European Opening News: RBNZ opts for 50bps cut, gold breaches USD 4000/oz for the first time

08 Oct 2025, 06:52 by Newsquawk Desk

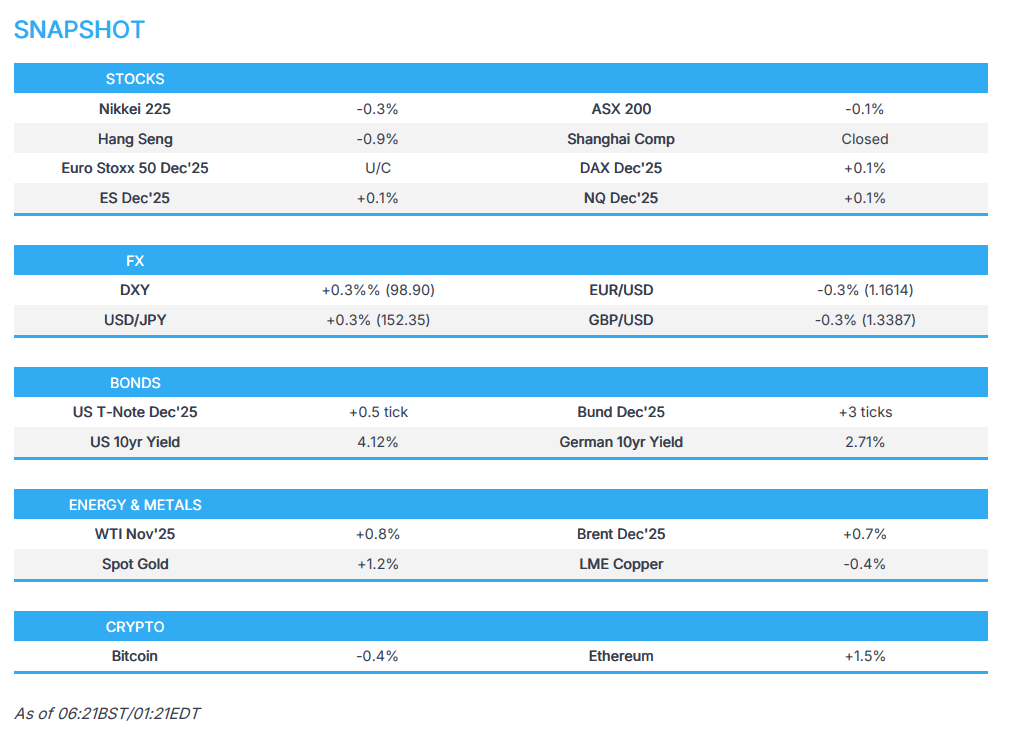

- APAC stocks trade mixed with demand hampered following the negative handover from the US; European futures flat.

- RBNZ cut rates by 50bps and kept the door open to further rate cuts.

- US President Trump said a lot of things will be eliminated due to the shutdown, and he will tell us about the eliminated jobs in four or five days.

- USD remains on the front foot, NZD lags post-RBNZ, JPY digests soft real cash earnings data.

- Spot gold continued its advances, in which spot prices climbed above the USD 4,000/oz level.

- Looking ahead, highlights include German Industrial Output (Aug), Swedish CPIF Flash (Sep), NBP Policy Announcements, FOMC Minutes (Sep), BoE’s Pill, ECB’s Elderson & Lagarde, Fed’s Musalem, Barr, Goolsbee & Kashkari, Supply from UK, Germany & US.

SNAPSHOT

US TRADE

EQUITIES

- US stocks were sold on Tuesday, with weakness seen in the wake of reports in The Information that internal data shows the financial challenge of renting out NVIDIA (NVDA) chips and its impact on margins. This hit the large-cap tech sectors and weighed on indices before then hovering into the close, while Oracle sold off aggressively but closed off lows as several analysts were out defending the Co. and described it as a buying opportunity. The downside in equities resulted in upside in T-notes, while gold had been pushing higher anyway, with futures hitting USD 4,000/oz and spot prices trailing to just beneath the psychological milestone.

- SPX -0.38% at 6,715, NDX -0.55% at 24,840, DJI -0.20% at 46,603, RUT -1.12% at 2,458.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said he will meet Chinese President Xi in a few weeks in South Korea.

