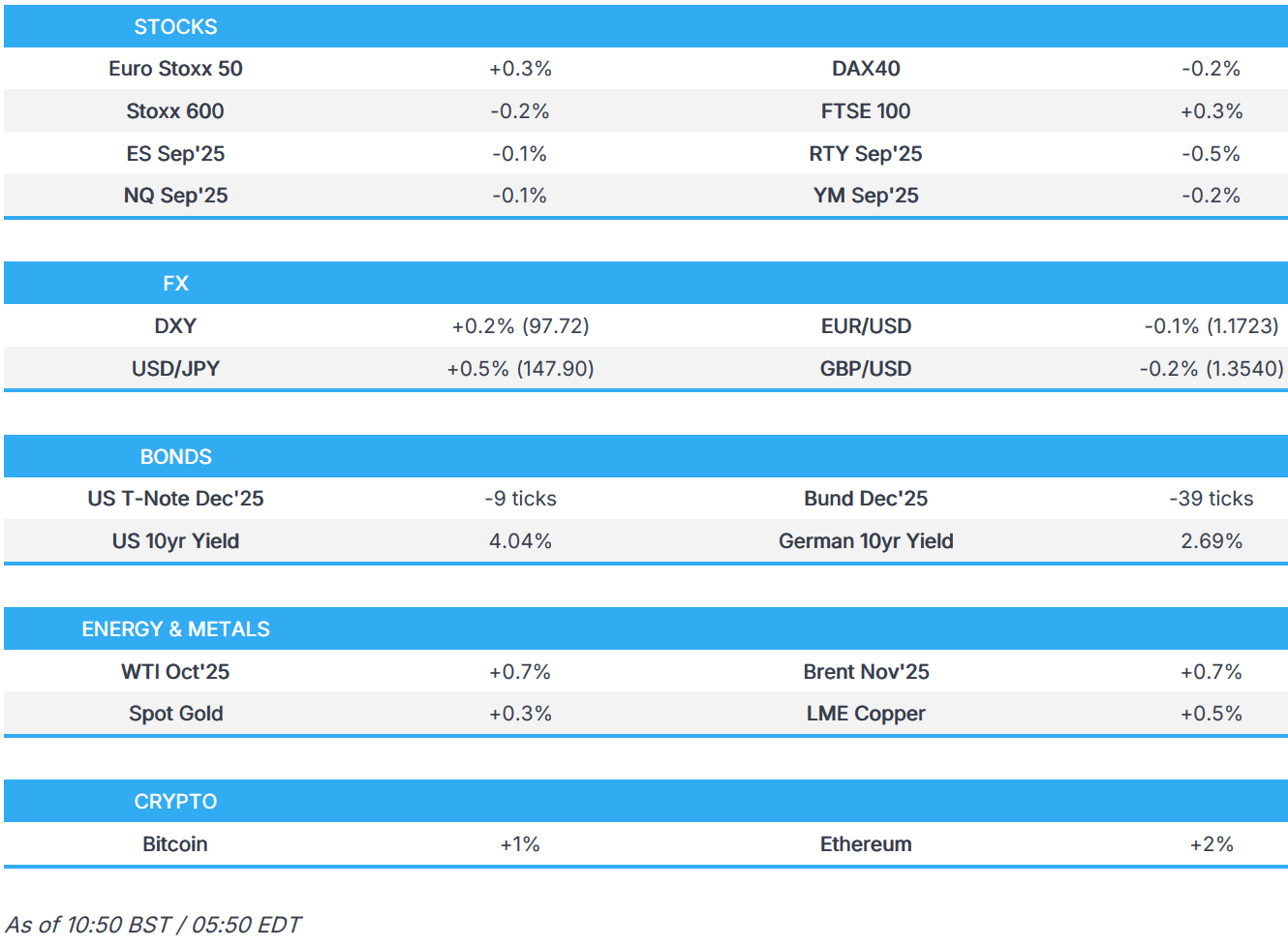

US Market Open: US equity futures are modestly lower, DXY mildly gains whilst Gilts outperform post-GDP

12 Sep 2025, 10:58 by Newsquawk Desk

- US Treasury Secretary Bessent will meet with Chinese Vice Premier He and other senior Chinese officials next week in Madrid, while Bessent and He are to discuss key US-China national security, economic and trade issues.

- US equity futures are lower across the board, RTY lags. European bourses began marginally firmer, but have since waned.

- USD attempts to recover from the pressure seen on Thursday's data, DXY at highs, while the JPY lags.

