US Opening News: Yen weakens after Takaichi, Euro hit by Lecornu's resignation.

06 Oct 2025, 11:35 by Newsquawk Desk

- Japan’s ruling LDP elected Sanae Takaichi as its leader, who is set to become Japan’s first female PM; Nikkei 225 +4.7%, JPY sinks.

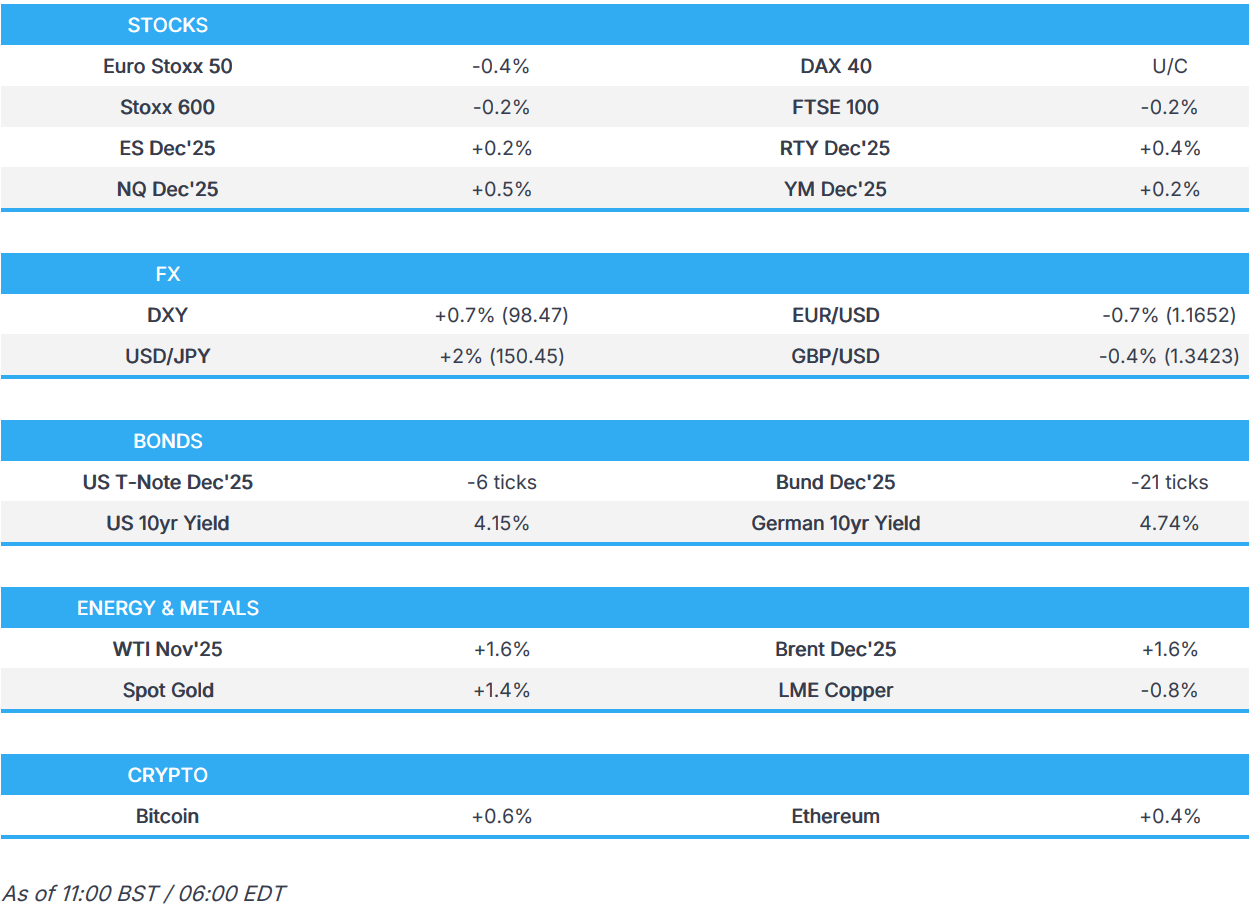

- European bourses opened modestly lower and then took a hit following French PM Lecornu's decision to resign; CAC 40 -1.6%. US equity futures are modestly firmer across the board.

