US Opening News: DXY lower, USTs contained & US futures higher into a thin data docket

02 Oct 2025, 11:55 by Newsquawk Desk

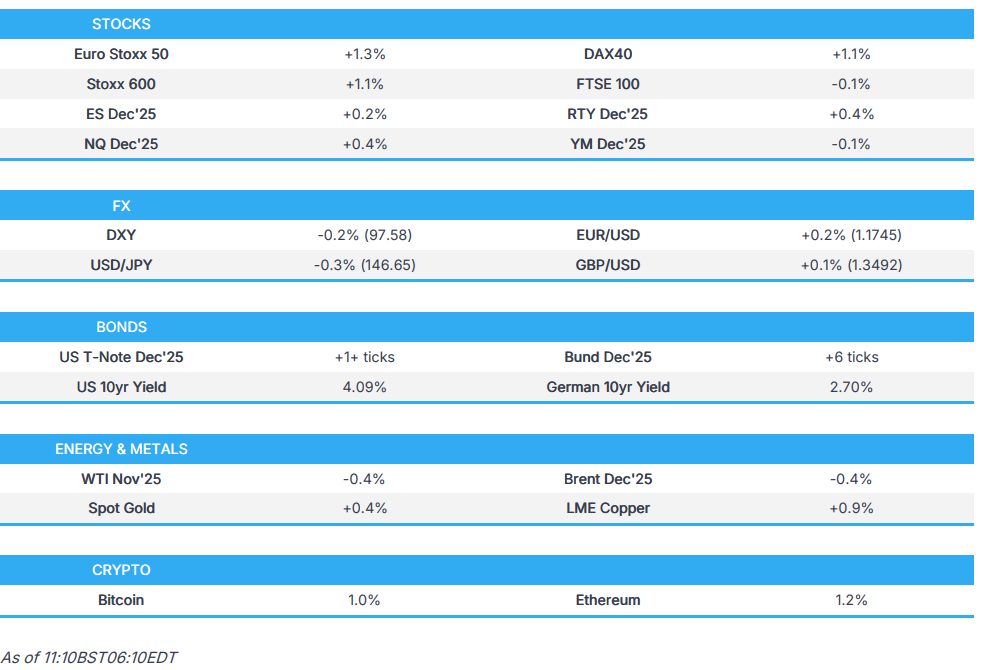

- European bourses are mostly higher as the solid start to the quarter continues, Euro Stoxx 50 +1.3%; US futures marginally extend on Wednesday's gains, ES +0.3%

- DXY currently lower for a 5th consecutive session, peers modestly firmer across the board with JPY leading

- EGBs softer into supply but despite mixed/tepid taps the complex has lifted back to initial marginal peaks, USTs flat with the docket thinner than usual

- Crude began firmer but has since pulled back to lows despite a lack of newsflow, spot gold has taken a slight breather while base metals remain underpinned

- Looking ahead, highlights include US Challenger Layoffs (Sep), Chicago Fed BLS Unemployment forecast, BoJ’s Uchida, Fed’s Logan, ECB’s de Guindos, BoC’s Mendes

- Due to the US government shutdown, the following US data will not be released: Weekly Claims, Factory Orders (Aug), Durable Goods Rev. (Aug)

- Click for the Newsquawk Week Ahead.

US GOVERNMENT SHUTDOWN

- US President Trump plans to cancel Western hydrogen hubs amid the government shutdown fight, according to Bloomberg.

- US President Trump posted that Republicans must use the Democrat-forced closure to clear out dead wood, waste, and fraud, adding that billions of dollars can be saved, via Truth Social.

- S&P warned that the US government shutdown adds uncertainty to the economic outlook, with extended delays in key economic data releases potentially complicating Fed monetary policy decisions. The agency estimated the shutdown could reduce GDP growth by 0.1–0.2 ppts per week.

TRADE/TARIFFS

- Preparations for US President Trump’s visit to Asia have ground to a halt amidst the government shutdown, Nikkei reported, with officials at the embassies of Malaysia, Japan, and South Korea scrambling to gather information ahead of his visit in just over three weeks.

- South Korea’s Foreign Minister said South Korea and the US have broadly reached an agreement in the security sector, Yonhap reported.

- Brazil and the US are working to arrange an in-person meeting between Presidents Lula and Trump, according to Bloomberg.