- Canadian PM Carney said the US and Canada have to come to an agreement that works in areas where they compete.

- US-Canada trade talks were successful, positive and substantial, according to the Canadian government's minister for US trade, LeBlanc, who stated that principal areas for potential US-Canada trade deals would be in the steel, aluminium and energy sectors, while he hopes to finalise deals in these sectors swiftly before extending agreements to other sectors.

- US House Committee said Applied Materials (AMAT), KLA Corp (KLAC), Lam Research (LRCX), ASML (ASML NA), and Tokyo Electron (8035 JT) fueled China chip production, following a months-long investigation, while it noted several recommendations, including aligning allied, such as Dutch and Japanese, export controls with US restrictions, so the Netherlands and Japan catch up to American controls and enforcement. It also recommended expanding country-wide controls for the PRC to make diversion more difficult, widening the list of restricted entities and prohibiting all allied manufacturers from selling to additional Chinese military entities.

- Norway’s Foreign Minister said Norway is exempt from the European Commission proposal on higher tariffs and lower quotas on steel in the EU.

NOTABLE HEADLINES

- Fed Governor Miran (voter) said the neutral rate has been buffeted by huge, unusual population shocks, and monetary policy needs to ease to get ahead of a shift down in the neutral rate, while he is optimistic on growth and stated the drag from uncertainty is abating. Miran also noted that housing matters more for the economy than the stock market, and that shelter is the key driver of inflation, as well as stated that he doesn't want to move the goal posts on the inflation target. Furthermore, he said in the longer run, it is hard to micromanage to an exact level of inflation, and that it is important for the Fed to set monetary policy outside of the political cycle.

- Fed's Kashkari (2026 voter) said it is too soon to know if inflation will be sticky from tariffs and noted that data is sending some stagflation signals, while he is bullish on labour and said workers have a very important role in the economy. Furthermore, he is not convinced that a few rate cuts will translate to lower mortgage rates and said if the Fed drastically lowers rates, they would expect the economy to have a burst of high inflation, as well as noted that the FOMC is committed to making decisions based on data and analysis, not political considerations.

- US President Trump said a lot of things will be eliminated due to the shutdown, and he will tell us about the eliminated jobs in four or five days.

- US President Trump said he doesn't know who to speak to with Democrats as they have no leader, while he added that AOC is not in a position to negotiate and Schumer is incapable of making a deal to end the shutdown.

- US House Democratic Leader Jeffries stated that a one-year extension of Obamacare is a 'non-starter' for reopening the government.

- US Senate leaders were reportedly trying to lock in votes on Tuesday evening with a variety of options, including the noms bloc, privileged resolutions (maybe Canada tariff disapproval), and the duelling CRs again, according to Punchbowl.

- US President Trump's administration has pushed back its plans to roll out economic support for farmers this week due to the government shutdown, according to four people familiar with the talks cited by POLITICO. Furthermore, officials were said to have readied nearly USD 13bln from an internal USDA fund, although there is no final decision on how much will be used for farm aid, or when.

- US President Trump's administration is reportedly mulling cancelling an additional USD 12bln in funding for clean energy projects beyond what was announced last week, according to Semafor.

APAC TRADE

EQUITIES

- APAC stocks traded mixed with demand hampered following the negative handover from the US, where stocks snapped a 7-day win streak as small caps underperformed and with sentiment weighed on by AI-profitability concerns.

- ASX 200 was rangebound as gains in healthcare and the top-weighted financial industry were offset by underperformance in Tech and Consumer sectors.

- Nikkei 225 lacked conviction and oscillated around the 48,000 level amid a weaker currency and soft wages data.

- Hang Seng retreated on return from the holiday closure with tech stocks heavily represented in the list of worst performers, while mainland participants were still away but are set to return from the National Day Golden Week celebrations tomorrow.

- US equity futures (ES +0.1%, NQ +0.1%) eked marginal gains in an attempt to nurse the prior day's tech-related selling pressure.

- European equity futures indicate a contained cash market open with Euro Stoxx 50 future flat after the cash market closed with losses of 0.3% on Tuesday.

FX

- DXY extended on gains against its peers despite the continuation of the US government shutdown and absence of US data. Nonetheless, the NY FED SCE saw an uptick in the one-year-ahead and five-year-ahead inflation expectations, while there were several Fed comments including from Miran, who remained optimistic on growth and stated the drag from uncertainty is abating, as well as reiterated calls for easier monetary policy.

