US Market Open: NQ boosted after Google (+5.7%) is spared break-up; Crude slips on reports OPEC+ is mulling a production hike

03 Sep 2025, 11:09 by Newsquawk Desk

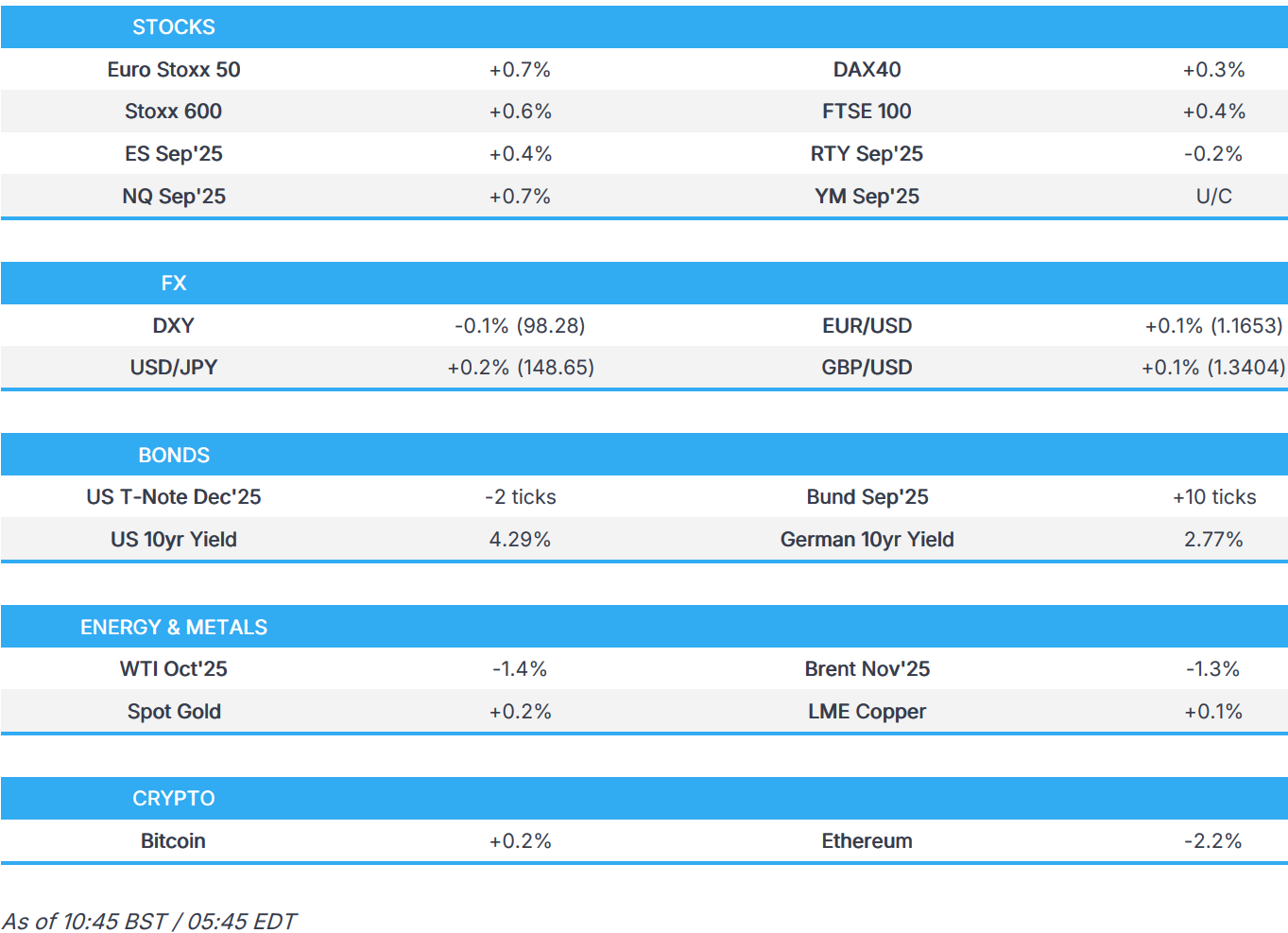

- European bourses are broadly in the green; US equity futures are mixed, with clear outperformance in the NQ, boosted by Google (+5.7% pre-market).

