US Opening News: US futures firmer whilst USD pulls back. Tariffs & potential shutdown in focus.

29 Sep 2025, 11:29 by Newsquawk Desk

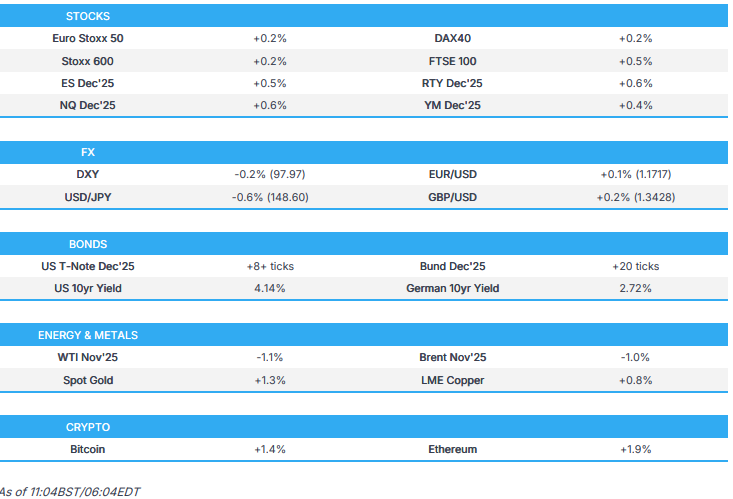

- A firmer start to the week for equities, Euro Stoxx 50 +0.3%, ES +0.5%; focus on a packed labour market agenda for the week and the looming US gov't shutdown.

- President Trump will be meeting with congressional leaders at 20:00BST/15:00ET; ahead of this, Trump has said if the Democrats refuse to make a deal "the country closes".

- USD pulling back from last week's data induced gains, JPY leads into a packed week and supported by BoJ's Noguchi. EUR & GBP also firmer

- Fixed benchmarks in the green, Bunds lead after mostly cooler-than-expected Spanish flash figures, Gilts await Chancellor Reeves

- Crude curtaield by OPEC+ production reports, XAU at another ATH, Copper posting modest gains

- Looking ahead, highlights include ECB’s Cipollone, Muller, Kazaks, Schnabel, Lane, BoE’s Ramsden, Fed’s Waller, Hammack, Musalem, Williams, Bostic. Events include Bank of Israel Announcement, Labour Party Conference (29th Sept - 1st Oct). Earnings from Jefferies, Carnival.

- Click for the Newsquawk Week Ahead.

TRADE/TARIFFS

- The UK will offer to pay more for drugs in a bid to placate US President Trump and pharmaceutical groups, according to the FT.

- US soybean farmers face a crisis as China halts purchases amid the tariff dispute, according to Reuters.

- The EU is plotting a “devastating tariff hit” against UK steelmakers, with officials in Brussels aiming to halve the UK’s tariff-free quotas and double tariffs to 50% under pressure from steel industries in member states, according to The Times.

- South Korea rejected a US request for USD 350bln in cash under a tariff-reduction deal, a senior official said, according to Reuters.

- China is urging the US to oppose the independence of Taiwan, saying it is incompatible with the One China principle.

EUROPEAN TRADE

EQUITIES

- A firmer start to the week for European bourses, Euro Stoxx 50 +0.3%. Largely on a constructive footing, though the periphery is a touch softer. Incremental macro drivers so far a little light for the bloc.

- Sectors mostly in the green, Basic Resources leads given underlying benchmarks, Tech benefits in a bounce from Fridy's pressure. Banking names lag amid softness in yields, Energy hit alongside crude on reports around OPEC+.

- Healthcare supported by the White House will honour a 15% cap on pharmaceutical tariffs as part of trade deals with the EU and Japan, according to CNBC; though, a reported 100% level on the UK offsets.

