US Market Open: DXY is firmer whilst USTs trade on the backfoot into US CPI, EUR awaits the ECB

11 Sep 2025, 11:00 by Newsquawk Desk

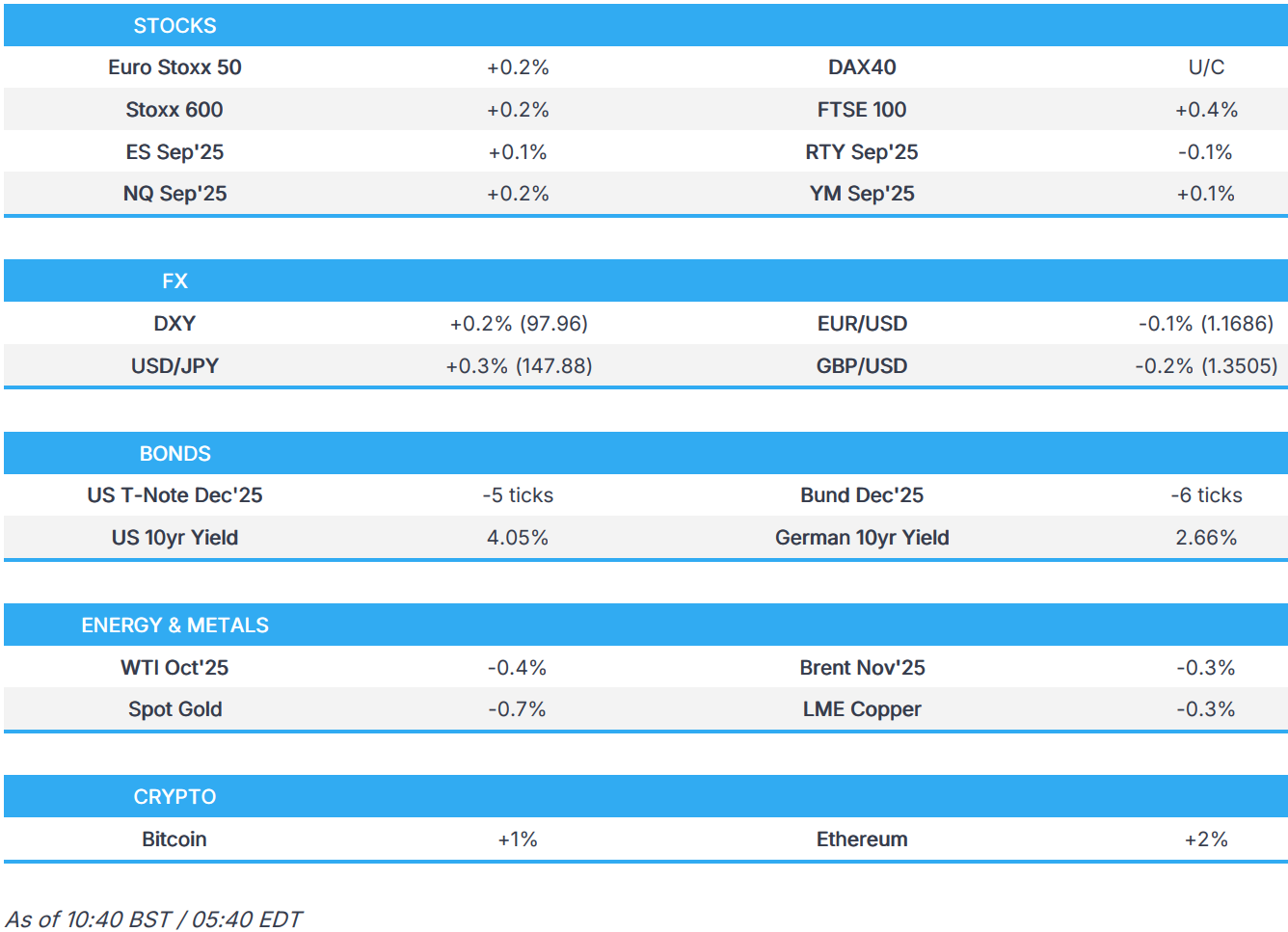

- European bourses are modestly firmer, whilst US equity futures are mixed ahead of the ECB and US CPI.

