European Opening News: European futures higher and Trump delays pharma tariffs

02 Oct 2025, 06:41 by Newsquawk Desk

- APAC stocks were firmer, with gains across the board following a positive handover from Wall Street, where tech outperformed, whilst the US jobs reports this week look set to be delayed after CR votes failed again on Wednesday, as expected.

- Fitch said a US government shutdown does not have near-term implications for the ‘AA+’/stable US sovereign rating; S&P estimated the shutdown could reduce GDP growth by 0.1–0.2 ppts per week.

- 10yr JGB futures came under pressure after the 10yr JGB auction, which printed a lower cover ratio than the prior sale and followed the recent 2yr JGB auction that saw the weakest cover ratio since 2009.

- The US will provide Ukraine with intelligence for missile strikes deep inside Russia, and US officials are asking NATO allies to provide similar support, via WSJ.

- Looking ahead, highlights include Swiss CPI (Sep), EZ Unemployment (Aug), US Challenger Layoffs (Sep), BoJ’s Uchida, Fed’s Logan, ECB’s de Guindos, BoC’s Mendes, Supply from Spain, France, and the UK.

- Due to the US government shutdown, the following US data will not be released: Weekly Claims, Factory Orders (Aug), Durable Goods Rev. (Aug).

SNAPSHOT

US TRADE

EQUITIES

- US stocks extended recent gains, overcoming earlier weakness tied to the government shutdown. The Nasdaq led the advance, while sector performance was mixed.

- SPX +0.37% at 6,711, NDX +0.49% at 24,801, DJI +0.09% at 46,441, RUT +0.24% at 2,442

- Click here for a detailed summary.

US GOVERNMENT SHUTDOWN

- Democrats’ continuing resolution (CR) again failed, via Punchbowl's Jake Sherman.

- US VP Vance said he does not think the government shutdown will last long and vowed to do everything possible in the coming weeks to ensure people receive essential services. He warned layoffs would be necessary if the shutdown continues and offered to meet with Schumer and Democrats to discuss the situation, according to Reuters.

- White House Press Secretary Leavitt said layoffs are imminent and that a replacement nominee for the BLS will be announced soon.

- US Senate Majority Leader Thune and Senate Minority Leader Schumer might meet in the next day or two, according to Punchbowl.

- US President Trump plans to cancel Western hydrogen hubs amid the government shutdown fight, according to Bloomberg.

- US President Trump posted that Republicans must use the Democrat-forced closure to clear out dead wood, waste, and fraud, adding that billions of dollars can be saved, via Truth Social.

- Fitch said a US government shutdown does not have near-term implications for the ‘AA+’/stable US sovereign rating, though regular reliance on continuing resolutions highlights continued weakness in fiscal policymaking. Fitch added that despite increased uncertainty around US policy, the US dollar’s predominant reserve currency status is expected to continue for the foreseeable future, and noted that reversing previously enacted Medicaid cuts would not meaningfully impact near-term deficit forecasts, as the effects would mostly be felt after 2028, via Fitch Ratings.

- S&P warned that the US government shutdown adds uncertainty to the economic outlook, with extended delays in key economic data releases potentially complicating Fed monetary policy decisions. The agency estimated the shutdown could reduce GDP growth by 0.1–0.2 ppts per week.

NOTABLE HEADLINES

- US President Trump said he really believes Fed Chair Powell is an obstructionist, via Truth Social.

- Fed’s Goolsbee (2025 voter) said he is starting to get more concerned about inflation moving the wrong way and that counting on it being transitory makes him nervous. He noted that with the BLS down, there are limited indicators on inflation, said he hopes tariff impacts will prove transitory, and added that while the underlying economy is strong enough to allow rates to come down a fair amount, the Fed should be careful, according to Reuters.

- BoC minutes said members agreed that while near-term uncertainty around US tariffs had diminished, uncertainty around USMCA renegotiation was coming into greater focus. They discussed keeping the policy rate at 2.75% or lowering it by 25bps to 2.5%, and the Governing Council judged the balance of risks favoured a cut. With the economy weaker and inflationary pressures more contained, members decided to reduce the policy rate to 2.5% to better balance risks going forward, according to the BoC.

NOTABLE US EQUITY HEALINES

- TikTok employees view Adam Presser as a likely candidate to lead the new US TikTok, though the deal has not yet been finalised and the CEO appointment could take time, according to The Information. Presser is the right-hand person to the current TikTok CEO, Shou Zi Chew.

- Intel (INTC) is reportedly in early talks to add AMD (AMD) as a foundry customer, via Semafor.

- Apple (AAPL) has shelved its headset revamp to prioritise Meta-style AI glasses (META), according to Bloomberg.

DATA RECAP

- Atlanta Fed GDPnow (Q3): 3.8% (prev. 3.9%)

TRADE/TARIFFS

- US President Trump is delaying pharmaceutical tariffs as the administration negotiates drug prices, after previously threatening triple-digit tariffs on imports starting Wednesday. A White House official said the plan has been paused while talks continue with pharmaceutical giants to avoid higher tariffs on name-brand products, similar to the deal announced with Pfizer on Tuesday, via Politico.