- Japan and US reportedly arranging a visit by US President Trump to Japan on October 27, according to Japanese press.

- The EU plans to hike steel import tariffs to 50%, according to a draft proposal seen by Bloomberg.

EUROPEAN TRADE

EQUITIES

- European bourses are mostly higher as the solid start to Q4 continues, Euro Stoxx 50 +1.3%. FTSE 100 -0.1% is the main outlier after the healthcare and energy-led gains seen on Wednesday. From a macro perspective, it is very much a case of more of the same as incremental drivers remain light aside from the overhang of the US government shutdown.

- Sectors mostly firmer, Tech outperforms after the strength on Wall St.; Autos firmer with heavyweight Ferrari supported by a broker upgrade. Luxury also strong after Brunello Cucinelli numbers, supporting peers.

- Stateside, futures are modestly firmer in a slight continuation of the gains seen yesterday after ADP drove a dovish move, ES +0.2%.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is currently lower for a 5th consecutive session. Continued focus on the shutdown, which has trimmed the data docket, as such other prints e.g. the Chicago Fed measure may draw greater attention. DXY has delved as low as 97.53 but is holding above yesterday's trough @ 97.46.

- Euro is a touch firmer after a choppy Wednesday. Specifics very light. EUR/USD is currently contained within yesterday's 1.1715-79 range.

- Sterling also slightly firmer against the UST but relatively even against the EUR. The latest BoE DMP report showed firms year-ahead own-price inflation was unchanged at 3.7%, whilst expectations for year-ahead CPI inflation rose by 0.1 percentage points to 3.4%. Cable has moved back onto a 1.35 handle but is yet to approach yesterday's best @ 1.3527.

- JPY firmer, with USD/JPY down to a 146.61 low before returning to a 147 handle. Attention on BoJ's Uchida who noted that the Bank will keep hiking rates if the economic outlook is realised.

- Antipodeans both in the green but the Kiwi is currently leading. Specifics light thus far, particularly with China away.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- JGBs hit overnight by a weak 10yr tap. No followthrough to remarks from BoJ's Uchida thereafter, though his positive lens on the Tankan survey underscores the narrative that a hike at the October meeting is the more likely outcome as things stand.

- USTs contained in a very narrow range. Specifics unsurprisingly light with the US government shutdown still underway. Currently, USTs chop around the unchanged mark in a 112-25+ to 112-30+ band, entirely within but at the upper end of yesterday’s 112-12 to 112-31 parameters.

- EGBs saw a slightly softer start to the day, though within recent parameters. Specifics light aside from supply. Overall, the auctions were slightly soft but still the passing of the morning's docket was sufficient to bring the benchmarks back to earlier highs and marginally firmer, with gains of a handful of ticks in Bunds at best.

- Gilts spent the morning near-enoguh flat into supply. A few updates around the Autumn Budget beforehand, but nothing that shifts the dial. Supply on face value was ok, though the cover was the lowest since 2022.

- Japan sold JPY 2.6tln 10yr JGB; b/c 3.34x (prev. 3.92x), average yield 1.6350% (prev. 1.6120%)

- Click for a detailed summary

COMMODITIES

- Crude spent the morning in a thin c. USD 0.60/bbl bound. However, the complex came under some modest pressure to respective lows of USD 61.22/bbl and USD 64.80/bbl for WTI and Brent respectively, nothing fresh behind the pressure.

- Overnight, a spike to session highs occured around an hour after a more modest move higher on reports in the WSJ that the US is to provide Ukraine with intelligence for missile strikes deep inside Russia, and are asking NATO allies to provide similar insight.

- Spot gold taking a slight breather from its recent rally, though it remains near the USD 3895/oz ATH into a thinner than usual docket.

- Base metals continue to gain despite the absence of its largest buyer, China. 3M LME Copper extended above USD 10.40k/t during APAC trade, a move that has continued to a USD 10.51k/t peak.

- Goldman Sachs said upside risks have intensified further for their mid-2026 and Dec-2026 gold price forecasts of USD 4,000/oz and USD 4,300/oz respectively, and reiterated that gold remains their highest-conviction long commodity recommendation, according to Reuters.