- USD has been boosted as JPY ponders looser fiscal/monetary mix and EUR hit by French political risk.

- 10yr JGBs soared then faltered after Takaichi while OATs were sold after Lecornu resigned.

- Crude benchmarks gain after OPEC+ producers agreed to a modest production increase of 137k bpd in November.

- Looking ahead, US Employment Trends (Sep), New Zealand NZIER (Q3), Speakers including BoE’s Bailey, ECB’s Lagarde, Earnings from Constellation Brands.

TARIFFS/TRADE

- EU is pushing a new AI strategy to cut its tech reliance on the US and China, according to FT.

- Japan will expand the scope of anti-dumping duties to include indirect exports via third countries as China's overproduction continues to hurt domestic industries, according to Nikkei.

- Mexican President Sheinbaum said she will present advances in made-in-Mexico tech EV, semiconductors, satellite and drone projects in the coming weeks, while she is confident, they will reach favourable agreements with the US and all nations worldwide regarding trade relations.

LDP ELECTION

- Japan’s ruling LDP elected Sanae Takaichi as its leader, who is set to become Japan’s first female PM.

- Japan’s newly elected LDP President Takaichi said they need speedy support for weak small- and medium-sized companies to help with wage growth, while she added that support is also needed for the farm sector, and urgent help is needed for the medical and nursing care sectors. Takaichi said one policy option is to increase subsidies to local governments and that she wants to submit a bill to abolish the extra gasoline tax and lower diesel fuel costs during the next parliament. Takaichi also said she won’t rule out lowering the consumption tax as an option and that they will honour the bilateral agreement made with the US. Furthermore, she noted that the government and BoJ need to be aligned on economic policy, while she added they will closely communicate with the BoJ until demand-led economic growth is achieved and wants to carefully consider whether the current government-BoJ accord is most appropriate.

- Credit Agricole Chief Japan Economist Aida, who is widely considered as a close advisor to LDP's Takaichi, said in a note on Saturday that Takaichi will likely tolerate another 25bps BoJ rate hike by January next year if the economy is in firm shape. Such a move would be on condition that the BoJ maintains relatively loose monetary policy with no further rate hikes likely until 2027.

EUROPEAN TRADE

EQUITIES

- European bourses (-0.2%) opened mostly and modestly in the red, but then took a leg lower following news that French PM Lecornu resigned - this downside has since pared a touch.

- The CAC 40 currently trades towards session lows and down by around 1.9%. At present, it is unclear why the PM decided to resign, but it comes after recent cabinet appointments received criticism from opposing parties. The outgoing PM is currently on the wires, and we remain attentive for any reasoning for his decision – thereafter, the spotlight shifts to Macron to see if he a) decides to appoint a new PM, b) calls legislative elections, c) resigns – though in the past he has made it clear that he intends to see out his term. The National Rally said, "Macron must now choose: dissolution or resignation", via France 24.

- European sectors hold a negative bias, with only a handful of industries managing to hold in the green. Energy tops the pile, with names boosted by strength in underlying oil prices. Telecoms follows in second spot, with Technology completing the top three. For the latter, ASML (+1.4%) received a PT upgrade at HSBC, now sees EUR 1,018 (prev. 809, currently 893). To the downside, French banks have slipped on the heightening political instability.

- US equity futures (ES +0.2% NQ +0.5% RTY +0.4%) are modestly firmer across the board, with some outperformance in the NQ.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has started the week very much on the front foot after last week's losses, which were driven by a combination of uncertainty surrounding the government shutdown and softening labour market metrics. There hasn't been a great deal of change in the US macro narrative with the US government still shut and the Trump administration stating that mass layoffs of federal workers will begin if President Trump sees that talks are going nowhere. Instead, today's upside in the USD is driven more by the weakness in the JPY and EUR. DXY has ventured as high as 98.39 with the next upside target coming via the 26th September peak at 98.53.

