US Market Open: USD gains whilst US equity futures are flat into Trump-Xi call; JPY benefits post-BoJ

19 Sep 2025, 11:06 by Newsquawk Desk

- BoJ kept rates unchanged at 0.50%, as expected, but surprised markets with the announcement to begin selling ETF and J-REIT holdings.

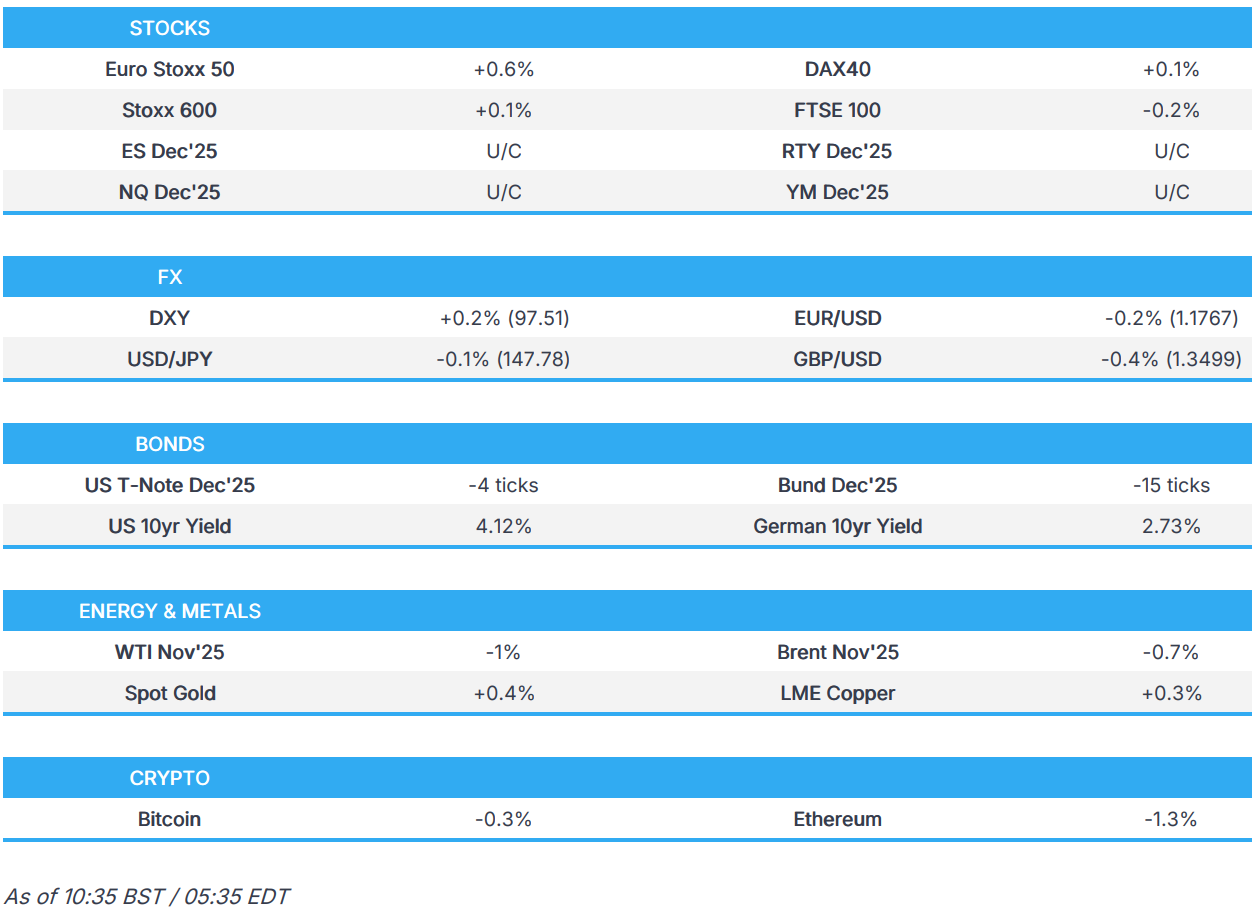

- European bourses are mostly higher whilst US equity futures are flat.

- USD extends its winning streak, GBP underperforms and is pressured by woeful borrowing data, which puts added pressure on UK Chancellor Reeves.

- USTs are slightly lower awaiting Fed speak, JGBs hit on the BoJ, Gilts lag after concerning borrowing data.

- Crude is on the backfoot, whilst Spot gold is firmer awaiting the Trump-Xi meeting.

- Looking ahead, Canadian Retail Sales (Jul), Quad Witching, Trump-Xi phone call. Speakers including Fed's Daly, Miran, & Former Fed President Bullard.

TARIFFS/TRADE

- Mexico's President Sheinbaum said she had an excellent conversation with Canadian PM Carney and agreed with Canada to strengthen the USMCA free trade agreement, while she added they will continue to work together with respect.

