bank and measures against the Palestinian Authority", according to Iran International citing i24.

- Huge explosions reportedly shook Gaza City and northern areas, according to Al-Haddath via X.

- "Iranian Foreign Ministry: We have not yet made a decision on continuing negotiations with the International Atomic Energy Agency (IAEA)", according to Al Jazeera.

RUSSIA-UKRAINE

- Russian President Putin stated that for a Ukrainian settlement to be sustainable and lasting, the root causes of the crisis that he has spoken about many times before must be addressed, and a fair balance in the sphere of security must be restored.

- French President Macron said he has spoken to the NATO Secretary General about preparations for the "Alliance of the Willing" meeting on Thursday in Paris. Macron also said they will move forward with their partners and in cooperation with NATO to define strong security guarantees for Ukraine, while he added that Ukraine's security guarantees are a prerequisite for real progress towards peace.

- Russian President Putin says Russia has no intention of attacking anyone; claims about Russia's intention to attack Europe are either a provocation or incompetence; West and NATO are trying to absorb the post-Soviet space, says "we have to react to this". Russia is now responding seriously to Ukrainian attacks on energy infrastructure. Ukraine's membership of NATO remains unacceptable to Russia. Believes there is an opportunity to find a consensus, in the context of matters discussed during the Alaska summit.

- Finnish President, on security guarantees for Ukraine, says, "we are making progress on this and hopefully will get a solution soon"; not very optimistic that Ukraine ceasefire or framework for peace will be achieved in the near future.

- NATO Secretary General Rutte says NATO takes the jamming of GPS signals very seriously.

OTHER

- Chinese President Xi met with Russian President Putin, while Putin commented that Russia-China close communication reflects the strategic nature of Russia-China relations which are at an unprecedentedly high level. Furthermore, it was also reported that North Korean leader Kim travelled to China via train ahead of China's Victory Day Parade.

CRYPTO

- Bitcoin is incrementally firmer and trades around USD 110k whilst Ethereum slips down below USD 4.4k.

APAC TRADE

- APAC stocks traded mostly lower with the region cautious amid a lack of fresh drivers and following the holiday lull stateside.

- ASX 200 was subdued amid underperformance in the consumer-related sectors, real estate, telecoms and energy, although the downside was somewhat cushioned by gains in the top-weighted financial industry.

- Nikkei 225 initially benefitted from currency weakness but pulled away from best levels following somewhat varied comments from BoJ's Himino who reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy and prices, but also noted high uncertainty surrounding the global economy and trade policy.

- Hang Seng and Shanghai Comp were pressured owing to weakness in tech and with a lack of fresh macro drivers, while participants also digested several automaker monthly updates and there were recent comments from US Treasury Secretary Bessent who downplayed the significance of the China-hosted meeting of leaders from non-Western countries as performative, and accused both China and India of being ‘bad actors’ by fuelling the Russian war machine.

NOTABLE ASIA-PAC HEADLINES

- BoJ Deputy Governor Himino said despite the three policy interest rate hikes by the central bank thus far, real interest rates have remained at significantly low levels as inflation has stayed strong, while he reiterated it is appropriate to continue raising interest rates in accordance with improvements in the economy and prices. Himino said there are various upside and downside risks to the economy and prices, as well as noted the baseline scenario is for Japan’s corporate profits to come under pressure from the global slowdown and the impact of trade policy. Himino said uncertainty surrounding the global economy remains high, and there is uncertainty over how trade policies could affect the economy and the fate of China’s ongoing trade negotiations with the US. Furthermore, he commented that as tapering moves forward, there may be a need to start exploring the amount of JGB monthly buying that is consistent with appropriate reserve levels, and it would be prudent to reduce the size of the BoJ’s balance sheet over time. There is no intention to signal the timing for the offloading of the BoJ's ETF and REIT holdings. Will make rate decision looking not just at whether the likelihood of underlying inflation achieving 2% heightening, but upside and downside risks to baselines. If it becomes clear US tariff impact on Japan's economy does not materialise, that would work in favour of raising rates. Hard to say exactly when BoJ can judge the impacts of US tariffs on Japan's economy would be limited. Wants to pay close attention to the impact of US tariffs on US/Japanese corporate profits. Wants to look not just at numerical data but mechanism in which the impact could spread, re. US tariffs.

- Japanese PM Ishiba is reportedly making arrangements to instruct ministers as early as this week to compile economic measures to address inflation and Trump tariffs, according to Sankei newspaper. It was separately reported that Japanese Finance Minister Kato said the government will continue monitoring the impact of inflation and US tariff policies on corporate profits, while he added that he is not aware of plans for new economic stimulus package.

- South Korea and the US agreed to increase South Korea's defence budget from 2.4% to 3.5% of GDP, costing KRW 30tln, according to Dong-A Ilbo.

- Russian President Putin says they are ready to support a strategic partnership with China and the strengthening of contacts on a high level, via Ria.

- Fast Retailing (9983 JT) UNIQLO Japan SSS August 5.3% Y/Y (prev. 2.4%).

- Possible meeting between Russian President Putin and North Korean leader Kim Jung Un will be discussed after the latter's arrival to China, according to Tass.

- Japan's Ruling LPD's Moriyama intends to step down, according to Kyodo.

- Japan's LDP Policy Chief Onodera will reportedly resign, according to TV Asahi

- Japanese PM Ishiba says there is responsibility for addressing various challenges the LDP faces; will decide on responsibility at the appropriate time. On the economy, says, need to swiftly conduct economic policies including tariffs.

DATA RECAP

- Australian Current Account Balance SA (AUD) -13.7B vs. Exp. -16.0B (Prev. -14.7B)

- Australian Net Exports Contribution (Q2) 0.1% vs. Exp. 0.0% (Prev. -0.1%)

- New Zealand Terms of Trade QQ (Q2) 4.1% vs. Exp. 1.9% (Prev. 1.9%)

- New Zealand Export Volumes SA (Q2) -3.7% vs. Exp. -0.4% (Prev. 4.6%)

- New Zealand Export Prices SA (Q2) 0.2% vs. Exp. 1.5% (Prev. 7.1%); Import Prices SA (Q2) -3.7% vs. Exp. -1.3% (Prev. 5.1%)