- Stateside, futures firmer across the board, ES +0.5% & NQ +0.6%. Focus very much on the packed data agenda for the week as a whole, potential gov't shutdown which could impact that data and several Fed speakers.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- Dollar is pulling back from the data induced upside seen last week. Focus now on this week's packed agenda of labour market data, Fed speak and angst into a potential gov't shutdown. DXY has slipped below its 50DMA @ 98.02 and made its way back onto a 97 handle. The next level of support comes via the 25th September trough @ 97.73.

- EUR is taking advantage of the softer USD with incremental macro drivers for the region on the light side over the weekend. Spanish HICP printed in-line with consensus at 3.0% (prev. 2.7%), whilst the M/M metric only picked up to 0.1% from 0.0% (exp. 0.3%). EUR/USD has continued its ascent on a 1.17 handle with a current session peak @ 1.1733. The next upside target comes via the 25th September peak @ 1.1754.

- JPY tops the G10 leaderboard into a pivotal week of domestic events including Tankan and the LDP leadership election. Strength this morning was spurred by BoJ's Noguchi, noting that upside risks are becoming more important in making policy decisions and the need to adjust policy has heightened. USD/JPY has delved as low as 148.48, taking out the 25th September low @ 148.55. Focus is now on a test of the 200DMA to the downside @ 148.41.

- Sterling firmer, marginally outpacing the EUR against the USD thus far. Awaiting the speech from Chancellor Reeves at the party conference, due around 12:00BST. Cable has risen as high as 1.3450 with the next resistance point coming via the 50DMA @ 1.3467.

- Antipodeans eventually gained after both initially struggling to fully benefit in APAC hours from the softer dollar amid a cautious risk tone at the time. Attention stays on tomorrow’s RBA meeting, where markets price only a slim 8% chance of a 25bps cut. Little reaction to the PBoC's firmer fix.

- PBoC set USD/CNY mid-point at 7.1089 vs exp. 7.1258 (Prev. 7.1152)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- Overall, a firmer start to the week. Bunds just off highs in a 128.29 to 128.57 band. Slightly outpacing USTs in terms of gains this far, surpassing last week’s 128.41 peak and looking to 129.02 from September 18th. Relative outperformance that is likely a function of three of the four main Spanish Flash inflation measures printing cooler than forecast.

- USTs bid, though as alluded to above the magnitude of performance is slightly more modest. At the top-end of a 112-08+ to 112-17 band, extending above Friday’s 112-15 best but shy of 112-22 and 113-00 from the two preceding sessions. Hammack (2026) was on CNBC this morning, stuck to her language from last week in outlining a need to maintain restrictive policy, describing the current level as mildly restrictive and that the Fed is a short distance from neutral.

- Gilts also in the green, opened alongside the discussed Spanish data and seemingly caught a tailwind from this. Focus almost entirely on Chancellor Reeves' upcoming speech, thus far in remarks to Bloomberg she said her commitment to not increasing the tax burden via VAT, Income Tax or NI stand. Remarks that, if held to, limit the Chancellor's revenue generating sources with the general view being that she will need to raise at least GBP 20bln via taxes during the Autumn Budget. No significant moves to those interviews. Benchmark at a 90.82 peak, taking out Friday’s 90.74 best in the process. Resistance ahead at 91.11, 91.12 and 91.28 from last week.

- Click for a detailed summary

COMMODITIES

- Crude clipped by OPEC+ production reports. Further bearishness stemming from the resumption of flows on the Ceyhan pipeline and potentially from Moldova. However, we remain conscious that the actual impact of any OPEC+ increase is likely to be less than the headline suggests, as in August OPEC cautioned that a lack of spare capacity among nations meant the enacted supply increase would be less than the headline figure for September; a narrative that remains in play for October and November.

- WTI and Brent weighed on this morning, down by c. USD 1.00/bbl at most and at respective lows of USD 64.72/bbl and USD 69.27/bbl.

- Continued upward action for precious metals, both spot gold and silver at fresh highs for the day and yet another ATH for XAU at USD 3819.8/oz thus far. Specifics for the space light with the yellow metal firmer despite the constructive risk tone but potentially benefiting from apprehension into the week’s key labour market data from the US and the looming government shutdown, a shutdown that could impact the delivery of Friday’s BLS report. USD pressure is another source of strength.