- Canadian PM Carney said they are committed to a shared partnership with the US and will create a new bilateral security dialogue with Mexico, as well as commented that they can find adjustments to boost competitiveness in North America.

BOJ

- Kept rates unchanged at 0.50%, as widely expected, with the decision made by a 7-2 vote in which Board members Takata and Tamura proposed a 25bps rate hike. Nonetheless, the central bank surprised markets with the announcement to begin selling its ETF and J-REIT Holdings at a pace of JPY 330bln per year and JPY 5bln per year, respectively, with the decision on ETF and J-REIT sales made by unanimous vote, while it stated the pace of sales may be modified at future MPMs after the start of ETF and J-REIT disposals, based on fundamental principles and experience from sales conducted. BoJ also stated that Japan's economy is recovering moderately, although some weakness has been seen and noted that private consumption has been resilient and inflation expectations have risen moderately, but exports and output remain more or less flat as a trend. Furthermore, it stated that Japan's economic growth is likely to slow due to the impact of trade policies on global growth, but re-accelerate, and Japan's underlying inflation to stagnate due to a slowdown in economic growth, but gradually accelerate thereafter.

- BoJ Press Conference: Governor Ueda says Japan's economy is recovering moderately, albeit with some weakness; will continue to raise policy rate if economy and prices move in line with forecast.

- On the economy: Downside risks to economy still present.

- On policy: Not considering changing pace of ETF sales to adjust monetary policy. Not thinking now of repurchasing ETFs as monetary policy tool. Decision on timing of next rate hike would depend on the risk of US tariff impact materialising and the course of food inflation.

- On trade/tariffs: The domestic economy is withstanding tariff impact. Tariff costs likely to be passed down to consumers in the US from November. Not seeing negative impact in Japan's economy from US tariffs.

- In summary, Ueda didn’t really give too much away with his focus on the economy, data and tariffs, unsurprisingly. Overall, it seems that an October move is on the cards assuming that data, October 1st Tankan in focus, presents no surprises and the October 4th LDP leadership contest occurs without a major curveball; helpfully, Ueda is scheduled to speak on October 8th.

- The implied odds of a hike stand at around 45% for October, vs c. 30% on Thursday.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) are mostly firmer; outperformers in Europe today include the CAC 40 and FTSE MIB, whilst the AEX (pressured by a pullback in Tech names) and the FTSE 100 (UK assets shunned today) underperform.

- European sectors hold a slight positive bias, with only a few industries found in negative territory. Autos takes the top spot today, with gains driven by upside in Stellantis (+4.5%) which benefits from a broker upgrade at Berenberg. The Construction & Materials sector follows behind, and is buoyed by strength in Vinci (+1%) after the Co. received a EUR 885mln contract related to Rail Baltica Electrification. Tech is very marginally lower, seemingly scaling back some of the significant upside seen in the prior session after the IT sector surged more than 5.6% in the prior session. Much of Thursday’s upside was driven by ASML (-0.5%), which received a PT upgrade at BofA following the NVIDIA-Intel partnership.

- US equity futures are flat, following on from a session of significant gains in the prior session in the aftermath of the FOMC and as traders reacted to the mega NVIDIA-Intel deal.

- FedEx (FDX) shares gain 4.8% in pre-market trade after it topped expectations in Q1, on higher US package volumes lifting results, though its freight unit was weaker. Management highlighted resilience despite global trade headwinds, including the loss of the de minimis exception.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is extending its winning streak to a third session and building on yesterday's gains, which were in part driven by a downtick in weekly claims data and a strong Philly Fed report. Dovish dissenter Miran will be explaining his decision to back a larger 50bps move at some point today. However, given he is such an outlier on the FOMC and was not joined by Waller or Bowman, his views will likely prove non-incremental for the market. Focus will also be on the potential read-out of a President Trump-Xi meeting, and then Daly thereafter. DXY sits just a touch below Thursday's peak at 97.60.

- EUR is softer vs. the broadly firmer USD with incremental macro drivers for the Eurozone lacking, as has been the case throughout the week. After printing a multi-year high earlier in the week at 1.1919, the pair has since delved as low as 1.1750 on Thursday.

- JPY is the only of the majors firmer vs. the USD, following the BoJ policy announcement. As expected, the Bank stood pat on rates. However, the decision to do so was subject to hawkish dissent from Takata and Tamura on account of concerns over upside inflation risks. The other source of surprise came from the BoJ's decision to begin selling its ETF and J-REIT Holdings at a pace of JPY 330bln per year and JPY 5bln per year, respectively. The hawkish dissent knocked USD/JPY lower and sent the pair to a session trough at 147.21 before fading a bulk of the downside heading into Governor Ueda's press conference. During which, he reiterated that the Bank will continue raising rates if prices move as forecast. From a hawkish perspective, he noted that the domestic economy is withstanding tariff impact and the Bank does not necessarily need to wait to see the full impact of US tariffs on inflation to make a decision on additional tightening. That being said, he acknowledged that downside risks to the economy are still present and didn't make any explicit signals to a move next month, which could have been a driver for the fading of JPY strength. USD/JPY has moved back above its 50DMA @ 147.65 and sits towards the top end of Thursday's 146.76-148.26 range.

