US Market Open: US equity futures are mixed, USD gains, EUR is pressured on soft German Ifo

24 Sep 2025, 11:31 by Newsquawk Desk

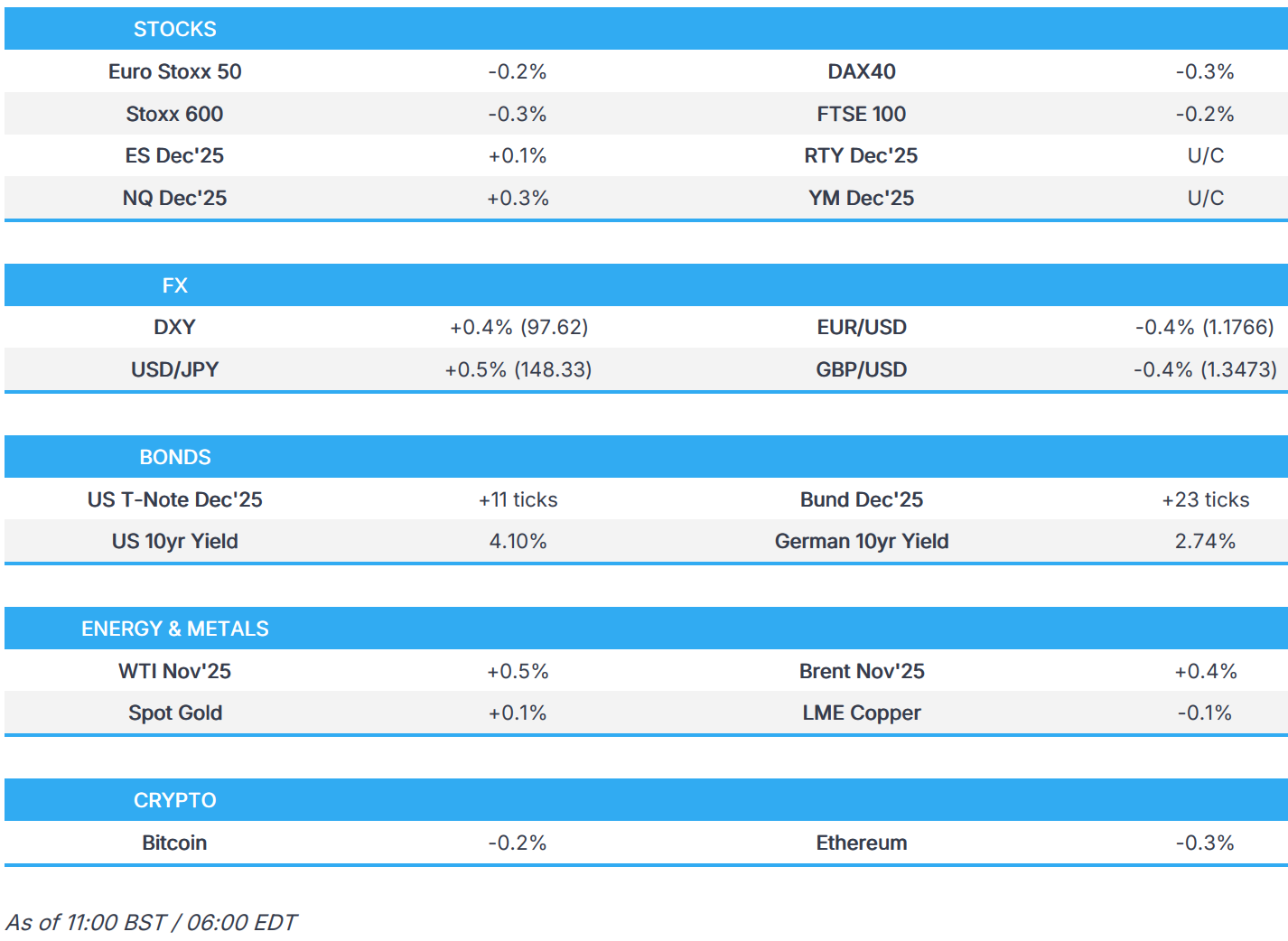

- European bourses are modestly lower; US equity futures are incrementally firmer/flat.