- Fixed income is in the red, though USTs are set to end the week near-enough unchanged. Gilts are the relative outperformer post-GDP.

- Crude began in the red, extending to a new WTD low before bouncing and recouping some of Thursday's pressure. Metals firmer despite the USD strength.

- Looking ahead, highlights include US University of Michigan Prelim (Sep), CBR Announcement, Credit Rating Reviews for France & Spain. US President Trump on Fox.

TARIFFS/TRADE

- US Treasury Secretary Bessent will travel to Spain and the UK on September 12th-18th on a trip that includes government and private sector meetings in London. Bessent will meet with Chinese Vice Premier He and other senior Chinese officials next week in Madrid, while Bessent and He are to discuss key US-China national security, economic and trade issues, including TikTok and anti-money-laundering cooperation. Furthermore, Bessent will also meet with Spanish government counterparts to discuss the US-Spain relationship and is to join US President Trump in the UK for an official state visit with King Charles.

- China's Commerce Ministry said planned Mexican tariffs on China are too seriously affect Mexico's business environment and confidence of enterprises in investing in Mexico, while it added that China will take necessary measures to safeguard legitimate rights and interests.

- Taiwan said it will continue advanced talks with the US and seeks more equitable reciprocal trade terms with the US, while Taiwan and the US affirmed that some progress was made in trade talks.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.3%) opened modestly firmer across the board, but sentiment slipped as the morning progressed to display a negative picture – nothing really behind the turn.

- European sectors are split down the middle, and with little overall newsflow driving this at the moment. Basic Resources takes the top spot, buoyed by strength in underlying metals prices. Insurance and Utilities follow closely behind. Autos is found at the foot of the pile, and then joined by Retail and Energy.

- US equity futures (ES -0.1%, NQ -0.1%, RTY -0.5%) are lower across the board, with some underperformance in the RTY, paring back some of the strength seen in the prior session.

- Japan to provide up to JPY 536bln subsidy for Micron's (MU) Hiroshima plant expansion, according to JiJi.

- EU Commission accepts commitments offered by Microsoft (MSFT) to address competition concerns related to Teams. Microsoft will offer Office 365 and Microsoft 365 suites without Teams at a reduced price, and allow long-term license holders to switch.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is attempting to claw back some lost ground after declining on Thursday in the wake of the jump in US weekly claims data, which overshadowed the mostly in-line/slightly firmer (on an underlying basis) CPI report. Pricing for next week's FOMC rate decision was largely unchanged with markets reluctant to price a 50bps reduction. With regards to personnel at the Fed, the latest reporting suggests US Treasury Secretary Bessent met this week with Warsh, Lindsey, and Bullard as the search for the next Fed chair continues. Ahead, focus is on UoM data for September. DXY sits towards the bottom end of Thursday's 97.47-98.08 range.

- EUR is steady vs. the USD after gaining yesterday in the wake of a broadly softer dollar and what turned out to be a hawkish ECB policy announcement. Source reporting has suggested that an October cut is very unlikely. However, the matter could be revisited in December alongside the latest economic projections. We have heard from a slew of ECB speakers this morning, who have largely echoed Lagarde's remarks that policy is in the right place. Afterhours, focus will be on Fitch's review of France. EUR/USD ventured as high as 1.1747 before pulling back. If upside resumes, the WTD peak sits at 1.1780.

- JPY is softer vs. the USD and at the bottom of the G10 leaderboard. Focus this week for Japan has primarily been on the fallout from political uncertainty after PM Ishiba announced his resignation, with pressure this morning potentially exacerbated by the Kyodo poll. The inference for markets has been that the upheaval in Japan could derail BoJ tightening expectations. Elsewhere, a joint statement between the US and Japan has reaffirmed their commitment to close consultations on foreign exchange matters and reaffirmed that exchange rates should be market-determined. USD/JPY is currently contained within Thursday's 146.98-148.19 range.

- GBP is on the backfoot vs. the USD following an in-line M/M outturn for UK GDP at 0%, leaving the 3M/3M rate at 0.2%, as expected. Looking ahead, Pantheon expects "GDP growth will probably undershoot the MPC’s forecast for Q3 slightly after today’s release, but that should have little effect on interest rates". Cable sits towards the middle of Thursday's 1.3490-1.3583 range.

- Antipodeans are both softer vs. the USD after faltering alongside the pullback in risk sentiment in early European trade. Macro drivers for both remain on the light side and as such, the risk environment and broader moves in the USD are likely to provide the greatest source of traction for AUD/USD and NZD/USD.