- EUR/USD remained pressured amid the firmer greenback and the backdrop of the political uncertainty in France, where National Rally leaders Bardella and Le Pen declined PM Lecornu's invitation to take part in talks.

- GBP/USD gave way to the dollar strength and tested 1.3400 to the downside as newsflow and the data calendar for the UK remained light.

- USD/JPY gained a firmer footing at the 152.00 handle to print its highest level in almost eight months, with the Japanese currency not helped by the softer-than-expected labour cash earnings.

- Antipodeans retreated with NZD underperforming after the RBNZ reverted to the 50bps rate cut moves seen earlier in the current easing cycle to lower the OCR to 2.50% and kept the door open to further rate cuts.

FIXED INCOME

- 10yr UST futures took a breather after gaining yesterday as risk sentiment soured, while the overall results of the 3yr auction stateside were strong but had little impact on prices, as a 10yr auction looms and with FOMC Minutes also on the horizon.

- Bund futures lacked firm direction after recent whipsawing, while participants await incoming German Industrial Production data and Bund issuances.

- 10yr JGB futures lingered around post-LDP election lows amid expectations of fiscal loosening and despite softer-than-expected wages data.

COMMODITIES

- Crude futures gained but with further upside capped after mixed private sector inventory data and after the EIA STEO raised its world oil demand forecast for this year but maintained its demand outlook for 2026.

- US Private Energy Inventories Data (bbls) Crude +2.8mln (exp. +1.9mln), Distillate -1.8mln (exp. -1.2mln), Gasoline -1.2mln (exp. -0.9mln), Cushing -1.2mln.

- EIA STEO raised its 2025 world oil demand forecast but maintained the 2026 demand forecast, while the world production forecast was raised for 2025 and 2026.

- UAE's ADNOC set November Murban crude OSP at USD 70.22/bbl (prev. 70.10 in October).

- Spot gold continued its advances in which spot prices climbed above the USD 4,000/oz level to track futures which had already breached the aforementioned key milestone during US trade.

- Copper futures were lacklustre amid the flimsy risk appetite and as its largest buyer, China, remained absent from the market.

CRYPTO

- Bitcoin lacked conviction with prices ultimately returning to flat territory after trading on both sides of the USD 122k level.

NOTABLE ASIA-PAC HEADLINES

- RBNZ cut the OCR by 50bps to 2.50% vs mixed views between a 25bps and 50bps cut, while the committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2% target mid-point in the medium term. RBNZ said higher near-term inflation could prove to be more persistent and that with spare capacity in the economy, inflation is expected to return to around the 2% target mid-point over the first half of 2026, but noted upside and downside risks to the inflation outlook. RBNZ Minutes revealed that the committee discussed the options of reducing the OCR by 25bps or by 50bps at the meeting, while it stated that the case for reducing the OCR by 50 basis points emphasised prolonged spare capacity and the associated downside risk to medium-term activity and inflation.

DATA RECAP

- Japanese Overall Labour Cash Earnings (Aug) 1.5% vs. Exp. 2.6% (Prev. 4.1%, Rev. 3.4%)

- Japanese Real Cash Earnings YY (Aug) -1.4% vs Exp. -0.5% (Prev. 0.5%, Rev. -0.2%)

GEOPOLITICS

MIDDLE EAST

- US President Trump met with his top national security team to discuss the progress of the Gaza deal negotiations prior to the departure of envoys Steve Witkoff and Jared Kushner to Egypt, according to Axios citing sources.

RUSSIA-UKRAINE

- Russian President Putin said Ukraine is attempting to strike deep into Russian territory and is targeting civilian objects, while he added that this will not help Ukraine.

EU/UK

NOTABLE HEADLINES

- UK Industry Minister McDonald said they will always defend the critical steel industry which is why they are pushing the European Commission for urgent clarification of the impact of this move on the UK.

- ECB President Lagarde said all EU institutions are watching France and hopes that a rate path can be found for respecting its international commitments, including on the budget.

- ECB's Rehn has warned there is a risk that inflation slows below the ECB's 2% inflation target, according to Bloomberg, citing the Karon Grilli podcast. There are downside inflation risks in sight over the next couple of years; cites EUR strength, stabilisation of wages and services inflation.