- USD is attempting to atone for recent losses. EUR digests soft German Ifo.

- Fixed benchmarks are firmer; Bunds caught a bid on softer-than-expected German Ifo metrics.

- Crude briefly boosted by reports that Israel's army has taken "another step" in the plan to occupy Gaza city; XAU takes a breather from recent upside.

- Looking ahead, highlights include Supply from the US; Speeches from BoE’s Greene, Fed’s Daly.

TRADE/TARIFFS

- The White House said US President Trump will meet Australian Prime Minister Albanese on 20th October in Washington, according to Reuters.

- Canadian PM Carney said discussions with US President Trump about a Canada-US trade deal will roll into the USMCA review process, noting that talks are ongoing and that Canada will sign when there is the right deal for the country, according to Reuters.

- Canadian PM Carney said he is open to discussions with the Chinese Premier regarding steel tariffs, according to Reuters.

- China’s Commerce Ministry stated it will not seek preferential treatment at the WTO, according to Reuters.

- China’s Premier expressed willingness to enhance cooperation with Canada to improve bilateral relations, according to Reuters.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.3%) began the session around the unchanged mark, but slipped into negative territory, soon after the cash open, but without a clear catalyst - perhaps some focus on the latest hawkish geopolitical rhetoric from Trump. More recently, the complex has picked up from worst levels to currently trade towards the mid-point of the day’s range.

- European sectors hold a negative bias, and with the breadth of the market fairly narrow today. Utilities is found towards the top of the pile, albeit only marginally so. Iberdrola (+0.8%) announced it will be investing USD 68bln to grow in the UK/US; the Co. also said it sees close to EUR 20bln in dividends between 2025 and 2028. Defence names today have been boosted today after President Trump said Ukraine can win all its land back from Russia.

- US equity futures are modestly firmer/flat, with the ES/NQ trading with incremental gains whilst the RTY bobbles around the unchanged mark.

- Pre-market movers; Micron (+1.9%, Q4 results topped expectations and guidance was decent), Alibaba (+9%, launched its largest AI model; collaborates with NVIDIA on Physical AI), NVIDIA (+0.8%, insider selling; OpenAI in talks to rent NVIDIA chips).

- Alibaba (BABA / 9988 HK) announces a collaboration with NVIDIA (NVDA) on physical AI, via CLS.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is attempting to claw back the losses seen on Monday and Tuesday in a session, which thus far has been void of fresh macro drivers. Docket today fairly thin, focus will be on Fed speak via Daly at 21:10BST, who will be speaking on the economic outlook. DXY has eclipsed Tuesday's best at 97.45.

- EUR/USD is lower on account of the broadly stronger USD and a disappointing IFO report from Germany. Both the expectations and current conditions prints declined from their priors and printed below the bottom end of analyst estimates, snapping a streak of six consecutive months of increases for the headline business climate metric. Desks remain cognizant of geopolitical tensions after US President Trump's UN address yesterday, in which he noted that NATO countries should shoot down Russian aircraft if they enter NATO airspace. Finally, in an olive branch to the Left, reports in French press suggest that Lecornu is open to a tax on top earners and firms. EUR/USD has extended its decline on a 1.17 handle.

- USD/JPY has moved back onto a 148 handle, supported by the stronger dollar and incremental JPY weakness after flash PMIs showed a deterioration across all components, commentary highlighted persistent cost pressures and elevated inflation. Elsewhere, focus remains on the outcome of the LDP leadership contest on October 4th with Sanae Takaichi still judged to be the front-runner for the position. As it stands, an October hike is currently seen as a coin-flip by markets. USD/JPY has ventured as high as 148.29.