- EUR/USD has slipped onto a 1.16 handle and below its 50DMA at 1.1680 as French political risk returns with a vengeance. Over the weekend, appointments to French PM Lecornu's cabinet were met with stark objections from opposition parties with National Rally leader Bardella stating that the cabinet failed to break with the past. Earlier today, the Socialist Party leaders stated he couldn't see how his party would not be in a position to vote against the government, given that the appointments failed to show a clear change in direction for the government. The political uncertainty saw the GE/FR spread hit its widest level since January with the move subsequently exacerbated (to 87bps) by the recent decision by Lecornu to resign. The next downside target for EUR/USD comes via the 25th September low at 1.1645.

- JPY is the standout laggard across the majors following the LDP leadership election win by Abe-protege Sanae Takaichi. Her victory has been viewed as a combination of looser fiscal policy and delayed BoJ rate hikes, which have triggered a notable steepening of the Japanese curve. Accordingly, markets have scaled back BoJ rate hike bets with money markets pricing around a 75% likelihood that the central bank will remain on hold in the October 30th meeting and just a 48% chance of a 25bps hike by December vs. 68% probability on Friday. Interestingly, Credit Agricole Chief Japan Economist Aida, who is widely considered as a close advisor to LDP's Takaichi, said in a note on Saturday that Takaichi will likely "tolerate" another 25bps BoJ rate hike by January next year if the economy is in firm shape. 150.43 is the high watermark for USD/JPY thus far with the next upside target coming via the 1st August high at 150.91.

- GBP is softer vs. the USD but firmer vs. the EUR. It remains the case that aside from ongoing angst in the run-up to the November 26th budget, incremental macro drivers for the UK are lacking, and this could remain the case with the domestic data slate light this week. Over the weekend, The Times reported that the UK economy could be on shakier ground than initially assumed amid a "chunky" revision to ONS data, which has increased doubts about how much households have been saving. Cable has slipped below Friday's 1.3429 trough but is holding above the 2nd October low at 1.3400.

- Both antipodeans are softer vs. the USD but to a lesser extent than most peers. For NZD, focus this week is on Wednesday's RBNZ rate decision, which is set to see a reduction in the OCR.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- 10yr JGB futures surged at the opening of trade, lifting from 135.88 to a 136.53 session high. In reaction to the appointment of Takaichi as LDP leader, with the market reacting to her preference towards looser fiscal and monetary policy. Thereafter, the 10yr JGB pulled back and reverted to below Friday’s close, hitting a 135.72 low with downside of just over 15 ticks at most on the session. A move that occurred as the Japanese curve, led by the ultra-long end, began to steepen as markets took the view that Takaichi’s appointment will delay BoJ tightening and policy normalisation, but not indefinitely.

- OATs were under pressure from the start of trade given the weekend updates by President Macron and PM Lecornu. Specifically, they announced a cabinet that was regarded as being a continuation of recent attempts, with Lescure set to be the new Finance Minister and Le Maire as Defence Minister. Since, PM Lecornu has presented his resignation to President Macron. A resignation that sent OATs to a 120.61 low with downside of just under a full point at worst. As such, the OAT-Bund 10yr yield spread widened to a 88.2bps peak for the session, notching a fresh YTD best and approaching the 90bps 2024 high.

- USTs are under modest pressure this morning but within recent ranges. Down to a 112-13+ base, just above last week’s 112-08+ trough. For the most part, the debt market is focussed on above updates initially from Japan but since from France. Ahead, the US docket is a light one on account of the ongoing shutdown, though the Conference Board will still be releasing its Employment Trends Index; a figure that declined in August to 106.41, from a downwardly revised 107.13 in July, to its lowest level since early 2021.

- Bunds began the morning under modest pressure, reflecting the price action seen across the fixed income space in light of the pronounced turnaround seen in JGBs by then. Thereafter, the complex derived a bit of a haven bid on the resignation of French PM Lecornu, lifting to a 128.76 peak with gains of nine ticks at best. However, this proved fleeting, and Bunds have since reverted back to pre-Lecornu levels of c. 128.46.