- US President Trump said soybean farmers are being hurt because China is not buying for negotiating reasons only, adding that tariffs have generated so much money the administration will use a portion to help farmers. He said he will meet Chinese President Xi in four weeks, with soybeans a major topic of discussion, declaring “MAKE SOYBEANS, AND OTHER ROW CROPS, GREAT AGAIN!” via Truth Social.

- Preparations for US President Trump’s visit to Asia have ground to a halt amidst the government shutdown, Nikkei reported, with officials at the embassies of Malaysia, Japan, and South Korea scrambling to gather information ahead of his visit in just over three weeks.

- South Korea’s Foreign Minister said South Korea and the US have broadly reached an agreement in the security sector, Yonhap reported.

- Brazil and the US are working to arrange an in-person meeting between Presidents Lula and Trump, according to Bloomberg.

APAC TRADE

EQUITIES

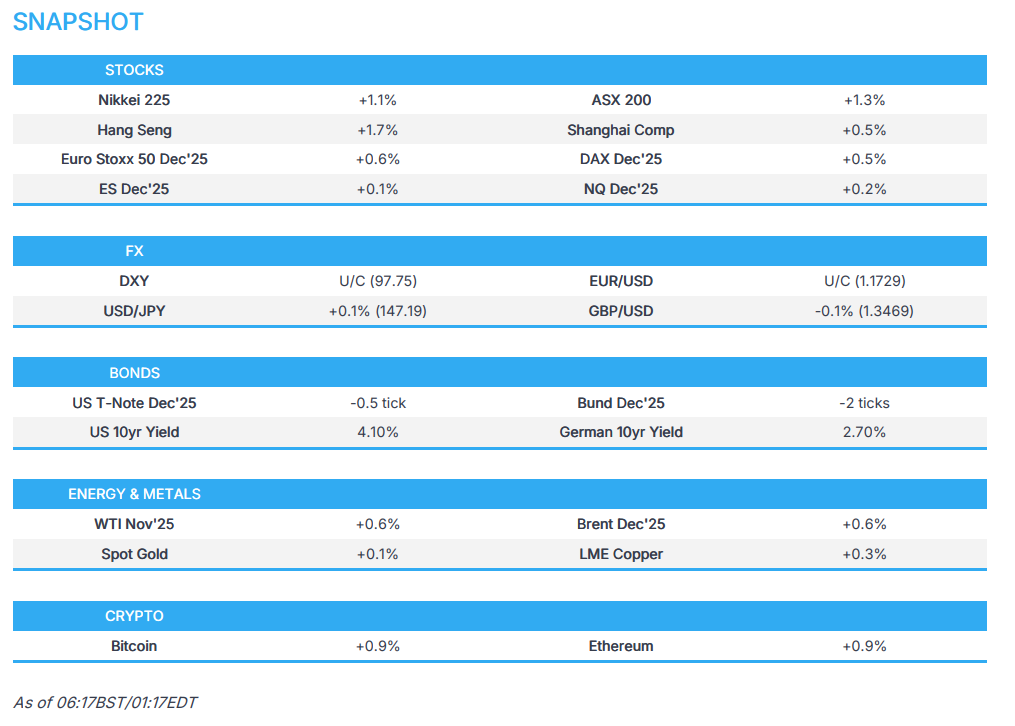

- APAC stocks were firmer, with gains across the board following a positive handover from Wall Street, where tech outperformed, whilst the US jobs reports this week look set to be delayed after CR votes failed again on Wednesday, as expected.

- ASX 200 was propped up by strength in gold and mining names while defensive sectors lagged, with no reaction seen to the RBA Financial Stability Review, which suggested Australia’s financial system remains well positioned to navigate a period of elevated global uncertainty.

- Nikkei 225 saw upside led by metals and pharma stocks, though gains were capped as the JPY trimmed earlier losses.

- Hang Seng conformed to regional gains and played catch-up to yesterday’s price action during the National Day closure, though momentum was limited by the absence of Stock Connect, with Mainland China remaining shut until next Thursday.

- KOSPI outperformed and hit a fresh record high, overlooking stronger-than-expected CPI, with gains driven by surges in SK Hynix and Samsung Electronics after both firms partnered with OpenAI under the Stargate initiative. Sentiment was also supported by news that South Korea and the US agreed on a basic security framework.

- US equity futures (ES +0.1%, NQ +0.2%) traded with an upward bias despite delayed US labour data amid the government shutdown, with focus on how long the current stalemate will last and the Fed’s reduced visibility ahead of the 29th October FOMC announcement.

- European equity futures are indicative of a firmer cash open with the Euro Stoxx 50 future +0.6% after cash closed +1.0% on Wednesday.

FX

- DXY was largely unchanged, chopping in a narrow range between 97.65–97.80 on either side of its 100DMA at 97.78 amid quiet newsflow. The US Jobless Claims data due Thursday is delayed by the government shutdown, and hopes are low for Friday’s NFP release.

- EUR/USD held steady above 1.1700 in a narrow range with EUR-specific updates light and the Eurozone docket sparse. The pair remains within yesterday’s 1.1715–1.1779 range.

