US Market Open: US equity futures move higher, DXY/USTs await key US data & Fed Chair nominee Miran's hearing

04 Sep 2025, 11:10 by Newsquawk Desk

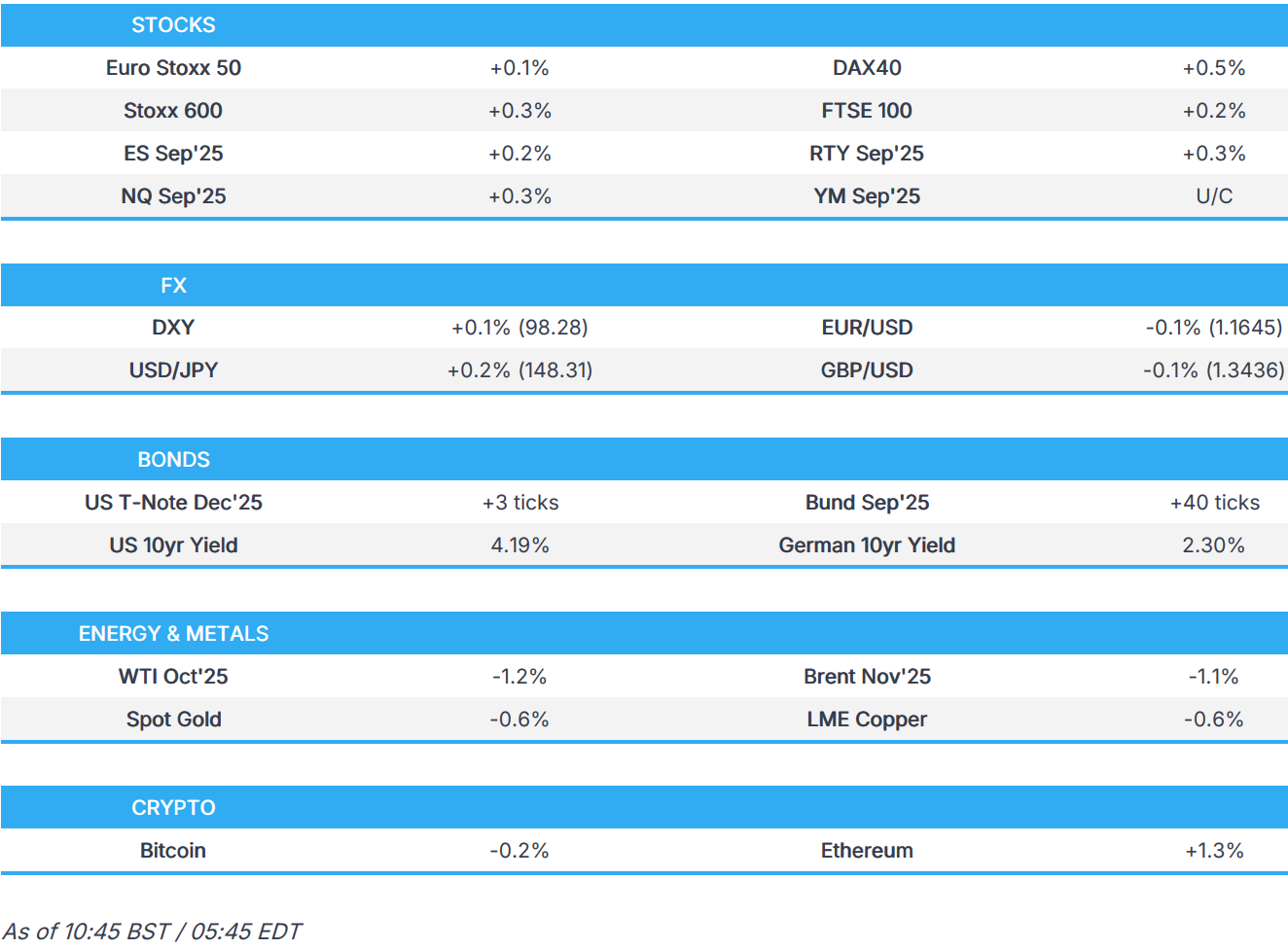

- European bourses and US equity futures are modestly firmer ahead of US data.