- GBP is on the backfoot vs. the broadly firmer USD and steady vs. the EUR. Incremental macro drivers from the UK are light in the wake of yesterday's soft showing for September flash PMI metrics, which were weighed on by angst ahead of the November 26th budget. Ahead of which, the Institute for Government (IfG) is the latest think tank to come out and suggest that Chancellor Reeves needs to consider going back on her “rash” tax commitments and impose serious tax reform. Today's docket is light in terms of data. However, MPC external member Greene is due to give remarks at 17:30BST on ‘Supply shocks and monetary policy’ (text release is due). Cable has slipped onto a 1.34 handle and below Tuesday's 1.3488.

- AUD is bucking the trend of the majors and is firmer vs. the USD in the wake of firm Australian CPI metrics, which saw the Y/Y CPI rate climbing from 2.8% to 3.0% - the top end of the RBA's target range.

- PBoC set USD/CNY mid-point at 7.1077 vs exp. 7.1080 (Prev. 7.1057)

- RBI reportedly likely intervened in NDF markets ahead of local opening to support the INR, according to traders cited by Reuters

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- A slightly firmer start to the day for USTs, though once again ranges are thin and US specific newsflow is light. Currently, USTs hold near the top end of a 112-28 to 113-00 band. Just about eclipsing Tuesday’s 112-30+ peak and last week’s best, which was a tick above that. After the deluge of speakers yesterday, today’s docket is a little quieter but does feature remarks from Fed’s Daly (2027) where we expect text and a Q&A. Before that, the week’s supply continues with 5yr notes due after Tuesday’s 2yr sale, an auction that was ok overall but did show a cooling of demand.

- A contained start for Bunds, firmer by a handful of ticks but also in a thin range with newsflow at the time light and largely digesting leaders remarks on the defense/Ukraine front after Trump’s language yesterday, language that took even Ukraine by surprise. The main update was Ifo, a surprisingly weak release with conditions and expectation printing below the forecast range. Metrics lifted Bunds by around 10 ticks in the minutes after and since have helped lift it to a 128.40 peak and also propped up peers across the board as well.

- Gilts are outperforming vs peers, in a continuation of the strength seen yesterday after poor PMIs and despite soft supply. At a 91.28 peak, but for the most part holding around the midpoint of 91.12-91.28 parameters. UK docket relatively light, supply was unremarkable from the UK, strong enough to keep the benchmark comfortably in the above range. Follows the soft tap on Tuesday, where a chunky price tail sparked notable pressure. Press remains focussed on the budget as more think tanks and other groups offer recommendations as to what Chancellor Reeves should do. Overall, the narrative from such groups is that significant tax cuts are inevitable and as such Reeves may need to break the manifesto pledge around them, in order to raise sufficient funds to cover the gap and avoid having to come back.

- UK sells GBP 4.75bln 4.375% 2030 Gilt: b/c 2.80x (prev. 3.15x), average yield 4.095% (prev. 4.022%), yield tail 0.4bps (prev. 0.1bps), price tail 1.6 ticks.

- Italy sells EUR 2.5bln vs exp. EUR 2-2.5bln 2.10% 2027 BTP Short Term & EUR 3.75bln vs exp. EUR 2-2.5bln 1.10% 2031 and 2.40% 2039 BTPei.

- Germany sells EUR 3.045bln vs exp. EUR 4.0bln 2.50% 2032 Bund: b/c 1.5x (prev. 1.2x), average yield 2.52% (prev. 2.46%), retention 23.88% (prev. 33.13%).

- South Korea will issue JPY 500bln in yen-denominated bonds, according to a Japanese regulatory filing.

- Click for a detailed summary

COMMODITIES

- Choppy price action across the crude complex thus far. Upticks in oil prices was seen following reports that the Israeli army had taken “another step” in the plan to occupy Gaza city spurred a move higher to peaks of USD 63.86/bbl and USD 68.12/bbl for WTI and Brent respectively. However, the move proved somewhat short-lived. Crude hit by a surprise German Ifo survey, with all metrics falling from the prior and both conditions and expectations printing below the forecast range. Potential demand-side concerns from this weighed and sent benchmarks back to fresh lows for the session of USD 63.25/bbl and USD 67.51/bbl respectively. Further bearish impulse potentially from Russia restarting a second unit at the UST-Luga facility and Russia saying Exxon is not the only firm interested in returning to Russia.