- Gilts are lagging Bunds and USTs but faring better than OATs. Gapped lower by 22 ticks and then slipped 23 more to a 90.51 low just before the French PM resigned, then seeing some, relative, allure over the next 20/30 minutes before falling back towards session lows. Pressure for the UK comes as we count down to the Autumn Budget. Updates over the weekend include a report in The Times that the domestic economy could be on shakier ground than initially assumed, as a "chunky" revision to ONS data has increased doubts about how much households have been saving. Next up, BoE's Bailey.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks have pared back some of last week’s losses following OPEC+ meeting where the group agreed to raise production by 137k, which is seen as a modest hike compared to the 500k bpd hike reported last week. Benchmarks gapped higher and extended to a peak of USD 62.04/bbl and USD 65.71/bbl in WTI and Brent respectively before oscillating in a c. USD 0.60/bbl range.

- Spot gold continues to extend new ATHs, reaching USD 3950/oz, as growing fiscal concerns in major economies and political concerns in the US add to the momentum of the “debasement trade”. Thus far, XAU has reached a peak of USD 3950/oz before pulling back to USD 3940/oz. Markets await updates on the US government shutdown.

- Base metals briefly extended on last week’s gains before reversing lower amid lack of newsflow, with China still away on holiday. 3M LME Copper extended to USD 10.8k/t early in the APAC session before dipping to a low of USD 10.34k/t. Base metals are being weighed on as Indonesia continues to crack down on illegal mining, with the country handing over six seized tin smelters to state miner PT Timah.

- Eight OPEC+ members agreed to raise oil production by 137k bpd in November, citing a steady economic outlook and current healthy market fundamentals, while they will meet next on November 2nd.

- Qatar set the November marine crude Official Selling Price at Oman/Dubai plus USD 2.00/bbl and land crude OSP at Oman/Dubai plus USD 2.05/bbl.

- Shell (SHEL LN) said US President Trump’s attacks on wind projects harm investment in the US and the decision to halt fully permitted offshore wind energy projects is very damaging to investment, according to FT.

- Saudi Arabia sets new November Arab light Crude oil OSP to NW Europe at plus USD 1.35/bbl to ice Brent settlement via Aramco. They've also set the November crude oil OSP to the USA at plus USD 3.70/bbl.

- Goldman Sachs open a trade recommendation to short Dec 2026 LME Aluminium contract Currently trading at USD 2650/t, 17% above Dec 2026 price forecast.

- Goldman Sachs lifts 2026 copper forecast to USD 10.5/t from USD 10k/t. Believes that copper prices are likely to remain above USD 10k following the Grasberg outage. Expects global copper market to move into deficit by the end of the decade and this should lift copper prices to beyond USD 11k/t from 2028.

- UBS says oil demand has likely peaked for 2025, should gradually fall in the months ahead. Expects Brent to remain in a USD 60-70/bbl band. While the OPEC+ production increase was 137k BPD for November, estimate the actual volume of additions will be only 60-70k BPD.

- Chevron (CVX) says that the Co. will be making operational adjustments to support the continued safe and reliable operation of the facility.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU Retail Sales MM (Aug) 0.1% vs. Exp. 0.1% (Prev. -0.5%, Rev. -0.4%); Retail Sales YY (Aug) 1.0% (Prev. 2.2%, Rev. 2.1%)

- EU Sentix Index (Oct) -5.4 vs. Exp. -8.5 (Prev. -9.2)

- EU HCOB Construction PMI (Sep) 46.0 (Prev. 46.7)

- French HCOB Construction PMI (Sep) 42.9 (Prev. 46.7)

- German HCOB Construction PMI (Sep) 46.2 (Prev. 46)

- Italian HCOB Construction PMI (Sep) 49.8 (Prev. 47.7)

- UK S&P Global Construction PMI (Sep) 46.2 (Prev. 45.5)

NOTABLE EUROPEAN HEADLINES

- French PM Lecornu has resigned, presented his resignation to President Macron.

- French far-right National Rally (RN) Bardella says they are very close to position of voting out government.

- Roland Lescure is set to be named the new French Finance Minister and Bruno Le Maire is set to be appointed as the new French Defence Minister, according to BFM Television.

- French National Rally leader Bardella said the new PM Lecornu cabinet fails to break with the past, while a French socialist party official said the party will vote against the new government if there is no change in policies.

- French Socialist Party (PS) leader Faure says there's a feeling of consternation following the new governments appointment; cannot see how the PS would not be in position to vote against the government.