- USD awaits a data deluge, Antipodeans lag and JPY digests potential US/Japan auto tariff reduction.

- EGBs and Gilts bounce while USTs remain flat into data; Spanish auction was well received, whilst some short-lived pressure was seen on the French outing.

- Oil pulls back as traders brace ahead of this weekend's OPEC meeting; some upside in the complex seen after Russian Deputy PM Novak said OPEC-8 are not discussing production increase now.

- Looking ahead, US ISM Services PMI (Aug), ADP National Employment (Aug), Challenger Layoffs (Aug), Jobless Claims, Atlanta Fed GDP, Canadian Trade Balance (Jul), BoE DMP, Senate Banking Committee to hold hearing for US President Trump's Fed nominee Stephen Miran, Speakers including Fed’s Williams & RBA’s Hauser.

TARIFFS/TRADE

- China's Commerce Ministry announced anti-dumping duties on some types of US optical fibres, effective September 4th.

- Japan and the US in final stage of talks to implement lower tariffs on Japanese auto imports, according to Japanese sources cited by Reuters; reductions could take effect within 10-14 days after US presidential executive order. Japan and the US to issue joint statement on July trade accord, also MoU on rules for Japan's investment package. Japan aims to secure an executive order soon after the trade negotiator arrives in Washington.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) opened mixed and traded tentatively on either side of the unchanged mark, before sentiment improved a little to now show a mostly positive picture.

- European sectors opened mixed but now hold a slight positive bias. Travel & Leisure is found right at the foot of the pile, and is the clear underperformer today. Downside which has been driven by Jet2 (-14%), after the Co. provided an awful trading update, where it now sees EBIT at the lower end of its guided range. Healthcare also sits towards the foot of the pile, giving back some of the prior day’s losses, but also following an update from Sanofi (-8.7%); the Co. announced that amlitelimab met all primary and key secondary endpoints in the COAST 1 phase 3 study. Though analysts highlight that the efficacy of the drug did not meet expectations.

- US equity futures (ES +0.2%, NQ +0.3%, RTY +0.3%) are modestly firmer today, with the ES / NQ building on some of the strength seen in the prior session.

- Chinese firms are reportedly still keen on NVIDIA (NVDA) AI chips despite gov't pressure not to purchase them, via Reuters citing sources; NVIDIA's planned new China market chip is likely to be double the price of the H20. NVIDIA has assured Chinese firms that they do not need to worry about the availability of the H20.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is a touch higher after suffering on Thursday in the wake of a larger-than-expected decline in US job openings, which further added to the narrative that the labour market is continuing to cool. Today sees further jobs metrics from the US with ADP, weekly claims and Challenger lay-offs all due on deck. Elsewhere, ISM Services will be parsed for evidence of how tariffs are impacting the non-manufacturing industry and used as a proxy for Q3 growth. Fed speak today includes Williams, who will be speaking on the outlook for policy and the economy. Traders will also be mindful of Fed nominee Miran's appearance before the Senate Banking Committee. DXY delved as low as 98.07.

- EUR is steady vs. the USD and holding below its 50DMA at 1.1665 after a session of slight gains yesterday. Following a non-incremental Eurozone inflation release earlier in the week, newsflow for the Bloc has slowed down. We have heard from a slew of ECB speakers covering both the dovish and hawkish ends of the spectrum. French political tensions remain a part of the market narrative ahead of next Monday's confidence vote in PM Bayrou. A softer-than-expected outturn for EZ retail had little sway on price action. EUR/USD is currently caged within Wednesday's 1.1607-82 range.

