US Market Open: US equity futures are flat, awaiting Fed Chair Powell and Trump; GBP hit on PMIs

23 Sep 2025, 11:33 by Newsquawk Desk

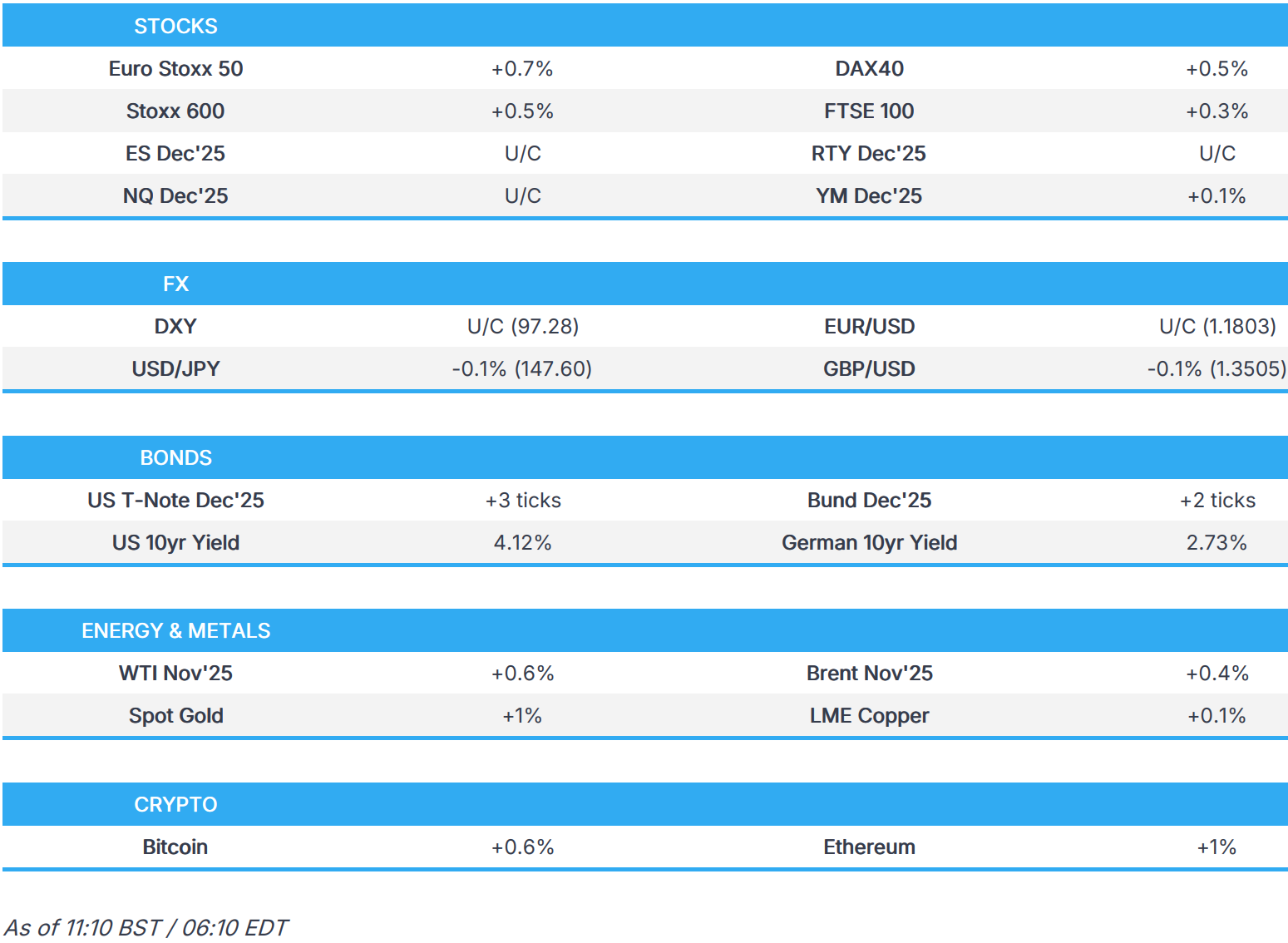

- European bourses gradually climb higher and currently at peaks; US equity futures are flat awaiting Fed Chair Powell.