- GBP is extending yesterday's losses vs. the EUR and USD as markets digest yesterday's BoE policy announcement and the latest batch of UK data. UK retail sales printed better-than-expected (M/M 0.5% vs. Exp. 0.3%). However, the release was overshadowed by a marked rise in UK public sector net borrowing (17.962bln vs, Exp. 12.75bln, prev. 2.818bln). Cable currently trades around 1.3496.

- Both antipodes are softer vs. the USD in quiet newsflow for Australia and New Zealand, with a decline in NZ exports having little follow-through into NZD.

- PBoC set USD/CNY mid-point at 7.1128 vs exp. 7.1174 (Prev. 7.1085).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs were pressured overnight on the BoJ. While the decision was unchanged at 0.50% as expected, that was subject to two hawkish dissenters (Takata and Tamura) who wanted a 25bps cut. Additionally, the bank is to commence sales of its ETF and J-REIT holdings at a very slow pace; underscored by Ueda, who said it would take over 100 years to exit their position at the current pace. Ueda didn’t really give too much away with his focus on the economy, data and tariffs, unsurprisingly. However, while familiar, his underlying message that the normalisation process can continue if the economy and prices proceed as forecast is notably in the context of domestic political instability.

- Gilts are underperforming. Opened lower by 28 ticks and then slumped another 18 to a 90.72 trough. Pressure stemmed from the lead from peers with JGBs in the red, Bunds at a fresh WTD base and the morning’s UK data. Retail Sales was stronger-than-expected, but ultimately overshadowed by the PSNB which stood at GBP 17.96bln, eclipsing the newswire consensus and the GBP 12.5bln forecast by the OBR. Figures that add to the pressure Chancellor Reeves is under as we look to the Autumn Budget at the end of November. UK 30yr yield back above 5.55% and now looking to the YTD peak at 5.75% if the fiscal situation deteriorates further.

- USTs are waiting for Fed speak as the post-FOMC blackout period lifts. Dissenter Miran will draw focus to gauge just how much easing he wants to see (though the dots provided some indication) and his views on the September meeting; Daly is also due. Fed aside, the Trump-Xi call is another major point of focus. USTs are in the red, echoing peers, though with action more contained ahead of the discussed catalysts. At a 112-24+ trough, just above Thursday’s 112-23+ WTD base.

- Bunds are softer, following the above. Down to a fresh WTD low at 128.18. If the pressure intensifies, we look to support at the figure before 127.82, 127.63 and 127.61 from recent weeks. August producer prices hit this morning, coming in negative and printing beneath the forecast range. Destatis determined the drop was primarily due to lower energy prices, and when adjusted for energy the figure was actually 0.8% Y/Y vs the -2.2% reported. Focus now turns to DBRS' review on France.

- Click for a detailed summary

COMMODITIES

- WTI and Brent remain subdued following a similar APAC session and after the choppy performance seen during the prior day. Headwinds were seen on Thursday following US President Trump's comments on oil, suggesting there is a lot of oil left in the North Sea and oil prices need to come down further. Trump also repeated the call for countries to stop buying from OPEC+ members. WTI currently resides in a tight USD 63.15-63.65/bbl range while Brent sits in a USD 67.11-67.57/bbl range.

- Precious metals are mixed with spot gold, gradually edging higher overnight before falling victim to the USD once again, following the same headwind yesterday. Volatility in the yellow metal was seen during the China open, albeit this was short-lived, whilst some upticks were seen during the BoJ announcement as the firmer JPY pushed down the USD at the time. Spot gold currently resides in a USD 3,632.38-3,661.35/oz range, well within yesterday's USD 3,627.96-3673.20/oz parameter.

- Mixed trade across base metals this morning, with the red metal overnight trading rangebound near this week's trough amid the ultimately mixed risk appetite in Asia.

- EU is reportedly considering a provision in the 19th sanctions package against Russia to phase out Russian LNG purchases a year earlier than currently planned, via Bloomberg citing sources.

