Europe Market Open: Mild upward bias in Europe as Wall Street sentiment reverberates

12 Sep 2025, 07:06 by Newsquawk Desk

- US Treasury Secretary Bessent will meet with Chinese Vice Premier He and other senior Chinese officials next week in Madrid, while Bessent and He are to discuss key US-China national security, economic and trade issues.

- US President Trump's administration asked the US appeals court to pause a ruling that blocked the removal of Fed's Cook.

- ECB rate cut debate is said to not be over, but October is seen as too soon, and the next real discussion is more likely in December, according to Reuters sources.

- APAC stocks were mostly higher following the gains on Wall St; European equity futures indicate a marginally positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed with gains of 0.5% on Thursday.

- Looking ahead, highlights include German CPI Final (Aug), UK GDP (Jul), French Final CPI (Aug), Spanish Final CPI (Aug), US University of Michigan Prelim (Sep), CBR Announcement, ECB Publication of ECB staff macroeconomic projections for the euro area, Credit Rating Reviews for France & Spain.

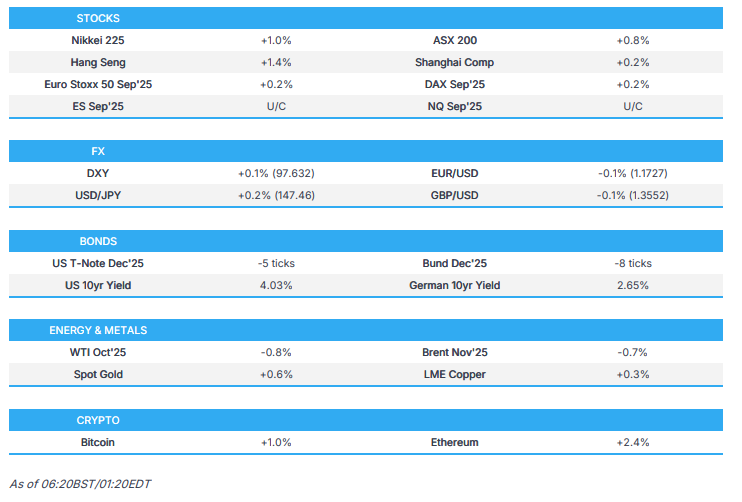

SNAPSHOT

US TRADE

EQUITIES

- US stocks gained despite an initial choppy reaction in equity futures to US data releases in which CPI printed broadly in line (ex. headline M/M, which was hot), while initial jobless claims soared to 263k (exp. 235, prev. 236k) and continued to add to the economic concerns around the labour market. As such, Fed money market pricing moved more dovish, with 73bps of easing priced in by year-end vs. 68bps pre-data and all main indices gained, despite the initial two-way price action.

- SPX +0.85% at 6,587, NDX +0.60% at 23,993, DJI +1.36% at 46,108, RUT +1.83% at 2,422.

- Click here for a detailed summary.

TARIFFS/TRADE

- US Treasury Secretary Bessent will travel to Spain and the UK on September 12th-18th on a trip that includes government and private sector meetings in London. Bessent will meet with Chinese Vice Premier He and other senior Chinese officials next week in Madrid, while Bessent and He are to discuss key US-China national security, economic and trade issues, including TikTok and anti-money-laundering cooperation. Furthermore, Bessent will also meet with Spanish government counterparts to discuss the US-Spain relationship and is to join US President Trump in the UK for an official state visit with King Charles.

- China's Commerce Ministry said planned Mexican tariffs on China are to seriously affect Mexico's business environment and confidence of enterprises in investing in Mexico, while it added that China will take necessary measures to safeguard legitimate rights and interests.

- Taiwan said it will continue advanced talks with the US and seeks more equitable reciprocal trade terms with the US, while Taiwan and the US affirmed that some progress was made in trade talks.

- US President Trump's nominee for ambassador to India said the US is on track to resolve "hiccups" in the relationship with India, and President Trump has been crystal clear that India must stop buying Russian oil.

NOTABLE HEADLINES

- US President Trump's administration asked the US appeals court to pause a ruling that blocked the removal of Fed's Cook.

- US Treasury Secretary Bessent met this week with Warsh, Lindsey, and Bullard as the search for the next Fed chair continues, while he is waiting for the end of the Fed blackout to speak with sitting Fed officials, and the goal is to add one or two names to candidates Trump has already mentioned, a group that includes 11 economists.

- GOP leaders reportedly eye stopgap funding until November 21st, according to Politico.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher following the gains on Wall St, where the major indices climbed to record highs after a jump in Initial Jobless claims further boosted Fed rate cut pricing.

- ASX 200 edged higher with outperformance in Real Estate, Miners, Materials & Financials spearheading the advances as Fed rate hike expectations boost global risk sentiment.

- Nikkei 225 extended on record highs and approached closer towards the 45,000 level despite little fresh pertinent drivers.

- Hang Seng and Shanghai Comp traded mixed with tech leading the gains in Hong Kong after it was reported that Alibaba (9988 HK) and Baidu (9888 HK) are using internally designed chips for training AI models are to adopt their own AI chips in a major shift for Chinese tech, while the mainland lagged amid frictions, with the US reportedly to urge G7 to impose high tariffs on China and India over Russian oil purchases.