- Copper was modestly firmer in APAC trade, benefiting from the USD though with gains capped by the cautious risk tone at the time and apprehension into a packed week. Since, 3M LME Copper has continued to tick higher, at a USD 10.29k peak but shy of last week’s USD 10.319k best.

- OPEC+ will likely raise oil production quotas by at least 137k bpd at its October 5th meeting, according to Reuters, citing sources. Subsequently, Kpler's Bakr, citing sources on OPEC+, reports "there have been no consultations with regards to the group’s November policy yet.".

- An Iraqi OPEC delegate said the country can boost exports beyond current levels once the Iraq–Turkey pipeline resumes and new projects come online, according to the state news agency.

- Click for a detailed summary

NOTABLE DATA RECAP

- Spanish CPI YY Flash NSA (Sep) 2.9% vs. Exp. 3.0% (Prev. 2.7%); Core 2.3% (prev. 2.4%)

- Spanish HICP Flash YY (Sep) 3.0% vs. Exp. 3.0% (prev. 2.7%)

- Spanish HICP Flash MM (Sep) 0.1% vs. Exp. 0.3% (Prev. 0.0%); CPI MM Flash NSA (Sep) -0.4% vs. Exp. -0.2% (Prev. 0.00%)

- EU Consumer Confidence Final (Sep) -14.9 vs. Exp. -14.9 (Prev. -14.9); Selling Price Expectations (Sep) 6.9 (Prev. 6.7, Rev. 6.8); Consumer Inflation Expectations (Sep) 24.0 (Prev. 25.9, Rev. 25.8)

- UK Mortgage Lending (Aug) 4.308B GB vs. Exp. 4.8B GB (Prev. 4.522B GB, Rev. 4.506B GB); Approvals (Aug) 64.68k vs. Exp. 64.5k (Prev. 65.352k, Rev. 65.161k)

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer urged Labour to unite for the “fight of our lives” against Nigel Farage’s Reform UK, as Starmer faces dire poll ratings and questions over his leadership ahead of the party conference, while ministers unveiled plans for three new towns as part of a broader housebuilding push, according to the FT.

- UK Chancellor Reeves risks a confrontation with the head of the government’s fiscal watchdog over plans to scrap her annual spring forecast, according to Bloomberg.

- Separately, UK Chancellor Reeves says she will work to bring inflation down; reiterates commitment to fiscal rules and stability and commitments to not increasing VAT, Income Tax or NI. UK does not need a wealth tax.

- ECB’s Makhlouf said the ECB is “near the bottom” of its easing cycle but will need to remain vigilant as the impact of tariffs on most EU exports is still to feed through. He added that his mind is not set on how to vote at the upcoming meeting at the end of October, according to FT.

- Bank of Italy kept the countercyclical capital buffer for banks in Q4 at zero, according to Reuters.

- Portugal will raise taxes on foreign home buyers amid a surge in property prices, according to Reuters.

- Switzerland voted to abolish a century-old system of taxing property, a move that will lower dues for homeowners and potentially boost real estate prices, according to Reuters.

- The head of Switzerland’s right-wing People’s Party said the government needs to find a compromise with UBS (UBSG SW) to raise the bank’s capital requirements, according to Reuters.

- SNB is lowering the threshold factor for the remuneration of sight deposits from 18 to 16.5, as of November 1st.

NOTABLE US HEADLINES

- Fed's Hammack (2026 voter) says it is a challenging time for monetary policy. Labour market is broadly in balance. More difficult to see that tariffs will be a one-time impact. Need to maintain restrictive policy, current policy is mildly restrictive. Short distance from neutral. Will not get to 2% inflation target until late 2027 or early 2028.

- US President Trump posted an image of himself “firing” Fed Chair Powell, via Truth Social.

- New York City Mayor Eric Adams dropped his bid for re-election, according to the New York Post.