- Democratic Republic of Congo considers extending cobalt export ban for at least two months, according to Reuters sources.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK Retail Sales MM (Aug) 0.5% vs. Exp. 0.3% (Prev. 0.6%, Rev. 0.5%); Ex-Fuel MM (Aug) 0.8% vs. Exp. 0.7% (Prev. 0.5%, Rev. 0.4%)

- UK Retail Sales YY (Aug) 0.7% vs. Exp. 0.6% (Prev. 1.1%, Rev. 0.8%); Ex-Fuel YY (Aug) 1.2% vs. Exp. 1.0% (Prev. 1.3%, Rev. 1.0%)

- UK PSNB Ex Banks GBP (Aug) 17.962B GB vs. Exp. 12.75B GB (Prev. 1.054B GB, Rev. 2.818B GB)

- UK GfK Consumer Confidence (Sep) -19.0 vs. Exp. -18.0 (Prev. -17.0)

- German Producer Prices YY (Aug) -2.2% vs. Exp. -1.7% (Prev. -1.5%); MM (Aug) -0.5% vs. Exp. -0.1% (Prev. -0.1%)

NOTABLE EUROPEAN HEADLINES

- ECB's Centeno say still sees inflation risks to the downside; ECB cannot tolerate inflation below 2% for too long; 2028 inflation forecast likely to be below 2%.

- UBS Wealth Management, Morgan Stanley & BofA no longer look for a BoE rate cut this year.

NOTABLE US HEADLINES

- US lawmakers plan bipartisan bill to exempt coffee from tariffs, may be introduced on Friday, according to the Washington Post.

- US President Trump's administration is considering a plan to spur the construction of factories and other infrastructure to boost the US manufacturing sector using the USD 550bln fund established through negotiations with Japan, according to WSJ.

- US President Trump posted that House Republicans will vote to pass a clean funding bill on Friday and that "The Leader of the Democrats, Cryin’ Chuck Schumer, wants to shut the Government down. Republicans want the Government to stay open. Every House Republican should UNIFY, and VOTE YES!"

- US House Speaker Johnson said he believes they have the votes to pass the stopgap funding bill, while US Senate Majority Leader Thune said the Senate will also vote on a House stopgap bill on Friday.

- White House is considering additional candidates for CFTC chair as the confirmation process for Brian Quintenz has stalled, while possible candidates include government officials focused on crypto policy, according to Bloomberg.

GEOPOLITICS

- Israel PM Netanyahu says "We will strike Hamas hard, we will not stop and we will not end this war until we achieve all our goals", via Al Jazeera

- Iranian Deputy Foreign Minister says actions by European nations to reimpose sanctions would be politically biased and a pretext for escalation.

- EU Council President Costa is inviting leaders to an informal summit on October 1st. Focus will be on strengthening European common defence, and reinforcing support for Ukraine.

CRYPTO

- Bitcoin is a little lower and trades just shy of USD 117k whilst Ethereum trades around USD 4.5k.

APAC TRADE

- APAC stocks traded mixed as the region only partially sustained the momentum from Wall St, where the S&P 500, DJIA and NDX climbed to fresh record highs as risk sentiment was supported by encouraging data, while participants digested a surprise announcement by the BoJ to begin selling its ETF and J-REIT holdings.

- ASX 200 climbed higher with a couple of the defensive sectors leading the advances and with most industries in the green aside from telecoms.

- Nikkei 225 rallied at the open after the latest CPI data mostly matched estimates but softened from the previous, although the index has slightly pulled back from all-time highs with some jitters seen as participants awaited the 'delayed' BoJ announcement, while downside accelerated after the BoJ decided to begin selling ETF and J-REIT holdings.

- Hang Seng and Shanghai Comp were rangebound amid tentativeness ahead of the scheduled Trump-Xi call and with ongoing trade-related uncertainty, while the US House Select Committee on the CCP urged action in a letter to US President Trump in response to China's weaponisation of critical minerals supply chains.

NOTABLE ASIA-PAC HEADLINES

- Japanese LDP lawmaker Takaichi is to propose an income tax cut and cash payout to households in a campaign pledge for the ruling party leadership race, while she will call for gradually lowering the ratio of government debt to GDP in her campaign pledge, according to Nikkei. Adds, Ministry of Finance should present an economic growth plan.

- PBoC says 14-day Reverse Repo operations in the open market will be conducted via fixed volume and interest rate bidding with multiple price allocation.

- Chinese FX regulator says commercial banks purchased net USD 14.7bln in FX in Aug (vs net USD 22.8bln purchase in Jul), purchased a net USD 12.1bln in Jan-Aug (vs net 2.5bln sale in Jan-Jul).

- BoJ Governor Ueda is to speak at the Paris Europlace Forum in Tokyo on October 8th.

DATA RECAP

- Japanese National CPI YY (Aug) 2.7% vs Exp. 2.8% (Prev. 3.1%)

- Japanese National CPI Ex. Fresh Food YY (Aug) 2.7% vs Exp. 2.7% (Prev. 3.1%)

- Japanese National CPI Ex. Fresh Food & Energy YY (Aug) 3.3% vs Exp. 3.3% (Prev. 3.4%)