- GBP hit by soft PMI, Eurozone data showed diverging fortunes for manufacturing and services.

- USTs are essentially flat; Gilts modestly out-edge peers following disappointing flash PMI metrics.

- Crude initially in the red but have managed to climb higher, XAU at another ATH, catching a bid on reports that China aims to become custodian of foreign gold reserves.

- Looking ahead, US Flash PMIs (Sep), US Richmond Fed Index, NBH Policy Announcement; Speakers include BoE’s Pill, Fed’s Powell, Bostic, Bowman, ECB’s Cipollone, BoC’s Macklem, US President Trump at UN General Assembly; Supply from the US; Earnings from Micron.

TRADE/TARIFFS

- JPMorgan (JPM) CEO Dimon noted tariffs could be modestly inflationary but uncertain if the impact is temporary, via Times of India interview.

- US lawmaker Smith noted the intention to improve communication channels between China and the US.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) opened with a slight positive bias, with a couple of indices opening lower. However, as the session progressed, sentiment picked up a touch, and sauntered higher to current peaks.

- European sectors hold a strong positive bias, with only a couple of industries residing marginally in the red. Retail takes the top spot, buoyed by strength in Kingfisher (+17%) after it reported strong metrics and upgraded its guidance. Healthcare is found right at the foot of the pile, no company-specific drivers but perhaps some jitters surrounding Trump’s move to link paracetamol use during pregnancy with autism.

- US equity futures (ES U/C NQ U/C RTY U/C) are modestly mixed on either side of the unchanged mark, with the ES/NQ holding afloat whilst the RTY is incrementally lower.

- ASM International (ASM NA): Confirms Q3 Revenue guidance -5% to flat, lowers H2 guidance, due to lower-than-exp. demand in leading-edge logic and foundry. Cuts FY25 Revenue guide to the "low end" of +10-20% (prev. guided "mid-point" +10-20% Y/Y). Bookings in H2'25: demand weakness in leading-edge logic and foundry is projected to result in a book-to-bill of below 1 in H2'25.

- Foxconn's (2345 TT) main iPhone (AAPL) unit is halting work at its Shenzhen campus due to the local typhoon; will resume work once the Government lifts its warning, via Bloomberg

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is a touch higher after yesterday's downside. Macro focus for the US at the start of the week has mainly focussed on Fed speak with policymakers (ex-Miran) largely taken a cautious approach to further easing. To recap, 2026 voter Hammack noted that she has one of the higher estimates of neutral and judges that policy is only modestly restrictive. Today's speaker highlight will be Fed Chair Powell at 17:35BST, who will be speaking on the economic outlook and in a more personal capacity to that seen last week at the Fed press conference. Other speakers today include 2025 voters Goolsbee and Bowman. On the data slate, flash PMIs are due. However, these often play second-fiddle in the US to the ISM series. DXY delved as low as 97.19 overnight before move back above Monday's 97.29 low.

- EUR was knocked lower in early trade following a dismal PMI report from France, which saw all three key metrics, decline from the prior, miss analyst consensus and sit in contractionary territory. The accompanying report noted that "the increasingly tense domestic political situation likely to have a negative impact on household consumption and investment decisions." As such, HCOB expects "GDP growth rates to be between 0.5 and 1 percent in both 2025 and 2026". Thereafter, the German release saw the manufacturing print dissapoint by remaining in contractionary territory. However, this was offset by an unexpected expansion in the services sector, which helped the composite remain above the 50 threshold and EUR fade French-induced downside. The Eurozone data reflected the trend seen in Germany (servives > manufacutring), however, the associated report suggested that "we’re still a long way from seeing any real momentum." EUR/USD has returned to a 1.17 handle.

- Overnight, USD/JPY fell under its 50 DMA (147.68) and dipped under Monday's low (147.66), before recovering amid a lack of noteworthy drivers and with Japanese participants away on the Autumnal Equinox holiday. Ahead of the LDP leadership election, poll leader Takaichi has proposed using tax revenues for tax cuts and spending measures to tackle inflation, but said she may consider issuing bonds if needed. Her closest rival, Koizumi said Japan should use the expected increase in tax revenues and proceeds from expenditure cuts to fund spending for steps to combat the rising cost of living. However, Japan must be mindful of the need for fiscal discipline.