- GBP/USD held a slight downward bias after yesterday’s gains, with the pair sandwiched between its 50DMA at 1.3463 and 100DMA at 1.3496, and trading within yesterday’s 1.3435–1.3521 range.

- USD/JPY was choppy after initially finding support at 147.00 and then briefly dipping under the level despite a lack of clear drivers overnight, with the pair consolidating after recent losses.

- Antipodeans were subdued, with AUD/USD initially hampered by a short-lived modest pullback in copper overnight while NZD/USD was initially flat before adopting an upward bias, with newsflow for both currencies light.

FIXED INCOME

- 10yr UST futures held an upward bias following the prior day’s bull steepening as the government entered shutdown and ADP painted another bleak picture of the labour market, with Jobless Claims data delayed amid a lack of progress to reopen the government.

- Bund futures conformed to broader price action in the complex, with moves likely to be macro-dictated amid a quiet Eurozone calendar for Wednesday.

- 10yr JGB futures initially moved higher in line with Western peers, but later came under pressure after the 10yr JGB auction, which printed a lower cover ratio than the prior sale and followed the recent 2yr JGB auction that saw the weakest cover ratio since 2009.

- Japan sold JPY 2.6tln 10yr JGB; b/c 3.34x (prev. 3.92x), average yield 1.6350% (prev. 1.6120%)

COMMODITIES

- Crude futures took a breather following the prior day’s decline, with some of Wednesday’s weakness attributed to Saudi Aramco cutting LPG prices to the lowest since August 2023 in a move aimed at bolstering sales amid rising competition. Crude benchmarks also saw some short-lived upside volatility at the Australia/Japan/South Korea open.

- Spot gold was ultimately flat alongside a contained dollar and quiet newsflow, with profit-taking likely as traders locked in gains from the recent rally, which stalled just shy of the USD 3,900/oz mark.

- Copper futures were firmer in line with the broader risk tone and despite the absence of demand from its largest buyer, China, while some also flagged emerging supply risks in Chile and Indonesia.

- Glencore’s (GLEN LN) Lomas Bayas mine in Chile said its mining operations will continue normally as crews work to fight the fire, according to Reuters.

- Alberta will apply to a crude oil pipeline to Canada’s major projects office by spring 2026, leading early planning and engineering work to determine the route, size and cost of the proposed line to British Columbia’s northwest coast, according to Reuters.

- Goldman Sachs said upside risks have intensified further for their mid-2026 and Dec-2026 gold price forecasts of USD 4,000/oz and USD 4,300/oz respectively, and reiterated that gold remains their highest-conviction long commodity recommendation, according to Reuters.

CRYPTO

- Bitcoin saw modest gains overnight in line with broader sentiment across APAC markets and hovered around USD 119k.

NOTABLE ASIA-PAC HEADLINES

- The RBA’s Financial Stability Review said Australia’s financial system remains well positioned to navigate elevated global uncertainty, with the largest risks to stability coming from abroad, including high and rising government debt in major economies, stretched asset valuations and leverage in global markets, and heightened geopolitical and operational risks. The RBA said most households with mortgages are keeping up with repayments and have built savings buffers, many businesses have established financial buffers, and Australian banks continue to maintain high levels of capital and liquidity. It underscored the importance of maintaining prudent lending standards and strengthening operational resilience via the RBA.

- A BoK official said the significant impact of US tariffs on exports has not yet been observed, but effects are expected to become more apparent next year, according to Reuters.

DATA RECAP

- Australian Goods/Services Exports (Aug) -7.8% (Prev. 3.30%)

- Australian Goods/Services Imports (Aug) +3.2% (Prev. -1.30%)

- Australian Balance on Goods (Aug) 1.825B vs. Exp. 6.20B (Prev. 7.31B)

- Australian Household Spending MM (Aug) 0.10% (Prev. 0.50%, Rev. 0.40%)

- South Korean CPI Growth YY (Sep) 2.1% vs. Exp. 2.0% (Prev. 1.7%)

- South Korean CPI Growth MM (Sep) 0.5% vs. Exp. 0.4% (Prev. -0.1%)

- South Korean Current Account Bal NSA (Aug) 9.15B (Prev. 10.78B, Rev. 10.78B)

GEOPOLITICS

RUSSIA-UKRAINE

- The US will provide Ukraine with intelligence for missile strikes deep inside Russia, and US officials are asking NATO allies to provide similar support, via WSJ.

- The G7 agreed on the importance of trade measures, including tariffs and import–export bans, to curb Russian revenue, according to Reuters.

EU/UK

NOTABLE HEADLINES

- The UK government is reportedly nearing a critical minerals deal with Greenland, via Politico.

- The UK will exempt newly listed company shares from the 0.5% stamp duty tax, in a move officials hope will boost liquidity and attract more London listings, via FT.

NOTABLE EUROPEAN EQUITY HEALINES

- Siemens (SIE GY) is said to be studying a spinoff of its stake in Siemens Healthineers (SHL GY), according to Bloomberg, citing sources.