- Czech billionaire Andrej Babis’s populist ANO party won the parliamentary election, although it failed to achieve an overall majority with just under 35% of the vote to win 80 seats in the 200-seat lower house, while he is seeking an agreement with two smaller groups, which are the populist Motorists and the anti-migration Freedom and Direct Democracy (SPD).

- The UK economy could be on shakier ground than initially assumed amid a "chunky" revision to ONS data has increased doubts about how much households have been saving, according to The Times.

- ECB's de Guindos says inflation risks are balanced; consumption has growth less than expected.

- ECB's Lane reiterates a "data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance, with no-precommitment to a particular rate path". "In particular, our interest rate decisions will be based on our assessment of the inflation outlook and the risks surrounding it, in light of the incoming economic and financial data, as well as the dynamics of underlying inflation and the strength of monetary policy transmission."

- ECB's Pereira says that policy is entering a period of greater normalcy

NOTABLE US HEADLINES

- US President Trump said Democrats are causing the shutdown and possible layoffs, while NEC Director Hassett separately commented that mass layoffs of federal workers will begin if President Trump sees that shutdown talks are going nowhere.

- US House Republican leaders told members that they plan to stay away from Washington, D.C. during the government shutdown but are ready to get back to work as soon as Senate Democrats reopen the government.

- US President Trump called for big US homebuilders to start building homes and said they’re sitting on 2mln empty lots, while he is asking Fannie Mae and Freddie Mac to get big homebuilders going and help restore the 'American Dream'.

- US President Trump authorised the deployment of 300 National Guard troops to Illinois despite the objections of state officials, including Governor Pritzker.

- US Judge temporarily blocked the Trump administration from sending California National Guard troops to Portland, Oregon, and blocked the administration from sending Texas or other states' National Guard to Oregon. It was also reported that California Governor Newsom will sue the Trump administration for sending California National Guard personnel to Oregon.

- COVID-19 Stratus variant replaced the Nimbus variant as the most prevalent strain across the US, with the CDC suggesting some regions of the country are experiencing “very high” COVID-19 activity including Nevada, Utah, Connecticut and Delaware.

- On the US gov't shutdown, Punchbowl surmises that as it stands "There’s no deal in sight to end the crisis". "The notion of Senate Minority Leader Chuck Schumer folding at this point seems very unlikely. Yet if you’re Schumer, you’re watching very closely how a handful of Democratic senators are posturing themselves as the shutdown impacts begin to accumulate". "One Democratic senator told us that some colleagues who want to fold could justify doing so by pointing to the fact that the GOP stopgap funding bill gives Democrats another leverage point in just six weeks. However, this argument would cut against the party’s messaging..." with reference to the Obamacare expiry.

GEOPOLITICS

MIDDLE EAST

- Israel and Hamas are set to begin mediated negotiations on Monday in Egypt after US President Trump hailed Hamas’s offer to release all hostages, according to Bloomberg.

- Israeli government spokeswoman confirmed negotiations for the release of hostages are expected to begin on Monday and stated there is no ceasefire in place in Gaza, but there has been a temporary halt in certain bombings, while she added the military can continue to act in Gaza for defensive purposes.

- Israeli military spokesperson issued a warning for residents of Gaza City on Saturday morning and called on them to avoid returning north, while the spokesperson added that Gaza City remains a dangerous combat zone. It was separately reported by an Al Arabiya correspondent that violent explosions were heard in the Gaza Strip on Sunday.

- US President Trump posted that after negotiations, Israel has agreed to an initial withdrawal line which has been shown to, and shared with Hamas, while he added that when Hamas confirms, a ceasefire will be immediately effective and a hostages and prisoner exchange will begin.

- US President Trump posted that there have been very positive discussions with Hamas and countries from all over the World (Arab, Muslim, and everyone else) this weekend, to release the hostages and end the war in Gaza but, more importantly, finally have long sought peace in the Middle East. Trump added that these talks have been very successful and are proceeding rapidly, while the technical teams will again meet Monday, in Egypt, to work through and clarify the final details, while he was told that the first phase should be completed this week, and he is asking everyone to move fast.

- US President told CNN that Hamas will face ‘complete obliteration’ if it refuses to cede power in Gaza and noted that Israeli PM Netanyahu is on board with ending the bombing in Gaza.