- After clawing back some of its recent losses vs. the USD yesterday, the JPY is once again on backfoot with USD/JPY reverting back onto a 148 handle. Price action for the pair this week has been dictated by perceptions of the BoJ being non-committal to additional tightening and broader moves in the USD. JPY saw some mild support following source reporting via Reuters that Japan and the US are in the final stage of talks to implement lower tariffs on Japanese auto imports; reductions could take effect within 10-14 days after a US presidential executive order. USD/JPY has ventured as high as 148.41.

- GBP is slightly firmer vs. the USD after a steady start to the session with little follow-through from Wednesday's BoE TSC hearing, which saw policymakers broadly (ex-Taylor) reaffirm their cautious stance on additional easing given the risks surrounding the persistence of underlying inflation. The August DMP report showed expectations for year-ahead CPI inflation rose by 0.1ppts to 3.3% in the three months to August. Cable currently sits towards the top end of Wednesday's 1.3333-1.3458 range.

- Antipodeans are both softer vs. the broadly firmer USD after gaining vs. the greenback on Wednesday. With little follow-through seen from a larger-than-expected Australian goods balance during APAC trade, broader moves in the USD will likely dictate the state-of-play for both pairs.

- PBoC set USD/CNY mid-point at 7.1052 vs exp. 7.1405 (Prev. 7.1108).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTS are flat/incrementally firmer. In a very thin 112-16 to 112-22 bound. Numerous updates on the trade and Fed front overnight, but nothing that has fundamentally shifted the narrative as we await the Senate hearing on Miran’s appointment to the Fed and then numerous US data prints, which include ADP National Employment, Jobless Claims, ISM Services PMI.

- Bunds are firmer. Specifics for the region remain focussed on politics and supply. On the first point, French PM Bayrou is holding a meeting with the Socialist Party this morning, though the Socialists remain clear that they will not support Bayrou and the gathering is essentially a formality. As such, the base case firmly remains that Bayrou will lose Monday’s confidence vote, barring an 11th hour deal. On the supply front, Spain was well received and passed without incident. More pertinently, given the political situation, France sold the top-end of its forecast amount though the longer-dated cover was a little softer than is typically the case, seemingly weighing on OATs by around 10 ticks. Bunds at the upper end of a 129.27 to 129.70 band; was briefly held back on the French auction but has since continued to climb to fresh highs.

- Gilts moved in tandem with EGBs throughout the morning. Opened higher by just under 10 ticks before extending to gains of over 40 at best. Printing a 90.66 WTD high, looking to a double-top of 90.84 from last week. Press focus remains firmly on the Deputy PM. Given this, updates around the Autumn Budget have quietened down a touch. On Wednesday, Chancellor Reeves pushed back against some forecasts that the “black hole” in UK finances is GBP 50bln in size, remarks which also saw her reiterate commitment to the fiscal rules and describe a lot of the speculation around her taxation plans as “rubbish”.

- Spain sells EUR 5.49bln vs exp. EUR 4.5-5.5bln 1.40% 2028, 3.10% 2031, 4.20% 2037 Bono and EUR vs exp. EUR 0.25-0.75bln 1.00% 2030 I/L.

- France sells EUR 11bln vs exp. EUR 9.5-11bln 3.50% 2035, 3.60% 2042, and 3.75% 2056 OAT.

- UK sells GBP 800mln 0.625% 2045 I/L Gilt: b/c 3.91x (prev. 3.19x) & real yield 2.412% (prev. 2.23%).

- Click for a detailed summary

COMMODITIES

- Crude remains subdued after declining yesterday on OPEC+ headlines with the group reportedly mulling another oil production hike at Sunday’s meeting but with the decision not yet made. That being said, prices this morning found a floor after Russian Deputy PM Novak clarified OPEC-8 are not discussing production increase now, and no agenda has been set for the upcoming OPEC+ meeting yet. Novak added current market conditions and forecasts are to be considered. WTI currently resides in a 63.05-63.84/bbl range while Brent sits in a USD 66.67-67.41/bbl range.

- Softer trade across the board for precious metals despite a lack of fresh catalysts but with some possible profit-taking ahead of tomorrow's jobs report. Spot gold resides in a USD 3,511-3,564.15/oz range at the time of writing, with the next upside level being Wednesday's peak at USD 3,578.66/oz.