- GBP sits at the foot of the G10 leaderboard following a dissapointing showing for September flash PMI metrics. All three metrics fell short of expectations with the services and composite prints remaining in expansionary territory but below the bottom end of analyst consensus. Manufacturing delved further into contractionary mode. The accompanying release noted "September’s flash UK PMI survey brought a litany of worrying news including weakening growth, slumping overseas trade, worsening business confidence and further steep job losses". Cable ventured as high as 1.3528 overnight before slipping back onto a 1.34 handle with a current session low at 1.3488.

- Antipodeans softened overnight amid weakness in Chinese markets. AUD/USD was also weighed on by a marked deterioration in Flash PMIs, albeit the data remained in expansion territory. NZD/USD was subdued, whilst Bloomberg sources suggested a new RBNZ Governor could be announced as soon as Wednesday.

- Alongside a split consensus between a 25bps reduction and an unchanged rate, the Riksbank opted to cut the policy rate by 25bps. The decision to do so was subject to hawkish dissent from Seim on account of her concerns over potential upside inflation surprises stemming supply side and fiscal factors. Offsetting the dovish impule from the rate cut was accompanying commentary that the Bank expects the policy rate to "remain at this level for some time to come." Two-way price action in EUR/SEK, given it the announcement shared the release timing with German PMIs; but overall EUR/SEK ended up heading back to above pre-release levels.

- PBoC set USD/CNY mid-point at 7.1057 vs exp. 7.1066 (Prev. 7.1106)

- RBI reportedly sold USD via state-run banks to support the rupee after hitting record lows, according to Reuters, citing traders

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs came under modest pressure overnight, to a 112-21+ low before gradually picking up into and throughout the European morning. Upside that occurred despite the constructive European risk tone and the slight pressure seen in Bunds at the time. Nothing particularly fresh in European hours for US participants, as we digest the numerous Fed speakers seen yesterday and look to today’s packed docket featuring Chair Powell; remarks that will allow the Chair to give his rather than the overall Fed’s view on monetary policy and the economy. Within the comments, any language around the neutral rate will draw focus given the range of views outlined in recent sessions.

- Bunds are softer by a handful of ticks. Began the day softer before lifting into the green in-line with USTs at first. French measures came in weaker across the board and outside the forecast range. HCOB wrote that activity weakened more sharply than at any point since April and forward-looking indicators not suggesting any major improvements in the coming months. Thereafter, the generally stronger German measures sent Bunds to a 128.15 low with downside of 11 ticks at most. Limited reaction to the EZ-wide figures. Further out, HCOB writes that “the outlook for manufacturing is looking a bit cloudy”. German auction was a little softer-than-prior but sparked little moved.

- Gilts opened near-enough unchanged. Modest action in-fitting with Bunds alongside the European PMI metrics. Thereafter, the UK’s own figures were softer than expected across the board and markedly so for the services and composite measures. Within the series, S&P said it brought a “litany” of worrying news with the only good news being a moderation of price pressure. Ahead, surmising that “...it’s unlikely that the economy will make any strong gains in the months ahead irrespective of the outlook for interest rates." A series that lifted Gilts by around 15 ticks to a 91.06 high with gains of 22 ticks at best. And at the time the clear outperformer. Thereafter, supply was poor. The first outing of the 2056 line saw a strong cover in excess of 3x but a substantial 20.5 tick price tail. Results of this weighed on Gilts and saw nearly all of the PMI move retraced, Gilts remain the outperformer but only marginally and are back towards the midpoint of 90.75-91.06 parameters.

- UK sells GBP 1.5bln 5.375% 2056 Gilt: b/c 3.07x, average yield 5.476%, tail 1.4bps.

- Germany sells EUR 3.601bln vs exp. EUR 4.5bln 1.90% 2027 Schatz: b/c 1.8x (prev. 2.0x), average yield 2.01% (prev. 1.96%) & retention 19.98% (prev. 21.07%).

- Click for a detailed summary

COMMODITIES

- A softer start to the session for crude, at most benchmarks lower by around USD 0.45/bbl. However, across the European morning the benchmarks have been gradually lifting off lows and moving to just above the unchanged mark on the session. Currently, towards the upper-end of USD 61.85-62.53/bbl and USD 66.10-66.75/bbl parameters for WTI and Brent respectively.