- A US judge ruled Google will not have to sell Chrome or Android in the monopoly case but must share search data with rivals and stop exclusive distribution contracts.

- Contained trade in FX as an early pick-up in the USD fizzled out ahead of JOLTS.

- Early rise in yields have since reversed with bonds now bouncing.

- Crude sinks on reports OPEC+ is mulling another oil production hike; spot gold holds an upward bias after reaching levels near USD 3,550/oz.

- Looking ahead, US Durable Goods R (Jul), JOLTS Job Openings (Jul), NBP Announcement, Fed Beige Book, BoE’s Bailey, Lombardelli, Greene & Taylor, Fed’s Musalem & Kashkari.

TARIFFS/TRADE

- Japanese Trade Negotiator Akazawa is reportedly arranging a visit to the US between September 4th-6th, according to Yomiuri. To travel to the US from Thursday through Saturday, according to the government.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) opened in the green and have held an upward bias throughout the morning. Sentiment which is seemingly driven by a paring of the significant pressure seen on Tuesday, and as Google received a favourable judge ruling.

- European sectors hold a slight positive bias, following on from a poor session on Tuesday. Tech takes the top spot, paring back some of the underperformance seen in the prior session as Google (+5.8% pre-market) helps to lift the mood within the sector (see US section for details). Consumer Products follows closely behind, with the Luxury sector building on the prior day’s gains, this time following a positive trading update from Watches of Switzerland (+7.6%). The Co. confirmed strong sales, affirmed its guidance and highlighted that it does not expect to be materially impacted by US tariffs in H1’26.

- US equity futures (ES +0.5%, NQ +0.7%, RTY -0.2%) are mixed at the moment, with outperformance in the NQ whilst the RTY lags a touch. The former benefits from pre-market strength in Google (+5.7%) whilst the RTY is hampered by the relatively higher yield environment.

- A US judge ruled Google will not have to sell Chrome or Android in the monopoly case but must share search data with rivals and stop exclusive distribution contracts.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY was initially a little firmer but is now trading on the backfoot and towards session lows. Traders are mindful of ongoing tariff-related updates with President Trump stating that his administration will be going to the Supreme Court today to appeal the judgement from the US appeals court that most of his tariffs are illegal. Given the other routes available to Trump, desks remain sceptical that an unfavourable Supreme Court judgement would have any material sway on the administration's approach to trade policy. Focus will today also be on the data slate with JOLTS job openings due on deck ahead of ADP tomorrow and NFP on Friday. DXY currently near lows in a 98.20 to 98.63 range.

- EUR is slightly firmer with incremental macro drivers for the Eurozone lacking. Final Eurozone PMI metrics passed with little in the way of fanfare with the August composite PMI metric revised a touch lower to 51.0 from 51.1. The accompanying report noted that "Yes, the economy has been growing since the start of the year, but the pace is painfully slow". One risk on the horizon for the Eurozone comes via French political tensions as markets brace for the September 8th confidence vote in PM Bayrou. Expectations are firmly in favour of him losing the vote. EUR/USD delved as low as 1.1609 before staging a recovery.

- JPY remains on the backfoot and unable to catch a break vs. the USD. Yesterday's softness was largely pinned on a lack of commitment from BoJ Deputy Governor Himino in backing further policy tightening, alongside increased domestic political risk. On which, the latest reports suggest that Japanese ruling party LDP's Aso is set to call for an early party election, according to Mainichi. On trade, Japanese Trade Negotiator Akazawa is reportedly arranging a visit to the US between September 4th-6th, according to Yomiuri. USD/JPY briefly moved back above its 200DMA at 148.83 and took out the 149 level with a session peak at 149.13 before retreating.