- PBoC set USD/CNY mid-point at 7.1019 vs exp. 7.1081 (Prev. 7.1034).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A softer start to the final session of a packed week. Today’s docket is a little lighter stateside, University of Michigan is the main data event while scheduled speakers are light aside from POTUS on Fox at 13:00BST, an interview likely to focus on Charlie Kirk. Currently, USTs are lower by a handful of ticks in a thin c. five tick range which is comfortably within Thursday’s 113-09 to 113-29 band. September aside, Treasury Secretary Bessent met this week with Warsh, Lindsey, and Bullard regarding the Chair position. Will be speaking with sitting officials’ post-blackout. His goal is to add one or two names to the list of candidates.

- Bunds are softer, continuing to pullback from the 129.38 peak that printed yesterday in reaction to US weekly claims. Entered today’s session just above the 129.00 mark but has since slipped below the figure and is at a 128.84 trough. Very much focussed on the post-ECB sources. In short, a move in October is off the cards (-1.3bps implied) with policymakers generally of the view that further easing is not required to get inflation to the 2.0% target; however, the December meeting (-3.8bps implied) is the point to review this when new forecasts will be available including the first look at 2028. ECB speak today has been mixed but has largely echoed commentary from Lagarde on Thursday.

- Gilts are just in the red, but outperforming peers. Outperformance that is a function of the morning’s growth data. Where the headline metrics were as expected for the M/M and 3M/3M, the Y/Y missed consensus and the manufacturing/production breakdown was very weak, printing beneath the forecast range. Notably, the M/M only just avoided being a negative print, helped out by some favourable 1dp rounding. A series that was sufficient to lift Gilts to a 91.75 peak, posting gains of 11 ticks at best. However, as the morning progressed this strength has waned and the benchmark is well off best, but still outperforming peers. The data has had no impact on BoE pricing, with markets not looking for a move until around March 2026.

- OATs are lower, in-fitting with peers. Awaiting the sovereign review from Fitch, due after the US close. Into this, OATs trade in-line with Bunds and the OAT-Bund 10yr yield spread holds just below the 80bps mark. Fitch has France at AA-, negative. Fitch last updated on March 14th, highlighting high levels of debt and a poor record of fiscal consolidation as points of weakness, adding the negative outlook is reflective of significant fiscal risks.

- Click for a detailed summary

COMMODITIES

- Crude opened lower, but traded with an upward bias since the European cash open, taking the complex into the green; currently resides at session highs. Some of the downbeat sentiment may be on EU officials suggesting it is unlikely the G7 will impose 100% tariffs on China and India, as India is a vital partner in trade and security matters, according to FT. WTI currently resides in a 61.69-62.83/bbl range while Brent sits in a USD 65.71-66.91/bbl range.

- Precious metals are steadily gaining despite this morning's dollar strength and in tandem with a rally in silver, which climbed above the USD 42/oz level. Spot gold currently resides in a USD 3,622.75-3,649.35/oz range. All-time high still sits at USD 3,674.69/oz printed on 9th September.

- Base metals trades firmly despite the weaker sentiment and stronger dollar, and with little in terms of newsflow to explain price action, although supply-side headlines yesterday suggested Peruvian copper output fell 2% in July. 3M LME copper resides in a USD 10,054.35-10,127.20/t range at the time of writing.

- US Energy Secretary Wright says the faster EU phase out of Russian energy would be helpful in ending the Ukraine war; thinks EU could phase out Russian oil and gas faster.

- Commerzbank raised gold price forecast to USD 3,800/oz by end-2026 (prev. USD 3,600/oz); raises silver end-2025 forecast to USD 41/oz to USD 43/oz; raises platinum forecast for 2025-end to USD 1,400/oz (prev. USD 1,350/oz).

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GDP Estimate MM (Jul) 0.00% vs. Exp. 0.00% (Prev. 0.40%); Estimate YY (Jul) 1.40% vs. Exp. 1.50% (Prev. 1.40%); Estimate 3M/3M (Jul) 0.2% vs. Exp. 0.2% (Prev. 0.30%)

NOTABLE EUROPEAN HEADLINES

- UBS Global Wealth Management expects ECB to remain on hold in 2025 (prev. 25bps cut in Dec); Now expect ECB to remain on hold for a prolonged period

- ECB's Simkus says inflation has stabilised at the target and labour market is in a good situation, adds economic activity is quicker than previously observed. Inflation risks are significantly high.