- US Secretary of State Rubio said that meetings are taking place on the Israel-Hamas deal and that Hamas agreed in principle to what happens after the war, while he responded ‘not yet’ and that some work remains to be done when asked if this is the end of the war in Gaza. Rubio suggested the second phase of discussing disarmament and demobilisation will be difficult and stated they will know very quickly if Hamas is serious. Furthermore, he said they are the closest they have been in a very long time to having no hostages held by Hamas, but added that no one can say it is a 100% guarantee.

RUSSIA-UKRAINE

- US President Trump said Russian President Putin’s offer last month to voluntarily maintain limits on deployed nuclear weapons sounds like a good idea.

- Russian President Putin warned that the possible supply of Tomahawk missiles to Ukraine will ruin the Russia-US relationship.

- Russia conducted a massive airstrike against targets across Ukraine using missiles and drones which killed at least five people and injured several others, according to Bloomberg. Furthermore, Russia’s Defence Ministry said Russian forces captured Kuzminovka in Ukraine’s Donetsk region and carried out a massive strike on Ukrainian military-industrial enterprises, as well as gas and energy infrastructure facilities.

- Ukrainian President Zelensky said on Sunday morning that Russia launched over 50 missiles and almost 500 drones in an overnight attack on Ukraine.

- Ukraine’s Energy Minister said the Russian overnight air attack damaged energy infrastructure in Ukraine’s Zaporizhzhia, Sumy and Chernihiv regions. It was also reported that a Russian strike hit a passenger train in Ukraine’s Sumy region, causing casualties.

- Russia's Kremlin says US President Trump's language on nuclear limits provide some ground for optimism.

- Russia's Kremlin says that there is no reason to blame Russia for the drone sightings in Europe.

OTHER

- US President Trump’s administration directed US diplomats to lobby against a UN resolution calling for Washington to lift its embargo on Cuba, while the US will tell countries that Cuba is actively supporting Russia’s invasion of Ukraine, according to a diplomatic cable cited by Reuters.

- US President Trump said the US hit another boat on Saturday off Venezuela and that the US will have to start looking at drug trafficking by land. In relevant news, US Defense Secretary Hegseth said he has every authorisation needed for Caribbean strikes against vessels allegedly carrying illegal drugs off the coast of Venezuela.

- North Korean leader Kim said Pyongyang allocated strategic assets to respond to the buildup of US military forces in Korea, while he also said they will develop additional military measures, according to KCNA.

CRYPTO

- Bitcoin and Ethereum are modestly firmer today, taking a breather from some of the upside seen over the weekend.

APAC TRADE

- APAC stocks began the week mixed amid several holiday closures throughout the week and the ongoing US government shutdown, while Japanese markets rallied on hopes of fiscal loosening and a delay to BoJ policy normalisation following Sanae Takaichi's LDP leadership victory, which sets her on course to become Japan's first female PM.

- ASX 200 failed to sustain early marginal gains and retreated to back beneath the 9,000 level as losses in tech, healthcare, and the consumer sectors offset the strength in the commodity-related industries.

- Nikkei 225 rallied to fresh record highs above the 48,000 level as the JPY weakened amid expectations of fiscal support and a potential delay to BoJ policy normalisation after the LDP leadership election victory by Abe-protege Takaichi.

- Hang Seng declined amid the absence of mainland participants for most of the week due to the National Day 'Golden Week' holiday and with underperformance in casino stocks following the recent flooding from Typhoon Matmo.

NOTABLE ASIA-PAC HEADLINES

- Chinese Foreign Minister Wang Yi will visit Italy and hold the 12th joint meeting of the China-Italy government committee, and will visit Switzerland for a 4th round of the China-Switzerland foreign ministers-level strategic dialogue.

- NVIDIA’s (NVDA) major server production partner Hon Hai (2317 TT) reported quarterly sales rose 11% to TWD 2.06tln which reportedly signals healthy demand for AI infrastructure, according to Bloomberg.

- Indonesia revoked its TikTok licence suspension after the social media platform submitted data that the Indonesian government requested, according to Bloomberg.

- Japan and the US are arranging a US President Trump-PM summit for October 28, via Kyodo.