- Base metals are lower across the board despite a relatively rangebound dollar and mixed risk sentiment, although Chinese markets traded with low spirit overnight which could explain the similar sentiment in industrial commodities.

- Russian Deputy PM Novak says OPEC-8 are not discussing production increase now; no agenda has been set for the upcoming OPEC+ meeting yet; current market conditions and forecasts are to be considered.

- OPEC+ could weigh a 12-month phase-out of the cut, delegate sources told Argus, implying monthly increments of about 137k BPD; should this go ahead they expect a cautious approach, maintaining the flexibility to increase, pause, reduce or even reverse. There are also doubts over some countries' ability to ramp up production. Kazakhstan has been consistently overproducing and is near its maximum capacity. The unwinding of the cut "will amount to nothing more than 700,000-800,000 b/d at best", a delegate said. "If we bring it in a phased process, monthly increments will be around 60,000 to 70,000 b/d. The impact will be minimal," the delegate said.

- US Private Energy Inventories (bbls): Crude +0.6mln (exp. -2mln), Distillates +3.7mln (exp. -0.6mln), Gasoline -4.6mln (exp. -1.1mln), Cushing +2.1mln.

- Russia's Energy Minister said Rosneft signed a deal on additional supply of 2.5mln tons of oil to China via Kazakhstan.

- Russian Energy Minister says construction work on raising of existing Power of Siberia pipeline capacity to 44bcm (currently 38bcm) has already commenced, via Ria; adjustments to be made so maintenance does not occur in high demand periods

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Retail Sales YY (Jul) 2.2% vs. Exp. 2.4% (Prev. 3.1%); EU Retail Sales MM (Jul) -0.5% vs. Exp. -0.2% (Prev. 0.3%)

- EU HCOB Construction PMI (Aug) 46.7 (Prev. 44.7); German HCOB Construction PMI (Aug) 46.0 (Prev. 46.3); Italian HCOB Construction PMI (Aug) 47.7 (Prev. 48.3); French HCOB Construction PMI (Aug) 46.7 (Prev. 39.7)

- UK S&P Global Construction PMI (Aug) 45.5 (Prev. 44.3)

- Swedish CPIF Ex Energy Flash YY (Aug) 2.9% vs. Exp. 3.1% (Prev. 3.2%); CPIF Flash YY (Aug) 3.3% vs. Exp. 3.2% (Prev. 3.0%)

- Swiss CPI MM (Aug) -0.1% vs. (exp. 0.0%, prev. 0.0%); CPI YY (Aug) 0.2% vs. Exp. 0.2% (Prev. 0.2%)

NOTABLE EUROPEAN HEADLINES

- Germany's IFW says 2025 GDP expected at 0.1%, 2026 at 1.3% and 2027 at 1.2%. Unemployment expected to decline to 5.8% from 6.3% this year.

- RWI forecasts that the German economy will grow 0.20% in 2025 (prev. saw 0.30%); sees 1.1% in 2026 (prev. saw 1.5%).

- Ifo Institute for Economic Research lowers 2025 German economic growth forecast to 0.2% (prev. saw 0.3%); cuts 2026 forecast to 1.3% (prev. saw 1.5%).

- BoE Monthly Decision Maker Panel data - August 2025: In the three months to August, firms reported that their year-ahead own-price inflation was expected to be 3.7%, unchanged from the three months to July. Expectations for year-ahead CPI inflation rose by 0.1 percentage points to 3.3% in the three months to August.

- Riksbank's Jansson says underlying inflation pressures do not look too dramatic. There is a risk that temporary inflation effects could become more persistent if they find a way into price-setting behaviour, wages, and inflation expectations. A situation with higher inflation is much worse than a slightly delayed economic recovery. Being on top of the inflationary issue, "even though we are optimistic", is important. Don't need to hit 2% exactly before bank can cut, but need confirmation that inflation is temporary and, on the way, down.