- After a wobble in early European trade, GBP has managed to recoup losses. Back-end UK yields remain higher as fiscal angst continues to grip the market narrative. Markets now have a date for the Autumn Budget with the Treasury opting for November 26th; somewhat later than what many had been expecting. On monetary policy, focus today will be on BoE's Bailey, Lombardelli, Greene and Taylor all due to appear before the TSC. Likely areas of focus will be on how the Bank looks to navigate the pathway between an expected slowdown in growth and stubborn inflation. An upward revision to the August services and composite PMIs failed to provide additional support for GBP. GBP/USD hit a multi-week low at 1.3334 before recovering to levels just above 1.34.

- AUD is a touch more resilient than most peers with the currency underpinned by a better-than-expected outturn for Q2 Australian GDP (Q/Q 0.6% vs. Exp. 0.5%). AUD/USD sits in close proximity to its 50DMA at 0.6519 and around the mid-point of Tuesday's 0.6483-0.6558 range.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A softer start to the day for Bunds, continuing the price action seen on Tuesday but holding above Tuesday's 128.68 low. Thereafter, a bout of pressure to a 128.63 trough, with downside of c. 15 ticks occurring amid a volume spike just after the cash equity open and the morning’s first PMI. The Spanish Services figure came in shy of consensus, though internal commentary was strong. Though this was short-lived. Thereafter, Germany was revised lower into contractionary territory, which helped to lift Bunds marginally back into the green and to a 129.00 high. No real move to a German 2035 auction, which saw a same-as-prior b/c, but higher avg. yield.

- OATs are gaining to a similar degree as German paper. The main update has been an interview with Finance Minister Lombard to the FT, the Minister outlined that the toppling of PM Bayrou next week (looks all but certain, currently) would require fresh concessions to be made to the left in order to secure support for the fiscal package. A package that is currently targeting a deficit cut of EUR 44bln. The Bund-OAT 10yr yield spread remains steady around the 80bps mark.

- Gilts began on the backfoot today, but recent price action has been upwards, following European peers. Confirmation this morning that the Treasury will unveil the Autumn Budget on November 26th, confirming a Huffington Post scoop. Price action this morning began with a continuation of Tuesday’s sell off, Gilts as low as 89.36, 24 ticks below Tuesday’s base. However, the magnitude of this has waned in-fitting with the upticks discussed in EGBs, and most recently UK paper has climbed incrementally into the green. As for yields, thus far a 4.86% high for the 10yr, eyeing January's 4.925% peak, and 5.75% for the 30yr. Ahead, the BoE appears before the TSC to discuss the last policy announcement (subject to two rounds of voting, resulting in a 25bps cut).

- USTs are directionally in-fitting with peers but with action contained to a thin 112-00 to 112-08+ band thus far. USTs await Fed speak Musalem and Kashkari, remarks that are intersected by a handful of data points headlined by JOLTS.

- Germany sells EUR 3.81bln vs exp. EUR 5bln 2.60% 2035 Bund: b/c 1.4x (prev. 1.4x), average yield 2.77% (prev. 2.69%), retention 23.8% (prev. 22.3%).

- Click for a detailed summary

COMMODITIES

- Softer trade in the crude complex this morning after whipsawing yesterday amid a stronger dollar and with the US imposing sanctions targeting Iranian oil. Newsflow for the complex has been quiet, although traders are keeping tabs on developments in the east, with focus overnight on the Chinese military parade - but more so the presence of Russian President Putin and North Korean leader Kim alongside Chinese President Xi. The complex then took a significant leg lower on Reuters source reports that OPEC+ is mulling another oil production hike at Sunday's meeting - this is in contrast to expectations that the OPEC-8 would hold production. WTI fell from USD 65.17/bbl to USD 64.33/bbl before paring around half of the move in the minutes since. At the same time, Brent slipped from USD 68.73/bbl to USD 67.89/bbl.