- Spot gold is continuing to climb and at another ATH of USD 3780/oz. A high that occurred after a Bloomberg report that China is aiming to become a custodian of foreign sovereign gold reserves as it aims to improve its standing on the global bullion market. Prior to this, the narrative for gold hadn't really changed, with the strength underpinned generally by the Fed’s easing cycle, day-to-day by ongoing geopolitical headlines and aided by numerous desks lifting their forecasts for the precious metal.

- Copper picked up overnight in reaction to the strong US risk tone amid the NVIDIA and OpenAI update. However, the complex failed to glean much from this with 3M LME Copper dipping back below the USD 10k/t mark and into the red.

- China is aiming to become a custodian of foreign sovereign gold reserves as it aims to improve its standing on the global bullion market, via Bloomberg. The PBoC is using the Shanghai Gold Exchange to country central banks in allied countries to buy bullion and store it within China.

- Chile's development agency Corfo informed the comptroller office of contract changes to enable the Codelco-SQM lithium deal, according to Reuters.

- Congo President noted intention to strengthen partnership with US, focusing on mining sector and infrastructure development but rules out auctioning mineral resources to US, according to Reuters.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HCOB Composite Flash PMI (Sep) 51.2 vs. Exp. 51.1 (Prev. 51); Services Flash PMI (Sep) 51.4 vs. Exp. 50.5 (Prev. 50.5); Manufacturing Flash PMI (Sep) 49.5 vs. Exp. 50.7 (Prev. 50.7)

- French HCOB Services Flash PMI (Sep) 48.9 vs. Exp. 49.6 (Prev. 49.8); Manufacturing Flash PMI (Sep) 48.1 vs. Exp. 50.1 (Prev. 50.4); Composite Flash PMI (Sep) 48.4 vs. Exp. 49.7 (Prev. 49.8)

- German HCOB Composite Flash PMI (Sep) 52.4 vs. Exp. 50.6 (Prev. 50.5); Services Flash PMI (Sep) 52.5 vs. Exp. 49.5 (Prev. 49.3); Manufacturing Flash PMI (Sep) 48.5 vs. Exp. 50 (Prev. 49.8)

- UK Flash Composite PMI (Sep) 51.0 vs. Exp. 53 (Prev. 53.5); Manufacturing PMI (Sep) 46.2 vs. Exp. 47.1 (Prev. 47); Services PMI (Sep) 51.9 vs. Exp. 53.5 (Prev. 54.2)

- UK CBI Trends - Orders (Sep) -27.0 (Prev. -33.0)

NOTABLE EUROPEAN HEADLINES

- Riksbank Rate: 1.75% vs. Exp. 2.00% (Prev. 2.00%), Seim dissented, wanted U/C; "If the outlook for inflation and economic activity holds, the policy rate is expected to remain at this level for some time to come."

- Riksbank decision on their holding of long-term Swedish gov't bonds: "Riksbank has now decided that the holding will be allowed to fluctuate between SEK 18-22bln." vs prev. SEK 20bln in order to facilitate efficient trading.

- Riksbank's Thedeen says that the Bank sees a pretty strong recovery ahead; labour market has weakened noticeably.

- OECD sees global growth at 3.2% in 2025 (prev. view of 2.9%) with the 2026 projection held at 2.9%.

- BoE's Pill says the UK's approach to QE is more transparent than elsewhere, via Bloomberg; wanted to keep QT at GBP 100bln at the last meeting. Says UK inflation has proved more stubborn than expected, via Bloomberg

NOTABLE US HEADLINES

- US President Trump to speak at 09:50 ET /14:50 BST at the UN General Assembly

- US President Trump will meet with House Minority Leader Hakeem Jeffries and Senate Minority Leader Chuck Schumer this week, according to Punchbowl News.

- US President Trump said the FDA will warn physicians about a potential link between acetaminophen (Tylenol) use in pregnancy and autism risk; he advised pregnant women to avoid Tylenol and said do not take it. Trump also said MMR vaccines should be taken separately and that there is no reason for newborns to be given the Hepatitis B vaccine, according to Reuters.