NOTABLE US HEADLINES

- BofA Institute total card spending +2.8% Y/Y in week ending August 30th (vs +1.8% July average); Spending growth for pre-Labor Day at 1.9%, supporting a Q3 rebound.

- US House Republicans are reportedly less than eager to extend Obamacare subsidies which expire at the end of the year, via Punchbowl; a GOP aide cited said an extension is “Incredibly unpopular within the conference, expensive, bad policy, etc.,”

- US Republicans are looking into and/or speaking out against the administration's plan to use the CHIPS Act to take a stake in Intel (INTC), via Punchbowl; Senator Rounds is looking into its legality while Young is said to be sceptical.

GEOPOLITICS

MIDDLE EAST

- Israel reportedly conducted a strike on Hezbollah terrorist infrastructure in Ansariyah in southern Lebanon, according to Visegrad 24 via X.

- "The "Gideon 2 vehicles" operation in Gaza may extend to a full year", via Sky News Arabia citing Yedioth Ahronoth's miliary sources

RUSSIA-UKRAINE

- US President Trump said he will find out over the next week or so how good the relationship is with Russia, while he also commented that the US will help Poland protect itself with US soldiers to remain in Poland and will put more there if they want. Furthermore, Trump said he will be talking to Ukrainian President Zelensky shortly in the next days, as well as implied 2nd and 3rd phases of Russian oil sanctions.

- Russia said security guarantees sought by Ukraine are "guarantees of danger to the European continent". It was separately reported that a Russian Foreign Ministry spokeswoman said allegations of Russia being behind European Commission President Von der Leyen's plane incident is fake and paranoia.

- North Korean leader Kim and Russian President Putin held a meeting in Beijing where Putin highly praised North Korean soldiers fighting in Kursk and Kim expressed thanks, while Kim told Putin that North Korea would continue to support Russia and the leaders reaffirmed they would keep bilateral relations at a high level, according to KCNA.

- Ukrainian President Zelensky is expected to have a one-on-one meeting with US Envoy Witkoff on Thursday, according to Reuters sources.

- WSJ's Norman posts "any claim that Europe is “ready” on its part in security guarantees is a very significant exaggeration."

CRYPTO

- Bitcoin is a little weaker today and trades around USD 110.5k whilst Ethereum is firmer and trades just shy of the USD 4.4k.

APAC TRADE

-

APAC stocks followed suit to the mixed performance stateside, where tech and communications outperformed following the Google antitrust ruling, and participants digested dovish data and Fed rhetoric.

- ASX 200 advanced with the gains led higher by outperformance in the top-weighted financial sector and with tech stocks inspired by US counterparts.

- Nikkei 225 outperformed despite light catalysts, although Japan's trade negotiator Akazawa is scheduled to visit the US from today, while he noted that administrative issues have been resolved and will continue to push for a presidential order for what has been agreed on tariffs.

- Hang Seng and Shanghai Comp were pressured following a report that China is said to consider curbs on stock speculation to foster steady gains, while US-China frictions resurfaced following US President Trump's comments during the Victory Day parade and with China announcing anti-dumping duties on optical fibre from the US.

NOTABLE ASIA-PAC HEADLINES

- China is said to consider curbs on stock speculation to foster steady gains, according to Bloomberg.

- China's Global Times, on Nasdaq exchange's proposed changes to its listing standard, says “The proposed rule could be seen as targeted or discriminatory, potentially restricting Chinese companies, especially tech firms, from listing in the US,”.

- China's DeepSeek is reportedly targeting AI agent release by year-end, according to Bloomberg.

- UMC (2303 TT) reports August 2025 revenue -7.2% Y/Y.

DATA RECAP

- Australian Balance on Goods (Jul) 7,310M vs Exp. 5,000M (Prev. 5,365M)

- Australian Goods/Services Imports (Jul) -1.3% (Prev. -3.1%); Exports (Jul) 3.0% (Prev. 6.0%)