- DXY is firmer and towards session highs; JPY underperforms, with USD/JPY rising to just shy of the 148.00 mark.

- USTs and Bunds are a touch softer into ECB/US CPI and a 30-year auction following a strong 3- and 10-year outing earlier this week.

- Industrial commodities and gold are subdued, awaiting key risk events; some modest upticks seen on Poland, Ukraine & Lithuania, calling the recent Russian drone incursion an “unprecedented” provocation.

- Looking ahead, US CPI (Aug) & Jobless Claims, ECB Policy Announcement & Press Conference, CBRT Announcement, OPEC Monthly Report, Supply from the US, and Earnings from Adobe.

TARIFFS/TRADE

- South Korean President Lee said there will be more ways to negotiate with the US, and a final conclusion on trade negotiations with the US is expected to be rational, while he added they are in discussions with the US to operate visa systems normally and that Korean businesses will now be hesitant about investing in the US following the immigration raid. Lee also noted that various factors are involved in trade negotiations with the US, including nuclear material reprocessing and defence costs. Furthermore, South Korea's Industry Minister is to travel to the US today for follow-up trade negotiations.

- US President Trump reportedly halted the deportation of Korean workers to encourage them to train Americans, and Seoul officials said Trump gave those at the Hyundai Motor (005380 KS)-LG Energy Solution (373220 KS) battery plant an option to stay, according to FT.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.4%) are modestly firmer across the board, with some outperformance in the CAC 40 (+0.7%).

- European sectors hold a strong positive bias, albeit with the breadth of the market fairly narrow. There are only a handful of industries holding marginally in the red. Retail is once again leading the pile, continuing the strength seen in the prior session. Energy follows closely behind, and Construction & Materials completes the top three.

- US equity futures are mixed with the ES/NQ posting modest gains, whilst the RTY is slightly on the back foot. Price action so far has been non-committal, heading into the US CPI report.

- Citi European Equity Strategy; Upgrades: Retail to Overweight from Neutral; Financial Services to Neutral from Underweight; Telecoms to Neutral from Underweight. Downgrades: Media to Neutral from Overweight.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is fractionally higher following an indecisive session on Wednesday in the wake of soft PPI metrics and in the run-up to today's CPI report. Expectations are for core M/M CPI to remain at 0.3% with the Y/Y rate seen holding steady at 3.1%. As such, the desk notes that the report "reinforces confidence that the upcoming CPI print is unlikely to exceed 0.3% M/M". Elsewhere on the data slate are the weekly jobs figures with initial claims expected to slip to 235k from 23k. DXY has ventured as high as 97.96 with attention on a test of 98.00; not breached since 5th September.

- EUR is steady vs. the USD ahead of the latest ECB policy decision, which is widely expected to see policymakers stand pat on the Deposit Rate at 2%. These expectations come off the back of the EU-US trade agreement, resilient growth in the face of trade tensions and a modest uptick in inflation. Ahead focus will be on clarity on the split of the Governing Council and any potential guidance on the monetary policy path. EUR/USD has slipped back onto a 1.16 handle but is holding above Wednesday's low at 1.1683.

- JPY sits at the bottom of the G10 leaderboard and has extended its mild losses vs. the USD seen on Wednesday. From a macro perspective, today's session has been lacking in Japanese-specific updates, but traders remain mindful of political risk and its potential impact on the BoJ. USD/JPY has ventured as high as 147.96 with focus on a test of 148 to the upside.

- GBP is a touch softer vs. the USD as incremental macro drivers for the UK remain on the light side. Concerns over longer-term UK borrowing costs have temporarily abated with the 30yr yield having pulled back to circa 5.48% from its recent multi-decade high at 5.752% printed on 3rd September. GBP/USD is currently holding above the 1.35 mark after basing out at 1.3502.

- Antipodeans are both marginally softer vs. the USD with not much in the way of incremental newsflow for the pair.

- PBoC set USD/CNY mid-point at 7.1034 vs exp. 7.1157 (Prev. 7.1062)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are softer, as was the case at this point on Wednesday. Once again, the action is relatively modest in nature as the complex awaits CPI and thereafter 30yr supply. Into the above, USTs at the low end of a 113-12 to 113-15+ band. Entirely within Wednesday’s 113-05 to 113-20 parameters; as a reminder, PPI drove USTs higher, but the mentioned peak printed a few hours later after the strong 10yr auction.