- US President Trump said he will discuss the looming government shutdown with congressional leaders on Monday and believes Democrats may want to make a deal; he added that if Democrats refuse to make a deal, "the country closes", according to Reuters. US President Trump will meet with the congressional leaders at 20:00BST/15:00ET, via Punchbowl

- Electronic Arts (EA) is near a roughly USD 50bln deal to go private, according to WSJ.

- Chinese factory workers are facing harsh conditions while racing to produce Apple’s (AAPL) new iPhone 17 lineup, according to China Labour Watch.

- US Vice President JD Vance said he is confident the US has separated TikTok from ByteDance, according to Reuters.

- Occidental Petroleum (OXY) is said to be in talks to sell its OxyChem petrochemical unit in a deal worth at least USD 10bln, according to the FT.

GEOPOLITICS

NATO

- Russian President Putin is to deliver a major speech this week, according to multiple media outlets.

- Belarus's President said that if NATO threatens to shoot down Russian and Belarusian fighter jets, the response will come immediately, according to Reuters.

- NATO will boost its presence in the Baltic region following drone incidents in Denmark, according to Reuters.

- Denmark announced that unknown drones were spotted over several military facilities on Friday night, including the country’s main air base Karup, which houses Denmark’s F-16s and F-35s, according to Reuters.

RUSSIA-UKRAINE

- Russian missiles and drones struck Ukraine in a “savage” 12-hour attack, according to Reuters.

- Russian sources said the Russian army launched strikes targeting military sites in Kyiv and its surroundings, as well as weapons depots and air defence systems.

- Poland closed its airspace after a “massive” Russian attack on Ukraine’s capital killed at least four people, according to Reuters.

- Ukrainian President Zelensky said he expects new EU sanctions on Russia this week, according to Reuters.

- Russian Foreign Minister Lavrov said no one expects a return to Ukraine’s 2022 borders, calling it politically blind, according to Reuters.

- Ukraine said drones struck an oil pumping station in Russia’s Chuvashia region, according to Reuters.

- The Kremlin said it has received no signals from Kyiv regarding the resumption of Russia-Ukraine talks, via RIA.

ISRAEL-HAMAS

- US President Trump told Axios his 21-point Gaza peace plan is in the final stages, saying it could end the war and open the way for wider Middle East peace. The plan, drafted by Steve Witkoff and Jared Kushner, includes a permanent ceasefire, release of hostages within 48 hours, gradual Israeli withdrawal, release of Palestinian prisoners, a post-war governing mechanism in Gaza without Hamas, Arab and Muslim funding, disarmament of Hamas, amnesty or safe passage for its members, no Israeli annexation of Gaza or the West Bank, an Israeli commitment not to attack Qatar again, and a future path to Palestinian statehood after reforms to the Palestinian Authority, according to Axios.

- Israeli PM Netanyahu discussed President Trump’s 21-point Gaza peace plan, saying priorities are freeing hostages and dismantling Hamas while expressing doubt over Palestinian Authority reform, according to Fox News.

- Israel’s Channel 12 reported that turning the Gaza Strip into an international trade zone is one of the clauses of the Trump plan.

- Israel is ready to consider withdrawing from a number of areas in Syria where IDF forces are deployed, but not from the Hermon Crown, according to Kann News.

- Israel’s Kan TV quoted a source close to PM Netanyahu as saying there are “significant gaps” between him and the White House over the terms of ending the war in the Gaza Strip.

- US President Trump told Reuters in a phone interview that he has gotten a "very good response" from Israel and Arab leaders to the Gaza peace plan proposal, adding that "everybody wants to make the deal" and he hopes to finalize it in a meeting with Netanyahu on Monday; he said the proposal is aimed not just at Gaza but at reaching a broader peace in the Middle East, according to Reuters.

- The US and Israel are reportedly very close to an agreement on President Trump’s plan to end the war in Gaza, though Hamas still needs to agree, according to officials cited by Axios.

IRAN

- A Russian and Chinese push to delay the return of Iran sanctions for six months failed at the UN Security Council, according to Reuters.

- Russia’s Deputy UN Envoy said the reimposition of UN sanctions on Iran could have very adverse consequences and lead to an escalation in the Middle East, according to Reuters.