- Mixed trade across precious metals in narrow parameters. Spot gold holds a mild upward bias but printed fresh record near the USD 3,550/oz level overnight despite recent dollar strength. Spot gold resides in a USD 3,526.54-3,547.33/oz range at the time of writing, with the next upside level the USD 3,550/oz mark.

- Upward tilt across base metals with prices supported by a stable dollar and with sentiment also net-positive. 3M LME copper breached USD 10k/t to the upside and resides in a USD 9,935.80-10,038.13/t range at the time of writing.

- World Gold Council said to launch a digital form of gold, according to FT.

- OPEC+ reportedly mulling another oil production hike at Sunday meeting, according to Reuters source; final decision not made yet

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Producer Prices MM (Jul) 0.4% vs. Exp. 0.2% (Prev. 0.8%); Producer Prices YY (Jul) 0.2% vs. Exp. 0.1% (Prev. 0.6%)

- EU HCOB - Composite Final PMI (August) 51.0 vs. Exp. 51.1 (Prev. 51.1); HCOB Services Final PMI (August) 50.5 vs. Exp. 50.7 (Prev. 50.7)

- German HCOB Services PMI (August) 49.3 vs. Exp. 50.1 (Prev. 50.1); HCOB Composite Final PMI (August) 50.5 vs. Exp. 50.9 (Prev. 50.9)

- Spanish Services PMI (August) 53.2 vs. Exp. 53.9 (Prev. 55.1)

- Italian HCOB Composite PMI (August) 51.7 (Prev. 51.5); HCOB Services PMI (August) 51.5 vs. Exp. 52.0 (Prev. 52.3)

- French HCOB - Services PMI (August) 49.8 vs. Exp. 49.7 (Prev. 49.7); "At the time of the August PMI survey dates, it was not yet known that Prime Minister Bayrou would seek a vote of confidence in parliament on September 8"; Composite PMI (August) 49.8 vs. Exp. 49.8 (Prev. 49.8)

- UK S&P Global PMI: Composite Output (August) 53.5 vs. Exp. 53.0 (Prev. 53.0); Global Services PMI (August) 54.2 vs. Exp. 53.6 (Prev. 53.6)

- Germany's VCI, chemical industry association, reports Q2 production -3.1% Y/Y, -5.1% Y/Y ex-pharma.

- Germany's VDMA says German Engineering Orders +4% Y/Y in July, with domestic orders flat, and foreign orders +7% Y/Y; Engineering Orders +2% May-July, with domestic orders -1% Y/Y and foreign orders +3%.

- German Car Registration +5% to 207.229k (vs +11% in July), according to KBA.

- Turkish CPI MM (Aug) 2.04% vs. Exp. 1.79% (Prev. 2.06%); Turkish CPI YY (Aug) 32.95% vs. Exp. 32.6% (Prev. 33.52%)

NOTABLE EUROPEAN HEADLINES

- UK Government confirms it will hold the Autumn Budget on November 26th

- UK Chancellor Reeves says need to bring inflation and borrowing costs down; says economy is not broken.

- French Finance Minister Lombard urged for a compromise on the 2026 Budget and said the deficit reduction plan will inevitably be less ambitious if the government falls, while he is confident France will accomplish its GDP growth forecast of 0.6% this year and said they are on track to reduce the deficit from 5.8% in 2024 to 5.4% in 2025, according to FT.

- EU court backs EU and US data transfer deal affecting thousands of firms.

NOTABLE US HEADLINES

- US Treasury Secretary Bessent is planning to start a blitz of interviews on Friday in search of a candidate to be the next Fed Chair, according to WSJ.

- US admin officials reportedly want to fund federal agencies until the first quarter of 2026, according to Punchbowl sources; "This would avoid repeated shutdown deadline dramas. Yet it also opens the door to a year-long continuing resolution”.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukraine's military said Russia launched an air attack on Kyiv and it was also reported that all of Ukraine was under air raid alerts following Ukrainian air force warnings of Russian missile and drone attacks, while Poland scrambled aircraft to ensure airspace security after Russia launched strikes on Ukraine.