- Kazakhstan's Energy Minister says they are doing everything possible to implement compensation plan; sees Kazakhstan oil output at 90mln tons in 2026

- Click for a detailed summary

NOTABLE DATA RECAP

- Swiss CPI YY (Sep) 0.2% vs. Exp. 0.3% (Prev. 0.2%); MM (Sep) -0.2% vs. Exp. -0.2% (Prev. -0.1%)

NOTABLE EUROPEAN HEADLINES

- BoE DMP: Expectations for year-ahead CPI inflation rose by 0.1 percentage points to 3.4% in the three months to September. The corresponding measure for three-year ahead CPI inflation expectations also remained unchanged at 2.9% in the three months to September.

NOTABLE US HEADLINES

- Fed’s Goolsbee (2025 voter) said he is starting to get more concerned about inflation moving the wrong way and that counting on it being transitory makes him nervous. He noted that with the BLS down, there are limited indicators on inflation, said he hopes tariff impacts will prove transitory, and added that while the underlying economy is strong enough to allow rates to come down a fair amount, the Fed should be careful, according to Reuters.

- Apple (AAPL) has shelved its headset revamp to prioritise Meta-style AI glasses (META), according to Bloomberg.

- US President Trump's Administration is reportedly working with Pharma, AI, Energy, Ship Building, Battery Products and other sectors according to Reuters sources.

GEOPOLITICS

- The US will provide Ukraine with intelligence for missile strikes deep inside Russia, and US officials are asking NATO allies to provide similar support, via WSJ.

- The G7 agreed on the importance of trade measures, including tariffs and import–export bans, to curb Russian revenue, according to Reuters.

CRYPTO

- Citi crypto forecasts, 2025: Bitcoin USD 133k (prev. 135k), Ether USD 4.5k (prev. 4.3k).

APAC TRADE

- APAC stocks were firmer, with gains across the board following a positive handover from Wall Street, where tech outperformed, whilst the US jobs reports this week look set to be delayed after CR votes failed again on Wednesday, as expected.

- ASX 200 was propped up by strength in gold and mining names while defensive sectors lagged, with no reaction seen to the RBA Financial Stability Review, which suggested Australia’s financial system remains well positioned to navigate a period of elevated global uncertainty.

- Nikkei 225 saw upside led by metals and pharma stocks, though gains were capped as the JPY trimmed earlier losses.

- Hang Seng conformed to regional gains and played catch-up to yesterday’s price action during the National Day closure, though momentum was limited by the absence of Stock Connect, with Mainland China remaining shut until next Thursday.

- KOSPI outperformed and hit a fresh record high, overlooking stronger-than-expected CPI, with gains driven by surges in SK Hynix and Samsung Electronics after both firms partnered with OpenAI under the Stargate initiative. Sentiment was also supported by news that South Korea and the US agreed on a basic security framework.

NOTABLE ASIA-PAC HEADLINES

- The RBA’s Financial Stability Review said Australia’s financial system remains well positioned to navigate elevated global uncertainty, with the largest risks to stability coming from abroad, including high and rising government debt in major economies, stretched asset valuations and leverage in global markets, and heightened geopolitical and operational risks. The RBA said most households with mortgages are keeping up with repayments and have built savings buffers, many businesses have established financial buffers, and Australian banks continue to maintain high levels of capital and liquidity. It underscored the importance of maintaining prudent lending standards and strengthening operational resilience via the RBA.

- A BoK official said the significant impact of US tariffs on exports has not yet been observed, but effects are expected to become more apparent next year, according to Reuters.

- BoJ's Uchida says Tankan survey showed positive business sentiment as US tariff outlook recedes; BoJ to raise rates if economic outlook is realised.

DATA RECAP

- Australian Goods/Services Exports (Aug) -7.8% (Prev. 3.30%)

- Australian Goods/Services Imports (Aug) +3.2% (Prev. -1.30%)

- Australian Balance on Goods (Aug) 1.825B vs. Exp. 6.20B (Prev. 7.31B)

- Australian Household Spending MM (Aug) 0.10% (Prev. 0.50%, Rev. 0.40%)

- South Korean CPI Growth YY (Sep) 2.1% vs. Exp. 2.0% (Prev. 1.7%)

- South Korean CPI Growth MM (Sep) 0.5% vs. Exp. 0.4% (Prev. -0.1%)

- South Korean Current Account Bal NSA (Aug) 9.15B (Prev. 10.78B, Rev. 10.78B)