- Israeli PM Netanyahu told Fox News that 450 kilos of enriched uranium remain, saying Israel knows where it is and shares that information with the US, and that both countries knew before bombing Iranian nuclear sites they would not be able to eliminate it.

- An Iranian Armed Forces spokesman said nuclear energy is a national need and that Iran will not abandon it, according to Reuters.

- Iraqi media reported the discovery of an unidentified spy drone near the border with Iran.

- Iran’s Parliamentary National Security Committee said the country has not yet withdrawn from the Nuclear Non-Proliferation Treaty, according to Reuters.

- The European Troika warned Iran against any “escalatory” actions following the reimposition of sanctions, according to Reuters.

- Iranian President Pezeshkian said the US offered to postpone snapback sanctions by three months if Tehran handed over all its enriched uranium.

OTHERS

- The US is preparing options for military strikes on drug targets inside Venezuela, with potential drone strikes on traffickers and labs being considered, though President Trump has not yet approved any action and talks are ongoing through Middle Eastern intermediaries, according to NBC News.

- US President Trump plans to attend a gathering of top generals and admirals in Virginia this week, an event described as a “pep rally” for senior military brass where Defense Secretary Hegseth will outline his vision of the Pentagon as the “Department of War” and set new standards for military personnel, according to CNN.

- The Israeli army announced it bombed a Hezbollah weapons depot in southern Lebanon, according to Reuters.

- Chinese President Xi is reportedly planning to press US President Trump to formally state that the US opposes Taiwan’s independence, according to WSJ.

- Pro-EU party won Moldova polls with over 50% of vote, according to AFP citing the official results.

- The North Korean and Chinese Foreign Ministers held talks, though details remain limited, according to KCNA.

APAC TRADE

- APAC stocks eventually traded mostly firmer following the positive Wall Street performance on Friday, albeit participants remain cautious ahead of a risk-packed week that culminates with Friday’s US jobs report.

- ASX 200 advanced, led by strength in gold miners and a rebound in healthcare, while traders looked ahead to tomorrow’s RBA decision in which Australia's Big 4 banks expect no change in rates.

- Nikkei 225 underperformed amid yen strength, with sentiment also weighed by the ex-dividend date for end-of-month payouts and risk trimming ahead of the BoJ Tankan Survey and the LDP leadership vote later in the week.

- Hang Seng and Shanghai Comp initially diverged, with Hong Kong buoyed by tech gains and foreign inflows. The Mainland swung between modest gains and losses heading into its weeklong break amid National Day and the Mid-Autumn Festival, whilst reports also suggested Chinese President Xi is reportedly planning to press US President Trump to formally state that the US opposes Taiwan’s independence, according to WSJ.

- KOSPI was lifted with tech spearheading the gains, whilst reports over the weekend suggested South Korea rejected a US request for USD 350bln in cash under a tariff-reduction deal.

- Nifty 50 traded with cautious gains after Friday's losses, and with traders looking ahead to the RBI policy announcement later this week.

NOTABLE ASIA-PAC HEADLINES

- China’s top economic planner, the NDRC, held a symposium on Sunday hosted by agency head Zheng Shanjie, inviting private enterprises to submit opinions and suggestions on expanding effective investment during the 15th Five-Year Plan period (2026–30), according to the NDRC’s official WeChat account via Global Times.

- Taiwan is eyeing an expanded tech presence in India amid surging US demand, according to the chief of a trade body, Reuters reported.

- BoJ's Noguchi says that Japan is moving towards 2% inflation target; need to adjustment to policy has heightened; economy and prices face downside risks. Vital to adjust easing at right timing. Need to conduct policy in flexible manner. Upside risks becoming more important in making policy decision.

- China's Communist Party will be holding its fourth plenum across October 20th-23rd, via Xinhua. Subsequently, China's Politburo has studied draft of next five-year plan; continues to enhance development momentum. Puts emphasis on high-quality growth, reform and opening.

- China State Planner Official says China's new policy-base financial tool amounts to 500bln Yuan.