- Spot gold is trading off the new ATH at USD 3791/oz made in yesterday's session, with the day's best price USD 12/oz lower at USD 3779/oz. Specifics light thus far, continued focus on the geopolitical drivers outlined above, these factors seemingly helped XAU recoup some of Tuesday’s pressure. However, USD strength is capping a return to mentioned highs.

- 3M LME Copper continues to trade below key USD 10k/ton level and in a tight range amid concerns over Super Typhoon Ragasa. The main move this morning came alongside the German Ifo series, preventing 3M LME Copper from retesting USD 10k/t to the upside and pushing the metal back towards earlier USD 9.96k/T lows. Currently, in the red but just off that trough.

- EU Trade Chief Sefcovic to meet with USTR Greer this week to revive talks on metal tariffs, via Bloomberg.

- US Private Inventories: Crude Stocks -3.82mln (exp. +0.2mln , prev. -3.4mln), Distillate +0.52mln (exp. -0.5mln, prev. +1.9mln), Gasoline Stocks +1.05mln (exp. +0.2mln, prev. -0.7mln), Cushing +0.07mln (prev. -0.38mln)

- Peru's Antamina mine expects to produce 380k metric tons of copper this year (vs 430k tons in 2024). 2026 copper output forecasts at 450k tons. Zinc production is projected at 450k tons this year (vs 270k tons in 2024).

- Trump officials are seeking an equity stake in Lithium Americas (LAC) as part of the renegotiation of a USD 2.3bln loan for the Thacker Pass lithium project; Lithium Americas has offered the administration no-cost warrants that would equate to 5% to 10% of the company’s common shares, according to Reuters.

- China reported its Crude Steel output fell by 0.7% in August 2025 v August 2024 to 77.4 million tonnes.

- Russia's Novatek restarts its second processing unit at UST-Luga complex following a fire.

- Iran's Oil Minister Paknejad says UN sanctions won't create a burden on restrictions of oil sales.

- Click for a detailed summary

NOTABLE DATA RECAP

- German Ifo Expectations New (Sep) 89.7 vs. Exp. 92 (Prev. 91.6); Ifo Current Conditions New (Sep) 85.7 vs. Exp. 86.5 (Prev. 86.4); Ifo Business Climate New (Sep) 87.7 vs. Exp. 89.3 (Prev. 89)

NOTABLE EUROPEAN HEADLINES

- French PM Lecornu is open to a tax on top earners and firms, via BFM TV.

- German Chancellor Merz says that a true reform is needed to fund the German welfare system. Says Germany will make a concrete proposal on pension system reform this year. Says Germany's aviation costs need to be lowered. Says Auto, Steel and Chemical sectors are key sectors in Germany and must remain.

- Swiss KOF: cuts 2026 outlook due to the deterioration in competitive conditions caused by US tariffs and ongoing heightened economic uncertainty, adj. GDP forecast at 0.9% in 2026 (prev. 1.5)

NOTABLE US HEADLINES

- House Democrats will meet on September 29th in Washington, D.C. to discuss government funding, according to Bloomberg.

- OpenAI, Oracle (ORCL), and Softbank (9984 JT) announced five new US data centres; expects new data centre site to create over 25,000 direct jobs and tens of thousands more across the US. The firm continues assessing further potential locations for expansion.

- NVIDIA (NVDA) director Mark A. Stevens sold over 350k common shares at an average price of USD 176.3923/shr on 19 September (vs 178.43 closing price on Tuesday)

- Micron (MU) Q2 2025 (USD): Adj. EPS 3.03 (exp. 2.86), Revenue 11.32bln (exp. 11.21bln). Adj. net income 3.469bln (exp. 3.158bln). Outlook: Q1 EPS 3.75 (exp. 3.07). Q1 revenue 12.5bln (exp. 11.87bln). Shares settled +0.4% after hours.