- Bunds began the morning firmer by 14 ticks at best, notching a 129.28 peak and matching Tuesday’s high but stopping shy of 129.33 and 129.44 from Monday and Wednesday respectively. However, initial impetus faded into the European cash equity open. A move that occurred alongside a broader modest pullback in the fixed income space and as the USD strengthened. No fresh fundamental catalysts emerged at the time. All focus now turns to the ECB. The Deposit Rate is expected to be maintained at 2.00%. Focus for the meeting will be on any insight into the divide between the doves/hawks, a point that could become starker depending on how the 2026 inflation forecast develops, with desks of the view that it will tick higher from 1.6% but remain beneath the 2% target.

- Gilts saw a softer start to the day, opened lower by just under 10 ticks and then slipped further to notch a 91.22 low. Action that followed the modest bearish bias that was in play for peers at that point. Since, Gilts have managed to lift off this low and move into the green, higher by near 15 ticks at best but stalling 11 ticks shy of Wednesday’s 91.58 peak. Upside that comes as Gilts are perhaps able to trade a little more freely than peers, as the UK docket is a very light one.

- UK DMO sells GBP 1bln 4.25% 2032 Gilt; b/c 3.72, average yield 4.206%.

- Italy sells EUR 3.25bln vs exp. EUR 2.75-3.25bln 2.35% 2029 & EUR 1.5bln vs exp. EUR 1.25-1.5bln 4.00% 2030 BTP.

- Click for a detailed summary

COMMODITIES

- Crude was subdued in early European hours following an uneventful APAC session and after their recent advances, which were facilitated by geopolitical developments in the Middle East and Eastern Europe, with an uplift seen after comments from US President Trump, who posted "What’s with Russia violating Poland’s airspace with drones? Here we go!". The modest downside comes amid a cautious mood ahead of US CPI and ECB, whilst this morning the IEA raises its 2025 world oil demand growth forecast to 740k BPD (prev. 680k BPD), and maintains its 2026 forecast at 700k BPD. Some modest upside seen on commentary via Poland, Ukraine and Lithuania who said the Russian drone incursion is an unprecedented provocation. WTI currently resides in a narrow 63.34-63.80/bbl range while Brent sits in a USD 67.21-67.62/bbl range.

- Mixed trade across precious metals, with gold and silver taking a breather following recent advances ahead of US CPI. Spot gold currently resides in a USD 3,614.32-3,649.35/oz range and within Wednesday's USD 3,620.13-3,657.61/oz range. All-time high still sits at USD 3,674.69/oz printed on 9th September.

- Copper futures gradually pulled back from Wednesday's peak and eventually the USD 10k/t mark, with price action contained alongside the cautious risk sentiment heading into US CPI and the ECB, with the latter expected to hold rates at 2% for a second meeting. Attention will centre on guidance regarding further easing and the split of views on the Governing Council.

- IEA OMR: IEA raises 2025 world oil demand growth forecast to 740k BPD (prev. 680k BPD); 2026 growth forecast maintained at 700k BPD.

- Saudi Aramco has reportedly asked buyers to lift more October oil after recent deeper-than-expected price cuts, according to Reuters sources.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK RICS Housing Survey (Aug) -19.0 vs. Exp. -10.0 (Prev. -13.0)

- Swedish CPIF MM (Aug) -0.2% vs. Exp. -0.2% (Prev. -0.2%); YY (Aug) 3.2% vs. Exp. 3.3% (Prev. 3.3%)

NOTABLE EUROPEAN HEADLINES

- UK Chancellor commits to exploring pro-growth tax reforms to support small businesses expanding operations.

- Germany's BGA Trade Association says German exports are expected to fall 2.5% in 2025 and imports to rise 4.5%.

NOTABLE US HEADLINES

- US President Trump's administration appealed the court ruling blocking the removal of Fed Governor Cook.

GEOPOLITICS

MIDDLE EAST

- Qatar said it condemns Israeli PM Netanyahu's explicit threats of future violations to state sovereignty, and it will work with its partners to ensure Netanyahu is held accountable.

- US President Trump reportedly had a heated call with Israeli Prime Minister Benjamin Netanyahu on Tuesday regarding the Israeli strike in Qatar, according to senior US administration officials cited by WSJ.