- Russian Foreign Minister Lavrov said Moscow expects Russia-Ukraine talks to continue and he stated that the heads of delegations are in direct contact. Lavrov said Russia expects statements from its partners in support of dialogue with the US on Ukraine, while he added that for a lasting peace in Ukraine, territorial realities must be recognised. Lavrov also said that India did not bow to US demands to stop purchasing resources from Russia, which Moscow appreciates, as well as noted the US is making active diplomatic efforts on Ukraine and that Putin–Trump contacts are substantive. Furthermore, he said a new system of security guarantees for Russia and Ukraine must be formed and that Moscow calls for ensuring a neutral, non-bloc and non-nuclear status of Ukraine, according to RIA and TASS.

- Russian Foreign Ministry spokeswoman said Kyiv and its allies reject the possibility of compromises on settlement of conflicts, according to RIA.

- Russia and the US are in the process of coordinating on dates and the venue of the next round of talks, according to RIA.

MIDDLE EAST

- "[Israeli] Finance Minister Smotrich seeks to impose sovereignty over 82% of the West Bank", according to Al Jazeera.

OTHER

- Chinese President Xi said at the military parade in Beijing that China is a great nation that fears no violence and is self-reliant and strong, while he added the Chinese people stand on the right side of history and are committed to peace. Xi also said the world is facing a choice of peace or war now and he called on nations to prevent historical tragedies from recurring.

- US President Trump posted on Truth Social "The big question to be answered is whether or not President Xi of China will mention the massive amount of support and “blood” that The United States of America gave to China in order to help it to secure its FREEDOM from a very unfriendly foreign invader. Many Americans died in China’s quest for Victory and Glory. I hope that they are rightfully Honored and Remembered for their Bravery and Sacrifice! May President Xi and the wonderful people of China have a great and lasting day of celebration. Please give my warmest regards to Vladimir Putin, and Kim Jong Un, as you conspire against The United States of America. PRESIDENT DONALD J. TRUMP”.

CRYPTO

- Bitcoin is flat and trades just above USD 110k whilst Ethereum slips a touch down to USD 4.3k.

APAC TRADE

- APAC stocks were predominantly lower following the weak handover from Wall St, where the major indices declined on return from the extended weekend as sentiment was dampened by global debt concerns amid a higher yield environment.

- ASX 200 retreated with the declines led by underperformance in tech, utilities and financials, while slightly stronger-than-expected Australian GDP data failed to inspire.

- Nikkei 225 was pressured amid a higher global yield environment but with the downside initially cushioned by recent currency weakness.

- Hang Seng and Shanghai Comp gradually fell despite the better-than-expected RatingDog Services PMI data from China and with the attention in Beijing on the military parade, which was attended by Russian President Putin and North Korean Leader Kim, while US President Trump reacted in a post and accused them of conspiring against the US.

NOTABLE ASIA-PAC HEADLINES

- BoJ Governor Ueda said he exchanged views with PM Ishiba on the economy and financial markets, while they had discussions on various topics about the economy and talked about forex. Ueda said it was a regular meeting to exchange views on the economy and financial markets and there is no change to their stance of raising interest rates if the economy and prices move in line with the forecast.

- Japanese ruling party LDP's Aso is set to call for an early party election, according to Mainichi.

- Japan's budget requests from government agencies for next FY total JPY 122.45tln, according to the MoF.

- RBA Governor Bullock says the RBA is actively exploring the implications of emerging technologies, particularly AI, and how they can support its mission.

DATA RECAP

- Chinese RatingDog Services PMI (Aug) 53.0 vs. Exp. 52.4 (Prev. 52.6); Composite PMI (Aug) 51.9 (Prev. 50.8)

- Australian Real GDP QQ SA (Q2) 0.6% vs. Exp. 0.5% (Prev. 0.2%, Rev. 0.3%); YY SA (Q2) 1.8% vs. Exp. 1.6% (Prev. 1.3%, Rev. 1.4%)