GEOPOLITICS

NATO-RUSSIA

- US Defense Secretary Hegseth spoke with his Estonian counterpart and affirmed that the US stands with NATO allies, stressing that any incursion into NATO airspace is unacceptable, according to the Pentagon.

- G7 Foreign Ministers' Joint Statement: G7 expresses concern over Russia's latest airspace violations in Estonia, Poland, and Romania; G7 discussed imposing additional economic costs on Russia

RUSSIA-UKRAINE

- Ukrainian President Zelensky said he was surprised at US President Trump’s recent comments on Ukraine but welcomed them as “a very positive signal” that the US and Trump would support Kyiv until the end of the war, according to Reuters.

- Ukraine hits Russia's Neftekhim Salavat plant with drones overnight, says Reuters citing sources.

- Russian Kremlin says the Ukraine war is not an "aimless war" and the idea that Ukraine can win something back is "deeply mistaken".

- Russian Kremlin states that improved relations with US is moving slow than would like; wants to remove 'irritants' in US ties; remains open to areas for profitable cooperation with US

MIDDLE EAST

- French President Macron said he will meet with the Iranian President on Wednesday to discuss the return of UN sanctions, according to Reuters.

- US envoy Barrack said Israel and Syria are close to reaching a “de-escalation” arrangement under which Israel would halt its bombings and Syria would not move military equipment toward the border, with a security agreement to follow, according to Al-Monitor.

- Israel's army has taken "another step" in the plan to occupy Gaza city, via Alhadath citing Walla

CRYPTO

- Bitcoin is a little lower and trades around USD 112.6k whilst Ethereum is holding around USD 4.1k.

APAC TRADE

- APAC stocks eventually traded mixed following a subdued open as the sentiment from Wall Street initially reverberated, but later improved after Chinese cash trade got underway, whilst Hong Kong remained open despite the Super Typhoon.

- ASX 200 declined as gold miners weighed following consecutive sessions of outperformance, while Tech mirrored Wall Street sectoral weakness.

- Nikkei 225 returned from holiday to trade softer in line with the regional tone, though losses were somewhat cushioned by the NVIDIA/OpenAI rally it missed yesterday and a weaker JPY intraday.

- KOSPI was pressured amid the broader global tech pullback and deteriorating South Korean consumer sentiment.

- Hang Seng and Shanghai Comp were choppy and eventually traded in the green, with the former also boosted by Alibaba, whose shares surged after releasing its largest LLM whilst announcing plans to ramp up spending on AI infrastructure to better compete with US rivals.

NOTABLE ASIA-PAC HEADLINES

- New Zealand Finance Minister Willis said Anna Breman will be the new RBNZ Governor, beginning her five-year term on 1st December 2025. Breman will leave her position at the Riksbank on October 10th as she has been appointed the governor of the RBNZ.

- Alibaba (BABA/ 9988 HK) officially released Qwen3-MAX, a 1tln-parameter large language model. CEO announced plans to ramp up spending on AI infrastructure to better compete with US rivals.

- Russian Kremlin states US President Trump is a businessman attempting to pressure global markets into purchasing US oil and gas at elevated prices Praises Trump's desire to bring an end to the conflict. States that Russian army are advancing in Ukraine and dynamics on the frontline are obvious.

- China announces measures to promote service export, via state media.

DATA RECAP

- Australian Weighted CPI YY (Aug) 3.00% vs. Exp. 2.90% (Prev. 2.80%)

- Australian CPI Annual Trimmed Mean YY (Aug) 2.60% (Prev. 2.70%)

- Australian CPI SA MM (Aug) 0.10% (Prev. 0.90%); YY (Aug) 3.00% (Prev. 2.80%)

- Japanese S&P Global Manufacturing PMI Flash SA (Sep) 48.4 (Prev. 49.7); Services PMI Flash SA (Sep) 53.0 (Prev. 53.1)

- Japanese S&P Global Composite Op Flash SA (Sep) 53.0 (Prev. 52.0)

- South Korean Consumer Sentiment (Sep) 110.1 (Prev. 111.4)