- US equity futures took a breather after advancing on soft jobs-related data and a subsequent boost in Fed rate cut bets.

- European equity futures indicate a marginally positive cash market open with Euro Stoxx 50 futures up 0.2% after the cash market closed with gains of 0.5% on Thursday.

FX

- DXY attempted to nurse some losses after suffering yesterday as participants reacted to soft labour data in which the initial jobless claims were higher than expected and subsequently spurred Fed rate cut bets with around 71bps of cuts currently priced in by year-end, while CPI figures somewhat took a back seat and largely matched estimates.

- EUR/USD held on to most of its recent spoils after benefitting from a weaker buck and following the ECB meeting, where the central bank unsurprisingly kept rates unchanged and Lagarde provided a somewhat more hawkish tone.

- GBP/USD slightly eased back from the prior day's highs amid light pertinent newsflow and as the attention turns to incoming data from the UK, including monthly GDP, as well as industrial and manufacturing production.

- USD/JPY gradually edged higher as the dollar regained composure and amid a lack of haven demand for the yen.

- Antipodeans plateaued overnight and held on to recent spoils alongside the widespread constructive mood

- PBoC set USD/CNY mid-point at 7.1019 vs exp. 7.1081 (Prev. 7.1034).

FIXED INCOME

- 10yr UST futures were subdued after having faded the spike seen following yesterday's surge in Initial Jobless Claims.

- Bund futures lacked direction and were stuck around the 129.00 focal point where prices have oscillated around throughout this week, and with demand also not helped following the hawkish commentary by ECB's Lagarde at the post-meeting press conference, while ECB source reports essentially ruled out prospects of an October rate cut.

- 10yr JGB futures mildly declined amid the record highs in Japanese stock markets and weaker demand at today's enhanced-liquidity auction.

COMMODITIES

- Crude futures continued to decline after recently snapping a 3-day win streak amid a lack of energy newsflow, although it was reported overnight that the US is to urge G7 to impose high tariffs on China and India over Russian oil purchases, while Japan announced to lower the price cap on Russian crude oil.

- Canada is in talks with energy firms and Alberta that could result in the scrapping of the federal oil and gas emissions cap. In exchange, Canada would seek renewed progress towards cutting the energy industry's carbon footprint.

- Spot gold steadily gained after recent dollar weakness and in tandem with a rally in silver, which climbed above the USD 42/oz level.

- Copper futures remained firmer alongside the mostly positive mood across global markets.

CRYPTO

- Bitcoin trickled lower after failing to sustain an early advance above the USD 116k level.

NOTABLE ASIA-PAC HEADLINES

- Japanese and US finance ministers' joint statement noted as trusted partners, the United States Department of the Treasury and the Japanese Ministry of Finance agreed to continue their close consultations on macroeconomic and foreign exchange matters, while they reaffirmed that exchange rates should be market-determined and that excess volatility can have adverse implications for economic and financial stability.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu signed an agreement to significantly expand West Bank settlement near Jerusalem.

- Israel's UN envoy to the Security Council said Israel will act against the leaders of terror wherever they are hiding.

- Qatar's PM said to the UN Security Council that the Israeli attack on Hamas leaders in Doha is a violation of Qatar's sovereignty, and the attack, which was carried out while we are engaged in mediation, exposes Israel's intentions to derail peace efforts. Furthermore, Qatar's PM said Israeli leaders show no regard for hostages' lives and Qatar will continue its humanitarian and diplomatic role to spare bloodshed, but will not tolerate any infringement on sovereignty and security.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said he discussed sanctions against Russia and potential joint weapons production with US envoy Kellogg.

- The US is to urge G7 to impose high tariffs on China and India over Russian oil purchases, while finance ministers from G7 leading economies will discuss a US proposal for a round of new measures on Friday, according to FT.

- EU officials say it is unlikely G7 will impose 100% tariffs on China and India as India is a vital partner in trade and security matters, according to FT.

- Japan's Chief Cabinet Secretary Hayashi said Japan is to impose additional asset freeze, export controls, and sanctions on Russia over Moscow's invasion of Ukraine, while he added they are to lower the price cap on Russian crude oil from today.

- Japan's Trade Ministry said they are to restrict exports to additional entities, including six in China, two in Turkey, and one in the UAE, as part of sanctions against Russia's invasion of Ukraine.

EU/UK

NOTABLE HEADLINES

- ECB rate cut debate is said to not be over, but October is seen as too soon, and the next real discussion is more likely in December, according to Reuters sources.

- ECB policymakers are convinced that no further interest-rate cuts are needed to deliver 2% inflation, despite new economic projections pointing to an undershoot over the next two years, according to Bloomberg sources who added that unless the EZ experiences another major shock, borrowing costs are set to stay where they are for some time. Furthermore, it was noted that while a reduction at October’s meeting can be virtually ruled out, December will be an opportunity to reassess as fresh quarterly forecasts will include 2028, and the reluctance for additional monetary loosening matches the views of investors, who are leaning against any more cuts.