- JPMorgan (JPM) CEO Dimon, on Fed rate cuts, said further reductions will be difficult, via CNBC-TV18.

GEOPOLITICS

NATO-RUSSIA

- Sweden's Defence Minister said "Sweden has the right to defend its airspace, with force if necessary", according to Swedish press.

- "Unidentified drones over Stockholm, the capital of Sweden", according to unconfirmed local reports cited by geopolitical watchers on X.

- Oslo Airport spokesperson confirmed airspace has been closed since midnight local time due to drone sightings, with all flights diverted to nearby airports, according to Reuters.

- Copenhagen airport reopened following closure due to drone activity, according to Reuters.

- Russia's Kremlin says time is short and allowing nuclear treaty with the US to expire would be fraught with risks for international security; Not clear yet when Russian President Putin and US President Trump will speak again

MIDDLE EAST

- EU and E3 to meet the Iranian Foreign Minister at 10:00ET / 15:00 BST on Tuesday, according to WSJ's Norman.

- Trump to present Arab leaders with US principles for ending Gaza war, and the US seeks agreement from Arab and Muslim nations to deploy troops to Gaza, facilitating Israeli withdrawal and securing transition funding, according to Axios.

- UKMTO reports incident 120 nautical miles east of Yemen's Aden; reports splash and sound of an explosion in its vicinity, crews and vessel reported safe.

OTHERS

- The White House said US President Trump will meet with the UN Secretary General and leaders of Ukraine, Argentina and the EU at the UN, and will also hold a multilateral meeting with Qatar, Saudi Arabia, Indonesia, Turkey, Pakistan, Egypt, the UAE and Jordan, according to Reuters.

- Turkish President Erdogan said he will discuss F-35 negotiations with US President Trump during the upcoming meeting, via Fox News interview.

- US, South Korean and Japanese foreign ministers jointly opposed unlawful maritime claims in the South China Sea, according to a statement.

CRYPTO

- Bitcoin is a little firmer, and Ethereum mildly outperforms attempting to pare back recent losses.

APAC TRADE

- APAC stocks eventually traded mixed as the positive sentiment from Wall Street failed to sustain during APAC trade despite a lack of fresh catalysts, whilst there was an absence of Japanese volume as participants were away due to the Autumnal Equinox holiday.

- ASX 200 eked gains, once again lifted by gold miners as the yellow metal printed fresh all-time highs, although upside was capped by a deterioration in Flash PMIs.

- Hang Seng and Shanghai Comp eventually traded lower with catalysts sparse, but amid the hangover from the anticlimactic Trump-Xi call last week, whilst Hong Kong markets braced for the Super Typhoon, expected to be the worst since at least 2018.

- KOSPI was again supported by the strong performance in its Tech sector after the NVIDIA/OpenAI announcement.

- Nifty 50 trimmed its earlier mild gains with the index continuing to be hampered by the US H-1B visa update.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM contender Takaichi proposed using tax revenues for tax cuts and spending measures to tackle inflation, but said she may consider issuing bonds if needed. She said policymakers should be mindful of the risk of causing a yield rise when guiding fiscal policy, but noted that when interest rates rise, so would interest from government assets, according to Reuters.

- Japanese PM contender Koizumi said Japan should use the expected increase in tax revenues and proceeds from expenditure cuts to fund spending for steps to combat the rising cost of living. He said Japan must be mindful of the need for fiscal discipline, but achieving solid economic growth is the basis for guiding sound fiscal policy, according to Reuters.

- Japanese PM contender Hayashi said they must avoid issuing deficit-covering bonds to fund spending and keep sending signals to the market that Japan will maintain fiscal discipline, according to Reuters.

- New Zealand is set to appoint its first female RBNZ Governor; announcement to come as soon as Wednesday, according to Bloomberg sources.

DATA RECAP

- Australian S&P Global Services PMI Flash (Sep) 52.0 (Prev. 55.8)

- Australian S&P Global Manufacturing PMI Flash (Sep) 51.6 (Prev. 53.0)

- Australian S&P Global Composite PMI Flash (Sep) 52.1 (Prev. 55.5)

- South Korean PPI Growth YY (Aug) 0.6% (Prev. 0.5%, Rev. 0.5%); MM (Aug) -0.1% (Prev. 0.4%, Rev. 0.4%)