- US Pentagon approved an estimated USD 14.2mln presidential drawdown authority package for Lebanon, which will build the capacity of Lebanese armed forces to dismantle weapons caches and military infrastructure of non-state groups, including Hezbollah.

- Doha is to host emergency Arab-Islamic summit on Sunday and Monday amid discussions over Israeli attacks on Gaza, according to the Qatar News Agency.

RUSSIA-UKRAINE

- French President Macron said he discussed with US President Trump the troubling developments in Russia's war of aggression against Ukraine.

- The UN Security Council was asked by five members to meet on Friday over Russia's violations of Polish airspace.

- EU said sanctions against Russia are to be increased significantly, and the EU foreign policy chief commented that the serious violation of European airspace strengthens their resolve to support Ukraine.

- Foreign ministers of Poland, Ukraine and Lithuania warn of deliberate Russian drone incursion, call it unprecedented provocation. Ministers urge partners to bolster Ukraine's air defence and extend support to Lithuania and Poland amid escalating tensions

OTHER

- South Korean President Lee said North Korea's reaction has been cold but stated that no matter how North Korea reacts, easing tensions will benefit South Korea, while he added North Korea's nuclear and missile programs are a complex issue directly involving the US. Furthermore, he said South Korea doesn't necessarily have to lead in improving relations with North Korea and that US President Trump can have the most powerful influence on North Korea issues, as well as noted that they will keep trying to restore trust with North Korea.

- North Korea's leader Kim is believed to be expanding ties with China following his visit to China, and there is a higher chance that China will support North Korea via unofficial trade, according to South Korean lawmakers citing South Korea's spy agency.

- The Philippines Foreign Ministry strongly protested the recent approval by China's State Council of the establishment of the Kuanyan Island National Nature Reserve, and urged China to respect the sovereignty and jurisdiction of the Philippines over Scarborough Shoal, while the Philippines also urged China to refrain from enforcing and immediately withdraw its State Council issuance.

CRYPTO

- Bitcoin is a little firmer and trades just shy of USD 114k whilst Ethereum posts larger gains and jumps past USD 4.4k.

APAC TRADE

- APAC stocks followed suit to the mixed performance stateside, where the S&P 500 and Nasdaq printed fresh record highs after cooler-than-expected PPI data, but with some cautiousness seen as participants braced for the incoming US CPI report.

- ASX 200 was subdued in the absence of any notable data or drivers, and with the downside led by healthcare, consumer discretionary and financials.

- Nikkei 225 returned to above the 44,000 level and extended on record highs despite mixed data.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark dragged lower by pharmaceutical stocks after reports that the US is considering severe restrictions on medicines from China, while the mainland was underpinned after recent policy pledges by China's state planner.

NOTABLE ASIA-PAC HEADLINES

- BoJ is firming up a strategy to unload its huge ETF holdings and is centring on gradual market sales, according to sources cited by Reuters, who added there is no consensus yet on the timing, with political uncertainty complicating the decision.

- South Korean President Lee held a conference on his first 100 days in office, where he stated the domestic economic indicators are showing signs of recovery and the stock market is recovering at a fast pace, while he added that measures on stabilising property prices will continue to be rolled out. Lee said unreasonably undervalued stocks are prevalent in the South Korean market and tax policies can be modified to revitalise stock markets, but noted that capital gains tax rules will not change, and he will leave it to Parliament to decide on capital gains tax rules. Furthermore, he said it is time for expansionary fiscal policy to achieve economic growth, even if it raises national debt.

- China is said to be mulling aiding local governments with USD 1tln of bills, according to Bloomberg sources. Chinese government reportedly considers directing state lenders and policy banks to provide loans to local authorities for overdue payments.

- Japan LDP senior member Takaichi confirmed that they will be running for LDP leadership, via Newsjp.

DATA RECAP

- Japanese Corp Goods Price MM (Aug) -0.2% vs. Exp. -0.1% (Prev. 0.2%, Rev. 0.3%); YY (Aug) 2.7% vs. Exp. 2.7% (Prev. 2.6%, Rev. 2.5%)

- Japanese Business Survey Index (Q3) 3.8% (Prev. -4.8%)