- ECB's Villeroy says another rate cut is possible in coming meetings; upward risks to inflation are lower than downward, via Bloomberg.

- ECB's Kazaks says risks remain elevated; a meeting-by-meeting approach is still appropriate, via CNBC; December meeting is 'rich'.

- ECB's Muller says rates in the right place at the moment.

- ECB's Rehn says the risk that inflation remains slower than the target level should not be underestimated. Must be mindful of downside risks to inflation stemming from cheaper energy and a stronger EUR.

- ECB's Kocher says the gap between Austrian inflation and EZ average is far too high; growth and inflation outlook presented at the meeting was little changed; will decide meeting-by-meeting and changes to risk landscape.

- Ipsos data: UK public inflation expectations at 3.6% (prev. 3.2%) for the coming year and 3.4% (prev. 3.2%) for the following 12-month period, 5-year 3.8% (prev. 3.6%)

NOTABLE US HEADLINES

- BofA Flow Show: Gold saw 4th largest weekly inflow ever (USD 3.4bln), Global Equity ETF saw the first outflow in four months (USD 3.1bln)

GEOPOLITICS

MIDDLE EAST

- Israel's UN envoy to the Security Council said Israel will act against the leaders of terror wherever they are hiding.

- Qatar's PM said to the UN Security Council that the Israeli attack on Hamas leaders in Doha is a violation of Qatar's sovereignty, and the attack, which was carried out while we are engaged in mediation, exposes Israel's intentions to derail peace efforts. Furthermore, Qatar's PM said Israeli leaders show no regard for hostages' lives and Qatar will continue its humanitarian and diplomatic role to spare bloodshed, but will not tolerate any infringement on sovereignty and security.

RUSSIA-UKRAINE

- The US is to urge G7 to impose high tariffs on China and India over Russian oil purchases, while finance ministers from G7 leading economies will discuss a US proposal for a round of new measures on Friday, according to FT.

- EU officials say it is unlikely G7 will impose 100% tariffs on China and India as India is a vital partner in trade and security matters, according to FT.

- Japan's Chief Cabinet Secretary Hayashi said Japan is to impose additional asset freeze, export controls, and sanctions on Russia over Moscow's invasion of Ukraine, while he added they are to lower the price cap on Russian crude oil from today.

- Japan's Trade Ministry said they are to restrict exports to additional entities, including six in China, two in Turkey, and one in the UAE, as part of sanctions against Russia's invasion of Ukraine.

- NATO Secretary General Rutte and Supreme Allied Commander to hold joint press conference at NATO headquarters today at 16:00 BST.

CRYPTO

- Bitcoin is a little firmer and trades just shy of USD 115k whilst Ethereum outperforms and holds above USD 4.4k.

APAC TRADE

- APAC stocks were mostly higher following the gains on Wall St, where the major indices climbed to record highs after a jump in Initial Jobless claims further boosted Fed rate cut pricing.

- ASX 200 edged higher with outperformance in Real Estate, Miners, Materials & Financials spearheading the advances as Fed rate hike expectations boost global risk sentiment.

- Nikkei 225 extended on record highs and approached closer towards the 45,000 level despite little fresh pertinent drivers.

- Hang Seng and Shanghai Comp traded mixed with tech leading the gains in Hong Kong after it was reported that Alibaba (9988 HK) and Baidu (9888 HK) are using internally designed chips for training AI models are to adopt their own AI chips in a major shift for Chinese tech, while the mainland lagged amid frictions, with the US reportedly to urge G7 to impose high tariffs on China and India over Russian oil purchases.

NOTABLE ASIA-PAC HEADLINES

- Japanese and US finance ministers' joint statement noted as trusted partners, the United States Department of the Treasury and the Japanese Ministry of Finance agreed to continue their close consultations on macroeconomic and foreign exchange matters, while they reaffirmed that exchange rates should be market-determined and that excess volatility can have adverse implications for economic and financial stability.

- Japanese Member of the House of Representatives Takaichi leads in a Kyodo poll to be next head of Japan ruling party.

- Chinese finance minister says local debt swap programme is achieving results. China's finance minister vows to resolutely curb new local hidden debt.

- Japan's former Top Currency Diplomat Gyoten says BoJ must take into consideration concerns that weak JPY could accelerate inflation; Japan's interest rates are too low and are contributing to the JPY weakness.

DATA RECAP

- China M2 (Aug): 8.8% YY vs. exp. 8.6%; New Yuan Loans CNY 13.46tln vs exp. 13.5tln.